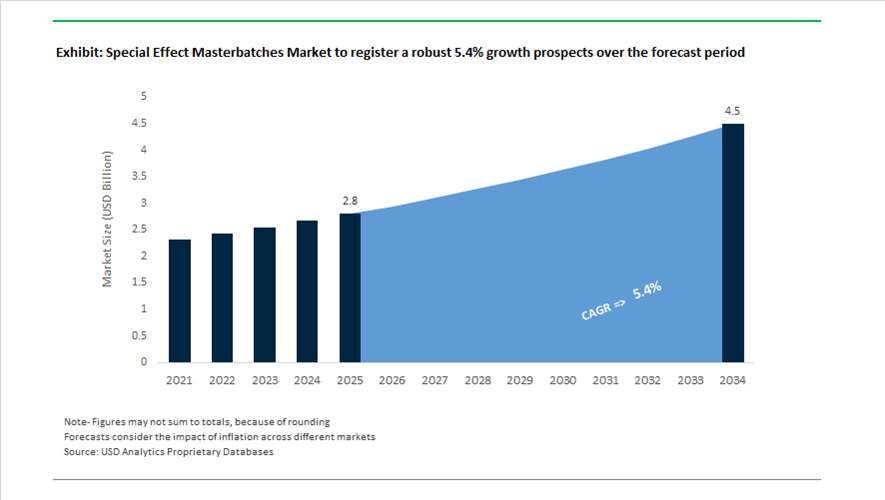

Special Effect Masterbatches Market Valuation 2025–2034: $2.8 Billion to $4.5 Billion at 5.4% CAGR Fueled by Premium Packaging Aesthetics and PFAS-Free Processing

The global special effect masterbatches market is valued at $2.8 billion in 2025 and is projected to reach $4.5 billion by 2034, expanding at a CAGR of 5.4%. Growth is driven by rising demand for metallic masterbatches, pearlescent effects, translucent colorants, graphene-enhanced additives, and high-opacity white formulations across rigid packaging, blow-molded bottles, oriented films, automotive interiors, aerospace components, and consumer electronics. Brand owners increasingly leverage visual differentiation through injection-molded metallic finishes, three-dimensional textures, high-gloss coatings, and minimalist semi-translucent aesthetics without secondary painting or lamination. Regulatory shifts toward non-PFAS processing aids and catalyst innovations that improve PET clarity are reshaping additive design and resin compatibility strategies.

In March 2024, LyondellBasell integrated the KARO® 5.0 laboratory stretching system at its Akron, Ohio facility, enhancing precision testing of special effect masterbatches for oriented film packaging and reducing development timelines for complex optical finishes. In early 2024, Ampacet introduced Matrix, a collection of highly pearlized colors tailored for blow-molded packaging targeting premium cosmetic and consumer goods segments. At Fakuma 2024, Avient debuted Colorant Chromatics™ Metallic Effect pre-colored sulfones, enabling aerospace and healthcare manufacturers to achieve gold, silver, and bronze finishes directly through molding while eliminating VOC-intensive secondary painting. In September 2024, Broadway launched GrapheneXcel, graphene-enhanced masterbatches delivering both mechanical reinforcement and dark metallic visual effects. In November 2024, Tosaf introduced its Special White range for extrusion coatings, engineered for extreme opacity and gloss stability on high-speed packaging lines. Later in 2024, Ampacet launched HyperLustre, a semi-translucent collection designed to deliver subtle luminosity aligned with minimalist packaging trends.

Capacity expansion and geographic diversification accelerated in 2025. In October 2025, Gabriel-Chemie completed a €6.5 million expansion at its Nyíregyháza, Hungary plant, increasing production lines from 10 to 19 and strengthening output of high-end effect masterbatches for European packaging and automotive markets. In mid-2025, Ampacet introduced the Cell-Struct 3D Effect Collection, creating visually textured surfaces without requiring complex mold tooling, reducing capital costs for rigid packaging producers. These innovations emphasize surface illusion engineering and material-efficient design as brand differentiation tools.

Strategic technology upgrades continued into 2026. In late 2025, Clariant announced commercialization of AddWorks™ titanium-based catalyst solutions in 2026, replacing antimony catalysts in polyester production and improving PET clarity and color performance for premium special effect applications. In January 2026, Avient expanded its Hiformer™ liquid masterbatch portfolio to include non-PFAS process aids for polyolefin films in Asia, ensuring high optical clarity while aligning with fluorochemical restrictions. The same month, Gabriel-Chemie announced the opening of a Nairobi hub scheduled for spring 2026, strengthening access to Sub-Saharan Africa’s growing packaging sector. These developments demonstrate how advanced catalyst systems, PFAS-free processing technologies, graphene-enabled aesthetics, and regional manufacturing investments are shaping the competitive evolution of the special effect masterbatches market toward $4.5 billion by 2034.

Key Trends and Strategic Opportunities in the Special Effect Masterbatches Market

Strategic Premiumization through Visual Sensory Packaging

Special effect masterbatches are increasingly central to premium brand strategy rather than a secondary aesthetic choice. Consumer packaged goods companies are deploying chroma-shift pigments, iridescent finishes, and soft-touch or matte textures as visual trust signals that communicate quality, authenticity, and price positioning without relying on text or labeling. This is particularly visible in prestige beauty, personal care, and premium spirits, where packaging functions as a non-verbal brand asset.

Investment patterns validate this shift. The Estée Lauder Companies disclosed in late 2024 that 71% of its packaging by weight now aligns with its internal 5 Rs sustainability framework, while simultaneously expanding luxury fragrance lines. These launches increasingly combine refillable glass with masterbatch-enhanced plastic components that reduce overall packaging weight by roughly 40%, yet preserve the visual depth and weighted tactile feel expected in the luxury segment.

Brand differentiation is also evolving toward advanced surface finishes. Cosmetics and haircare launches in 2025 show accelerated adoption of liquid-metal, satin-matte, and soft-touch effects. Masterbatch suppliers such as M. Holland report that brand-sensitive categories including deodorants and shampoos are now specifying carrier resins with up to 100% post-consumer recycled content. This enables global brands such as Dove and TRESemmé to retain iconic metallic effects and color consistency while meeting aggressive sustainability targets, elevating special effect masterbatches from decorative inputs to strategic brand enablers.

Automotive OEM Pivot toward EV-Specific Aesthetic Identities

The rapid growth of electric vehicles is redefining exterior and interior design language across the automotive sector. As grille-heavy architectures disappear, large continuous plastic surfaces have become dominant visual elements, increasing reliance on high-performance special effect pigments to communicate technology leadership and brand differentiation. This has shifted color and effect selection from styling preference to a core OEM specification parameter.

According to BASF Automotive Color Trends 2024–2025 report titled ROUTING, OEMs are gravitating toward liquid-metal finishes, intense purples, and high-chroma effects that convey futurism and digital sophistication. In Asia-Pacific markets, shades such as SCINTILLATION are gaining traction, using low-emission pigment technologies that deliver metallic depth while aligning with stricter environmental standards for EV manufacturing.

Specification rigor is also increasing. Automotive OEMs now routinely mandate light-fastness ratings of 7 to 8 on the standard scale for exterior plastics. Data shared by Veeraco Colourants in 2025 highlights surging demand for Quinacridone and Perylene pigments in deep reds and maroons, particularly for premium trim levels. These pigments allow OEMs to justify higher price points while maintaining long-term color stability under UV exposure and thermal cycling, reinforcing the role of special effect masterbatches as value drivers in EV platform differentiation.

Integration of Bio-Aesthetic and Recyclate-Compatible Effects

One of the most compelling growth opportunities in the special effect masterbatches market lies in resolving the long-standing conflict between visual impact and recyclability. Traditional metallic and pearlescent masterbatches often rely on carbon black or metal flakes that disrupt Near-Infrared sorting systems, contaminating post-consumer resin streams. As sustainability becomes non-negotiable, demand is accelerating for effects that are fully compatible with mechanical recycling infrastructure.

The sustainable packaging market is projected to reach approximately USD 117 billion by the end of 2025, intensifying the need for NIR-detectable blacks, mineral-based pearlescents, and heavy-metal-free pigments. Masterbatch suppliers that can deliver high-impact aesthetics without compromising recyclate purity are positioned to secure preferred supplier status with global CPG brands.

Technical performance further strengthens this opportunity. Studies conducted in 2024 on HDPE dimensional stability show that certain organic pigments act as nucleating agents, introducing 2 to 3% variance in shrinkage and warpage. This has created demand for low-warpage special effect masterbatches engineered specifically for thin-wall packaging and precision automotive components using recycled polymers. These formulations address both aesthetic and processing challenges, enabling broader adoption of PCR materials in high-visibility applications.

High-Value Functional Effect Hybrids for Smart Electronics

A second high-margin opportunity is emerging at the intersection of aesthetics and functionality. Electronics, wearables, and smart home devices increasingly require housings that deliver visual differentiation while embedding performance attributes such as antimicrobial resistance, UV stability, or anti-static behavior. This convergence is driving demand for hybrid masterbatches that combine special visual effects with functional additives in a single pellet.

Pricing dynamics underscore the value potential. Market data from 2025 indicates that standard color masterbatches typically trade between USD 1,800 and USD 2,500 per ton, while functional special effect variants command premiums ranging from USD 2,800 to USD 4,200 per ton. This delta reflects both formulation complexity and the direct value these hybrids provide to OEMs by reducing compounding steps and qualification time.

The transition toward mono-material designs in consumer electronics further amplifies this opportunity. To improve recyclability, manufacturers are eliminating multi-layer assemblies and coatings, increasing reliance on masterbatches that deliver a finished surface appearance such as brushed aluminum or edge-glow effects while simultaneously incorporating heat stabilizers and flame retardants. Suppliers capable of delivering these all-in-one solutions are positioned to become strategic partners in next-generation electronics platforms, where aesthetics, compliance, and circularity must coexist.

Special Effect Masterbatches Market Share and Segmentation Insights

Appearance Effect Masterbatches Lead the Market Through Premium Visual Differentiation

Appearance effect masterbatches accounted for 58.60% of the special effect masterbatches market in 2025, reflecting their dominant role in enhancing the visual appeal of plastic products. These masterbatches incorporate pigments and additives that create metallic, pearlescent, fluorescent, phosphorescent, and color-shifting effects, enabling manufacturers to produce visually distinctive plastic components. Industries such as packaging, automotive, and consumer goods rely on these effects to enhance product aesthetics and brand recognition. A key 2025 industry driver is the growing demand for premium packaging designs, where appearance masterbatches enable brands to create unique finishes and textures that stand out on retail shelves while offering a cost-effective alternative to secondary decoration techniques.

Packaging Industry Drives Demand for Special Effect Masterbatches in Consumer Branding

Packaging represents the largest end-use segment in the special effect masterbatches market, accounting for 42.80% of global demand in 2025 due to the strong role of visual differentiation in consumer product marketing. Packaging manufacturers use effect masterbatches to create metallic finishes for premium beverages, pearlescent effects for cosmetics packaging, and vibrant fluorescent colors for youth-oriented products. These effects enhance product visibility and reinforce brand identity in competitive retail environments. A significant 2025 market trend is the convergence of visual differentiation with sustainable packaging design, where manufacturers develop masterbatch systems compatible with mono-material recyclable packaging structures, while exploring bio-based carrier resins and renewable pigment technologies to support sustainability-focused packaging strategies.

Special Effect Masterbatches Market Competitive Landscape

The global special effect masterbatches market in 2026 is driven by functional aesthetics, PFAS-free formulations, and smart packaging integration. Industry leaders are advancing pearlescent effects, laser-marking additives, and recyclable masterbatch solutions to meet circular economy mandates and enhance brand differentiation across packaging, automotive, and healthcare sectors.

Avient Expands Non-PFAS Specialty Masterbatches and Recycled Content Solutions for High-Performance Applications

Avient Corporation is strengthening its leadership in specialty masterbatches through its transition toward high-margin, sustainable additives, supported by strategic portfolio realignment and the integration of Dyneema® technologies. Its Hiformer™ liquid masterbatch expansion introduces non-PFAS process aids for polyolefin films, enabling high-clarity optical effects under regulatory compliance. The OnColor™ SenseAction™ platform delivers combined organoleptic protection and metallic or pearlescent finishes for sensitive beverage packaging. Avient’s Edgetek™ REC PC solutions enable compatibility with 35%–98% post-consumer recycled polycarbonate, supporting circular economy targets. The company’s focus on functional aesthetics and sustainable materials enhances its positioning in premium consumer and industrial applications. Its innovation strategy aligns with demand for high-performance, recyclable masterbatch systems.

Ampacet Advances TiO2-Free Pearlescent Masterbatches and Laser-Marking Solutions for Sustainable Packaging and Healthcare

Ampacet Corporation is leading innovation in special effect masterbatches through its HyperLustre collection, offering TiO2-free pearlescent effects designed for recyclable PET packaging. Its ProVital™+ LaserMark solutions enable high-contrast, permanent marking for medical devices, integrating traceability with healthcare-compliant materials. The company’s Digital Design Library accelerates product development by enabling virtual prototyping of complex aesthetic effects. Natura Jet introduces a bio-derived alternative to carbon black, delivering superior jetness for electronics while reducing environmental impact. Ampacet’s focus on disruptive aesthetics and sustainable materials aligns with circular packaging requirements. Its ability to combine visual differentiation with functional performance strengthens its competitive advantage.

LyondellBasell Strengthens Circular Masterbatch Production and Paint-Free Automotive Solutions Through Integrated Feedstock Advantage

LyondellBasell is leveraging its integrated production model to expand high-performance masterbatch applications within its Advanced Polymer Solutions segment. Its Channelview propylene project ensures a secure supply of carrier resins for high-load special effect masterbatches used in automotive and durable goods. Strategic divestment of low-margin assets enables greater focus on specialty applications in Europe and North America. The company’s “Paint-Free” automotive solutions utilize metallic-effect polymers to eliminate traditional coating processes, reducing environmental impact and manufacturing complexity. Strong cash flow improvements support reinvestment in circular and high-value polymer technologies. Its feedstock advantage and scale position it as a key player in sustainable masterbatch innovation.

Clariant Accelerates PFAS-Free Additive Innovation and Bio-Based Masterbatch Development for Circular Applications

Clariant is advancing purpose-led innovation in special effect masterbatches through its PFAS-free additive portfolio and bio-based chemistry initiatives. With a 17.8% EBITDA margin in 2025, the company is reinvesting in renewable feedstocks and blue hydrogen projects to decarbonize production. Its new North American facility supports pharmaceutical-grade additives for healthcare masterbatch applications. The Aristoflex SUN innovation demonstrates Clariant’s capability to integrate sensory and haptic properties into plastic surfaces, expanding functionality beyond visual effects. Its PFAS-free solutions enable matte and soft-touch finishes without restricted processing aids. Clariant’s focus on sustainability and advanced materials strengthens its position in next-generation masterbatch technologies.

Gabriel-Chemie Enhances Smart Packaging and CO2-Reduced Masterbatches with NIR-Detectable Pigment Innovation

Gabriel-Chemie Group is positioning itself as a niche innovation leader in special effect masterbatches, supported by expanded production facilities in Hungary and Austria. Its Colour Vision collections deliver trend-driven aesthetic solutions tailored for premium packaging and lifestyle applications. The company’s laser-marking masterbatches provide durable, tamper-evident solutions for food packaging and industrial applications. Its CO2-reduced white masterbatch minimizes reliance on titanium dioxide, addressing sustainability and regulatory pressures. Integration of NIR-detectable pigments enables accurate sorting of dark and metallic plastics in automated recycling systems. Gabriel-Chemie’s focus on smart packaging and recyclability enhances its competitiveness in circular material solutions.

United States Special Effect Masterbatches Market Accelerated by PFAS-Free Innovation and Onshoring

The United States special effect masterbatches market is being reshaped by sustainability mandates, domestic capacity expansion, and advanced functional aesthetics. At NPE 2024, Avient Corporation introduced ColorMatrix Capture oxygen scavenger technology alongside the Cesa Non-PFAS process aid portfolio, enabling special effect pigments to retain chromatic intensity and visual depth in recycled PET packaging. These innovations address a critical technical challenge in rPET, where residual contaminants often compromise metallic and pearlescent effects. Capacity expansion has followed innovation. In late 2024, Avient announced construction of a new manufacturing facility in Norwalk, Ohio, purpose-built to scale advanced additive and effect masterbatches for North American sustainable packaging and high-performance film applications.

Regulatory pressure has further accelerated portfolio transitions. Following the EPA’s December 2024 PFAS rulings, U.S. producers such as Ampacet have fully migrated special effect offerings to fluoro-free carrier systems, targeting food-contact and industrial film markets. Ampacet’s 2025 launch of the HyperLustre Collection demonstrates how proprietary dispersion technology can deliver glass-like luminosity in HDPE without heavy metal content. Beyond packaging, federal investment under the CHIPS and Science Act has catalyzed development of electrically conductive and laser-markable effect masterbatches for automotive interiors and electronic housings. Trade policy has reinforced onshoring, with U.S. supply chains increasingly localized for high-value metallic and interference flakes to reduce reliance on East Asian imports.

Germany Special Effect Masterbatches Market Anchored by Circular Economy and Automotive Integration

Germany remains a global reference market for high-end special effect masterbatches, driven by circular economy mandates and automotive design leadership. Under the EU 2025–2030 Circular Economy Action Plan, German producers have led development of PCR-compatible effects that compensate for color instability in recycled polymers. Clariant, now part of Avient, introduced chrome-effect masterbatches engineered to neutralize yellowing in post-consumer recycled resins, supporting premium packaging and consumer goods applications.

Safety and performance standards continue to tighten. At K 2025, Ampacet unveiled Halolite 527 and Halofree 533 flame-retardant effect masterbatches for polypropylene electrical components, compliant with EN 50642 low-toxicity emission requirements. Germany also remains the epicenter for prestige packaging aesthetics. Gabriel‑Chemie Group established a dedicated research center in 2024 focused on bio-based carriers for pearlescent and liquid-look metallic finishes in luxury cosmetics. In automotive interiors, OEMs such as Volkswagen and BMW have integrated soft-touch effect masterbatches into 2025–26 models, eliminating secondary painting and reducing VOC emissions. Adoption of the GreenScreen for Safer Chemicals framework has further positioned Germany as a leader in heavy-metal-free metallic and iridescent effects.

China Special Effect Masterbatches Market Defined by Export Scale and Multifunctional Integration

China dominates global special effect masterbatch exports, accounting for 29.1% of worldwide shipments valued at more than USD 4.5 billion in 2025. This scale is increasingly aligned with sustainability policy. Government-driven Green Mode of Production guidelines have accelerated the shift toward eco-friendly pigment dispersions and high-purity carrier systems. Industrial integration is deepening, as BASF SE commissioned a multifunctional masterbatch line at its Zhanjiang Verbund site during 2024–25, combining special effects with UV stabilization and antimicrobial functionality for packaging and consumer goods.

China’s electronics manufacturing dominance is also shaping aesthetics. Local suppliers are scaling thermochromic and photochromic masterbatches for smartphones and consumer devices, enabling dynamic color response to heat and UV exposure. Laser-markable, ink-free additives have reached commercial scale, allowing permanent coding on metallic-look plastics without surface damage. Regulatory standardization is reinforcing quality. Implementation of GB 4806.16-2025 has imposed strict limits on volatile residues in food-contact masterbatches, accelerating adoption of high-purity organic pigments and reinforcing China’s competitiveness in regulated export markets.

India Special Effect Masterbatches Market Driven by Construction Aesthetics and Bio-Based Carriers

India’s special effect masterbatches industry is expanding through infrastructure demand, policy support, and FMCG premiumization. Masterbatch exports reached USD 1.61 billion in the 2024–25 cycle, with domestic leaders such as Plastiblends India Limited expanding R&D capacity in 2025 to develop stone, granite, and marble effects tailored for construction and architectural plastics. These mineral-inspired effects are gaining traction in façade panels, pipes, and interior fittings.

Policy stimulus is accelerating material innovation. The BioE3 Policy approved in August 2024 has incentivized bio-based masterbatch carriers, leading to the introduction of biodegradable metallic effects for agricultural films. FMCG growth is reshaping packaging aesthetics, with pearlescent and sparkle-mist masterbatches increasingly specified for premium personal care and homecare containers. In textiles, Indian producers have advanced dope-dyed special effect masterbatches that embed glitter and metallic effects directly into synthetic fibers, reducing water usage by eliminating post-dyeing processes.

Australia and New Zealand Special Effect Masterbatches Market Focused on Durability and Regional Consolidation

Australia and New Zealand represent a niche but strategically important market characterized by climate-driven performance requirements. In July 2025, Ampacet completed the acquisition of Allied Color and Additives, expanding its regional footprint with a focus on functional additive and effect masterbatches. Production priorities in 2025 have centered on UV-stabilized special effects for building and construction materials, engineered to maintain color fidelity under extreme oceanic and high-UV conditions. This emphasis on durability positions the region as a testing ground for long-life aesthetic performance.

Comparative Snapshot: Country-Level Special Effect Masterbatches Dynamics

Special Effect Masterbatches Market County Level Snapshot

|

Country / Region

|

Primary Demand Drivers

|

Strategic Focus Areas

|

Structural Impact

|

|

United States

|

Sustainable packaging, automotive, electronics

|

PFAS-free effects, onshored pigment supply

|

Regulatory-led innovation and capacity build-out

|

|

Germany

|

Automotive interiors, luxury packaging

|

PCR-compatible effects, low-toxicity systems

|

Circular economy leadership

|

|

China

|

Consumer electronics, exports

|

Multifunctional masterbatches, laser marking

|

Global scale with regulatory alignment

|

|

India

|

Construction, FMCG, textiles

|

Mineral effects, bio-based carriers

|

Rapid domestic and export growth

|

|

Australia & New Zealand

|

Construction durability

|

UV-stabilized effects

|

Climate-resilient specialization

|

Special Effect Masterbatches Market Report Scope

Special Effect Masterbatches Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Effect Type (Appearance Effects, Functional Effects, Material & Texture Effects), By Carrier Resin (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene, Engineering Plastics, Bio-Based Carriers), By End-Use Industry (Packaging, Automotive, Consumer Goods & Electronics, Hygiene & Medical Products, Building & Construction, Sports & Leisure)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avient Corporation, Ampacet Corporation, Clariant AG, LyondellBasell Industries N.V., Cabot Corporation, Plastiblends India Limited, Tosaf Group, Gabriel-Chemie Group, Kafrit Group, Americhem Inc., RTP Company, Sudarshan Chemical Industries Ltd., Penn Color Inc., Global Colors Group, Broadway Colours

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Special Effect Masterbatches Market Segmentation

By Effect Type

- Appearance Effects

- Functional Effects

- Material & Texture Effects

By Carrier Resin

- Polyethylene

- Polypropylene

- Polyethylene Terephthalate

- Polystyrene

- Engineering Plastics

- Bio-Based Carriers

By End-Use Industry

- Packaging

- Automotive

- Consumer Goods & Electronics

- Hygiene & Medical Products

- Building & Construction

- Sports & Leisure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Special Effect Masterbatches Industry

- Avient Corporation

- Ampacet Corporation

- Clariant AG

- LyondellBasell Industries N.V.

- Cabot Corporation

- Plastiblends India Limited

- Tosaf Group

- Gabriel-Chemie Group

- Kafrit Group

- Americhem Inc.

- RTP Company

- Sudarshan Chemical Industries Ltd.

- Penn Color Inc.

- Global Colors Group

- Broadway Colours

*- List not Exhaustive