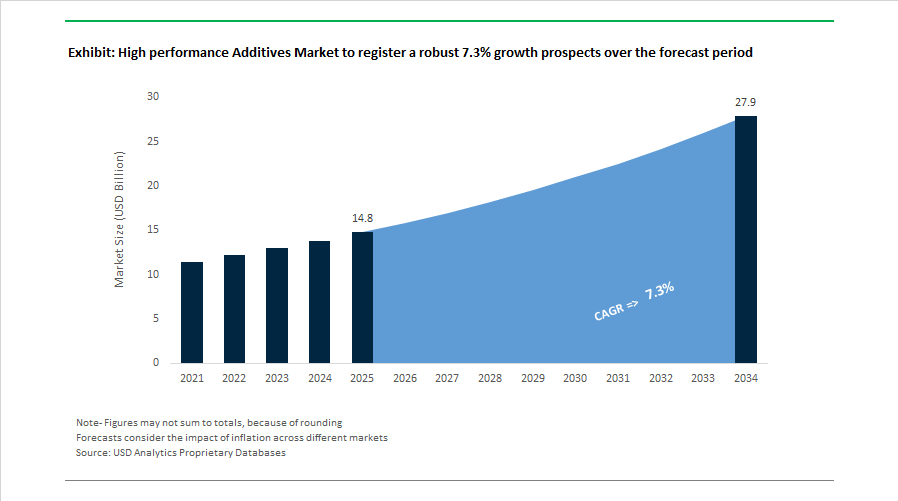

High Performance Additives Market to Reach $27.9 Billion by 2034 at 7.3% CAGR Driven by Sustainable Polymer Stabilization, Flame Retardants, and Advanced Dispersant Technologies

The High Performance Additives Market is projected to grow from $14.8 billion in 2025 to $27.9 billion by 2034, registering a CAGR of 7.3%. Expansion is fueled by accelerating demand for advanced polymer stabilizers, dispersants, flame retardants, lubricant additives, antioxidant systems, and specialty intermediates that enhance thermal stability, electrical insulation, UV resistance, and mechanical performance in automotive, electronics, aerospace, coatings, and energy infrastructure applications. Market momentum is closely aligned with electrification trends, recycled polymer processing, halogen-free regulatory mandates, and carbon-reduction strategies embedded across global manufacturing value chains.

In September 2025, Songwon Industrial Co., Ltd. introduced XP2121 and SONGNOX® PQ at K 2025, targeting stabilization of recycled LDPE and polypropylene streams to enable higher-value reuse. In October 2025 at the same trade fair, Clariant unveiled AddWorks™ titanium-based catalyst solutions for polyester production, positioning antimony-free systems as a strategic alternative following China’s 2024 export restrictions on antimony. In November 2025, BASF commissioned a new high-performance dispersant production line at its Nanjing facility using Controlled Free Radical Polymerization technology. The plant supports low-carbon automotive and industrial coatings transformation in Asia. In 2025, Afton Chemical launched next-generation passenger car engine oil and industrial fluid additives engineered for improved oxidation resistance, deposit control, and hardware durability under electrified drivetrain conditions.

Strategic expansion into flame retardants and energy infrastructure intensified in late 2025 and early 2026. In November 2025, Clariant formed a joint venture with FUHUA to produce phosphorus-based halogen-free flame retardants in China, ramping production through 2026 for electronics and EV applications. In January 2026, CAI Performance Additives launched ST-MCA-H, a nylon flame retardant achieving UL-94 V-0 at 4–5% loading, preserving mechanical integrity in PA6 and PA66 connectors. In early 2026, BASF introduced Irgastab® Cable KV 10, targeting mid- and high-voltage power transmission systems requiring long-term thermal and dielectric endurance. In 2025, NewMarket Corporation committed $100 million to expand ammonium perchlorate production at its AMPAC facility, with completion scheduled for end-2026 to support aerospace and defense materials demand.

Sustainability-driven polymer innovation accelerated into 2026. In January 2026, Evonik Industries launched TROGAMID® R, a transparent polyamide derived from recycled plastics developed with Poliplastic SRL, demonstrating the role of high-performance additives in preserving optical clarity and structural strength in recycled engineering polymers. In January 2026, Evonik also introduced TEGO® Dispers 695 for radiation-curing and solventborne polyurethane inks, enhancing pigment dispersion and color intensity in high-performance printing. In February 2026, ADEKA Corporation established a renewable plastic supply chain with Sony, supplying critical polymer additives to ensure performance compliance in premium electronics. In January 2026, Nouryon recognized BASF Chemical Intermediates as a 2025 Supplier of the Year, underscoring the importance of resilient high-performance additive supply chains in specialty downstream applications.

The High Performance Additives Market is increasingly shaped by halogen-free flame retardant adoption, recycled polymer stabilization chemistry, advanced dispersant technologies, high-voltage cable durability requirements, aerospace propellant intermediates expansion, and carbon-conscious manufacturing strategies. Competitive differentiation is anchored in polymer lifecycle optimization, electrification-ready additive systems, controlled radical polymerization platforms, and vertically integrated specialty chemical supply networks serving high-growth automotive, electronics, coatings, and defense sectors.

High-Performance Additives Market Trends and Opportunities

Vertical Integration of High-Purity Additives for EV Battery Supply Chains

The rapid scale-up of electric vehicle and grid-scale energy storage manufacturing is transforming high-performance additives from commoditized formulation aids into strategic battery-enabling materials. Specialty chemical producers are increasingly integrating upstream into high-purity electrolyte additives, conductive dispersants, and polymer modifiers that directly influence Solid Electrolyte Interphase stability, fast-charging capability, and long-cycle durability in next-generation lithium-ion cells. This vertical integration trend reflects the tightening performance window for 800V and higher battery architectures, where even trace impurities can reduce cycle life or compromise safety.

Capacity expansion initiatives underline the strategic importance of this segment. In March 2024, Orbia Fluor & Energy Materials significantly expanded its Madison, Wisconsin facility, tripling output of custom electrolyte additives designed for defense-grade and commercial EV batteries. These investments are aligned with U.S. policy objectives to localize battery supply chains and reduce dependence on imported high-purity chemicals. Parallel to capacity expansion, cross-industry technology partnerships are accelerating additive adoption. In December 2025, Arkema entered a strategic collaboration with Semcorp to integrate its PVDF and acrylic-based additives into advanced battery separators, improving electrolyte wetting and thermal stability. Industry roadmaps supported by DOE-funded studies indicate that flame-retardant and high-dielectric electrolyte additives will represent the fastest-growing functional class through 2034, driven by stricter safety requirements for stationary energy storage and fast-charging EV platforms.

Advanced Additive Packages Enabling High-Speed Circular Packaging Films

Global commitments to fully recyclable mono-material packaging are reshaping additive demand in polyolefin films. As brand owners move away from multilayer laminates, high-performance additive packages are becoming essential to bridge the processing and performance gap between mono-material PE or PP films and traditional barrier structures. These additives enable recycled-content and mono-material films to maintain clarity, toughness, and machinability on high-speed converting and filling lines without contaminating the recycling stream.

A critical inflection point in this trend is the transition away from fluoropolymer-based processing aids. In September 2025, Dow launched a silicone-based polymer processing aid that eliminates melt fracture and die buildup in LLDPE films while avoiding PFAS chemistries under regulatory scrutiny. At the same time, polyolefin elastomer additives showcased at K 2025 demonstrated that mono-PE and mono-PP structures can achieve puncture resistance and optical clarity at line speeds exceeding 400 meters per minute, matching the productivity of legacy laminate systems. Clarifying additives are further expanding application scope. During 2024 and 2025, clarified polypropylene grades increasingly replaced PET in hot-fill and food packaging applications, benefiting from improved heat resistance, lower moisture permeability, and reduced carbon footprint.

Non-PFAS Repellent Additives for Textiles and Food-Contact Applications

The global shift toward PFAS-free consumer products has moved decisively into the enforcement phase, creating a substantial innovation opportunity for non-fluorinated water- and oil-repellent additives. Regulatory bans enacted from January 2025 onward across multiple U.S. states, including California and Maine, now prohibit intentionally added PFAS in textiles, cookware, and food-contact materials. These measures are forcing a full-scale reformulation of durable water repellent systems across apparel, upholstery, medical textiles, and packaging.

In response, additive developers are introducing novel surface-modification chemistries that rely on physical barrier effects rather than fluorinated chains. Commercial launches in 2025 demonstrated that micro-rough polymer architectures can deliver durable stain resistance suitable for technical textiles and healthcare environments. The medical and hygiene segment represents a particularly attractive niche, as hospitals and regulators increasingly demand fluid-repellent performance aligned with evolving REACH restrictions. PFAS-free additives introduced in late 2025 for surgical gowns and drapes illustrate how regulatory pressure is accelerating premium, high-margin innovation in nonwoven and protective textile markets.

High-Solid Rheology Modifiers for Waterborne and Low-VOC Coatings

The transition toward waterborne architectural and industrial coatings is driving sustained demand for advanced rheology modifiers capable of delivering sag resistance, leveling, and spray stability under high-solids, low-VOC conditions. Organic rheology modifiers such as HEUR and HASE have become indispensable formulation tools, accounting for roughly two-thirds of the organic segment by 2024. These additives allow coatings to maintain viscosity control across shear conditions while supporting regulatory compliance with increasingly strict VOC limits.

Sustainability considerations are amplifying this opportunity. Leading suppliers including Evonik and BASF are introducing mass-balanced and bio-based wetting and defoaming agents to meet the growing demand for eco-labeled paints. Product launches in early 2025 targeting green-certified architectural coatings indicate rising acceptance of additives that combine high-performance rheology control with reduced carbon intensity. As construction markets recover and retrofit activity accelerates, these high-solid, waterborne-compatible additives are positioned as critical enablers of next-generation coating systems that balance performance, compliance, and sustainability.

High Performance Additives Market Share and Segmentation Insights

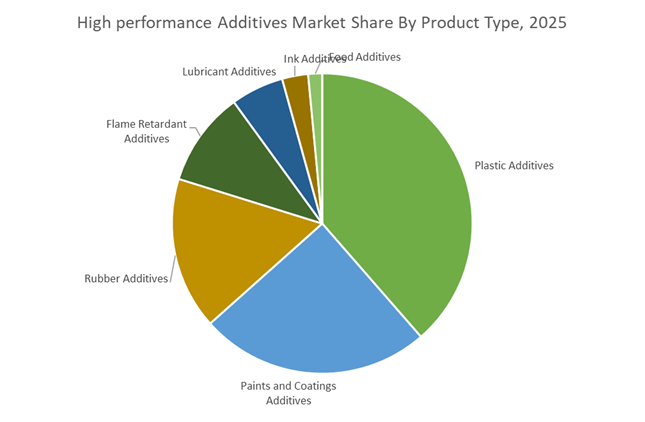

Plastic Additives Lead the High Performance Additives Market Through Polymer Performance Enhancement

Plastic Additives accounted for 38.60% of the High Performance Additives Market share in 2025, making them the largest product category within the advanced additive industry. Plastic additives play a critical role in enhancing the processing efficiency, durability, stability, and functional performance of polymer materials used across multiple industries including packaging, automotive, electronics, and construction. These additives include antioxidants, UV stabilizers, plasticizers, impact modifiers, processing aids, antistatic agents, and slip additives, which enable manufacturers to tailor polymer properties for specific performance requirements. Plastic additives are essential for maintaining polymer integrity during high-temperature processing and long-term exposure to environmental conditions, extending the service life of plastic products in demanding applications. In 2025, the segment is increasingly influenced by the transition toward circular economy plastic systems. Additive manufacturers are developing advanced stabilizer packages that support multiple recycling cycles, polymer compatibility enhancement, and improved recyclate processing stability, allowing recycled polymers to maintain mechanical strength and performance while enabling higher recycled content incorporation in finished plastic products.

Packaging Industry Drives the Largest Demand for High Performance Additives

Packaging represented 32.40% of the High Performance Additives Market share in 2025, making it the leading end-use industry for advanced additive technologies. The packaging sector relies heavily on polymer materials such as polyethylene, polypropylene, PET, and multilayer plastic films, which require specialized additive systems to maintain performance throughout the product lifecycle. Additives are incorporated into packaging materials to provide thermal stabilization during processing, UV protection for shelf-life extension, slip and antiblock properties for efficient film handling, and antistatic protection for dust control. These functionalities are essential for maintaining packaging performance during manufacturing, storage, transportation, and consumer use. In 2025, the packaging sector is undergoing significant transformation due to the increasing adoption of recycled plastic content in packaging materials. Recycled polymers often exhibit degraded molecular structure, reduced mechanical strength, and increased impurity levels, creating challenges for manufacturers. To address these issues, additive producers are developing specialized stabilization packages including advanced antioxidants, chain extenders, and compatibilizers, enabling packaging manufacturers to increase recycled content while preserving product appearance, mechanical integrity, and barrier performance.

Competitive Landscape in High performance Additives Market

BASF SE Scales Dispersant Innovation and Renewable Additive Production

BASF SE maintains global leadership in high performance additives through its Dispersions & Resins division, supplying advanced dispersants and rheology modifiers for automotive coatings and industrial plastics. In November 2025, BASF commissioned a new high-performance dispersant production line in Nanjing utilizing Controlled Free Radical Polymerization technology, improving pigment dispersion efficiency while lowering product carbon footprint. The company’s Luvotix rheology modifiers and Efka dispersants remain industry standards for premium coatings requiring color stability and scratch resistance. Following leadership changes in 2025, BASF accelerated its Green Transformation strategy, targeting 100% renewable energy usage across additive production sites. Its 2025–2026 Automotive Color Trends initiative integrates renewable raw materials and multi-effect pigments, reinforcing its dominance in high-end automotive finishes.

Evonik Industries Expands Specialty Additives for Adhesives and Flow Chemistry

Evonik Industries AG focuses on high-margin specialty additives delivering precision functional performance in coatings, adhesives, pharmaceuticals, and inks. In February 2026, Evonik announced expansion of hydroxyl-terminated polybutadiene production, strengthening supply for high-performance adhesives and sealants. The company previously established POLYVEST ST-E 60 production in Shanghai to serve Asia’s growing demand for specialty elastomers. Its TEGO additives and ACEMATT matting agents remain benchmarks for surface control and gloss management in architectural and industrial coatings. Evonik is also advancing Noblyst F catalysts for continuous flow chemistry, supporting pharmaceutical manufacturing modernization. This Beyond Chemistry strategy emphasizes value-added additives rather than commodity volumes.

Clariant AG Drives Bio-Based and Digitalized Additive Solutions

Clariant AG has streamlined its portfolio toward Adsorbents & Additives, focusing on sustainable, high-margin specialty solutions. The company reported a 17.8% EBITDA margin for FY 2025, reflecting operational efficiencies and a CHF 50 million performance improvement program. Clariant recently secured EU approval for renewable rice bran wax additives in food-contact plastics, strengthening its bio-based polymer additive portfolio. Through its CLARITY digital platform, Clariant enables real-time performance monitoring and optimization of catalysts and additives. The company is accelerating adoption of mass-balance certified raw materials and targeting a 46.9% reduction in Scope 1 and 2 emissions by 2030, reinforcing its sustainability-led differentiation.

Dow Inc. Targets PFAS-Free Processing and Digital Cooling Applications

Dow Inc. is leveraging its global R&D infrastructure to modernize high performance additive systems across coatings, packaging, and electronics. In January 2026, Dow launched Transform to Outperform, a $2 billion EBITDA improvement initiative centered on operational simplification and AI-enabled customer engagement. The company introduced alternatives to fluoropolymer-based polymer processing aids, addressing regulatory scrutiny of PFAS in film packaging applications. Its DALPAD A Plus coalescing agent reduces emissions in coatings by more than 60%, while DOWSIL TC-3080 thermal gel supports advanced high-performance computing and data center cooling. The establishment of a Cooling Science Studio in Shanghai underscores Dow’s focus on electronics thermal management and digitalized additive solutions.

Songwon Industrial Strengthens Circular Polymer Stabilization

Songwon Industrial Co., Ltd. remains a global co-leader in polymer stabilizers, emphasizing additive packages designed for recycled plastics and circular economy integration. In October 2025, the company announced construction of a new One Pack Systems facility in Saudi Arabia to serve Middle Eastern and African markets. Songwon showcased XP2121 stabilizer technology tailored for lower-quality recycled polypropylene and SONGNOX PQ for recycled LDPE and LLDPE films, addressing performance gaps in mechanically recycled materials. Its upstream investment in di-alkylphenol production enhances supply security and cost stability. Songwon actively collaborates with regulatory consortia to anticipate policy shifts, positioning itself as a technical advisory partner for global polymer producers.

Arkema S.A. Advances Bio-Based Polymers and Semiconductor Additives

Arkema S.A. leads in bio-based high performance polymers and specialty additives for aerospace, electronics, and advanced composites. In January 2026, Arkema started up a new Rilsan Clear transparent polyamide unit in Singapore, tripling global capacity for bio-based PA11 materials used in 3D printing and specialty coatings. At SEMICON China 2026, Arkema is showcasing high-purity Kynar PVDF and Zenimid polyimide solutions designed for ultra-pure water and chemical piping in semiconductor fabrication plants. Through its Elium recyclable resin platform and Rilsan PA11, Arkema is promoting circular composites for hydrogen storage and transportation systems. Its high-performance powder coatings and specialty polymers reinforce its leadership in durable, lightweight additive-enabled materials for industrial and medical applications.

China: Industrial Policy Acceleration and Localization of High-End Additives

China’s high performance additives industry is being reshaped by coordinated industrial policy, targeted capital deployment, and a clear push toward domestic substitution of advanced chemical inputs. In September 2025, the Ministry of Industry and Information Technology, together with six other ministries, issued a joint Work Plan for Petrochemical Growth covering 2025–2026. The plan targets average annual added-value growth above 5% for the chemical sector and explicitly prioritizes breakthroughs in high-end polyolefin additives, electronic chemicals, and specialty stabilizers. This policy direction is accelerating investment into antioxidants, light stabilizers, flame retardants, and electronic-grade additives that were previously sourced from overseas suppliers.

Capacity expansion is reinforcing this localization drive. In November 2025, Clariant completed a CHF 100 million expansion at its Daya Bay facility, commissioning a second production line for Exolit OP halogen-free flame retardants. These additives are engineered for the thermal and electrical stress profiles of 800V electric mobility platforms, aligning additive development with China’s rapidly scaling high-voltage EV ecosystem. Parallel investments are under way in polymerization chemistry. Nouryon finalized the scale-up of its organic peroxide site in China, reaching full production in 2025 to support high-performance polymer synthesis used in 5G infrastructure and advanced wire and cable applications. Looking ahead, the MIIT’s “AI plus Petrochemicals” assessment framework for 2026 is compelling additive manufacturers to adopt real-time digital monitoring systems to improve emission control, yield consistency, and process efficiency, embedding digital transformation directly into additive manufacturing operations.

Germany: Circularity, Carbon Contracts, and Additive Innovation Leadership

Germany remains a reference market for high performance additives shaped by sustainability policy, advanced formulation science, and financial instruments that support decarbonization. At the K 2025 trade fair in Düsseldorf, BASF presented its expanded VALERAS portfolio, including Tinuvin NOR 112, a next-generation hindered amine light stabilizer designed to maintain durability under exposure to aggressive agrochemicals. This product positioning reflects rising demand from controlled-environment agriculture and organic greenhouse farming, where material longevity and regulatory compliance intersect.

Policy support is reinforcing these innovation pathways. Preparations for Germany’s 2026 Climate Contracts program are under way, providing carbon contracts for difference to chemical producers investing in carbon-neutral manufacturing routes, including carbon capture, utilization, and storage. This framework directly benefits high performance additive production, which is energy-intensive and increasingly scrutinized under EU climate targets. Circularity is another structural driver. In October 2025, Evonik introduced TEGO CYCLE additives that enable mechanical recycling of contaminated plastics by removing inks and labels during wet processing. To finance its low-carbon and mass-balanced certified material pipeline, Evonik issued a green hybrid bond in September 2025, channeling capital toward advanced additives and sustainable polyamide platforms such as VESTAMID. Germany’s additive ecosystem is therefore evolving at the intersection of regulation, capital markets, and high-value application demand.

United States: Regulatory Realignment and Bio-Based Additive Acceleration

The United States high performance additives industry is undergoing regulatory-driven reformulation and application-led innovation, particularly in food, energy, and aerospace markets. The U.S. Environmental Protection Agency Office of Chemical Safety and Pollution Prevention released its 2025–2026 National Program Guidance, prioritizing chemical safety and accelerating review pathways for high-performance bio-based additives that can replace legacy petrochemical formulations. This guidance is influencing additive development across polymers, coatings, and specialty materials.

Food and consumer applications are experiencing a parallel shift. In April 2025, the U.S. Food and Drug Administration and the Department of Health and Human Services announced measures to phase out petroleum-based synthetic food dyes by the end of 2026. This initiative fast-tracked approval of new natural color additives, including algae-derived blue pigments, expanding opportunities for performance additives in food and nutraceutical formulations. Industrial innovation continues in parallel. Nouryon launched a new Innovation Center in Texas in June 2025 focused on specialty additives for high-pressure, high-temperature oilfield extraction. In aerospace materials, companies such as 3M expanded U.S. production of lightweight glass bubble fillers in 2025, responding to demand for additives that reduce composite weight while preserving structural performance in aviation and defense platforms.

India: Cluster-Led Manufacturing and Additive Self-Reliance

India’s high performance additives industry is progressing through a combination of financial resilience among multinational players and policy-led expansion of domestic innovation clusters. In the first quarter of the 2025–26 fiscal year, BASF India reported revenues of Rs. 38,745.4 million, maintaining stability across its Industrial Solutions and Surface Technologies segments despite global raw material volatility. This performance underscores steady demand for performance additives in coatings, construction chemicals, and industrial formulations.

Government policy is reinforcing domestic capability. India is expanding its Science and Technology Cluster program from eight to 25 clusters by 2028, with 2026 priorities focused on “Make in India” production of high performance additives for paints and coatings. Renewable and bio-based inputs are also gaining traction. In 2025, Nouryon partnered with Atul Ltd to expand monochloroacetic acid capacity, supporting the manufacture of cellulose-based additives used in construction chemicals, pharmaceuticals, and personal care. These developments signal India’s gradual transition from additive import dependence toward localized, application-specific production.

Summary Table: Country-Level Strategic Signals in the High Performance Additives Industry

High performance Additives Market County Level Snapshot

|

Country

|

Primary Policy or Strategy

|

Key Additive Focus Areas

|

Structural Implication

|

|

China

|

MIIT growth plan, digital mandates

|

Flame retardants, peroxides, electronic additives

|

Localization and AI-enabled manufacturing

|

|

Germany

|

Climate Contracts, circular economy

|

Light stabilizers, recycling additives

|

Low-carbon and circular leadership

|

|

United States

|

EPA and FDA guidance

|

Bio-based additives, lightweight fillers

|

Regulatory-driven reformulation

|

|

India

|

S&T cluster expansion, Make in India

|

Coatings additives, cellulose derivatives

|

Domestic capacity and self-reliance

|

High performance Additives Market Report Scope

High performance Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.8 Billion

|

|

Market Size (2034)

|

$27.9 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Product Type (Plastic Additives, Rubber Additives, Paints and Coatings Additives, Lubricant Additives, Flame Retardant Additives, Food Additives, Ink Additives), By Functionality (Antioxidants, UV Stabilizers, Processing Aids, Flame Retardants, Antimicrobials), By End-Use Industry (Automotive and Transportation, Packaging, Construction and Infrastructure, Electronics and Electrical, Healthcare and Pharmaceuticals, Agriculture and Plasticulture, Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, Clariant AG, Nouryon, Songwon Industrial Co., Ltd., W. R. Grace & Co., Avient Corporation, Lanxess AG, The Lubrizol Corporation, Infineum International Ltd., Chevron Oronite Company LLC, Innospec Inc., Baerlocher GmbH, Dow Inc., Eastman Chemical Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Performance Additives Market Segmentation

By Product Type

- Plastic Additives

- Rubber Additives

- Paints and Coatings Additives

- Lubricant Additives

- Flame Retardant Additives

- Food Additives

- Ink Additives

By Functionality

- Antioxidants

- UV Stabilizers

- Processing Aids

- Flame Retardants

- Antimicrobials

By End-Use Industry

- Automotive and Transportation

- Packaging

- Construction and Infrastructure

- Electronics and Electrical

- Healthcare and Pharmaceuticals

- Agriculture and Plasticulture

- Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the High Performance Additives Industry

- BASF SE

- Evonik Industries AG

- Clariant AG

- Nouryon

- Songwon Industrial Co., Ltd.

- W. R. Grace & Co.

- Avient Corporation

- Lanxess AG

- The Lubrizol Corporation

- Infineum International Ltd.

- Chevron Oronite Company LLC

- Innospec Inc.

- Baerlocher GmbH

- Dow Inc.

- Eastman Chemical Company

*- List not Exhaustive