Plastic Coatings Market Size, Lightweight Materials Demand, and Sustainable Coating Technologies

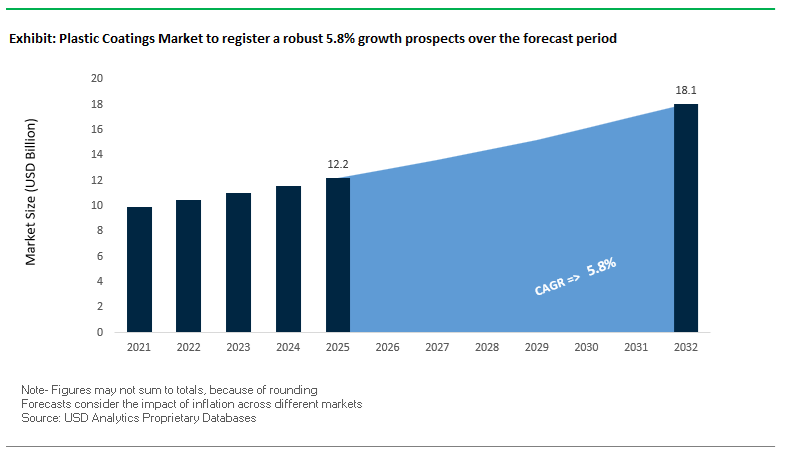

The global Plastic Coatings Market was valued at $12.2 billion in 2025 and is projected to expand at a CAGR of 5.8% through 2032, reaching $18.1 billion by 2032. This growth is driven by the rising use of polymer-based components across automotive, electronics, appliances, packaging, and aerospace industries, where coatings enhance surface durability, aesthetics, chemical resistance, and functional performance.

A core structural driver is the global transition toward lightweight materials, particularly in automotive and consumer electronics, where plastics are replacing metals to improve energy efficiency and design flexibility. However, plastic substrates require specialized coatings to address limitations such as scratch sensitivity, UV degradation, and poor surface adhesion. This is accelerating demand for advanced coating systems, including waterborne, UV-curable, and powder coatings tailored for heat-sensitive substrates.

Sustainability is becoming a defining factor in product development. The market is witnessing increasing adoption of low-VOC, waterborne, and circular coating technologies, alongside innovations that incorporate recycled materials into coating formulations. Regulatory pressure and corporate decarbonization targets are pushing manufacturers to develop coatings that not only protect plastic components but also contribute to reduced lifecycle emissions and improved recyclability.

Additionally, the growing complexity of multi-material assemblies and smart devices is driving demand for coatings with multi-functional properties, such as electromagnetic shielding, anti-fingerprint surfaces, soft-touch finishes, and enhanced haptics. Regional growth is particularly strong in Asia-Pacific, supported by expanding manufacturing ecosystems in automotive, electronics, and industrial production.

Market Analysis: Strategic Divestments, Circular Coating Innovation, and Regional Manufacturing Expansion Driving Market Evolution

Recent developments in the Plastic Coatings Market highlight a convergence of portfolio restructuring, sustainability innovation, and regional capacity expansion. A major structural shift is BASF’s €7.7 billion divestment of a majority stake in its coatings business, expected to close in 2026. This move creates a standalone coatings entity with strong exposure to plastic-intensive applications, particularly in automotive interiors and exterior components, reshaping competitive dynamics across the market.

Sustainability-led product innovation is accelerating. PPG’s ENVIROLUXE™ Plus (May 2025) introduces powder coatings formulated with recycled plastic content, enabling manufacturers to align with circular economy principles while maintaining performance standards. Similarly, PPG’s ENVIROCRON® Extreme Protection Edge Plus (October 2025) is being adapted for heat-sensitive plastic substrates, offering enhanced edge coverage without high-temperature curing that could damage polymers.

Regional manufacturing and supply chain strategies are becoming increasingly critical. PPG’s waterborne automotive coatings plant in Thailand (March 2025) supports Southeast Asia’s automotive sector with low-VOC coatings for plastic components, while AkzoNobel’s new Dubai blending and distribution hub (2026) enhances access to specialized coatings for aviation and electronics applications in the Middle East.

Market consolidation and expansion are also shaping growth trajectories. Sherwin-Williams’ integration of Suvinil (January 2026) strengthens its presence in Latin America’s consumer electronics and appliance coatings segments, where demand for plastic coatings is increasing. Meanwhile, BASF India’s localized divestment (March 2026) ensures continuity in supply chains as the global restructuring unfolds.

Innovation in design and functionality is further differentiating market offerings. Mankiewicz’s “2026 Colors of the Year” (November 2025) highlights the growing importance of tactile and aesthetic coatings for plastic surfaces, particularly in automotive interiors. At the same time, Fujikura Composites’ “Accelerate X” strategy (April 2026) focuses on expanding high-performance plastic coatings for EV and digital hardware applications, reinforcing the role of coatings in next-generation technologies.

Market Trend: Waterborne Polyurethane Coatings Advancing Automotive Interior Air Quality and Compliance Standards

The plastic coatings industry is undergoing a major transformation as automotive OEMs standardize waterborne polyurethane coatings for interior plastic components, including ABS, PC/ABS, and TPO substrates. This shift is driven by increasingly stringent indoor air quality requirements, consumer sensitivity to cabin odor, and regulatory pressure to reduce volatile organic compound emissions from vehicle interiors.

Waterborne polyurethane dispersions enable ultra-low VOC formulations, typically below 50 g/L, compared to 450 to 600 g/L associated with legacy solvent-borne acrylic-urethane systems. This substantial reduction in emissions aligns with global automotive standards for interior air quality and supports compliance with evolving environmental regulations across major markets.

Performance characteristics have reached parity with solvent-based systems. Modern soft-touch WPU coatings achieve top-tier chemical resistance, maintaining a Rating 5 in sunscreen and skin-oil exposure tests. This ensures long-term durability of high-contact surfaces such as dashboards, armrests, and door panels. In addition, these coatings contribute to a reduction in overall carbon footprint of up to 45%, supporting automotive sustainability targets.

Odor performance is a critical differentiator. According to standardized sensory testing, WPU-coated components consistently achieve low odor intensity scores in the range of 2.0 to 2.5, indicating perceptible but non-intrusive emissions. This represents a significant improvement over solvent-borne coatings, which often exceed 3.5 and contribute to the undesirable “new car smell.” These combined attributes are positioning waterborne polyurethane coatings as the preferred solution for next-generation automotive interiors.

Market Trend: UV-Curable Hard Coatings Enhancing Scratch Resistance and Longevity in Consumer Electronics Plastics

The consumer electronics segment is driving strong demand for ultra-hard UV-curable coatings designed to improve the durability and aesthetic retention of plastic housings. As devices become thinner and more design-centric, manufacturers are increasingly applying glass-like protective coatings to polycarbonate and PMMA substrates to extend product lifecycle and maintain premium appearance.

Advanced UV-curable coatings now achieve 9H pencil hardness on plastic surfaces, enabled by the incorporation of nano-silica and ceramic-reinforced additives within the polymer matrix. This level of hardness provides exceptional resistance to scratches, abrasion, and daily wear, addressing common issues such as surface dulling and micro-scratching in high-use consumer devices.

Processing efficiency has improved significantly with the adoption of UV-LED curing technology. Compared to traditional mercury vapor lamps, UV-LED systems reduce energy consumption by approximately 70% while enabling instant curing. This eliminates dust contamination during cooling and supports high-throughput manufacturing environments with minimal downtime.

Abrasion resistance metrics further reinforce performance gains. In standardized Taber abrasion testing, these coatings maintain haze increases below 2% after 1,000 cycles, preserving optical clarity for high-gloss finishes such as piano black and transparent surfaces. These properties are driving widespread adoption of UV-curable coatings across smartphones, wearables, and other consumer electronics applications.

Market Opportunity: EPA NESHAP Revisions Driving Rapid Adoption of Low-HAP Plastic Coating Technologies

Regulatory updates in the United States are creating a strong impetus for the adoption of low-emission coating technologies in the plastic coatings industry. The 2026 revisions to federal standards governing hazardous air pollutant emissions from surface coating operations introduce tighter limits on organic emissions and eliminate operational exemptions previously allowed during startup and shutdown phases.

The updated emission threshold of 0.16 kilograms of organic hazardous air pollutants per kilogram of coating solids significantly restricts the use of high-solvent formulations. Facilities are now required to maintain continuous compliance over rolling 12-month periods, increasing the operational risk associated with non-compliant coating systems.

These regulatory pressures are accelerating the transition toward waterborne polyurethane and UV-curable coating technologies, which inherently meet low-HAP and low-VOC requirements. Manufacturers adopting these systems can avoid the need for capital-intensive emission control equipment such as regenerative thermal oxidizers, improving both compliance efficiency and cost structure.

This regulatory environment is expected to drive sustained demand for advanced, low-emission coating chemistries across automotive, consumer goods, and industrial plastic applications.

Market Opportunity: China VOC Phase 4 Action Plan Driving Localization of Waterborne and Low-Emission Plastic Coatings

China’s implementation of the VOC Phase 4 Action Plan is creating significant growth opportunities for the plastic coatings industry by mandating stricter emission controls and promoting the adoption of environmentally compliant technologies. The updated regulatory framework introduces tighter VOC limits for plastic part coatings and establishes clear targets for the adoption of low-emission solutions.

The revised national standards impose a maximum VOC content of 420 g/L for solvent-borne coatings, with strong policy incentives for manufacturers achieving levels below 200 g/L. This is driving a shift away from traditional solvent-based systems toward waterborne, powder, and UV-curable coatings that can meet or exceed these thresholds.

The policy also emphasizes localization of advanced coating technologies, targeting a 60% adoption rate for low-VOC solutions in key industrial regions by 2030. This is particularly relevant in major manufacturing hubs such as the Yangtze River Delta and Pearl River Delta, where environmental enforcement is most stringent.

Additional regulatory measures targeting hazardous substances, including stricter limits on hexavalent chromium content, are reinforcing the transition toward safer and more sustainable coating systems. These combined regulatory and industrial drivers are expected to accelerate innovation and investment in waterborne and high-performance plastic coatings across China’s manufacturing ecosystem.

Plastic Coatings Market Share and Segmentation Insights

ABS Captures 24.9% Share Driven by Coating Compatibility and Interior Automotive Applications

The plastic coatings market by plastic substrate is dominated by ABS (Acrylonitrile Butadiene Styrene), accounting for 24.9% of global market share in 2025, owing to its exceptional coating adhesion properties and widespread use in automotive interiors. ABS and ABS/PC blends are extensively utilized in dashboard components, trims, control panels, and electronic housings, where coatings provide UV resistance, scratch protection, soft-touch finishes, and decorative aesthetics. A key advantage of ABS is its ability to accept a wide range of coating technologies, including waterborne coatings, solvent-borne paints, and UV-curable systems, without requiring aggressive surface pretreatment. This ease of coating significantly reduces processing complexity and cost, making ABS the most coatable engineering thermoplastic. As demand for high-performance plastic coatings in automotive, electronics, and consumer goods continues to rise, ABS remains the leading substrate in the global plastic coatings market.

Contract Coaters Hold 48.5% Share Driven by Surface Activation and Low-Temperature Processing Expertise

In the plastic coatings market by sales channel, third-party coating service providers lead with a 48.5% market share in 2025, reflecting the technical challenges associated with coating diverse plastic substrates. Many plastics such as polypropylene (PP), polyethylene (PE), and polyamide (nylon) require advanced surface activation techniques—including corona treatment, plasma treatment, and flame treatment—to achieve proper coating adhesion. Contract coaters offer these specialized processes as part of integrated coating solutions. Additionally, plastic substrates are highly sensitive to heat, necessitating low-temperature curing technologies such as UV curing and low-bake ovens (50–80°C), which are often unavailable in standard in-house paint lines. These capabilities make outsourced providers essential for industries such as automotive, consumer electronics, and packaging, reinforcing their dominance in the global plastic coatings services market.

Competitive Landscape of the Plastic Coatings Market

AkzoNobel Leads Sustainable Plastic Coatings Innovation with AI and Circular Technologies

AkzoNobel N.V. is a global leader in the plastic coatings market, leveraging its sustainability-driven “Rhythm of Blues” strategy. In 2026, the company announced a merger with Axalta, creating the world’s largest performance coatings entity with strong R&D capabilities and projected synergies of $600 million. AkzoNobel has strengthened profitability through pricing strategies and cost optimization, while maintaining leadership in low-VOC waterborne and powder coatings for plastics. Its innovation in “Coatings on Command” introduces removable and repairable polymer films, enhancing recyclability. Additionally, its AI-powered inspection tools are being adapted for large-scale plastic infrastructure applications.

PPG Drives High-Performance Plastic Coatings with Advanced Scratch-Resistant and EV Solutions

PPG Industries, Inc. is a key player in the plastic coatings market, particularly in automotive and electronics applications, which account for a significant share of global demand. In Q1 2026, the company reported strong revenue growth supported by high-performance coating technologies. PPG has introduced next-generation scratch-resistant coatings that improve durability by over 40%, addressing critical performance challenges in automotive interiors. The company is also deeply integrated into the EV supply chain, providing dielectric and EMI/RFI shielding coatings for battery housings and sensor systems. Its continued investment in R&D reinforces its leadership in high-performance and functional plastic coatings.

Sherwin-Williams Expands Market Share with High-Efficiency Coating Systems and Bio-Based Solutions

The Sherwin-Williams Company continues to strengthen its position in the plastic coatings market through its focus on high-margin industrial applications. In 2026, the company achieved strong financial performance, driven by growth in its industrial coatings segment. Its Sher-Bar TEC technology offers smooth-finish coatings with enhanced chemical resistance, reducing application and curing times by up to 20%. The integration of Suvinil has expanded its footprint in South America, particularly in construction and appliance coatings. Sherwin-Williams is also increasing its portfolio of bio-based coatings with over 25% renewable content, aligning with sustainability standards and ESG requirements.

BASF Enhances Plastic Coating Performance with Advanced Stabilizers and Circular Economy Solutions

BASF SE is a major innovator in the plastic coatings market, focusing on extending the lifecycle and performance of plastic materials. In 2026, the company introduced the Tinuvin® NOR® platform, improving UV stability in applications such as agricultural films and solar infrastructure. BASF’s expertise in light stabilizers and thermal protection additives ensures durability in harsh environments. Its “Make, Use, Recycle” strategy integrates advanced technologies such as trinamiX spectroscopy to improve material identification and recycling efficiency. BASF also leads in biocompatible and flexible coatings for medical and e-mobility applications, strengthening its presence in high-growth sectors.

Axalta Strengthens Mobility Coatings Leadership with UV-Stable and Digital Color Technologies

Axalta Coating Systems is a leading player in the plastic coatings market, particularly in automotive and mobility applications. Prior to its merger with AkzoNobel, the company achieved record financial performance with strong EBITDA margins. Axalta’s innovations include UV-stable coatings that improve color retention on plastic components, enhancing long-term durability and vehicle aesthetics. Its “2026 A Plan” focuses on high-growth mobility markets, including the development of PVD-on-plastic alternatives to chrome plating. The company’s digital color matching ecosystem ensures high accuracy in coating applications, reinforcing its leadership in advanced coating technologies for plastics.

Nippon Paint Expands APAC Leadership with Functional and Antimicrobial Plastic Coatings

Nippon Paint Holdings is a dominant force in the Asia-Pacific plastic coatings market, which accounts for a significant share of global demand. The company is pursuing a “Granularity of Growth” strategy, leveraging local partnerships and acquisitions to expand its market presence. Its DGL Pacific division is driving growth in antimicrobial plastic coatings, particularly in public transport and healthcare applications. Nippon Paint is also investing in advanced functional coatings such as heat-shielding and self-healing films, addressing emerging market needs. Its strong regional presence and innovation focus position it as a key competitor in the global plastic coatings industry.

China Plastic Coatings Market: Dual-Carbon Transition and Ultra-High Purity PVD Innovation

China continues to lead the global plastic coatings market, transitioning from high-volume production toward ultra-high purity (UHP) coatings on advanced engineering plastics to support industries such as New Energy Vehicles (NEVs), semiconductors, and 6G infrastructure. The enforcement of GB 30981.1-2025 has accelerated the shift to water-borne UV plastic coatings, significantly reducing VOC emissions across key industrial clusters in Guangdong and Zhejiang.

Regulatory advancements such as GB 4806.10-2025 are reshaping food-grade plastic coatings by expanding approved raw materials while enforcing strict safety thresholds. Technological progress is evident in magnetron sputtering on PEEK and polyimide substrates, enabling ultra-clean coatings for semiconductor applications. Automotive demand is also rising, particularly for backlit PVD-coated plastic interiors in smart cabins. Large-scale investments, including the Meishan Industrial Base expansion, and policy incentives promoting closed-loop solvent recovery systems are strengthening China’s leadership in high-performance and sustainable plastic coating technologies.

Germany Plastic Coatings Market: Circular Economy Leadership and Blue Angel Compliance

Germany is at the forefront of sustainable plastic coatings, driven by strict environmental regulations and circular economy initiatives. The phase-out of traditional chrome plating under EU REACH Annex XIV has led to widespread adoption of PVD-coated PC/ABS materials for automotive applications, offering improved durability and environmental compliance.

Innovation is focused on digital traceability and recyclability, with embedded markers enabling automated sorting of metallized plastics with high accuracy. The development of HiPIMS-based coating technologies is achieving densities comparable to electroplating, while low-temperature deposition processes allow coatings on heat-sensitive polymers without deformation. Germany’s Blue Angel eco-label criteria are further encouraging the adoption of recyclable plastic coatings, while research into biodegradable lubricants is expanding applications in renewable energy sectors such as offshore wind.

United States Plastic Coatings Market: Aerospace Lightweighting and FDA-Grade Medical Applications

The U.S. plastic coatings market is undergoing rapid transformation, driven by aerospace innovation, healthcare applications, and environmental regulations. Aerospace manufacturers are increasingly adopting PVD-coated CFRP components, enabling significant weight reduction while maintaining structural integrity.

In the healthcare sector, a growing number of companies are utilizing titanium-PVD coatings on medical-grade plastics to meet stringent biocompatibility and sterilization standards. Regulatory pressures such as the EPA NESHAP mandate are accelerating the replacement of traditional chrome plating with vacuum metallization technologies. Additionally, advancements in UV-LED curing systems are improving energy efficiency in coating processes. Federal investments linked to semiconductor expansion are also increasing demand for coated fluoropolymer components used in ultra-pure water systems, strengthening the U.S. position in high-performance plastic coatings.

India Plastic Coatings Market: Smart Cities Growth and PLI-Driven Manufacturing Expansion

India is emerging as one of the fastest-growing markets in the plastic coatings industry, supported by urbanization, government initiatives, and expanding manufacturing capabilities. Regulatory updates under the Plastic Waste Management Rules (2025/2026) are driving demand for coatings compatible with recycled plastics, encouraging innovation in sustainable coating formulations.

Government support through the PLI scheme expansion is promoting domestic production of PVD targets and coating materials, reducing import dependence. Infrastructure projects under the Smart Cities Mission are increasing the use of PVD-coated plastic hardware for durability in harsh environmental conditions. The rapid growth of consumer electronics manufacturing, particularly in Noida and Chennai, is boosting demand for high-volume plastic coating systems. Additionally, advancements in agritech, including PVD-metallized plastic sensors, are opening new application areas and strengthening India’s market position.

Japan Plastic Coatings Market: Precision Sputtering and Advanced Optical Applications

Japan continues to lead in high-precision plastic coatings, particularly in sectors such as advanced optics, telecommunications, and pharmaceutical packaging. The deployment of ultra-thin coatings for 6G smart surfaces is enabling building facades to function as signal reflectors in next-generation urban networks.

Innovations in PVD-coated PET barrier films are enhancing pharmaceutical packaging by extending shelf life without additional preservatives. The adoption of DMD-modulated sputtering technologies is enabling highly detailed textures in consumer electronics, while the growth of AR/VR devices is driving demand for anti-reflective coatings on plastic lenses with near-perfect light transmission. Updated standards such as JIS R 1703:2024 are setting global benchmarks for coating adhesion on recycled plastics, reinforcing Japan’s leadership in advanced material science.

South Korea Plastic Coatings Market: Semiconductor Precision and OLED Encapsulation

South Korea’s plastic coatings market is closely aligned with its dominance in semiconductors, OLED displays, and advanced packaging technologies. The development of plasma-resistant coatings for plastics is critical for 3D NAND and FinFET fabrication processes, particularly within the Gyeonggi-do semiconductor cluster.

The country leads in Thin-Film Encapsulation (TFE) using PVD-based inorganic layers to protect flexible OLED displays from environmental damage. Innovations in packaging include high-barrier coatings that block UV light and oxygen in food applications, while low-voltage curing technologies enable coating of heat-sensitive plastic substrates. Additionally, demand from the K-beauty sector is driving the adoption of PVD-metallized recycled plastic packaging, combining premium aesthetics with sustainability. Marine applications are also emerging, with the development of environmentally friendly anti-fouling coatings for plastic panels.

Brazil Plastic Coatings Market: Healthcare Growth and Bio-Based Coating Innovations

Brazil is emerging as a high-growth market in the plastic coatings sector, driven by increased healthcare investment and the adoption of sustainable materials. Rising demand for coated plastic medical devices and surgical instruments is supported by government funding for healthcare infrastructure.

The country’s leadership in bio-ethanol production is enabling the integration of renewable solvents into coating processes, supporting environmentally friendly manufacturing practices. Industrial developments, including expansions in agricultural machinery production, are boosting demand for PVD-coated plastic components. Additionally, R&D focused on improving UV resistance using advanced stabilizers is enhancing coating durability in high-solar environments. The expansion of retail distribution channels is further accelerating the adoption of premium plastic coatings, while localized production of sputtering targets is improving supply chain resilience.

Plastic Coatings Market Report Scope

Plastic Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.2 Billion

|

|

Market Size (2032)

|

$18.1 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Material (Polyurethane, Acrylic, Polyester, Epoxy, Silicone, Fluoropolymer, Vinyl, Bio-based), By Coating Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, Radiation-Cured, Electrophoretic Painting), By Plastic Substrate (ABS, Polycarbonate, Polypropylene, Polyethylene, Polyvinyl Chloride, Polyamide, PCR), By End-Use Industry (Automotive and Transportation, Building and Construction, Consumer Electronics, Packaging, Medical and Healthcare, Aerospace and Defense, Industrial Goods and Appliances), By Application Process (Spray Coating, Dip Coating, Flow, In-Mold Coating, Roll Coating), By Functional Property (Decorative and Aesthetic, Protective, UV-Resistance and Weatherability, Specialty), By Sales Channel (Direct Sales, Specialty Chemical Distributors, Third-party Coating Service Providers)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Axalta Coating Systems Ltd., BASF SE, Nippon Paint Holdings Co., Ltd., RPM International Inc., Kansai Paint Co., Ltd., Mankiewicz Gebr. and Co., Evonik Industries AG, Fujikura Kasei Co., Ltd., Red Spot Paint and Varnish Company, Inc., Zhejiang Juhua Co., Ltd., Sun Chemical Corporation, United Soft Coat Systems

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Coatings Market Segmentation

By Material

- Polyurethane

- Acrylic

- Polyester

- Epoxy

- Silicone

- Fluoropolymer

- Vinyl

- Bio-based

By Coating Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- Radiation-Cured

- Electrophoretic Painting

By Plastic Substrate

- ABS

- Polycarbonate

- Polypropylene

- Polyethylene

- Polyvinyl Chloride

- Polyamide

- PCR

By End-Use Industry

- Automotive and Transportation

- Building and Construction

- Consumer Electronics

- Packaging

- Medical and Healthcare

- Aerospace and Defense

- Industrial Goods and Appliances

By Application Process

- Spray Coating

- Dip Coating

- Flow

- In-Mold Coating

- Roll Coating

By Functional Property

- Decorative and Aesthetic

- Protective

- UV-Resistance and Weatherability

- Specialty

By Sales Channel

- Direct Sales

- Specialty Chemical Distributors

- Third-party Coating Service Providers

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Plastic Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Mankiewicz Gebr. & Co.

- Evonik Industries AG

- Fujikura Kasei Co., Ltd.

- Red Spot Paint & Varnish Company, Inc.

- Zhejiang Juhua Co., Ltd.

- Sun Chemical Corporation

- United Soft Coat Systems

*- List not Exhaustive