Low Temperature Coatings Market Size, Energy-Efficient Curing Technologies, and Cold-Environment Applications Outlook

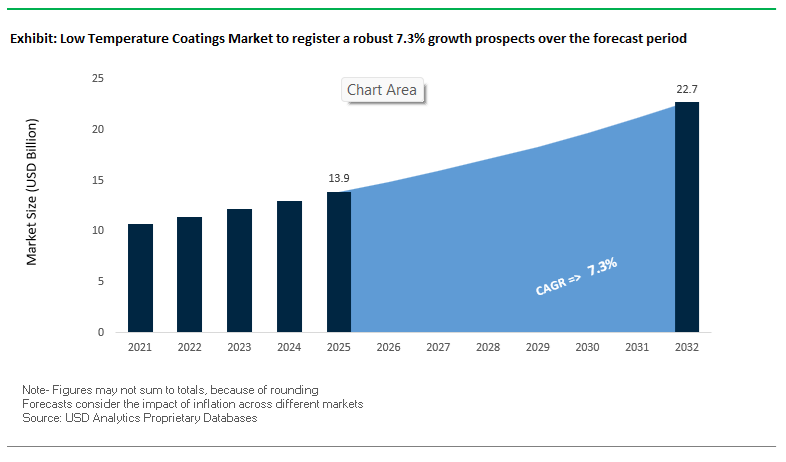

The global low temperature coatings market was valued at $13.9 billion in 2025 and is projected to reach $22.8 billion by 2032, expanding at a strong CAGR of 7.3%. This growth is being driven by increasing demand for low-cure powder coatings, ambient-cure coatings, low-temperature electrocoats (e-coats), and energy-efficient industrial coatings across automotive, construction, infrastructure, furniture, and industrial manufacturing sectors. These coatings are specifically engineered to cure at reduced temperatures or ambient conditions, enabling significant reductions in energy consumption, carbon emissions, and production costs.

A primary growth driver is the rising focus on sustainable manufacturing and decarbonization, particularly in energy-intensive industries such as automotive OEMs, metal fabrication, and industrial coating lines. Low temperature coatings allow manufacturers to operate curing ovens at significantly lower temperatures or eliminate baking altogether, leading to energy savings of up to 20–50%. Additionally, these coatings enable the treatment of heat-sensitive substrates such as plastics, composites, and medium-density fiberboard (MDF), expanding their application scope in furniture, electronics, and lightweight automotive components.

The market is also benefiting from increased demand in cold climate and remote industrial environments, where traditional coatings fail to cure effectively. Technologies such as cold-cure epoxies, fast-cure maintenance coatings, and low-temperature catalysts are enabling coating application in sub-zero conditions, particularly in oil & gas, infrastructure maintenance, and offshore projects. Regionally, Europe and North America lead in sustainability-driven adoption, while Asia-Pacific is witnessing rapid growth due to expanding automotive manufacturing and industrial production capacity.

Market Analysis: Low-Cure Coating Innovations, Automotive Energy Reduction, and Cold-Climate Technologies Driving Market Evolution

The low temperature coatings industry is undergoing rapid transformation driven by energy efficiency requirements, advanced curing technologies, and strategic consolidation. In March 2026, PPG Industries introduced a new generation of low-temperature cure electrocoats (e-coats), capable of delivering high-performance corrosion protection at bake temperatures as low as 150°C. This innovation directly addresses the automotive industry’s need to reduce energy consumption and CO₂ emissions in paint shops, which are among the most energy-intensive operations in vehicle manufacturing.

Market consolidation is further accelerating technological integration. The February 2026 merger between AkzoNobel and Axalta combines Interpon Low-E powder coating technology with Axalta’s low-cure automotive refinish systems, creating a strong portfolio of low-energy coating solutions across both industrial and automotive applications. This consolidation is expected to drive broader adoption of energy-efficient coatings globally.

Product innovation is also expanding into extreme environmental applications. In January 2026, Jotun launched upgraded Jotatemp and Jotapipe coatings featuring cold-cure catalysts, enabling application and curing at temperatures as low as -10°C, which is critical for Arctic, offshore, and high-altitude energy projects. Similarly, Tnemec’s July 2025 launch of ProBond epoxy sealers targets marginal surfaces and low-temperature conditions, ensuring reliable adhesion where traditional coatings fail.

Sustainability and operational efficiency remain central to innovation strategies. AkzoNobel’s June 2025 launch of Interpon 610 Low-E powder coatings enables curing at 150°C, delivering up to 20% energy savings for industrial fabricators. Sherwin-Williams reinforced this trend through its November 2025 expansion of low-cure Powdura® Eco coatings, incorporating recycled plastic content and reducing curing temperature requirements. Additionally, Axalta’s September 2025 sustainability report highlighted the widespread adoption of its Cromax Gen and Standox Xtreme systems, which allow ambient curing or up to 50% energy reduction in automotive refinish operations.

Emerging applications in advanced manufacturing are further expanding market scope. PPG’s ENVIROCRON® HeatSense coatings, introduced in July 2024, enable low-temperature curing for heat-sensitive substrates such as wood and MDF, preventing material deformation. Tiger Drylac’s May 2024 expansion into low-temperature coatings for 3D-printed metal parts highlights the growing intersection of additive manufacturing and coating technologies, where delicate components require low-heat finishing processes.

Strategic R&D investments are also supporting long-term growth. Hempel A/S, following strong financial performance in March 2025, announced a focus on fast-cure coatings designed for winter application in European infrastructure projects, addressing seasonal constraints in construction and maintenance.

The low temperature coatings market is witnessing strong momentum driven by increased pipeline construction and maintenance activities in Arctic and sub-Arctic regions. Operators are transitioning toward low-temperature-cure (LTC) epoxy coatings to overcome the limitations of conventional epoxy systems, which typically fail to cure effectively below 10°C. Advanced LTC epoxy formulations are now engineered to cure reliably at temperatures ranging from −10°C to −20°C, enabling uninterrupted coating operations during harsh winter conditions.

This capability is significantly extending construction windows in northern geographies, with field deployments indicating up to a 25% increase in workable installation periods. This extension eliminates the need for expensive heated enclosures and logistical complexities associated with winter construction, directly improving project economics. In terms of performance, LTC epoxies achieve a handle-ready state within 8 to 12 hours at 0°C, a substantial improvement over traditional coating that require multiple days or fail entirely under similar conditions.

Surface tolerance has also advanced considerably, with modern Arctic-grade epoxy coatings demonstrating adhesion strengths exceeding 15 MPa even when applied to substrates with residual surface frost. This ensures reliable bonding in real-world field conditions where perfect surface preparation is often impractical. Additionally, long-term corrosion resistance remains uncompromised, with testing confirming approximately 99% resistance to cathodic disbondment in accordance with ASTM G8 standards. These performance metrics are positioning LTC epoxy coatings as a critical solution for pipeline integrity management, winter construction efficiency, and lifecycle cost optimization in extreme cold environments.

Offshore wind energy projects, particularly in the North Sea and Baltic regions, are increasingly adopting polyurea-based low temperature coatings to enable winter installation campaigns and improve asset durability in aggressive marine environments. Traditional coating systems often fail under high humidity and low temperature conditions, leading to application delays and increased operational costs. Polyurea coatings address these limitations through ultra-fast curing and exceptional environmental tolerance.

One of the most critical advantages of polyurea coatings is their rapid curing capability, achieving a tack-free state in under 60 seconds even in sub-zero temperatures. This allows immediate deployment of coated components such as monopiles and jacket structures, minimizing idle time for installation vessels. Given the high daily costs associated with offshore installation vessels, this rapid return-to-service capability translates into significant economic benefits. Developers report operational cost savings of approximately 15% due to reduced weather-related delays and improved scheduling flexibility.

Polyurea systems also exhibit strong resistance to high humidity environments, maintaining coating integrity even at relative humidity levels up to 98%. This eliminates issues such as blooming, which commonly affect moisture-sensitive coatings in offshore conditions. In terms of mechanical durability, these coatings provide impact resistance exceeding 15 Joules, ensuring resilience against ice impacts and mechanical abrasion from service vessels. As offshore wind capacity expands into colder regions, polyurea low temperature coatings are becoming a critical enabler of year-round project execution and long-term structural protection.

Market Opportunity: Canadian Arctic Infrastructure Fund Driving Demand for Cold-Applied High-Durability Coatings

Government-led infrastructure investments in high-latitude regions are creating significant opportunities for low temperature coatings, particularly in Canada’s Arctic territories. The Canadian Arctic Infrastructure Fund, valued at $1 billion and active through 2026, is prioritizing the development of resilient transportation infrastructure such as bridges and ports. These projects require advanced coating solutions capable of withstanding extreme environmental conditions while supporting efficient application in remote locations.

The fund emphasizes lifecycle cost reduction, targeting a 30% decrease in maintenance expenditures through the use of durable, cold-applied coating systems. This is driving demand for liquid-applied thermal barriers and low-temperature curing coatings that can be deployed without specialized heating equipment. Port infrastructure development along the Northwest Passage further reinforces this trend, with specifications requiring coatings that deliver a certified service life of up to 50 years in CX-class extreme maritime environments.

A notable component of the funding strategy is the allocation of approximately $400 million toward Indigenous-led infrastructure projects. These initiatives prioritize coatings that are easy to apply, fast-curing, and adaptable to local workforce capabilities, reducing reliance on complex installation technologies. This creates a strong market opportunity for manufacturers offering user-friendly, high-performance coating systems tailored to remote and resource-constrained environments. As Arctic infrastructure development accelerates, low temperature coatings are positioned as a critical material category supporting long-term durability and operational efficiency.

Low Temperature Coatings Market Share and Segmentation Insights

Standard Low-Cure (80–120°C) Coatings Capture 52% Share Driven by Substrate Versatility

The low temperature coatings market by curing profile is dominated by standard low-cure coatings (80–120°C), accounting for 52% of the global market share in 2025. This segment is gaining strong traction due to its compatibility with heat-sensitive substrates such as plastics (ABS, polycarbonate, nylon), MDF, wood composites, and assembled electronic components that cannot tolerate traditional 150–200°C curing cycles. These coatings are widely used in automotive components, consumer electronics, furniture, and industrial assemblies, where thermal limitations are critical. Additionally, reducing curing temperatures from 180°C to approximately 100°C delivers 40–60% energy savings, significantly lowering operational costs and carbon emissions. This dual advantage of substrate protection and energy efficiency is accelerating adoption across manufacturing sectors, positioning standard low-cure coatings as the preferred solution for sustainable and high-performance industrial finishing.

Contract Coating Service Providers Hold 48% Share by Overcoming Equipment and Process Barriers

In the low temperature coatings market by sales channel, contract coating service providers lead with a 48% market share in 2025, driven by their ability to overcome technical and capital barriers for manufacturers. Transitioning to low-temperature curing systems often requires costly oven retrofits or new curing equipment, which many manufacturers prefer to avoid. Contract coaters absorb these capital investments and provide low-cure coating services as a scalable solution. Moreover, they enable single-pass coating of mixed-material assemblies, including components made from metal, plastic, and rubber, which would otherwise degrade under high-temperature curing. This capability is especially valuable in industries such as automotive assemblies, electronics, and appliance manufacturing. By combining process expertise, equipment access, and cost efficiency, contract service providers play a critical role in expanding adoption of low-temperature coating technologies.

Competitive Landscape in the Low Temperature Coatings Market

AkzoNobel leads low-bake powder coating innovation with energy-efficient curing technologies

AkzoNobel is positioning itself as a leader in low temperature coatings through its Interpon and Resicoat product lines, targeting high-efficiency industrial applications. The company is advancing toward a strategic merger with Axalta, expected to create a global coatings powerhouse with EBITDA margins exceeding 16%. At PaintExpo 2026, AkzoNobel introduced laser-based curing technology, developed in collaboration with IPG Photonics, enabling ultra-fast curing cycles and reducing energy consumption by up to 30%. Its Interpon Low-E series allows curing at temperatures as low as 150°C, increasing production line speeds by approximately 20% while lowering Scope 1 emissions. The company’s focus on bio-attributed resins and partnerships with BASF further reinforces its commitment to circular economy-driven coating solutions.

PPG expands low-temperature coating solutions for aerospace, automotive, and data centers

PPG Industries is focusing on advanced, low-temperature coating technologies tailored for high-tech applications, including aerospace and data center infrastructure. In April 2026, the company launched a new range of low-temperature cure electrocoats designed for automotive OEMs, enabling corrosion protection for mixed-metal vehicle structures without thermal distortion. PPG has also invested in a dedicated testing line for radiation-curable coatings in France, targeting a segment projected to grow at a 7.12% CAGR through 2031. Its end-to-end coating solutions for data centers address the need for low-heat application to protect sensitive electronic systems. Leveraging AI-driven color matching and its MoonWalk automated mixing system, PPG ensures precision and consistency even at reduced curing temperatures.

Sherwin-Williams drives high-build low-cure coatings for energy and industrial infrastructure

The Sherwin-Williams Company continues to dominate the North American low temperature coatings market with a focus on high-build, low-cure protective systems for energy and industrial assets. Its Heat-Flex® 7000 series provides thermal insulation and personnel protection in high-temperature environments up to 177°C, while requiring fewer application layers. The company is adapting its FIRETEX® passive fire protection systems for lower curing temperatures, reducing downtime in offshore and petrochemical installations. Following record net sales of $23.06 billion in 2025, Sherwin-Williams is prioritizing growth in refinish and industrial wood coatings, where low-bake processes prevent substrate damage. Expansion of its global supply chain is enabling faster deployment of next-generation coatings in cold-weather and time-sensitive applications.

Axalta advances low-cure coating technologies for EV battery and mobility applications

Axalta Coating Systems is a key innovator in low temperature coatings, particularly within the electric vehicle ecosystem. The company reported a record adjusted EBITDA of $1.13 billion in 2025, with margins reaching 22%, supporting its strategic alignment with AkzoNobel in a planned merger. Axalta’s Energy & Battery Solutions portfolio includes low-bake powder coatings engineered for EV battery enclosures, offering high dielectric strength while minimizing thermal stress on battery cells. Its Imron™ product line continues to lead in transportation coatings, with “Cool-Cure” variants enabling coating of plastics and composite materials alongside traditional metals. Axalta’s strong presence in the automotive refinish market allows body shops to reduce energy consumption by approximately 15% per coating cycle.

Hempel focuses on low-temperature coatings for marine, wind energy, and extreme environments

Hempel A/S is a specialist in coatings designed for harsh and low-temperature environments, particularly in marine and infrastructure sectors. Its “Accelerate to Win” strategy launched in 2026 emphasizes energy-efficient coatings for wind energy and shipping industries. The company achieved an adjusted EBITDA margin of 18.2% in 2025, driven by strong adoption of its Hempaguard low-emission technologies. Hempel has also achieved a 70% reduction in Scope 1 and 2 emissions, with a target of 90% reduction by late 2026 through low-energy production and curing processes. Its coating solutions are widely used for passive fire protection and corrosion resistance in environments subject to extreme temperature fluctuations, reinforcing its position in global infrastructure projects.

Jotun strengthens low-temperature coating solutions for marine and architectural sectors

Jotun A/S is a key player in protective and decorative coatings, particularly in regions such as the Middle East and Asia-Pacific. Its Jotacote Universal S120 is recognized as a benchmark for low-temperature application, enabling year-round coating operations in cold-weather shipyards. The company is focusing on industrial durability by developing epoxy-based systems that perform effectively in high-humidity and salt-laden environments without requiring high-temperature curing. Jotun’s expansion of its Green Building Solutions portfolio includes low-VOC, low-temperature cure coatings for architectural aluminum applications, aligning with sustainability standards. Its strong regional distribution networks, particularly in hubs like Dubai and Singapore, enable rapid technical support and execution of complex industrial coating projects.

US DoD Arctic Strategy Accelerating Demand for Ultra-Low Temperature Resistant Coating Systems

The implementation of the United States Department of Defense Arctic Strategy is driving substantial demand for advanced low temperature coatings across military infrastructure and equipment. As part of its strategic focus on Arctic readiness, the DoD is mandating the deployment of coating systems capable of maintaining structural integrity and performance at temperatures as low as −50°C. This is creating new opportunities for specialized coating technologies, particularly Chemical Agent Resistant Coating (CARC) systems designed for extreme environments.

For ground vehicles, compliance with military specifications such as MIL-DTL-53072F is now required, ensuring that coatings can withstand low-temperature impact without cracking or delamination. This is critical for maintaining operational readiness of tactical vehicles deployed in Arctic regions. In parallel, advancements in hydrophobic coating technologies are improving aircraft performance by reducing ice adhesion strength by up to 70%. This reduces dependency on chemical de-icing agents, lowering operational costs and environmental impact at Arctic airbases.

The strategy also includes significant investment in infrastructure and surveillance systems, where coatings must provide both corrosion resistance and functional performance under extreme cold conditions. Protective coatings for sensors and communication equipment are required to maintain signal transparency while withstanding prolonged exposure to temperatures below −40°C. This convergence of military requirements, environmental challenges, and technological innovation is positioning low temperature coatings as a strategic enabler of defense infrastructure modernization in Arctic regions.

Germany Low Temperature Coatings Market: Energy-Efficient Curing and Green Manufacturing Leadership

Germany stands at the forefront of the low temperature coatings market, driven by rising industrial energy costs and a strong push toward climate-neutral manufacturing and energy-efficient coating technologies. The country is pioneering the development of hybrid resin powder coatings that cure at significantly lower temperatures (130°C–150°C), enabling the coating of heat-sensitive substrates such as medium-density fibreboard (MDF), engineered plastics, and lightweight automotive components. This advancement is critical in supporting Germany’s transition toward sustainable, low-energy industrial processes.

Government support from the Federal Ministry for Economic Affairs and Climate Action (BMWK) is accelerating adoption through subsidies for SMEs transitioning to UV-LED and Near-Infrared (NIR) curing systems. The market is also witnessing innovation in bio-based low-temperature resins derived from agricultural waste, reducing Scope 3 emissions across automotive supply chains. With significant investment in smart curing paint lines integrated with real-time sensors, Germany is optimizing coating efficiency and performance. Regulatory alignment with the EU Green Deal is further driving the adoption of low-VOC, low-carbon coating solutions, reinforcing the country’s leadership in sustainable industrial coatings.

United States Low Temperature Coatings Market: Aerospace Sustainability and Rapid-Return Coating Technologies

The United States low temperature coatings market is defined by its strong presence in aerospace innovation, defense maintenance, and infrastructure modernization. The demand for low-temperature epoxy coatings for composite airframes is growing rapidly, as these coatings protect sensitive materials without causing thermal degradation. This is particularly important in aircraft manufacturing and maintenance, where substrate integrity is critical.

Technological advancements include the development of PFAS-free low-temperature formulations, aligning with evolving EPA regulations on hazardous chemicals. The market is also benefiting from investments under the Infrastructure Investment and Jobs Act (IIJA), which is driving demand for fast-curing, low-temperature coatings in bridge maintenance and naval infrastructure. Companies such as PPG and AkzoNobel are adopting AI-driven formulation technologies to predict coating durability under varying environmental conditions. Additionally, low-temperature coatings are extensively used in military asset refurbishment, enabling rapid repairs without risking heat-induced damage. Regulatory frameworks like SCAQMD Rule 1113 continue to enforce low-VOC standards across industrial finishing processes.

China Low Temperature Coatings Market: Industrial Modernization and High-Volume Manufacturing Expansion

China is emerging as a high-growth market for low temperature coatings, supported by large-scale industrial modernization and expanding manufacturing sectors such as electronics, electric vehicles (EVs), and consumer appliances. Government policies under the “14th Five-Year Plan” are mandating a shift toward waterborne and low-cure powder coatings to improve air quality and reduce industrial emissions.

The development of specialized industrial coating parks in provinces like Jiangsu is enhancing the country’s capacity for energy-efficient coating technologies. Technological advancements in high-efficiency curing agents are enabling existing powder coating lines to operate at reduced temperatures with minimal infrastructure changes. Low temperature coatings are widely used in electronics and cleanroom equipment manufacturing, where components cannot tolerate high thermal exposure. Domestic players, including Wanhua Chemical, are significantly expanding production of low-temperature curing resins, reinforcing China’s position as a global manufacturing powerhouse in this segment.

India Low Temperature Coatings Market: Infrastructure Growth and Consumer Manufacturing Driving Adoption

India’s low temperature coatings market is witnessing rapid expansion, fueled by infrastructure development, rising consumer demand, and government-backed manufacturing initiatives. Programs such as the Gati Shakti master plan are driving demand for anti-corrosive, energy-efficient coating solutions in logistics, transportation, and heavy infrastructure projects.

The “Make in India” initiative is accelerating local production of consumer appliances, including air conditioners and refrigerators, which are key end-users of low-cure powder coatings. A significant shift from traditional liquid paints to low-temperature powder coatings is being observed in the furniture and construction sectors, driven by cost efficiency and reduced emissions. Investments by companies like Kansai Nerolac and Berger Paints in R&D for energy-efficient coatings are strengthening the domestic ecosystem. The demand is particularly strong for corrosion-resistant coatings suitable for India’s high-humidity environments, especially in agricultural and construction equipment applications.

Japan Low Temperature Coatings Market: Advanced Materials and Precision Coating Technologies

Japan’s low temperature coatings market is characterized by its focus on high-performance materials, precision engineering, and advanced coating innovations. The development of nanocomposite coatings is enabling superior scratch resistance, chemical durability, and performance even at reduced curing temperatures.

Japanese manufacturers are also leading in self-healing low-temperature coatings, capable of autonomously repairing micro-cracks, enhancing product longevity. These coatings are widely used in industrial robotics and precision optics, where thermal sensitivity and accuracy are critical. Investments in UV-curing and photopolymerization technologies are enabling rapid coating of complex 3D-printed components. Regulatory compliance under the Chemical Substances Control Law (CSCL) is encouraging the adoption of bio-renewable and low-toxicity materials, further supporting sustainable innovation. Additionally, the introduction of ultra-matte finishes for premium consumer electronics and automotive interiors is expanding application scope.

South Korea Low Temperature Coatings Market: Semiconductor and Battery Innovation Driving Demand

South Korea is emerging as a critical market for low temperature coatings, driven by its global leadership in semiconductor manufacturing, EV batteries, and advanced electronics. Significant investments in the Gyeonggi Province semiconductor cluster are increasing demand for coatings used in high-vacuum lithography equipment, where low-temperature application is essential to prevent damage to sensitive components.

Technological advancements such as moisture-cure low-temperature coatings are eliminating the need for high-energy curing ovens, improving efficiency for large-scale industrial components. These coatings are also widely applied in EV battery systems, including cell partitions and cooling plates, where electrical insulation and thermal stability are crucial. Companies like KCC Corporation are expanding their industrial coatings divisions to cater to shipbuilding and offshore wind sectors. Regulatory updates under K-REACH are promoting the use of safer, low-temperature curing agents, while innovations such as low-temperature coatings for plastic automotive components are supporting the transition toward multi-material vehicle design.

Low Temperature Coatings Market Report Scope

Low Temperature Coatings Market

Parameter

Details

Market Size (2025)

$13.9 Billion

Market Size (2032)

$22.8 Billion

Market Growth Rate

7.3%

Segments

By Resin Type (Polyester, Epoxy, Polyurethane, Acrylic, Specialty Resins), By Technology (Powder Coatings, Water-borne, Solvent-borne, UV), By Substrate Type (Metals, Plastics and Composites, Wood and Medium-Density Fibreboard, Engineered Glass, Electronics), By End-Use Industry (Automotive and Transportation, Consumer Goods and Appliances, Furniture, Architectural and Construction, Industrial Manufacturing, Medical and Healthcare), By Curing Profile (Standard Low-Cure, Ultra-Low-Bake, Ambient), By Application Method (Electrostatic Spraying, Fluidized Bed Coating, Dip and Flow Coating, Coil Coating), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Contract Coating Service Providers)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, BASF SE, Axalta Coating Systems Ltd., Jotun A/S, Hempel A/S, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., RPM International Inc., Tiger Coatings GmbH and Co. KG, Teknos Group, Beckers Group, IGP Pulvertechnik AG, Forrest Technical Coatings

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Low Temperature Coatings Market Segmentation

By Resin Type

Polyester

Epoxy

Polyurethane

Acrylic

Specialty Resins

By Technology

Powder Coatings

Water-borne

Solvent-borne

UV

By Substrate Type

Metals

Plastics and Composites

Wood and Medium-Density Fibreboard

Engineered Glass

Electronics

By End-Use Industry

Automotive and Transportation

Consumer Goods and Appliances

Furniture

Architectural and Construction

Industrial Manufacturing

Medical and Healthcare

By Curing Profile

Standard Low-Cure

Ultra-Low-Bake

Ambient

By Application Method

Electrostatic Spraying

Fluidized Bed Coating

Dip and Flow Coating

Coil Coating

By Sales Channel

Direct Sales

Specialty Industrial Distributors

Contract Coating Service Providers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Low Temperature Coatings Industry

PPG Industries, Inc.

Akzo Nobel N.V.

The Sherwin-Williams Company

BASF SE

Axalta Coating Systems Ltd.

Jotun A/S

Hempel A/S

Nippon Paint Holdings Co., Ltd.

Kansai Paint Co., Ltd.

RPM International Inc.

Tiger Coatings GmbH & Co. KG

Teknos Group

Beckers Group

IGP Pulvertechnik AG

Forrest Technical Coatings

*- List not Exhaustive

Table of Contents: Low Temperature Coatings Market

2. Low Temperature Coatings Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Low Temperature Coatings Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the Low Temperature Coatings Market

3.1. Trend: Arctic Pipeline Expansion Accelerating Adoption of Low-Temperature-Cure Epoxy Coatings

3.2. Trend: Polyurea Low-Temperature Coatings Enabling Year-Round Offshore Wind Installation

3.3. Opportunity: Canadian Arctic Infrastructure Fund Driving Demand for Cold-Applied High-Durability Coatings

3.4. Opportunity: U.S. DoD Arctic Strategy Accelerating Ultra-Low Temperature Coating Adoption

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Low Temperature Coatings Market

5.1. By Resin Type

5.1.1. Polyester

5.1.2. Epoxy

5.1.3. Polyurethane

5.1.4. Acrylic

5.1.5. Specialty Resins

5.2. By Technology

5.2.1. Powder Coatings

5.2.2. Water-borne

5.2.3. Solvent-borne

5.2.4. UV

5.3. By Substrate Type

5.3.1. Metals

5.3.2. Plastics and Composites

5.3.3. Wood and Medium-Density Fibreboard

5.3.4. Engineered Glass

5.3.5. Electronics

5.4. By End-Use Industry

5.4.1. Automotive and Transportation

5.4.2. Consumer Goods and Appliances

5.4.3. Furniture

5.4.4. Architectural and Construction

5.4.5. Industrial Manufacturing

5.4.6. Medical and Healthcare

5.5. By Curing Profile

5.5.1. Standard Low-Cure

5.5.2. Ultra-Low-Bake

5.5.3. Ambient

5.6. By Application Method

5.6.1. Electrostatic Spraying

5.6.2. Fluidized Bed Coating

5.6.3. Dip and Flow Coating

5.6.4. Coil Coating

5.7. By Sales Channel

5.7.1. Direct Sales

5.7.2. Specialty Industrial Distributors

5.7.3. Contract Coating Service Providers

6. Country Analysis and Outlook of Low Temperature Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Low Temperature Coatings Market Size Outlook by Region (2025–2034)

7.1. North America Low Temperature Coatings Market Size Outlook to 2034

7.1.1. By Resin Type

7.1.2. By Technology

7.1.3. By Substrate Type

7.1.4. By End-Use Industry

7.1.5. By Curing Profile

7.1.6. By Application Method

7.1.7. By Sales Channel

7.2. Europe Low Temperature Coatings Market Size Outlook to 2034

7.2.1. By Resin Type

7.2.2. By Technology

7.2.3. By Substrate Type

7.2.4. By End-Use Industry

7.2.5. By Curing Profile

7.2.6. By Application Method

7.2.7. By Sales Channel

7.3. Asia Pacific Low Temperature Coatings Market Size Outlook to 2034

7.3.1. By Resin Type

7.3.2. By Technology

7.3.3. By Substrate Type

7.3.4. By End-Use Industry

7.3.5. By Curing Profile

7.3.6. By Application Method

7.3.7. By Sales Channel

7.4. South America Low Temperature Coatings Market Size Outlook to 2034

7.4.1. By Resin Type

7.4.2. By Technology

7.4.3. By Substrate Type

7.4.4. By End-Use Industry

7.4.5. By Curing Profile

7.4.6. By Application Method

7.4.7. By Sales Channel

7.5. Middle East and Africa Low Temperature Coatings Market Size Outlook to 2034

7.5.1. By Resin Type

7.5.2. By Technology

7.5.3. By Substrate Type

7.5.4. By End-Use Industry

7.5.5. By Curing Profile

7.5.6. By Application Method

7.5.7. By Sales Channel

8. Company Profiles: Leading Players in the Low Temperature Coatings Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. The Sherwin-Williams Company

8.4. BASF SE

8.5. Axalta Coating Systems Ltd.

8.6. Jotun A/S

8.7. Hempel A/S

8.8. Nippon Paint Holdings Co., Ltd.

8.9. Kansai Paint Co., Ltd.

8.10. RPM International Inc.

8.11. Tiger Coatings GmbH and Co. KG

8.12. Teknos Group

8.13. Beckers Group

8.14. IGP Pulvertechnik AG

8.15. Forrest Technical Coatings

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Low Temperature Coatings Market Segmentation

By Resin Type

Polyester

Epoxy

Polyurethane

Acrylic

Specialty Resins

By Technology

Powder Coatings

Water-borne

Solvent-borne

UV

By Substrate Type

Metals

Plastics and Composites

Wood and Medium-Density Fibreboard

Engineered Glass

Electronics

By End-Use Industry

Automotive and Transportation

Consumer Goods and Appliances

Furniture

Architectural and Construction

Industrial Manufacturing

Medical and Healthcare

By Curing Profile

Standard Low-Cure

Ultra-Low-Bake

Ambient

By Application Method

Electrostatic Spraying

Fluidized Bed Coating

Dip and Flow Coating

Coil Coating

By Sales Channel

Direct Sales

Specialty Industrial Distributors

Contract Coating Service Providers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global low temperature coatings market was valued at $13.9 billion in 2025 and is projected to reach $22.8 billion by 2032, expanding at a CAGR of 7.3%. Growth is being driven by rising demand for low-cure powder coatings, ambient-cure coatings, low-temperature electrocoats, and energy-efficient industrial coating technologies across automotive, infrastructure, furniture, electronics, and industrial manufacturing sectors.

Low temperature coatings significantly reduce curing energy requirements by enabling curing at temperatures as low as 80°C to 150°C or even under ambient conditions. Manufacturers can achieve energy savings of 20% to 50%, reduce carbon emissions, and coat heat-sensitive substrates such as plastics, composites, MDF, and electronics without deformation. These benefits are accelerating adoption in automotive OEMs, consumer appliances, and industrial fabrication facilities focused on decarbonization and operational efficiency.

The expansion of Arctic pipeline infrastructure and offshore wind installations is creating strong demand for cold-cure epoxy and polyurea coating systems capable of curing in sub-zero environments. Advanced low-temperature coatings now cure effectively at temperatures as low as -20°C while maintaining corrosion resistance, adhesion strength, and rapid return-to-service performance. These technologies help extend construction windows, reduce operational delays, and improve long-term durability in extreme environmental conditions.

Europe and North America lead the market due to strong sustainability regulations, industrial energy-efficiency initiatives, and advanced automotive manufacturing. Asia-Pacific is rapidly expanding through growth in EV production, electronics manufacturing, consumer appliances, and industrial modernization projects in China, South Korea, India, and Japan. Major application sectors include automotive, infrastructure, aerospace, offshore energy, consumer electronics, furniture, and industrial maintenance.

Major companies operating in the low temperature coatings industry include PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, BASF SE, Axalta Coating Systems Ltd., Jotun A/S, Hempel A/S, and Nippon Paint Holdings Co., Ltd.. These companies are investing in low-bake powder coatings, UV-curable technologies, cold-cure epoxies, sustainable resin systems, and AI-driven coating innovations to strengthen their global market presence.