Low Friction Coatings Market Size, Drag Reduction Technologies, and Efficiency-Driven Applications Outlook

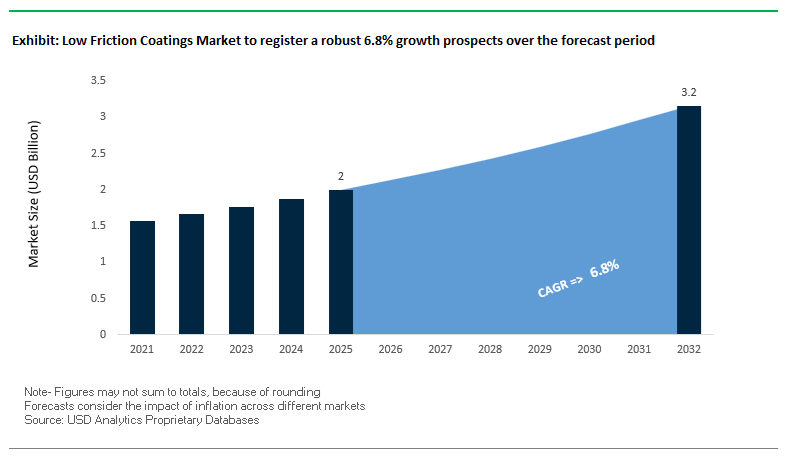

The global low friction coatings market was valued at $2 billion in 2025 and is projected to reach $3.2 billion by 2032, expanding at a CAGR of 6.8%. This growth is being driven by increasing demand for anti-friction coatings, dry film lubricants, PTFE coatings, molybdenum disulfide coatings, and low-drag marine coatings across automotive, aerospace, marine, industrial machinery, and energy sectors. These coatings are engineered to reduce surface friction, wear, and energy loss, making them critical for enhancing operational efficiency, component lifespan, and fuel economy.

A key growth driver is the rising emphasis on energy efficiency and emissions reduction, particularly in industries such as shipping and automotive, where even marginal reductions in friction can lead to substantial fuel savings. In marine applications, low-friction hull coatings significantly reduce hydrodynamic drag, improving vessel speed and lowering fuel consumption. Similarly, in automotive and industrial machinery, these coatings minimize mechanical wear and lubrication dependency, contributing to improved performance and reduced maintenance costs.

Technological advancements in surface engineering, laser cladding, and advanced polymer coatings are expanding the application scope of low friction coatings. The integration of nano-coatings, self-lubricating materials, and biocide-free formulations is enhancing durability while meeting environmental compliance standards. Additionally, the growing adoption of electric vehicles (EVs), renewable energy systems, and high-precision manufacturing is driving demand for coatings that can operate efficiently under high thermal and mechanical stress conditions. Regionally, Asia-Pacific dominates due to strong manufacturing activity, while Europe leads in sustainability-driven innovations and marine coating technologies.

The low friction coatings industry is rapidly evolving, driven by sustainability mandates, advanced application technologies, and strategic capacity expansions. In February 2026, Jotun reported a significant milestone, with its low-friction marine coatings contributing to 11.8 million tonnes of avoided CO₂ emissions in 2025, validated by DNV. This underscores the growing role of low-drag coating systems as carbon reduction tools in the maritime industry, where minimizing hull resistance directly translates into lower fuel consumption and emissions.

Capacity expansion and strategic investments are strengthening supply capabilities. In February 2026, AkzoNobel announced a €21 million expansion at its Como, Italy facility, adding new production lines focused on low-friction nylon powder coatings and advanced automotive primers. This expansion targets high-growth segments such as automotive lightweighting and industrial surface protection, where friction reduction is critical for efficiency and durability.

Technological innovation is further enhancing coating performance and application precision. In January 2026, IPG Photonics introduced an 8kW single-mode laser source optimized for high-speed laser cladding, enabling the creation of ultra-smooth, low-friction surfaces on aerospace-grade materials. Similarly, Meltio’s June 2025 launch of the Engine Blue system utilizes blue laser technology to apply low-friction coatings on highly reflective metals such as copper and aluminum, which are essential in EV battery systems and thermal management applications.

Strategic partnerships and large-scale deployments are reinforcing market adoption. AkzoNobel’s December 2025 agreement with Winning Shipping to supply Intersleek® 1100SR coatings for multiple vessels highlights the increasing adoption of slime-release, low-friction marine coatings aligned with China’s “Dual Carbon” strategy. Additionally, AkzoNobel’s involvement in the world’s first sail-assisted Aframax tanker project in July 2025 demonstrates how low-friction coatings are enabling next-generation propulsion systems by minimizing underwater drag and maximizing efficiency.

Application technology advancements are also improving coating performance and sustainability. PPG Industries has been at the forefront with its electrostatic coating application method, achieving smoother and more uniform coating layers while reducing overspray and emissions by up to 35%. Its SIGMAGLIDE® 2390 and NEXEON™ 810 coatings, highlighted in April 2025, exemplify the shift toward biocide-free, ultra-low friction coatings that meet stringent environmental standards while maintaining high performance in cruise and cargo vessels.

Market Trend: Diamond-Like Carbon (DLC) Coatings Enhancing EV Drivetrain Efficiency and Durability

The rapid expansion of electric vehicles is fundamentally reshaping demand dynamics in the low friction coatings market, particularly in drivetrain applications such as constant-velocity joints and transmission systems. Diamond-Like Carbon (DLC) coatings are emerging as a critical enabling technology for improving efficiency, durability, and thermal resilience in high-performance electric drivetrains. As electric motors generate instant torque and operate under high-frequency load cycles, traditional surface treatments are increasingly insufficient to prevent wear mechanisms such as scuffing and pitting.

DLC coatings significantly enhance scuffing resistance, with hydrogen-free variants increasing the critical scuffing temperature from 224.6°C to 348.6°C, representing a 55% improvement. This performance gain is essential for managing the thermal spikes associated with aggressive acceleration in electric vehicles. In addition, DLC coatings deliver substantial improvements in surface hardness, typically reaching approximately 2,000 HV, which provides a robust protective barrier against micro-wear and seizure under continuous operation.

Friction reduction is another key performance parameter driving adoption. DLC-coated interfaces achieve extremely low coefficients of friction, ranging from 0.007 to 0.013 in vacuum conditions and around 0.1 under lubricated boundary conditions. This reduction in friction directly lowers parasitic energy losses within the drivetrain, contributing to improved vehicle range and energy efficiency. Furthermore, the ultra-thin deposition thickness of 1 to 5 microns ensures that dimensional tolerances are preserved, eliminating the need for component redesign in precision-engineered e-motor assemblies. These attributes position DLC coatings as a core material innovation in next-generation EV drivetrain optimization strategies.

Market Trend: Tungsten Disulfide (WS₂) Dry Film Lubrication Transforming Aerospace and Space Systems

The aerospace and space sectors are increasingly adopting Tungsten Disulfide (WS₂) as a high-performance dry film lubricant for critical components operating under extreme environmental conditions. Unlike conventional lubricants that degrade, outgas, or freeze in vacuum or temperature extremes, WS₂ coatings provide stable, reliable lubrication across a wide range of operating environments, making them highly suitable for aerospace hydraulics, actuators, and satellite deployment systems.

WS₂ coatings offer exceptional load-bearing capacity, with the ability to withstand pressures up to 350,000 psi. This makes them ideal for high-stress components such as actuator pins, bearings, and landing gear assemblies subjected to intense mechanical forces during takeoff and landing cycles. Their thermal stability further enhances their applicability, maintaining lubricity from cryogenic temperatures as low as −188°C to elevated temperatures of 538°C in atmospheric conditions and up to 1,316°C in vacuum environments.

Another critical advantage of WS₂ coatings is their molecular-scale thickness, typically around 0.5 microns, which ensures no dimensional build-up on precision components. This is essential in aerospace systems where tight tolerances are non-negotiable. Additionally, WS₂ coatings exhibit a dynamic coefficient of friction of approximately 0.030, significantly lower than untreated metal interfaces. This reduction in friction decreases the actuation force required in hydraulic systems, contributing to improved energy efficiency and reduced wear over extended operational cycles. These performance characteristics are driving widespread adoption of WS₂ coatings in both commercial aviation and space exploration applications.

Market Opportunity: Regulatory Pressure on PFAS Accelerating Shift Toward Biocompatible Low-Friction Coatings in Medical Devices

The global reassessment of per- and polyfluoroalkyl substances (PFAS), including PTFE-based coatings, is creating a significant opportunity landscape for alternative low-friction coating technologies in the medical device sector. Regulatory scrutiny, particularly following the U.S. FDA’s safety review in 2025, is intensifying the industry’s focus on developing PFAS-free solutions that align with evolving environmental and health standards while maintaining high-performance characteristics.

Although current medical-grade fluoropolymers remain approved for use, the growing regulatory momentum in both North America and Europe is prompting manufacturers to proactively transition toward safer, future-proof materials. Advanced coatings such as WS₂ and specialized DLC variants are gaining traction due to their demonstrated biocompatibility under ISO 10993 standards. These coatings are increasingly being specified for surgical instruments, guide wires, and implantable devices, where material safety and performance reliability are critical.

The demand for minimally invasive surgical technologies is further amplifying this opportunity. Medical devices used in micro-vascular procedures require ultra-low friction coefficients below 0.05 to ensure smooth navigation through complex anatomical pathways. This is driving innovation in coating formulations that deliver consistent lubricity without the risk of flaking, delamination, or toxic residue. As regulatory frameworks continue to tighten around PFAS usage, manufacturers capable of offering validated, non-toxic low-friction coatings are expected to gain a competitive advantage, positioning this segment as a high-growth area within the broader coatings industry.

Low Friction Coatings Market Share and Segmentation Insights

Automotive Components Account for 32% Share Fueled by Emission Regulations and EV Drivetrain Needs

The low friction coatings market by component is led by automotive parts, capturing 32% of the global market share in 2025, driven by stringent fuel efficiency regulations and CO₂ emission reduction targets. Advanced coatings such as diamond-like carbon (DLC), molybdenum disulfide (MoS₂), PTFE, and graphite-based lubricious coatings are widely applied to piston rings, tappets, pins, and transmission components to reduce parasitic losses and improve engine efficiency. This is critical for compliance with global standards like CAFE regulations and fleet emission norms. Additionally, the rapid expansion of electric vehicles (EVs) is further accelerating demand, as high-speed EV gearboxes and bearings (15,000–20,000+ RPM) require low friction coatings to minimize heat generation and acoustic noise. This dual relevance across internal combustion engines and next-generation EV drivetrains reinforces automotive components as the dominant segment.

Contract Coating Service Providers Hold 48% Share Due to Vacuum Technology Expertise and Cost Efficiency

In the low friction coatings market by sales channel, contract coating service providers dominate with a 48% market share in 2025, reflecting the high technical barriers associated with coating processes. Technologies such as PVD (Physical Vapor Deposition), CVD (Chemical Vapor Deposition), and plasma coating systems require capital-intensive vacuum chambers and precision-controlled environments, making outsourcing more viable for most manufacturers. Contract coaters serve multiple industries—including automotive, aerospace, and medical devices—allowing them to maximize equipment utilization and deliver cost efficiencies. Their ability to perform batch processing, consolidating components from multiple clients into single coating runs (e.g., DLC or CrN coatings), significantly reduces per-part costs while maintaining strict quality standards. This operational efficiency, combined with advanced process expertise, positions contract coating providers as the preferred channel for high-performance low friction surface treatments.

Competitive Landscape in the Low Friction Coatings Market

AkzoNobel accelerates consolidation and digital coating innovation in low friction coatings

AkzoNobel is emerging as a pivotal force in the low friction coatings market, driven by its strategic move toward consolidation through a planned merger with Axalta, expected to finalize in late 2026. This initiative aims to establish a dominant entity in industrial and vehicle refinish coatings, targeting an adjusted EBITDA margin exceeding 16%. The company reported a projected €1.47 billion adjusted EBITDA for 2026, supported by consistent margin expansion despite supply chain volatility. Its collaboration with IPG Photonics to develop laser-curing technology significantly reduces energy consumption in coating applications. Additionally, AkzoNobel’s focus on bio-attributed resins, developed in partnership with BASF, positions it at the forefront of sustainable, petroleum-free low friction coating solutions.

The Chemours Company maintains a dominant position in fluoropolymer-based low friction coatings through its Teflon™ and Opteon™ product lines. Reporting $5.8 billion in net sales in 2025, the company achieved strong growth in its Thermal & Specialized Solutions segment, particularly with increased adoption of Opteon™ refrigerants. However, its 2026 strategy is focused on stabilizing margins and addressing litigation-related financial impacts, targeting 3–5% sales growth. Chemours has implemented global price increases for TiO2 and specialty coatings to offset rising input costs. Importantly, the company is aggressively advancing PFAS-alternative additives to comply with evolving environmental regulations in Europe and North America, reinforcing its long-term market sustainability.

DuPont MOLYKOTE expands advanced lubrication solutions for hydrogen and EV systems

DuPont, through its MOLYKOTE® brand, is a critical innovator in anti-friction coatings designed for extreme environments and next-generation energy systems. Its MOLYKOTE® HP-300 Grease has been validated against ISO 14687:2019 hydrogen purity standards, positioning it as a key solution for hydrogen refueling infrastructure and fuel cell technologies. The company has developed advanced testing protocols in collaboration with HyCentA Research, enabling performance validation under pressures up to 700 bar. DuPont’s coatings are widely used in automotive propulsion systems, particularly in EVs, where reducing noise, vibration, and harshness (NVH) is essential. Its expertise in solid lubricant dispersions, including MoS2 and PTFE, supports performance across a wide temperature range, from -40°C to extreme heat conditions.

PPG integrates AI and automation for scalable low friction coating applications

PPG Industries is leveraging its extensive R&D capabilities to integrate artificial intelligence and automation into low friction coating processes. The company has introduced end-to-end protective coating solutions tailored for next-generation data centers, focusing on liquid-applied coatings for cooling system components. Its expansion strategy includes significant investments in the Asia-Pacific region, projected to account for 37% of the market by 2035, driven by automotive manufacturing hubs in China and India. PPG’s MoonWalk® automated mixing system enhances coating consistency while reducing material waste by approximately 15–20%. Additionally, the company is transitioning toward circular manufacturing models, emphasizing coatings that extend the operational lifespan of components in renewable energy applications such as wind turbines.

Poeton delivers precision-engineered low friction coatings for aerospace and medical sectors

Poeton Industries Ltd is a specialized provider of high-performance surface treatments, particularly for aerospace and medical applications requiring precision and reliability. Its Apticote 100 and 800 series coatings are recognized for superior anti-galling and low-friction performance on challenging substrates such as titanium and magnesium alloys. The company has expanded its portfolio to include FDA-approved low friction coatings for high-speed packaging machinery, addressing growing demand in food processing industries. Poeton’s expertise in electroless nickel plating combined with PTFE enables coatings with hardness exceeding 500 HV and friction coefficients below 0.1. These capabilities make it a critical supplier for surgical instruments and medical probes, where smooth operation and patient safety are paramount.

Endura Coatings advances multifunctional and zero-friction coating technologies

Endura Coatings is gaining traction through its patented approach to combining multiple surface treatment benefits into single-layer applications. Its Endura® 300 series incorporates lubricants directly into the crystal structure of the coating, preventing delamination under high-stress conditions and enhancing durability. The company’s “Zero-Friction” initiative targets packaging and plastic processing industries, reducing downtime caused by stick-slip effects in high-speed operations. Endura is also expanding into ISO-certified healthcare coatings, offering dual-function solutions that combine antimicrobial properties with low friction performance. Its digital surface modeling capabilities allow precise matching of coatings to substrates, enabling predictive wear analysis and optimized coating performance before physical deployment.

India’s Railway Modernization Driving Adoption of MoS₂ Coatings for Energy Efficiency and Asset Longevity

India’s large-scale railway modernization initiatives are creating substantial opportunities for low friction coating technologies, particularly Molybdenum Disulfide (MoS₂)-based solutions. The Ministry of Railways is actively promoting the adoption of advanced coating systems for wagon axle bearings, couplers, and other critical components to improve operational efficiency, reduce maintenance frequency, and support national sustainability targets.

MoS₂ coatings are being deployed to extend maintenance intervals by up to 30%, significantly reducing the frequency of maintenance interventions and improving rolling stock availability. This is particularly important in a network exceeding 68,000 kilometers, where operational efficiency is directly linked to freight and passenger throughput. Field-level audits have demonstrated that MoS₂-coated axle bearings reduce rolling resistance, leading to measurable energy savings in both diesel and electric locomotives.

The durability of MoS₂ coatings under diverse and extreme environmental conditions further enhances their suitability for India’s railway network. These coatings are engineered to withstand high vibration levels, dust exposure, and temperature variations ranging from sub-zero conditions in northern regions to extreme heat in central and western zones. Additionally, the adoption of low-friction coatings aligns with national initiatives such as 100% railway electrification and net-zero carbon emission targets by 2030. By reducing mechanical energy losses across the network, MoS₂ coatings represent a cost-effective and scalable solution for improving infrastructure sustainability and long-term asset performance.

China Low Friction Coatings Market: EV Battery Manufacturing and Semiconductor Expansion Driving Volume Leadership

China dominates the global low friction coatings market, supported by its expansive manufacturing ecosystem, particularly in electric vehicle (EV) battery production and semiconductor fabrication. The country is aggressively localizing the supply chain for advanced fluoropolymer coatings, PTFE (polytetrafluoroethylene), PFA, and MoS₂-based coatings, strengthening its global competitiveness. Government mandates under the “14th Five-Year Plan” for green manufacturing, including VOC emission reduction targets, are accelerating the transition toward environmentally compliant coating technologies.

Significant infrastructure investments, including the development of over 600 EV battery gigafactories, are fueling demand for friction-reducing coatings used in electrode rollers and lithium-ion battery manufacturing equipment. These coatings enhance throughput, reduce material adhesion, and improve precision in production processes. Domestic companies such as Nanjing Tianshi are expanding capacity to address high-end industrial applications. Additionally, stricter GB standards regulating PFOA phase-out are pushing innovation toward sustainable, high-performance coatings, reinforcing China’s leadership in high-volume industrial applications.

United States Low Friction Coatings Market: Aerospace Innovation and Advanced Surface Engineering Leadership

The United States represents a high-value low friction coatings market, driven by its strong aerospace, defense, and semiconductor sectors. Advanced coating technologies such as Diamond-Like Carbon (DLC) and Tungsten Disulfide (WS₂) are being commercialized for use in extreme environments, including space applications where traditional lubricants fail. These innovations are essential for vacuum-based operations and high-performance aerospace components, positioning the U.S. as a leader in cutting-edge coating technologies.

Government-backed initiatives like the CHIPS and Science Act are boosting research into coatings for cleanroom robotics and wafer handling systems, critical for semiconductor manufacturing. The market is also witnessing a shift toward PFAS-free and environmentally compliant formulations, driven by tightening EPA regulations under the Toxic Substances Control Act (TSCA). Low friction coatings are widely used in aerospace MRO applications, including turbine blade roots and actuator assemblies, where they reduce wear and extend component life. Strong investment from the aerospace sector continues to drive demand for precision-engineered, high-performance surface coatings.

Germany Low Friction Coatings Market: Smart Coatings and Automotive Efficiency under Industrie 4.0

Germany anchors the European low friction coatings market through its focus on precision engineering, automotive innovation, and Industrie 4.0 integration. The country is pioneering the development of smart coatings embedded with sensors, enabling real-time monitoring of friction, wear, and component performance in automated production environments.

The transition toward electric vehicles (EVs) and hydrogen-based energy systems is creating new demand for specialized coatings used in high-pressure hydrogen compressors, valves, and drivetrain components. Coatings such as MoS₂ are widely applied in automotive systems to reduce mechanical losses and enhance energy efficiency, supporting sustainability goals. Major players like Klüber Lubrication are expanding their specialized coating centers to support this transition. Additionally, strong R&D investment in bio-based and circular economy-friendly coating materials, combined with strict adherence to EU REACH regulations, is driving the shift away from legacy fluoropolymers and reinforcing Germany’s leadership in sustainable coating technologies.

India Low Friction Coatings Market: Infrastructure Boom and Defense Manufacturing Fueling Growth

India is emerging as a high-growth market for low friction and anti-friction coatings, supported by large-scale infrastructure development and expanding domestic manufacturing capabilities. Under the Gati Shakti initiative, over $1.3 trillion worth of infrastructure projects are driving demand for coatings in bridge bearings, heavy construction equipment, and industrial machinery.

The “Make in India” initiative is further boosting demand through the development of indigenous defense platforms, including guided missile frigates and advanced marine systems, where specialized low friction coatings are critical for performance and durability. In addition, the increasing use of water-based anti-friction coatings in hydraulic and pneumatic systems reflects the shift toward environmentally sustainable solutions. The domestic railway and locomotive manufacturing sector is also adopting solid lubricant thin films to improve efficiency and reduce maintenance. Rising foreign direct investment from global leaders like Daikin and AGC is strengthening local production capabilities and accelerating market expansion.

Japan Low Friction Coatings Market: Robotics, Nano-Coatings, and Ultra-Precision Engineering

Japan’s low friction coatings market is defined by its focus on ultra-precision manufacturing, robotics, and advanced material science innovations. The country is at the forefront of developing nano-composite coatings, combining PTFE with ceramic particles to achieve extremely low coefficients of friction, enabling high-performance applications in sensitive environments.

These coatings are extensively used in industrial robotics, where reduced friction ensures high-speed motion with minimal heat generation, improving operational efficiency and equipment lifespan. Japan is also investing heavily in solid-state battery technologies, where low friction coatings play a critical role in maintaining stable interfaces between components. Leading companies such as AGC Inc. and Nitto Denko are expanding their portfolios of advanced coatings for electronics and 5G applications. Regulatory compliance under the Chemical Substances Control Law (CSCL) ensures the adoption of safe and sustainable coating materials. Innovations in micro-textured surface engineering are further enabling “super-lubricity” effects, particularly in medical devices and high-tech applications.

South Korea Low Friction Coatings Market: Electronics Innovation and Shipbuilding Demand Driving Growth

South Korea is emerging as a key market for low friction coatings in electronics, semiconductor manufacturing, and shipbuilding industries. The adoption of UV-cured low friction coatings in mobile electronics is enhancing product durability, offering scratch resistance and improved tactile performance in next-generation devices such as foldable smartphones.

The country’s strong shipbuilding sector is driving demand for coatings applied to engine components to reduce friction and improve fuel efficiency, particularly in the Yeongnam industrial region. In semiconductor cleanroom environments, low friction coatings are essential for robotic wafer handling systems, preventing wear debris and ensuring production precision. Government support for R&D in chemical engineering and advanced materials is sustaining innovation in coating technologies. Additionally, product developments such as hybrid polyurethane-PTFE coatings are improving adhesion across diverse substrates, while companies like KCC Corporation are expanding their presence in automotive and industrial coating segments.

Low Friction Coatings Market Report Scope

Low Friction Coatings Market

Parameter

Details

Market Size (2025)

$2 Billion

Market Size (2032)

$3.2 Billion

Market Growth Rate

6.8%

Segments

By Product Type (Polytetrafluoroethylene, Molybdenum Disulfide, Tungsten Disulfide, Fluorinated Ethylene Propylene, Perfluoroalkoxy Alkanes, Graphite-based Coatings, Polyaspartic and Silicone-modified, Others), By Technology (Solvent-borne Coatings, Water-borne Coatings, Powder Coatings, Solvent-Free), By Substrate (Metals and Alloys, Plastics and Polymers, Composites, Glass and Ceramics), By Component (Bearings and Bushings, Automotive Parts, Power Transmission Items, Valve Components and Actuators, Fasteners, Surgical and Medical Tools, Molds and Tooling), By End-Use Industry (Automotive and Transportation, Aerospace and Defense, Healthcare and Medical, General Engineering and Industrial Machinery, Food and Beverage Processing, Energy, Consumer Electronics and Appliances), By Functional Performance (Wear and Abrasion Resistance, Corrosion Resistance, High Load-Carrying Capacity, Chemical and Heat Resistance, Noise Reduction), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Contract Coating Service Providers)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

The Chemours Company, DuPont de Nemours, Inc., PPG Industries, Inc., Klüber Lubrication, Daikin Industries, Ltd., The Sherwin-Williams Company, Akzo Nobel N.V., The FUCHS Group, Carl Bechem GmbH, Oerlikon Balzers, Endura Coatings, Whitford Corporation, Poeton Industries Ltd., Everlube Products, Hempel A/S

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Low Friction Coatings Market Segmentation

By Product Type

Polytetrafluoroethylene

Molybdenum Disulfide

Tungsten Disulfide

Fluorinated Ethylene Propylene

Perfluoroalkoxy Alkanes

Graphite-based Coatings

Polyaspartic and Silicone-modified

Others

By Technology

Solvent-borne Coatings

Water-borne Coatings

Powder Coatings

Solvent-Free

By Substrate

Metals and Alloys

Plastics and Polymers

Composites

Glass and Ceramics

By Component

Bearings and Bushings

Automotive Parts

Power Transmission Items

Valve Components and Actuators

Fasteners

Surgical and Medical Tools

Molds and Tooling

By End-Use Industry

Automotive and Transportation

Aerospace and Defense

Healthcare and Medical

General Engineering and Industrial Machinery

Food and Beverage Processing

Energy

Consumer Electronics and Appliances

By Functional Performance

Wear and Abrasion Resistance

Corrosion Resistance

High Load-Carrying Capacity

Chemical and Heat Resistance

Noise Reduction

By Sales Channel

Direct Sales

Specialty Industrial Distributors

Contract Coating Service Providers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

2. Low Friction Coatings Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Low Friction Coatings Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the Low Friction Coatings Market

3.1. Trend: Diamond-Like Carbon (DLC) Coatings Enhancing EV Drivetrain Efficiency

3.2. Trend: Tungsten Disulfide (WS₂) Dry Film Lubrication Transforming Aerospace and Space Systems

3.3. Opportunity: PFAS Regulations Accelerating Biocompatible Coatings in Medical Devices

3.4. Opportunity: India’s Railway Modernization Driving Adoption of MoS₂ Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Low Friction Coatings Market

5.1. By Product Type

5.1.1. Polytetrafluoroethylene (PTFE)

5.1.2. Molybdenum Disulfide (MoS₂)

5.1.3. Tungsten Disulfide (WS₂)

5.1.4. Fluorinated Ethylene Propylene (FEP)

5.1.5. Perfluoroalkoxy Alkanes (PFA)

5.1.6. Graphite-based Coatings

5.1.7. Polyaspartic and Silicone-modified

5.1.8. Others

5.2. By Technology

5.2.1. Solvent-borne Coatings

5.2.2. Water-borne Coatings

5.2.3. Powder Coatings

5.2.4. Solvent-Free

5.3. By Substrate

5.3.1. Metals and Alloys

5.3.2. Plastics and Polymers

5.3.3. Composites

5.3.4. Glass and Ceramics

5.4. By Component

5.4.1. Bearings and Bushings

5.4.2. Automotive Parts

5.4.3. Power Transmission Items

5.4.4. Valve Components and Actuators

5.4.5. Fasteners

5.4.6. Surgical and Medical Tools

5.4.7. Molds and Tooling

5.5. By End-Use Industry

5.5.1. Automotive and Transportation

5.5.2. Aerospace and Defense

5.5.3. Healthcare and Medical

5.5.4. General Engineering and Industrial Machinery

5.5.5. Food and Beverage Processing

5.5.6. Energy

5.5.7. Consumer Electronics and Appliances

5.6. By Functional Performance

5.6.1. Wear and Abrasion Resistance

5.6.2. Corrosion Resistance

5.6.3. High Load-Carrying Capacity

5.6.4. Chemical and Heat Resistance

5.6.5. Noise Reduction

5.7. By Sales Channel

5.7.1. Direct Sales

5.7.2. Specialty Industrial Distributors

5.7.3. Contract Coating Service Providers

6. Country Analysis and Outlook of Low Friction Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Low Friction Coatings Market Size Outlook by Region (2025–2034)

7.1. North America Low Friction Coatings Market Size Outlook to 2034

7.1.1. By Product Type

7.1.2. By Technology

7.1.3. By Substrate

7.1.4. By Component

7.1.5. By End-Use Industry

7.1.6. By Functional Performance

7.1.7. By Sales Channel

7.2. Europe Low Friction Coatings Market Size Outlook to 2034

7.2.1. By Product Type

7.2.2. By Technology

7.2.3. By Substrate

7.2.4. By Component

7.2.5. By End-Use Industry

7.2.6. By Functional Performance

7.2.7. By Sales Channel

7.3. Asia Pacific Low Friction Coatings Market Size Outlook to 2034

7.3.1. By Product Type

7.3.2. By Technology

7.3.3. By Substrate

7.3.4. By Component

7.3.5. By End-Use Industry

7.3.6. By Functional Performance

7.3.7. By Sales Channel

7.4. South America Low Friction Coatings Market Size Outlook to 2034

7.4.1. By Product Type

7.4.2. By Technology

7.4.3. By Substrate

7.4.4. By Component

7.4.5. By End-Use Industry

7.4.6. By Functional Performance

7.4.7. By Sales Channel

7.5. Middle East and Africa Low Friction Coatings Market Size Outlook to 2034

7.5.1. By Product Type

7.5.2. By Technology

7.5.3. By Substrate

7.5.4. By Component

7.5.5. By End-Use Industry

7.5.6. By Functional Performance

7.5.7. By Sales Channel

8. Company Profiles: Leading Players in the Low Friction Coatings Market

8.1. The Chemours Company

8.2. DuPont de Nemours, Inc.

8.3. PPG Industries, Inc.

8.4. Klüber Lubrication

8.5. Daikin Industries, Ltd.

8.6. The Sherwin-Williams Company

8.7. Akzo Nobel N.V.

8.8. The FUCHS Group

8.9. Carl Bechem GmbH

8.10. Oerlikon Balzers

8.11. Endura Coatings

8.12. Whitford Corporation

8.13. Poeton Industries Ltd.

8.14. Everlube Products

8.15. Hempel A/S

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Low Friction Coatings Market Segmentation

By Product Type

Polytetrafluoroethylene

Molybdenum Disulfide

Tungsten Disulfide

Fluorinated Ethylene Propylene

Perfluoroalkoxy Alkanes

Graphite-based Coatings

Polyaspartic and Silicone-modified

Others

By Technology

Solvent-borne Coatings

Water-borne Coatings

Powder Coatings

Solvent-Free

By Substrate

Metals and Alloys

Plastics and Polymers

Composites

Glass and Ceramics

By Component

Bearings and Bushings

Automotive Parts

Power Transmission Items

Valve Components and Actuators

Fasteners

Surgical and Medical Tools

Molds and Tooling

By End-Use Industry

Automotive and Transportation

Aerospace and Defense

Healthcare and Medical

General Engineering and Industrial Machinery

Food and Beverage Processing

Energy

Consumer Electronics and Appliances

By Functional Performance

Wear and Abrasion Resistance

Corrosion Resistance

High Load-Carrying Capacity

Chemical and Heat Resistance

Noise Reduction

By Sales Channel

Direct Sales

Specialty Industrial Distributors

Contract Coating Service Providers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global low friction coatings market was valued at $2 billion in 2025 and is projected to reach $3.2 billion by 2032, expanding at a CAGR of 6.8%. The market is growing due to increasing demand for anti-friction coatings, PTFE coatings, dry film lubricants, DLC coatings, and low-drag marine coatings across automotive, aerospace, industrial machinery, and energy sectors focused on efficiency improvement and emissions reduction.

Diamond-Like Carbon (DLC) coatings are increasingly used in EV drivetrains because they significantly reduce friction, improve thermal resistance, and enhance wear protection under high-speed operating conditions. Tungsten Disulfide (WS₂) coatings are also gaining traction in aerospace and space systems due to their ability to maintain lubrication in vacuum, cryogenic, and high-temperature environments where conventional lubricants fail. These technologies improve operational efficiency, durability, and component lifespan in mission-critical applications.

Environmental regulations targeting PFAS, VOC emissions, and marine pollution are accelerating the shift toward sustainable and biocide-free low friction coating technologies. Manufacturers are increasingly developing PFAS-free alternatives, water-based coatings, self-lubricating materials, and low-drag marine coatings that reduce fuel consumption and carbon emissions. Regulatory pressure in Europe, North America, and Asia is driving innovation in environmentally compliant surface engineering solutions.

Automotive and transportation remain the largest application sectors due to fuel efficiency regulations and rapid EV adoption. Aerospace, marine, semiconductor manufacturing, renewable energy, and medical devices are also creating substantial opportunities for advanced low friction coatings. Regionally, Asia-Pacific dominates through strong manufacturing activity in China, Japan, South Korea, and India, while Europe leads in sustainable marine coating technologies and advanced industrial surface engineering innovations.

Major companies operating in the low friction coatings industry include The Chemours Company, DuPont de Nemours, Inc., PPG Industries, Inc., Klüber Lubrication, Daikin Industries, Ltd., The Sherwin-Williams Company, Akzo Nobel N.V., Oerlikon Balzers, and Hempel A/S. These companies are investing in advanced fluoropolymer technologies, laser-applied coatings, AI-driven coating systems, and sustainable low-drag surface engineering solutions to strengthen their global market positions.