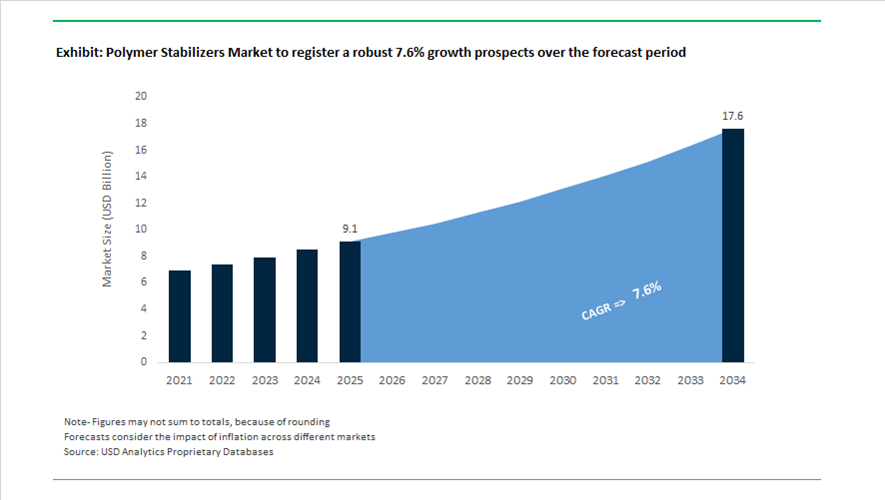

Polymer Stabilizers Market Valued at $9.1 Billion in 2025, Forecast to Reach $17.6 Billion by 2034 at 7.6% CAGR

The global polymer stabilizers market is valued at $9.1 billion in 2025 and is projected to reach $17.6 billion by 2034, expanding at a robust CAGR of 7.6%. Demand is accelerating across polyolefins, PVC, PET, engineering plastics, automotive polymers, power cables, greenhouse films, and recycled plastics, where thermal stability, UV resistance, oxidation control, and long-term durability are critical performance parameters. Growth is closely linked to regulatory tightening around food-contact safety, PFAS elimination, circular plastics adoption, and electrification-driven material upgrades in automotive and energy infrastructure.

In March 2024, the U.S. FDA extended approval for SI Group’s WESTON™ 705 and 705T phosphite antioxidants for use in PET food-contact packaging. These nonylphenol-free stabilizers address stringent compliance requirements in food-grade polyethylene terephthalate applications. In the same month, Baerlocher USA partnered with Innoleics to distribute bio-based materials, focusing on customizable liquid mixed-metal stabilizers for flexible PVC formulated with bio-based plasticizers. This marked a strategic pivot toward bio-based polymer stabilizers and sustainable PVC stabilization systems. At NPE 2024, Clariant introduced AddWorks PKG 158, an antioxidant solution engineered specifically for polyolefins containing post-consumer recycled content. The product mitigates yellowing and color degradation during reprocessing, addressing a core limitation in mechanically recycled plastics.

In late 2024, Clariant completed the transition to a fully PFAS-free additive portfolio, including the AddWorks PPA processing aid line. This transition responds to global regulatory scrutiny of fluorinated chemistries and reinforces demand for PFAS-free polymer additives and environmentally compliant stabilizer solutions. Market restructuring intensified in 2025. In April 2025, Sabo S.p.A. terminated its long-standing distribution agreement with Songwon Industrial Group to establish direct global market access for its Hindered Amine Light Stabilizers, effective June 2025. This strategic shift enhances pricing control, brand positioning, and direct customer engagement in the HALS segment.

Also in April 2025, BASF expanded production capacity at its Kaisten, Switzerland site to support rising demand for antioxidant and light stabilizer additives in automotive and construction polymers. In August 2025, BASF launched Tinuvin® NOR® 112 under its VALERAS® portfolio, targeting greenhouse films used in organic farming. This HALS formulation protects against agrochemical exposure and intense UV radiation while maintaining crop compatibility, strengthening the agricultural plastics stabilizers segment. In November 2025, Songwon Industrial Group announced a greenfield investment in Saudi Arabia to build a One Pack Systems plant dedicated to customized stabilizer blends for the Middle East polyolefin industry. In parallel, Arclin completed the acquisition of Polymer Solutions Group, integrating specialty stabilizer technologies into engineered wood and rubber portfolios.

Technological specialization accelerated into 2026. In February 2026 at PlastIndia, BASF introduced Irgastab® Cable KV 10, a high-performance thermal stabilizer designed for high-voltage polyethylene cable insulation. The formulation provides scorch protection during cross-linking and prevents long-term thermal oxidation, supporting grid modernization and renewable energy transmission infrastructure. In the same month, Milliken unveiled RESIST XTR colorants engineered for EV battery connectors, delivering enhanced UV resistance and thermal stability under elevated operating temperatures.

The polymer stabilizers market is evolving toward high-efficiency HALS systems, advanced phosphite antioxidants, PFAS-free processing aids, bio-based PVC stabilizers, recycled polymer protection additives, and high-voltage cable stabilization technologies. Regulatory compliance, recycled-content compatibility, electrification, and sustainable additive chemistry are redefining competitive positioning across global polymer stabilization applications.

Transformational Trends and High-Impact Opportunities in the Polymer Stabilizers Market

Regulatory-Forced Transition to Non-Hazardous and Lead-Free Polymer Stabilizers

The polymer stabilizers market has entered a post-grace-period phase in which regulatory compliance is no longer gradual but immediate and non-negotiable. The enforcement of Regulation (EU) 2023/923 has fundamentally altered stabilizer selection strategies across PVC pipes, profiles, cables, and construction materials. As of November 29, 2024, the placement of PVC articles containing lead concentrations equal to or exceeding 0.1% by weight is prohibited, triggering a structural and irreversible shift toward Calcium-Zinc (Ca-Zn) and organic-based stabilizer systems.

Beyond outright bans, enforcement mechanisms are reshaping buyer behavior. Under REACH, recycled rigid PVC products benefiting from temporary exemptions allowing up to 1.5% lead until 2033 must now carry mandatory labeling stating “Contains ≥ 0.1% lead.” This visible toxic labeling has become a commercial liability for brand owners and infrastructure contractors, accelerating voluntary migration to Ca-Zn one-pack systems to avoid reputational and procurement risks. As a result, stabilizer demand is increasingly concentrated around lead-free solutions that offer regulatory certainty across the full product lifecycle.

The regulatory push is also catalyzing technology substitution within stabilizer chemistry. At the K 2025 trade fair, Baerlocher formalized its Global Tin Replacement initiative, targeting the systematic phase-out of organotin stabilizers. The program enables PVC processors to maintain extrusion speeds exceeding 100 meters per minute while eliminating the compliance risks associated with tin-based systems. In parallel, geopolitical constraints are influencing material choices. Following China’s 2024 export controls on antimony, Clariant introduced its AddWorks titanium-based catalyst technology in October 2025, allowing PET and PBT producers to decouple from antimony-dependent stabilizer systems while reducing polymerization temperatures and energy intensity.

Engineering Stabilizer Systems for High-Voltage and High-Heat EV Applications

Electrification is redefining the functional requirements of polymer stabilizers. Engineering plastics used in electric vehicles are now expected to operate continuously above 150°C for the entire service life of the vehicle, while also maintaining dielectric integrity in high-voltage environments. This has driven the evolution of stabilizers from single-function antioxidants into synergistic systems combining long-term thermal stability, oxidative resistance, and electrical insulation performance.

Industrial investment patterns reflect this shift. In October 2025, SONGWON announced a major capital investment to establish a dedicated One Pack Systems production facility in Saudi Arabia. This site is designed to serve the fast-growing Middle East and Asian EV supply chains with high-performance stabilizer blends optimized for polyolefins and engineering plastics used in under-the-hood electronics and battery management systems. The strategic location supports both regional manufacturing localization and lower-carbon additive supply.

Performance validation is reinforcing adoption. Independent 2024–2025 testing of Songnox binary antioxidant blends demonstrated stable Oxidation Induction Time even after repeated high-heat cycling. These stabilizers enable polyamides and polybutylene terephthalate to function reliably as busbar insulators, battery housings, and power module components, allowing OEMs to replace heavier metal assemblies with stabilized polymer solutions that improve vehicle efficiency and thermal management.

Re-Stabilization Packages Enabling Upcycling of PCR Polyolefins

The most commercially significant opportunity in the polymer stabilizers market is emerging from recycled plastics. Mechanical recycling introduces chain scission and residual peroxides that lead to discoloration, embrittlement, and inconsistent melt behavior, historically limiting post-consumer recycled resins to low-value applications. Advanced re-stabilization packages are now changing this equation by restoring processing and performance profiles close to virgin materials.

Demonstrated industrial results are accelerating adoption. In May 2024, collaborative trials by Baerlocher USA and the EREMA Group showed that BAEROPOL T-Blend 1214 TX reduced large gel defect coverage in recycled polyethylene films by nearly 50%. By stabilizing the polymer melt during filtration and extrusion, the technology allows films containing 20% PCR to achieve clarity and mechanical performance comparable to virgin-grade products, unlocking higher-margin packaging applications.

Material science innovation is also broadening the stabilizer portfolio. Research published in late 2024 highlighted the effectiveness of natural-derived antioxidant stabilizers sourced from spent coffee residues in suppressing melt flow rate increases during recycled polypropylene processing. These systems slow chain degradation and imitate virgin resin behavior, preventing rapid downcycling and supporting automotive interior and durable goods applications where appearance and mechanical consistency are critical.

Stabilization Solutions for Biodegradable and Bio-Based Polymer Systems

The rapid scale-up of biodegradable plastics is creating a parallel stabilizer demand cycle. Polylactic Acid and Polyhydroxyalkanoates are highly sensitive to heat and moisture during processing, particularly in tropical and high-humidity environments. This sensitivity is driving demand for hydrolytic stabilizers that preserve molecular weight and mechanical integrity without compromising compostability certifications.

India’s bio-plastics industrialization highlights this opportunity. In 2024, Praj Industries commissioned India’s first integrated PLA demonstration plant, underscoring the need for tailored stabilizer systems that manage the critical lactide-to-polymer conversion while ensuring stable processing in challenging climatic conditions. Without such stabilization, PLA degradation accelerates, limiting its competitiveness against conventional polymers.

Regulatory alignment is further shaping product development. In June 2025, Clariant launched the AddWorks PPA portfolio, a new generation of PFAS-free polymer processing aids designed for bio-based and recycled polyolefins. These stabilizers eliminate surface defects such as shark skin while complying with upcoming EU Packaging and Packaging Waste Regulation requirements. Their compatibility with sustainable polymers positions them as essential enablers for large-scale adoption of biodegradable and circular plastics.

Polymer Stabilizers Market Share and Segmentation Insights

Antioxidants Dominate Polymer Stabilizer Demand in Thermoplastic Processing and Product Protection

Antioxidants accounted for 42.8% of the Polymer Stabilizers Market by type in 2025, reflecting their essential role in protecting polymers from oxidative degradation during high-temperature processing and long-term product use. Primary antioxidants such as hindered phenols and secondary antioxidants including phosphites and thioesters are widely used in polyethylene, polypropylene, PVC, polystyrene, and engineering plastics to maintain polymer molecular weight, mechanical strength, and color stability. Virtually all thermoplastic materials require antioxidant stabilization during extrusion, injection molding, and compounding processes. In 2025, growing use of recycled plastics has increased demand for advanced antioxidant stabilizer systems, enabling polymer processors to stabilize degraded recyclate streams while maintaining processing stability and performance in circular plastic production systems.

Packaging Industry Drives Polymer Stabilizer Consumption in Food and Consumer Product Applications

Packaging represented 38.6% of the Polymer Stabilizers Market by application in 2025, reflecting the large-scale use of stabilized polymers in food containers, beverage bottles, flexible films, caps, and closures used across global consumer markets. Polyolefin packaging materials such as polyethylene and polypropylene require antioxidant and light stabilizer systems to maintain polymer integrity during manufacturing and throughout product shelf life. The scale of global packaging production and increasing demand for durable, lightweight plastic packaging continue to support stabilizer consumption in this segment. In 2025, food contact regulatory compliance has become a key factor influencing stabilizer formulation, with polymer additive manufacturers developing low migration, food approved stabilizers designed to meet strict global food packaging safety standards.

Polymer Stabilizers Market Competitive Landscape

The global polymer stabilizers market is transitioning toward PFAS-free processing aids, heavy-metal-free PVC stabilizers, and circularity-enabling additives. Competitive dynamics are shaped by regulatory compliance, thermal stability requirements, and advanced stabilizer systems for automotive, construction, packaging, and recycling applications.

BASF Leads Sustainable Stabilizer Innovation with VALERAS® Portfolio and ISCC PLUS Certification

BASF SE continues to dominate polymer stabilizers through its VALERAS® portfolio, focusing on high-performance and sustainable additives. A global price increase of up to 20% in March 2026 reflects rising raw material and logistics costs. Tinuvin® NOR® 211 AR enhances durability of agricultural films by resisting sulfur and chlorine exposure. ISCC PLUS certification at Kaisten and McIntosh sites enables mass-balanced stabilizers with reduced product carbon footprint. Tinuvin® NOR® 600 targets outdoor applications requiring high acid resistance and long-term weatherability. Strategy emphasizes sustainable stabilizers, regulatory compliance, and advanced UV and thermal protection technologies.

Songwon Strengthens Global Stabilizer Supply with OPS Systems and High-Temperature Antioxidants

Songwon Industrial Co., Ltd. maintains strong market positioning through reliable supply of polymer stabilizers and antioxidants. A 12% to 20% price adjustment in 2026 addresses cost pressures across the specialty chemical value chain. The company specializes in phosphite and phenolic antioxidants critical for high-temperature polyolefin processing. Its Songnox® and Songsorb® portfolios are increasingly delivered as dust-free One Pack Systems (OPS), improving manufacturing efficiency and safety. Expansion into coatings and electronics applications supports demand for long-term thermal stability. Strategy focuses on supply chain resilience, formulation efficiency, and high-performance stabilizer systems.

Adeka Advances Heavy-Metal-Free Stabilizers with Recycling Solutions and High-Performance Clarifiers

Adeka Corporation is leading the transition toward environmentally friendly stabilizers, particularly in PVC and polypropylene applications. The ADK CYCLOAID™ UPR series supports mechanical recycling by preventing thermal degradation in post-consumer plastics. Adeka Transparex™ delivers high transparency and heat resistance in polypropylene, gaining industry recognition for performance innovation. The ADK STAB RX calcium-zinc stabilizers replace lead-based systems, ensuring compliance with global REACH standards. Investment in organometallic compound production strengthens its portfolio in advanced materials and polymer intermediates. Strategy emphasizes sustainable stabilizers, recycling compatibility, and high-performance polymer additives.

Clariant Expands Bio-Based Stabilizers and High-Performance Additives for Green Building and Agrochemical Applications

Clariant AG is focusing on specialty stabilizers for high-growth sectors including agriculture, medical plastics, and construction. Dispersogen® PSL 100 provides advanced stabilization for agrochemical formulations, improving crystal growth control and product stability. Renewable rice bran wax additives mark a shift toward bio-based stabilizers for food-contact plastics. The company achieved a 17.8% EBITDA margin in 2025, supported by operational efficiency programs. Exolit™ flame retardants and AddWorks® stabilizers are tailored for low-VOC, high-durability construction materials. Strategy centers on bio-based innovation, niche applications, and sustainable additive technologies.

Baerlocher Drives PVC Stabilizer Transformation with Calcium-Zinc Systems and Circular Economy Focus

Baerlocher Group is advancing the global transition from tin-based to calcium-zinc stabilizers under its Tin Replacement initiative. BAEROSTAB and BAEROPAN systems enable up to 50% CO₂ reduction while maintaining processing performance. Baeropol® T-Blend and Baerolub® AID support recycling by preventing gel formation and thermal degradation. The company is transitioning European production to fully heavy-metal-free stabilizers for regulated applications. Investments in renewable energy support its carbon neutrality target by 2045. Strategy focuses on sustainable PVC stabilization, recycling compatibility, and regulatory-driven innovation.

Evonik Integrates Advanced Stabilizers with Circular Polymer Systems and High-Performance Applications

Evonik Industries AG is leveraging specialty additives and polymer science to address circularity and performance challenges. The company reported €1.87 billion EBITDA in 2025, with strong demand in advanced polymer applications. Stabilizers and crosslinkers support high-performance plastics used in 3D printing and membrane technologies. The establishment of SYNEQT enables focus on core additives and custom solutions businesses. Free cash flow of €695 million is being reinvested into bio-based stabilizers and hydrogen economy applications. Strategy emphasizes advanced materials integration, circular economy solutions, and next-generation stabilizer development.

Germany: Regulatory-Led Innovation and High-Durability Stabilizer Leadership

Germany continues to position itself as a technology and compliance anchor within the global polymer stabilizers industry, with 2025 marked by a convergence of advanced chemistry, regulatory alignment, and sustainability execution. In October 2025, BASF launched Tinuvin® NOR® 600 at K 2025, introducing a next-generation NOR-HALS light stabilizer engineered for high-acid resistance. This innovation directly addresses durability challenges in roofing membranes and artificial turf, segments where chemical exposure and long service life requirements are increasingly dictated by European construction and infrastructure standards. Parallel to this, Baerlocher accelerated its PFAS-free roadmap with the August 2025 commercialization of the Baerolub® AID family, positioning non-PFAS polymer processing aids as a compliance-driven alternative amid tightening EU and U.S. safety scrutiny.

Regulatory readiness is reinforced by Baerlocher’s 2025 transition toward tin-replacement stabilizer systems across its global PVC portfolio, aligning with REACH and RoHS requirements for medical-grade and potable water applications. Sustainability has moved beyond signaling to execution, with Baerlocher committing to carbon-neutral operations by 2045 and deploying solar and biomass investments at its Munich production hubs during 2025. Performance benchmarking also remained central, as Clariant and Omya jointly demonstrated that AddWorks™ IBC 760 can extend SMP sealant service life by up to 50%, reaching 3,000 hours under accelerated weathering. BASF further expanded its VALERAS® sustainability platform in August 2025 to include high-durability stabilizers certified for organic farming greenhouse films, reinforcing Germany’s role as a reference market for compliant, long-life polymer stabilization.

South Korea: Decarbonization-Driven Manufacturing and Automotive Stabilizer Specialization

South Korea’s polymer stabilizers landscape in 2025 is characterized by operational decarbonization and application-specific portfolio refinement. Songwon Industrial initiated a major shift at its Ulsan facility by replacing conventional steam with zero-GHG emission steam in late 2025, targeting an annual reduction of 25,900 tCO2-eq by 2027. This move strengthens South Korea’s positioning as a low-carbon manufacturing base for antioxidants and UV stabilizers, increasingly favored by global polymer producers seeking Scope 3 emissions reductions. Songwon’s sustainability credentials were further validated through its fifth consecutive EcoVadis Gold rating in 2025, underlining the integration of sustainable procurement across its stabilizer supply chain.

On the demand side, automotive lightweighting continues to shape stabilizer development. Sumitomo Chemical Korea enhanced its stabilizer formulations in October 2025 to deliver long-term heat stability for polyolefin-based interior components, reflecting the thermal and durability requirements of next-generation vehicle platforms. Circularity initiatives also gained traction, with Songwon transitioning Korean sites to 20 kg packaging bags containing up to 50% recycled polyethylene. Collectively, these developments position South Korea as a stabilizer hub where emissions reduction, automotive performance, and circular packaging standards converge.

India: Regulatory Enforcement and Biodegradable Stabilizer Momentum

India’s polymer stabilizers industry in 2025 is being reshaped by regulatory enforcement, renewable energy adoption, and structural shifts in ownership. In December 2025, Arkema announced the proposed divestment of its global MBS copolymers and acrylic impact modifiers business to Indian group Praana, a transaction expected to close in Q1 2026. This move signals increasing domestic control over stabilizer-adjacent technologies and strengthens India’s role in global supply chains. Regulatory pressure intensified with the July 1, 2025 enforcement of Plastic Waste Management Rules mandating QR-code traceability for all plastic packaging, compelling stabilizer producers to deliver digital documentation on additive safety and recycled content.

Sustainability execution is advancing in parallel. Songwon’s Panoli plant reached 63% renewable energy sourcing in 2025 and implemented Zero Liquid Discharge systems, setting new operational benchmarks for additives manufacturing in India. Demand-side stimulus is being reinforced by a ₹3,000 crore MSME subsidy scheme launched in 2025, targeting modernization of 15,000 plastic processing units and accelerating adoption of biodegradable stabilizers. Full enforcement of the Single-Use Plastic (Regulation) Act in 2025 further catalyzed demand for stabilizers compatible with PLA and compostable polymers, positioning India as a high-velocity market for compliant, bio-compatible stabilization solutions.

Saudi Arabia: Localization Strategy and Extreme-Climate Stabilizer Demand

Saudi Arabia’s polymer stabilizers market in 2025 reflects the Kingdom’s broader industrial localization agenda under Vision 2030. In October 2025, Songwon Industrial announced a greenfield investment to establish a One Pack Systems production facility, directly supporting localized polyolefin compounding and reducing reliance on imported stabilizer blends. This investment aligns with downstream integration efforts led by SABIC, which strengthened its stabilizer offerings in November 2025 to support high-efficiency antioxidant systems for domestic polymer processors.

Climatic conditions remain a defining factor. Regional producers increasingly adopted high-dosage UV stabilizers in 2025, formulated specifically to withstand extreme heat and solar radiation in Middle Eastern construction and infrastructure applications. As a result, Saudi Arabia is emerging as a reference market for durability-driven stabilizer formulations optimized for harsh environmental exposure rather than purely regulatory compliance.

China: Policy-Driven Transition Toward Traceable and Durable Stabilizers

China’s polymer stabilizers industry in 2025 is undergoing structural realignment following the conclusion of the Plastic Pollution Control Action Plan (2021–2025). The finalized framework mandates the prohibition of additives harmful to human health and the environment in consumer-facing plastics, accelerating the phase-out of legacy stabilizer chemistries. Concurrently, the 2025 Green Packaging roadmap has forced logistics and e-commerce operators to adopt certified compostable stabilizers and implement clear material labeling, reshaping demand across flexible packaging applications.

Agricultural and traceability regulations further influenced stabilizer selection. New rules prohibiting mulch films thinner than 0.01 mm shifted demand toward long-lasting UV stabilizers that prevent premature degradation. Extended Producer Responsibility pilots in Shanghai and Hainan now require QR-traceable end-of-life pathways, compelling stabilizer manufacturers to integrate digital traceability into product documentation. These measures position China as a policy-driven market where durability, transparency, and environmental compliance define competitive differentiation.

Japan: High-Performance Stabilizers for Electronics and Transparency Applications

Japan’s polymer stabilizers landscape in 2025 is defined by precision performance and alignment with long-term decarbonization goals. In October 2025, ADEKA Corporation achieved Guinness World Record certification for ADK TRANSPAREX™, recognized as the most effective clarifier for polypropylene transparency with a haze value of 2.0. This milestone underscores Japan’s leadership in optical performance additives for high-clarity polymer applications. ADEKA further advanced electronics-grade stabilizers in November 2025, delivering enhanced heat resistance tailored to 5G and emerging 6G high-frequency electronics.

Sustainability alignment is progressing through material innovation. Mitsubishi Chemical expanded its eco-friendly stabilizer portfolio in September 2025 by incorporating bio-based feedstocks, supporting Japan’s 2050 carbon-neutral commitment. Collectively, these developments reinforce Japan’s position as a premium market for high-purity, high-performance polymer stabilizers serving electronics, optics, and advanced manufacturing sectors.

Summary of Country-Level Developments in the Polymer Stabilizers Industry

Polymer Stabilizers Market County Level Snapshot

|

Country

|

2025 Strategic Focus Areas

|

Key Industry Implications

|

|

Germany

|

NOR-HALS innovation, PFAS-free aids, tin replacement, carbon-neutral operations

|

Benchmark market for compliant, high-durability stabilizers

|

|

South Korea

|

Zero-GHG manufacturing, automotive heat stability, circular packaging

|

Low-carbon production hub with automotive specialization

|

|

India

|

QR traceability, biodegradable stabilizers, renewable-powered plants

|

High-growth compliance market with domestic ownership shift

|

|

Saudi Arabia

|

OPS localization, extreme-climate UV stabilization

|

Durability-driven demand under Vision 2030

|

|

China

|

Additive bans, EPR traceability, durable agricultural films

|

Policy-led transition toward transparent stabilizer systems

|

|

Japan

|

Ultra-low haze clarifiers, electronics-grade stabilizers, bio-based feedstocks

|

Premium performance market for advanced applications

|

Polymer Stabilizers Market Report Scope

Polymer Stabilizers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.1 Billion

|

|

Market Size (2034)

|

$17.6 Billion

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Type (Antioxidants, Light Stabilizers, Heat Stabilizers, Anti-Degradants & Deactivators), By Application (Packaging, Building & Construction, Automotive, Agriculture, Electrical & Electronics), By End-Use Material (Polyethylene, Polypropylene, Polyvinyl Chloride, Polystyrene, Engineering Plastics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Songwon Industrial Co. Ltd., Adeka Corporation, Clariant AG, Baerlocher GmbH, SI Group Inc., Evonik Industries AG, Sabo S.p.A., Solvay SA, Sumitomo Chemical Co. Ltd., Mitsubishi Chemical Group, SABIC, Albemarle Corporation, Fine Organics, PMC Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymer Stabilizers Market Segmentation

By Type

By Application

- Packaging

- Building & Construction

- Automotive

- Agriculture

- Electrical & Electronics

By End-Use Material

- Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Polystyrene

- Engineering Plastics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polymer Stabilizers Industry

- BASF SE

- Songwon Industrial Co. Ltd.

- Adeka Corporation

- Clariant AG

- Baerlocher GmbH

- SI Group Inc.

- Evonik Industries AG

- Sabo S.p.A.

- Solvay SA

- Sumitomo Chemical Co. Ltd.

- Mitsubishi Chemical Group

- SABIC

- Albemarle Corporation

- Fine Organics

- PMC Group

*- List not Exhaustive