Low Smoke Halogen Free Flame Retardant Polypropylene Market Size, EV Safety Regulations, and High-Performance Polymer Demand Outlook

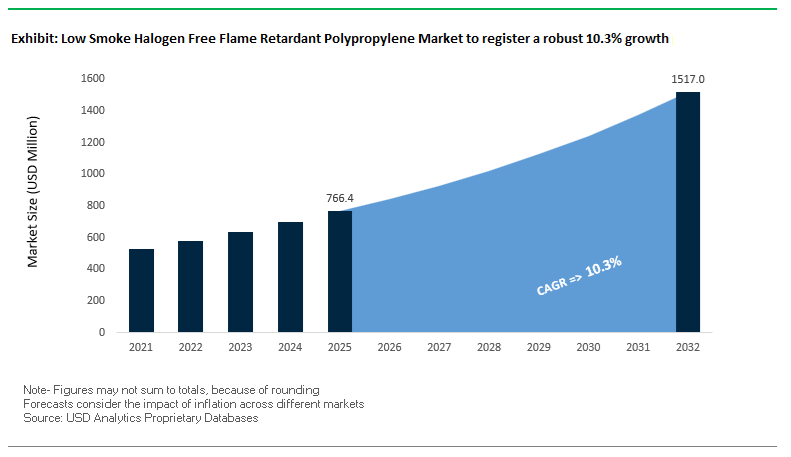

The global low smoke halogen free flame retardant polypropylene (LSHF PP) market was valued at $766.4 million in 2025 and is projected to reach $1,522.2 million by 2032, expanding at a robust CAGR of 10.3%. This strong growth trajectory is driven by increasing demand for halogen-free flame retardant polypropylene compounds, low-smoke thermoplastics, and high-performance polymer materials across electric vehicles (EVs), wire & cable, electronics, aerospace, and public infrastructure applications. These materials are critical in environments where fire safety, low smoke emission, and reduced toxicity are essential for protecting human life and sensitive electronic systems.

A major growth catalyst is the rapid expansion of the electric vehicle ecosystem, where LSHF PP is widely used in battery modules, charging infrastructure, busbar holders, and high-voltage components. Stringent fire safety standards, including requirements for UL94 V-0 flame ratings, thermal runaway resistance, and electrical insulation performance, are accelerating the adoption of advanced polypropylene compounds. Additionally, increasing regulatory pressure in transportation, telecommunications, and construction sectors is driving the shift away from traditional halogenated flame retardants toward environmentally compliant, recyclable, and low-toxicity alternatives.

The market is also benefiting from advancements in polymer compounding technologies, additive chemistry, and sustainable feedstocks, enabling improved mechanical strength, thermal stability, and recyclability. Growth in 5G infrastructure, renewable energy systems, and public transit modernization is further expanding the application scope of LSHF PP materials. Regionally, Asia-Pacific dominates due to strong EV manufacturing and electronics production, while Europe leads in regulatory-driven adoption and sustainable material innovation, and North America remains a key market for high-performance polymer applications.

Market Analysis: Regulatory Mandates, EV Battery Safety Innovation, and Sustainable Polymer Development Driving Market Transformation

The LSHF polypropylene market is undergoing rapid transformation, driven by regulatory enforcement, product innovation, and strategic capacity expansion. A critical inflection point is the GB 38031-2025 regulation, finalized in June 2025 and effective from July 2026, which mandates that EV battery packs must not catch fire during thermal runaway events. This regulation effectively establishes LSHF PP as a standard material for internal battery structural components in China, significantly accelerating demand across the global EV supply chain.

Capacity expansion and supply chain strengthening are aligning with this demand surge. In March 2026, SABIC inaugurated a dedicated compounding line in Asia focused on halogen-free flame-retardant polypropylene, specifically targeting EV battery modules and charging infrastructure. Similarly, LyondellBasell’s March 2025 propylene expansion project in Texas is strategically linked to rising global demand for specialty polypropylene grades, including LSHF materials used in automotive and aerospace applications.

Product innovation is advancing performance benchmarks in flame retardant polymers. RTP Company introduced a new generation of glass-fiber-reinforced LSHF PP compounds in January 2026, capable of achieving UL94 V-0 ratings at ultra-thin wall thicknesses (as low as 0.8 mm), enabling miniaturization in electronic connectors and power distribution units. This builds on its July 2025 launch of impact-resistant LSHF PP compounds, engineered for low-temperature performance in EV battery enclosures and outdoor charging systems. BASF further strengthened the value chain with its November 2025 Irgafos® and Flamestab® additive systems, which enhance mechanical integrity and color stability even after multiple recycling cycles, supporting circularity in the electrical and electronics (E&E) sector.

Sustainability is becoming a core competitive differentiator. Borealis AG’s December 2025 commercialization of Bornewables™ LSHF PP, produced from 100% renewable feedstock via mass-balance, addresses increasing demand for Scope 3 emission reductions in telecom and construction markets. Complementing this, Clariant AG expanded its Exolit® OP flame retardant capacity in February 2025, ensuring supply of phosphorus-based halogen-free additives, which are essential for producing compliant LSHF PP compounds globally.

Emerging applications are also broadening market scope. Avient Corporation’s Edgetek™ PKE LSHF compounds, launched in October 2024, are tailored for public transit interiors, meeting stringent EN 45545-2 fire safety standards. Additionally, SABIC’s March 2024 PP compound for EV busbar holders achieved UL94 V-0 ratings with improved Comparative Tracking Index (CTI), enhancing electrical safety in high-voltage environments.

Market Trend: EN 45545-2 Compliance Driving Adoption of LSHF FR-PP in Rail Interior Applications

The global railway sector is undergoing a material transition toward Low Smoke Halogen Free Flame Retardant Polypropylene (LSHF FR-PP), primarily driven by stringent fire safety standards such as EN 45545-2. This regulatory framework, particularly for Hazard Level 3 (HL3) classifications, is compelling rail OEMs and interior component manufacturers to replace traditional materials with advanced halogen-free thermoplastics that offer superior fire performance, reduced toxicity, and improved passenger safety in confined environments such as tunnels and underground transit systems.

LSHF FR-PP compounds are engineered to achieve a Conventional Index of Toxicity below 0.75, significantly minimizing the release of harmful gases during combustion. This performance is critical in evacuation scenarios, where reduced toxicity levels directly influence passenger survivability. In parallel, smoke density benchmarks are being aggressively optimized, with advanced formulations consistently achieving maximum specific optical smoke density values below 150. This ensures enhanced visibility during fire incidents, particularly in high-risk rolling stock such as sleeper trains and metro systems.

Material substitution is also contributing to structural and energy efficiency gains. By replacing heavier metal and thermoset components, LSHF FR-PP enables weight reductions of up to 30% in interior applications such as wall panels and seating structures. This reduction directly supports energy efficiency and electrification goals across national rail networks. Additionally, these materials exhibit a Limiting Oxygen Index exceeding 32%, preventing flame propagation in high-airflow environments typical of rail cabins. These combined attributes are positioning LSHF FR-PP as a standard material specification in next-generation rail interior design and safety engineering.

Market Trend: EV Battery Pack Safety Requirements Accelerating Use of LSHF FR-PP for Thermal Runaway Protection

The electrification of mobility is creating a high-growth application segment for LSHF FR-PP in electric vehicle battery systems, where fire safety and thermal management are critical design parameters. Battery pack manufacturers are increasingly specifying halogen-free polypropylene materials for components such as module housings, busbar covers, and internal spacers, driven by the need to contain thermal runaway events and ensure passenger safety.

LSHF FR-PP materials are engineered to function as thermal barriers, capable of withstanding temperatures exceeding 300°C for durations ranging from 5 to 10 minutes. This performance provides a critical response window for passenger evacuation during battery failure scenarios, aligning with evolving global EV safety standards. In high-voltage architectures exceeding 800V, electrical insulation properties are equally critical. Advanced LSHF PP compounds achieve a Comparative Tracking Index of 600V (PLC 0), effectively preventing electrical tracking and short circuits even under adverse environmental conditions.

Material efficiency is further enhanced through advancements in flame retardancy at reduced thicknesses. Modern LSHF FR-PP grades can achieve UL 94 V-0 ratings at thicknesses as low as 0.8 mm, enabling thinner battery pack designs and improving volumetric energy density. Additionally, anti-dripping formulations eliminate the formation of flaming droplets during combustion, reducing the risk of secondary ignition within densely packed battery modules. These capabilities position LSHF FR-PP as a critical material innovation supporting the safety, efficiency, and scalability of next-generation electric vehicle platforms.

Market Opportunity: U.S. Federal Green Procurement Policies Expanding Market for Halogen-Free Flame-Retardant Materials

Sustainability-driven procurement policies in the United States are creating a significant opportunity landscape for LSHF FR-PP materials, particularly within federal infrastructure projects. The General Services Administration’s updated Green Procurement Compilation is prioritizing materials that eliminate halogenated flame retardants, aiming to reduce the environmental and health impacts associated with persistent bioaccumulative and toxic substances.

Under the 2025 and 2026 updates, federal contractors are incentivized to adopt halogen-free materials to achieve a targeted 20% reduction in PBT chemical usage across government facilities. This is accelerating the replacement of traditional PVC-based materials with LSHF FR-PP alternatives in applications such as electrical conduits, cable management systems, and interior architectural components. The integration of LSHF FR-PP into federal building projects also supports compliance with LEED v4.1 certification frameworks, particularly under the Material Ingredients credit category. The availability of Environmental Product Declarations for these materials enhances transparency and strengthens their positioning in sustainable construction.

Indoor air quality considerations further reinforce this transition. Halogen-free polypropylene materials significantly reduce the release of corrosive acidic gases during fire events, protecting sensitive infrastructure such as data centers and IT equipment within federal buildings. As government-led sustainability mandates continue to expand, LSHF FR-PP is expected to gain substantial traction as a preferred material solution in public sector construction and retrofitting initiatives.

Market Opportunity: China’s GB 51348-2025 Electrical Standards Driving Large-Scale Adoption of LSHF FR-PP in Construction

China’s updated GB 51348-2025 standard for electrical design in civil buildings is establishing a strong regulatory foundation for the widespread adoption of LSHF FR-PP materials in the construction sector. The mandate requires the use of low smoke halogen-free materials in electrical conduits and cable protection systems, particularly in high-rise and high-density urban developments, creating immediate and large-scale demand for compliant products.

A key provision of the standard is the requirement for LSHF materials in buildings exceeding 100 meters in height, where fire safety risks are amplified due to vertical evacuation challenges. This is driving rapid replacement of conventional halogenated materials with LSHF FR-PP pipes and fittings in residential and commercial construction projects. The regulation also introduces stricter smoke toxicity classifications, such as ZA1 ratings, effectively prohibiting the use of traditional flame retardants in communal electrical infrastructure.

In addition to safety compliance, the standard aligns with China’s broader green building initiatives. Developers incorporating LSHF FR-PP materials in projects across Tier-1 cities such as Shenzhen and Shanghai are eligible for enhanced ratings under the Three-Star Green Building certification system, facilitating access to favorable green financing mechanisms. Concurrently, regulatory enforcement around Low Smoke Zero Halogen labeling is becoming more stringent, pushing manufacturers toward high-purity phosphorus-nitrogen flame retardant systems that meet advanced toxicity and performance criteria.

Low Smoke Halogen-Free Flame Retardant Polypropylene Market Share and Segmentation Insights

Ready-to-Use LSHF Flame Retardant Polypropylene Compounds Capture 58% Share with Processing Efficiency

The low smoke halogen-free flame retardant polypropylene (LSHF-FR PP) market by product form is led by ready-to-use compounds, accounting for 58% of the global market share in 2025. This dominance is driven by their drop-in manufacturing convenience, eliminating the need for in-house compounding while ensuring consistent dispersion of phosphorus-based and magnesium hydroxide flame retardants. These compounds are engineered to meet stringent UL 94 V-0 flame retardancy standards, making them ideal for safety-critical applications. Their widespread use in electrical enclosures, EV battery components, wire & cable insulation, and mass transit interiors highlights their suitability for high-volume injection molding processes. By minimizing formulation variability and reducing scrap rates, ready-to-use LSHF-FR PP compounds significantly enhance production efficiency, positioning them as the preferred solution for manufacturers seeking reliable, compliant, and scalable flame-retardant polymer systems.

Direct Sales Channel Holds 48% Share Driven by Regulatory Compliance and OEM Partnerships

In the LSHF flame retardant polypropylene market by distribution channel, direct sales dominate with a 48% market share in 2025, reflecting the importance of technical customization and long-term supply reliability. These materials require highly specific formulations tailored to glow wire ignition temperature (GWIT), comparative tracking index (CTI), and melt flow properties, necessitating close collaboration between manufacturers and OEMs. Direct engagement ensures compliance with global standards such as EN 45545 (rail), BS 6853 (building safety), and IEC 60332 (wire and cable fire performance). Additionally, large OEMs in automotive, electronics, and electrical infrastructure secure multi-year supply agreements to mitigate risks associated with raw material fluctuations, particularly in phosphate and magnesium hydroxide supply chains. This strategic alignment enhances material consistency, regulatory assurance, and supply chain stability, reinforcing direct sales as the leading distribution channel.

Competitive Landscape in the Low Smoke Halogen Free Flame Retardant Polypropylene Market

SABIC dominates EV battery applications with advanced LSHF polypropylene solutions

SABIC holds a leading position in the LSHF polypropylene market by leveraging its feedstock advantage and strong R&D capabilities focused on e-mobility applications. Its STAMAX™ long glass fiber-reinforced PP (LGFPP) series includes halogen-free flame-retardant grades engineered specifically for high-voltage EV battery housings. Through its Bluehero™ ecosystem, SABIC provides integrated material solutions and engineering support to help OEMs comply with stringent thermal runaway safety standards set for July 2026. The company’s advanced CAE simulation tools enable predictive analysis of fire growth and structural performance under extreme conditions. With phosphorus-based LSHF compounds capturing approximately 14% of the global automotive FR-PP segment in 2026, SABIC continues to strengthen its leadership in next-generation mobility materials.

LyondellBasell advances circular and high-performance flame retardant polypropylene solutions

LyondellBasell is positioning itself at the forefront of sustainable fire safety materials by integrating circular economy principles with high-performance LSHF polypropylene. Its CirculenRenew™ polymer range has seen a 22% production increase, offering bio-attributed flame-retardant PP grades that maintain UL 94 V-0 performance while reducing carbon footprint. The company’s expertise in masterbatch technology enables lower additive loading levels (20–25 wt%), preserving mechanical integrity and impact resistance. LyondellBasell has also expanded its Purell medical-grade portfolio to incorporate halogen-free flame retardancy for healthcare and laboratory applications. Its recent innovation in polyphosphonate-functionalized PP minimizes additive migration, ensuring consistent fire performance over a 15-year lifecycle, a critical requirement for long-term infrastructure and industrial applications.

BASF drives additive innovation and regional expansion for LSHF polypropylene applications

BASF continues to lead in additive chemistry and compounded resin development within the LSHF polypropylene market. The company initiated commercial production of Elastollan® flame-retardant grades at its Shanghai facility in March 2026, targeting the rapidly expanding EV charging infrastructure market in Asia-Pacific. BASF’s materials are widely used in industrial automation and robotics, where cable insulation and connectors must withstand repeated flex cycles while maintaining fire safety standards. Through its #OurPlasticsJourney initiative, BASF is promoting mass balance-certified flame retardants to reduce reliance on fossil-based feedstocks. The introduction of Irgastab® Cable KV 10 enhances oxidative stability and extends the service life of mid-voltage cable insulation, reinforcing BASF’s role in high-reliability electrical applications.

Avient delivers customized LSHF polypropylene compounds for electronics and telecom sectors

Avient Corporation specializes in highly engineered LSHF polypropylene compounds tailored for demanding applications in consumer electronics and telecommunications. Its GraviTech™ and Maxxam™ FR product lines are optimized for 5G infrastructure, offering high dielectric strength and low smoke emission characteristics essential for data transmission environments. The company has established a “CycleWorks” facility focused on improving recyclability of flame-retardant polymers, enabling circular material flows without compromising fire performance. Avient’s non-blooming intumescent FR compounds address critical aesthetic requirements by eliminating surface residue on molded components used in premium electronics. Strategic acquisitions of European compounders further enhance its presence in building and construction applications, particularly in halogen-free roofing and insulation systems.

Clariant leads halogen-free additive innovation with advanced phosphorus-based technologies

Clariant remains a foundational player in the LSHF polypropylene value chain as a leading supplier of halogen-free flame retardant additives under its Exolit® portfolio. The company expanded its Exolit® OP production capacity in Germany to address growing global demand for phosphorus-based additives in electronics applications. Its expertise in Aluminum Hypophosphite (AHP) chemistry delivers superior flame-retardant efficiency with high flame-to-weight ratios. Clariant is also collaborating with automotive suppliers to develop laser-markable LSHF PP materials, enabling durable safety labeling without compromising fire performance. The introduction of Exolit® Terra, a fully bio-based phosphorus flame retardant, positions the company at the forefront of sustainable additive innovation, particularly for large-scale appliance manufacturing.

Lanxess strengthens high-performance LSHF solutions for energy and transportation sectors

Lanxess focuses on delivering high-end flame-retardant solutions for energy, transportation, and industrial applications requiring chemical stability and low toxicity. Its Emerald Innovation™ and Levagard® product lines are designed for extreme environments where traditional retardants fail or release corrosive gases. These materials are widely used in photovoltaic connectors and junction boxes, maintaining UL 94 V-0 ratings under prolonged UV exposure and environmental stress. In early 2026, Lanxess reported a 9.2% growth in its Flame Retardant Additives segment, driven by regulatory phase-outs of brominated compounds such as DecaBDE in North America. The company’s strategic focus on “Zero Halogen” systems aligns with global regulatory trends, particularly in high-speed rail and aerospace interior applications.

China Low Smoke Halogen Free Flame Retardant Polypropylene Market: EV Supply Chain and Infrastructure Megaprojects Driving Volume Leadership

China dominates the low smoke halogen free (LSHF) flame retardant polypropylene market, driven by its expansive electric vehicle (EV) manufacturing ecosystem and large-scale urban infrastructure development. Government initiatives under the “14th Five-Year Plan for Energy-Saving and Environmental Protection” are mandating a shift toward halogen-free materials and significant VOC reductions, accelerating the transition toward safer, eco-friendly polymer solutions. The implementation of GB/T 17651 standards for smoke density has further restricted the use of halogenated materials, especially in underground metro and public infrastructure projects.

Technologically, domestic manufacturers have advanced phosphorus-nitrogen synergistic flame retardant systems, reducing additive loading while maintaining high-performance safety standards such as V-0 ratings. The material is widely adopted in EV battery module spacers, connector housings, and semiconductor cleanroom applications, where fire safety and lightweight design are critical. Major investments in polymer hubs, particularly in Jiangsu province, are expanding LSHF compounding capacity to support electronics and high-tech industries. China continues to lead globally due to its localized production capabilities and strong demand from the electronics sector.

Germany LSHF Flame Retardant Polypropylene Market: Circular Economy and High-Performance Material Innovation

Germany represents a technology-driven LSHF polypropylene market, emphasizing sustainability, regulatory compliance, and advanced material engineering. The country aligns closely with the EU Green Deal, REACH, and RoHS directives, leading to a near-complete phase-out of halogenated flame retardants in consumer and industrial applications. This has positioned Germany as a hub for bio-based and low-carbon LSHF materials, including innovations using lignin-derived retardants that significantly reduce environmental impact.

German companies are pioneering intumescent flame retardant systems, which create protective char layers at lower temperatures, enhancing safety in critical applications such as high-voltage DC (HVDC) power grids. The automotive sector remains a major application area, where LSHF PP is used in interior components requiring low toxicity, minimal odor, and high fire resistance. Additionally, investments in hydrogen infrastructure and AI-driven material informatics under Industry 4.0 are accelerating the development of customized flame-retardant formulations, reinforcing Germany’s leadership in advanced polymer technologies.

United States LSHF Flame Retardant Polypropylene Market: Aerospace, Defense, and Smart Infrastructure Applications

The United States market is characterized by high-value, specialized applications of LSHF polypropylene, particularly across aerospace, defense, and smart infrastructure sectors. Defense programs, including the U.S. Army’s Component Repair and Modernization initiatives, are increasingly specifying LSHF PP for internal wiring conduits to enhance fire survivability and reduce toxic emissions during emergencies.

Technological advancements such as nanoclay-reinforced LSHF polypropylene are enabling improved mechanical strength and flame resistance, making them ideal for drone housings and small satellite components. The growing demand for LSHF materials in hyperscale data centers and smart city infrastructure is further driving adoption, particularly for cable management systems and 5G network components. Regulatory pressure from the EPA’s Toxic Substances Control Act (TSCA) is accelerating the transition toward halogen-free chemistries in residential and commercial construction, reinforcing market growth across multiple sectors.

India LSHF Flame Retardant Polypropylene Market: Infrastructure Safety and Domestic Manufacturing Acceleration

India is emerging as the fastest-growing market for LSHF flame retardant polypropylene, supported by strong government initiatives and infrastructure expansion. The National Infrastructure Pipeline (NIP) is driving rapid growth in construction, with mandatory adoption of LSHF cables and materials in airports, railways, and public transit systems to enhance fire safety standards.

The “Make in India” initiative is encouraging local compounding and manufacturing of flame-retardant polymers, reducing reliance on imports and strengthening domestic supply chains. LSHF PP is increasingly used in mass transit systems, including Vande Bharat and Amrit Bharat train fleets, where fire safety and low smoke emission are critical. Strategic investments, such as the development of a large-scale LSHF PP facility in Gujarat, are boosting production capacity. Additionally, the adoption of standards like IS 17017 for EV charging infrastructure is further expanding the use of halogen-free materials in emerging sectors such as electric mobility and consumer appliances.

Japan LSHF Flame Retardant Polypropylene Market: Advanced Electronics and High-Speed Rail Innovation

Japan’s LSHF polypropylene market is defined by precision engineering, miniaturization, and high-performance applications, particularly in electronics and transportation. The development of ultra-thin LSHF PP materials capable of maintaining high flame-retardant ratings is enabling their use in next-generation 6G smartphones, wearable devices, and compact electronics.

In the transportation sector, Japan continues to innovate in high-speed rail systems, incorporating LSHF PP into Shinkansen interiors to reduce weight while maintaining stringent fire safety standards. The material is also widely used in industrial robotics and offshore wind energy components, where durability and resistance to harsh environmental conditions are essential. Strict regulatory oversight under the Chemical Substances Control Law (CSCL) ensures environmental compliance, while advancements in magnesium hydroxide surface treatments and self-extinguishing compounds are enhancing product performance and safety.

South Korea LSHF Flame Retardant Polypropylene Market: Battery Innovation and Semiconductor Integration Driving Demand

South Korea is emerging as a strategic hub for LSHF polypropylene applications, particularly in the electric vehicle battery and semiconductor industries. Leading companies such as LG, Samsung, and SK are driving large-scale investments in battery manufacturing, creating strong demand for LSHF PP in battery cell carriers and safety components.

Technological innovations include the development of high-nickel battery materials integrated with LSHF polypropylene, capable of withstanding extreme temperatures without ignition, ensuring enhanced safety in energy storage systems. The material is also critical in semiconductor manufacturing equipment, where fire safety and chemical resistance are essential. Government initiatives such as the “K-Battery Development Strategy” are supporting R&D and offering incentives for safe, sustainable materials. Additionally, the growing adoption of recycled flame-retardant polypropylene aligns with global sustainability goals and circular economy practices, further strengthening South Korea’s position in the advanced materials market.

Low Smoke Halogen Free Flame Retardant Polypropylene Market Report Scope

Low Smoke Halogen Free Flame Retardant Polypropylene Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$766.4 Million

|

|

Market Size (2032)

|

$1522.2 Million

|

|

Market Growth Rate

|

10.3%

|

|

Segments

|

By Flame Retardant (Phosphorus-based, Nitrogen-based, Mineral-based, Synergists and Hybrid Systems), By Product Form (Ready-to-use Compounds, Masterbatches, Additive Powders and Pellets), By Type (UL 94 V-0 Grade, UL 94 V-1 Grade, UL 94 V-2 Grade, High-Heat Resistance Grades), By End-Use Industry (Electrical and Electronics, Automotive and Transportation, Building and Construction, Energy and Power, Industrial Manufacturing), By Processing Method (Injection Molding, Extrusion, Cable Extrusion, Blow Molding, 3D Printing), By Property (Low Smoke Density, Low Toxicity, High Impact Strength, UV-Stabilized, Chemical Resistant), By Distribution Channel (Direct Sales, Specialty Chemical and Polymer Distributors, Compounders and Third-party Processors)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, SABIC, Borealis AG, Clariant AG, Lanxess AG, Albemarle Corporation, Huber Advanced Materials, Avient Corporation, RTP Company, LyondellBasell Industries N.V., DuPont de Nemours, Inc., Mitsubishi Chemical Group Corporation, Teknor Apex Company, Inc., Adeka Corporation, Budenheim KG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Low Smoke Halogen Free Flame Retardant Polypropylene Market Segmentation

By Flame Retardant

- Phosphorus-based

- Nitrogen-based

- Mineral-based

- Synergists and Hybrid Systems

By Product Form

- Ready-to-use Compounds

- Masterbatches

- Additive Powders and Pellets

By Type

- UL 94 V-0 Grade

- UL 94 V-1 Grade

- UL 94 V-2 Grade

- High-Heat Resistance Grades

By End-Use Industry

- Electrical and Electronics

- Automotive and Transportation

- Building and Construction

- Energy and Power

- Industrial Manufacturing

By Processing Method

- Injection Molding

- Extrusion

- Cable Extrusion

- Blow Molding

- 3D Printing

By Property

- Low Smoke Density

- Low Toxicity

- High Impact Strength

- UV-Stabilized

- Chemical Resistant

By Distribution Channel

- Direct Sales

- Specialty Chemical and Polymer Distributors

- Compounders and Third-party Processors

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Low Smoke Halogen Free Flame Retardant Polypropylene Industry

- BASF SE

- SABIC

- Borealis AG

- Clariant AG

- Lanxess AG

- Albemarle Corporation

- Huber Advanced Materials

- Avient Corporation

- RTP Company

- LyondellBasell Industries N.V.

- DuPont de Nemours, Inc.

- Mitsubishi Chemical Group Corporation

- Teknor Apex Company, Inc.

- Adeka Corporation

- Budenheim KG

*- List not Exhaustive