Low VOC Paint Market Size, Indoor Air Quality Regulations, and Sustainable Coatings Demand Outlook

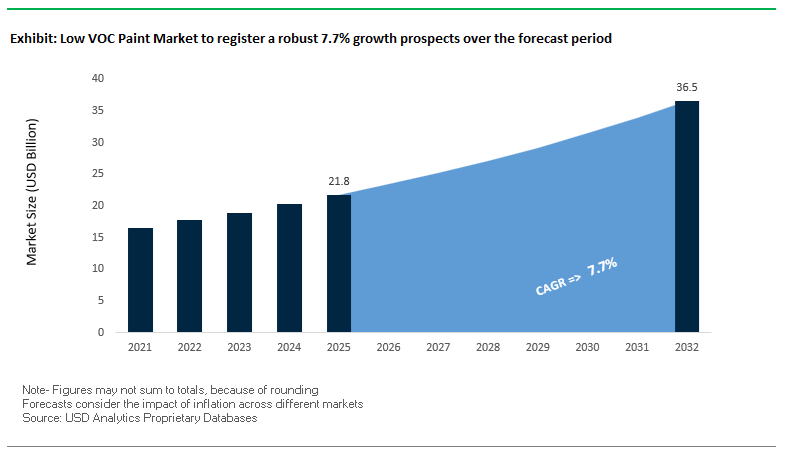

The global low VOC paint market was valued at $21.8 billion in 2025 and is projected to reach $36.6 billion by 2032, expanding at a robust CAGR of 7.7%. This growth is being driven by increasing demand for low-VOC paints, zero-VOC coatings, waterborne architectural coatings, and eco-friendly interior paints across residential, commercial, healthcare, and institutional construction sectors. As regulatory bodies tighten restrictions on volatile organic compound (VOC) emissions, low VOC paints are becoming the standard for indoor air quality (IAQ) compliance, green building certifications, and occupant health safety.

A key growth driver is the heightened awareness of indoor air pollution and its health implications, particularly in enclosed environments such as homes, offices, hospitals, and schools. Low VOC and zero-emission coatings significantly reduce toxic off-gassing, odor levels, and long-term exposure risks, making them essential for wellness-focused building design. Additionally, the shift toward water-based coatings and plant-based resins is accelerating as manufacturers align with ESG goals, sustainability mandates, and circular economy initiatives.

The market is also benefiting from rapid urbanization, renovation cycles, and the expansion of green building standards such as LEED and WELL certifications. Innovations in air-purifying paints, formaldehyde-absorbing coatings, and low-odor fast-drying formulations are enhancing product differentiation and performance. Regionally, Asia-Pacific dominates due to large-scale construction activity and growing environmental awareness, while North America and Europe lead in regulatory enforcement, premium product adoption, and sustainable coating innovation.

Market Analysis: Ultra-Low Emission Innovations, and ESG-Driven Strategies Reshaping Market Dynamics

The low VOC paint industry is undergoing significant transformation driven by consolidation, sustainability innovation, and strategic repositioning toward premium eco-friendly coatings. A major development occurred in January 2026, when AkzoNobel and Axalta announced a $25 billion merger of equals, combining AkzoNobel’s decorative leadership (Dulux) with Axalta’s industrial and refinish portfolio. This merger is expected to accelerate innovation and global distribution of low-VOC and waterborne coating technologies, particularly in the premium architectural segment.

Sustainability and product stewardship are becoming central to competitive strategy. Nippon Paint’s 2025–2026 Medium-Term Strategy, released in February 2026, emphasizes scaling its network of Authorized Service Providers (ASPs) while increasing the share of ultra-low VOC products and recycled-content packaging across its portfolio. Similarly, Asian Paints reported in May 2025 that over 95% of its decorative coatings portfolio is now lead-free and low-VOC, supported by a new automated manufacturing facility in India focused on eco-friendly emulsions.

Product innovation is advancing toward zero-emission and bio-based formulations. In November 2025, Behr launched BEHR PREMIUM PLUS® ECOMIX™, a plant-based, zero-VOC interior paint meeting stringent sustainability certifications. Benjamin Moore further strengthened this trend with its next-generation Eco Spec paint, introduced in September 2025, which maintains zero VOC emissions even after tinting and is specifically designed for sensitive environments such as hospitals and schools, with ultra-low odor profiles.

Leading players are also focusing on functional performance enhancements alongside sustainability. Jotun’s January 2025 upgrade to its Majestic Sense line incorporates “Clean Air” technology, capable of actively absorbing formaldehyde while maintaining ultra-low VOC emissions, reflecting growing demand for air-purifying coatings. AkzoNobel’s September 2025 “Rhythm of Blues” color launch further integrates region-specific low-VOC formulations, ensuring consistent air-quality performance across global markets.

Strategic portfolio realignment is also influencing the market landscape. Sherwin-Williams’ August 2025 integration of BASF’s Suvinil business strengthens its presence in Latin America’s low-VOC decorative coatings segment, while PPG Industries’ October 2024 divestment of its North American architectural coatings business marks a shift toward high-performance industrial coatings, reducing its exposure to the retail low-VOC segment.

Expansion strategies in premium segments are also evident. Hempel A/S, following strong financial performance in January 2026, announced the expansion of its Farrow & Ball luxury retail format, focusing on water-based, ultra-low VOC premium interior finishes in North America, targeting high-end consumers seeking both aesthetic quality and environmental compliance.

Market Trend: Zero-VOC Interior Paint Adoption Accelerating High-Velocity Real Estate Turnover and Premium Leasing

The low VOC paint industry is undergoing a structural shift as real estate developers and hospitality asset managers standardize Zero-VOC interior coatings to optimize occupancy cycles and enhance indoor environmental quality. Multifamily housing developers and hotel REITs are increasingly specifying coatings with VOC content below 5 g/L to eliminate the off-gassing delays associated with conventional latex paints, which typically require 48 to 72 hours before safe occupancy.

This transition is directly improving asset utilization metrics. Zero-VOC coatings enable same-day occupancy following painting activities, resulting in measurable reductions in vacancy downtime. Industry data indicates that hotel renovation cycles leveraging ultra-low odor coatings tested under ASTM D6886 standards achieve approximately 15% faster room turnover rates. This improvement translates into higher revenue realization per available room, particularly in high-demand urban markets.

Tenant preference is also reinforcing this trend. A 2025 survey of multifamily residents reveals that 68% of premium tenants prioritize indoor air quality as a key decision factor. This has led developers to integrate Green Seal GS-11 certified products into their standard specifications, positioning IAQ as a differentiating feature in competitive rental markets. Projects marketed under “Healthy Home” certifications are reporting rental premiums in the range of 3% to 5%, particularly in mature markets such as New York and London.

Operational cost efficiencies further strengthen the business case. The elimination of residual chemical odors reduces strain on HVAC systems, resulting in a 20% decrease in air filtration maintenance and filter replacement cycles during large-scale repainting programs. These combined economic, environmental, and occupant-driven factors are positioning Zero-VOC paints as a standard specification in modern residential and hospitality developments.

Market Trend: Bio-Functional Low-VOC Coatings Advancing Infection Control in Healthcare Environments

The healthcare sector is advancing beyond passive emission reduction toward multifunctional low VOC coatings that actively contribute to infection control and patient well-being. These next-generation coatings integrate antimicrobial technologies such as silver-ion additives and photocatalytic agents, enabling continuous suppression of pathogens on coated surfaces. This evolution reflects the increasing emphasis on environmental hygiene as a core component of clinical safety protocols.

Performance benchmarks for these coatings are significant. Certified antimicrobial low VOC paints demonstrate the ability to inhibit up to 99.9% of bacteria, including resistant strains such as MRSA and E. coli, within two hours of exposure. This capability supports sterile zone management in high-risk areas such as intensive care units, operating rooms, and isolation wards. Unlike traditional disinfectants, these coatings provide continuous protection without requiring reapplication, ensuring consistent hygiene coverage.

Durability under aggressive cleaning conditions is another critical attribute. Healthcare-grade low VOC coatings are engineered to withstand more than 1,000 scrub cycles using hospital-grade disinfectants without degradation of their antimicrobial properties. This ensures long-term functionality in environments with strict sanitation protocols. Additionally, compliance with UL GREENGUARD Gold certification standards enables these coatings to maintain extremely low indoor emissions, reducing formaldehyde concentrations below the 9-ppb threshold in sensitive environments such as pediatric and oncology wards.

Patient experience metrics also highlight the impact of low VOC formulations. The reduction of paint-related odors contributes to improved comfort levels, with studies indicating a 12% increase in patient satisfaction scores linked to enhanced indoor air quality. These factors collectively position bio-functional low VOC coatings as a critical innovation in healthcare infrastructure design and infection prevention strategies.

Market Opportunity: CARB 2027 SCM Driving Transition to Ultra-Low VOC Industrial and Marine Coatings

The tightening of environmental regulations in the United States is creating a significant opportunity landscape for low VOC paint technologies, particularly in industrial maintenance and marine applications. The California Air Resources Board is advancing its 2027 Suggested Control Measure, which is expected to significantly lower permissible VOC levels, creating a strong market shift toward waterborne and high-solids coating systems.

The proposed reduction in VOC limits for industrial maintenance coatings from 250 g/L to 100 g/L represents a substantial regulatory compression that will require reformulation of a large portion of existing products. This is driving immediate demand for advanced low VOC epoxies and polyurethane systems capable of meeting performance requirements under stricter emission thresholds. The regulatory influence of California extends beyond state boundaries, as approximately 12 additional states are expected to align with CARB standards within a two-year period, amplifying the market impact.

The marine coatings segment is also undergoing transformation under these regulations. New formulations must simultaneously meet low-VOC and low-leach requirements, accelerating the adoption of silicone-based foul-release coatings. These advanced systems offer operational benefits, including approximately 10% improvement in fuel efficiency due to reduced hydrodynamic drag, creating a strong value proposition for commercial shipping operators.

From a compliance perspective, early adoption of CARB-compliant coatings provides financial advantages. Facilities transitioning in advance of enforcement timelines can avoid escalating non-compliance penalties, which are projected to increase by 20% under the updated framework. This regulatory shift is positioning low VOC technologies as essential solutions for both compliance and operational efficiency in industrial and marine coating markets.

Market Opportunity: India CPCB VOC Regulations Unlocking Growth for Waterborne and Eco-Friendly Architectural Paints

India’s evolving regulatory framework for architectural coatings is creating a high-growth opportunity for low VOC paint manufacturers. The Central Pollution Control Board has introduced draft regulations that establish defined VOC limits for the first time in the country’s rapidly expanding paint market. These proposed limits, including 50 g/L for interior emulsions and 200 g/L for enamels, will necessitate reformulation of a significant portion of existing product portfolios.

This regulatory development is expected to act as a catalyst for market transformation. More than 40% of current paint formulations in India exceed the proposed VOC thresholds, creating a substantial replacement demand for compliant low VOC alternatives. The integration of these standards with green building certification systems such as those promoted by the Indian Green Building Council further strengthens adoption. Projects utilizing compliant paints gain additional scoring advantages, supporting India’s expanding smart city and sustainable infrastructure initiatives.

Consumer awareness is also playing a critical role in market expansion. Rising concerns over air quality in urban centers are driving a shift toward eco-friendly paints, with demand projected to grow at approximately 25% annually through 2027 in Tier 1 and Tier 2 cities. This shift is particularly evident in the transition away from high-odor solvent-based distempers toward waterborne emulsions and low VOC formulations.

From a supply-side perspective, global and domestic manufacturers are increasing investments in localized research and development capabilities focused on low VOC technologies. This includes the establishment of dedicated innovation centers to develop water-based alternatives tailored to regional climatic and application conditions. These combined regulatory, consumer, and industrial factors are positioning India as a key growth market for low VOC architectural paints in the global coatings industry.

Low VOC Paint Market Share and Segmentation Insights

Architectural and Decorative Low-VOC Paints Capture 52% Share Amid Regulatory Push and Sustainability Demand

The low VOC paint market by product category is led by architectural and decorative coatings, accounting for 52% of the global market share in 2025, driven by stringent environmental regulations and rising sustainability awareness. Regulatory frameworks such as the EPA AIM (Architectural & Industrial Maintenance) rules and the EU Paints Directive have accelerated the adoption of low-VOC latex emulsions, waterborne alkyds, and eco-friendly interior paints across residential and commercial construction. Additionally, green building certifications like LEED, BREEAM, and WELL mandate the use of low-emission coatings, influencing architects, contractors, and homeowners to prioritize certified low-VOC solutions. This segment benefits from high repainting frequency in urban housing and commercial spaces, further boosting demand. As a result, architectural coatings remain the cornerstone of the sustainable paints and coatings market, combining compliance, indoor air quality improvement, and aesthetic performance.

Home Improvement Retail Chains Hold 38% Share with Strong DIY and Private Label Growth

In the low VOC paint market by sales channel, home improvement (big box) retailers dominate with a 38% market share in 2025, fueled by strong DIY repainting trends and retail accessibility. Consumers prefer large-format stores such as Home Depot, Lowe’s, and B&Q for their convenience, competitive pricing, and integrated color matching kiosks, which simplify the paint selection process. These retailers also benefit from the expansion of private label low-VOC paint brands, including Behr, Valspar, and Dulux retail lines, offering cost-effective alternatives to premium specialty coatings. This strategy allows retailers to capture higher margins while appealing to price-sensitive consumers seeking environmentally friendly options. The dominance of big box channels is further reinforced by growing consumer awareness of indoor air quality, low-emission paints, and sustainable home improvement solutions, making them the primary distribution hub for mass-market low-VOC coatings.

Competitive Landscape in the Low VOC Paint Market

AkzoNobel drives consolidation and near-zero VOC innovation in decorative coatings

AkzoNobel is a dominant force in the low VOC paint market, driven by its strategic move toward an all-stock merger with Axalta, expected to create the world’s largest coatings company with a 20% share in the premium low-VOC architectural segment. The company reported a 14.2% adjusted EBITDA margin in 2025, supported by strong price-mix growth and cost optimization initiatives targeting €200 million in annual savings. Its “Rhythm of Blues” 2026 collection features next-generation near-zero VOC resin technology, achieving comparable opacity with 15% lower material usage. AkzoNobel’s AI-driven Dulux Visualizer enhances color precision while reducing sample waste and secondary emissions, reinforcing its leadership in sustainable and digitally enabled paint solutions.

PPG expands ultra-low VOC technologies for infrastructure and high-tech environments

PPG Industries is strengthening its position in the low VOC paint market by integrating industrial durability with advanced low-emission technologies. In 2026, the company invested in a radiation-curable coatings testing line in France, eliminating the need for thermal curing and significantly reducing VOC emissions during application. PPG is targeting hyperscale data centers with specialized coating systems designed to protect sensitive electronic infrastructure from contamination. Its acquisition of Ozark Materials enhances its presence in sustainable infrastructure coatings, particularly in pavement markings. The company has achieved 50% of its 2030 Scope 1 and 2 emissions reduction target, driven by electrification of manufacturing processes, positioning it as a leader in environmentally responsible coating production.

Sherwin-Williams dominates contractor-driven low VOC paint demand in North America

The Sherwin-Williams Company maintains a leading position in the North American low VOC paint market, with an estimated 39.2% market share in 2026 supported by its extensive network of over 4,800 company-operated stores. The company’s strategy focuses on high-build, low-odor coatings tailored for professional contractors and repaint applications. Its Harmony® Zero VOC interior acrylic latex introduces air-purifying functionality, actively reducing airborne VOCs from external sources after application. Sherwin-Williams also leverages its PRO+ digital platform, enabling contractors to track LEED and GREENGUARD certifications, streamlining compliance for green building projects. With record net sales of $23.57 billion in 2025, the company is expanding into Asia-Pacific to capture emerging demand for sustainable coatings.

BASF enables next-generation low VOC paints through advanced dispersion chemistry

BASF plays a critical enabling role in the low VOC paint market by supplying advanced chemical dispersions that support near-zero emission formulations. In 2026, the company introduced a breakthrough near-zero SVOC technology that eliminates semi-volatile compounds, enabling room occupancy within 2–4 hours after application. BASF is advancing beyond low-odor coatings toward air-purifying solutions that actively capture indoor pollutants such as formaldehyde. Its TÜV Rheinland-certified Eco Impact Assessment tool provides transparent lifecycle carbon footprint analysis, supporting regulatory compliance and sustainability reporting. BASF’s expertise in multi-phase morphology resins ensures high durability, stain resistance, and performance without relying on traditional solvent-based additives.

Nippon Paint drives functional low VOC coatings across Asia-Pacific markets

Nippon Paint Holdings leads the Asia-Pacific low VOC paint market by focusing on functional coatings that combine aesthetics with health and safety benefits. Under its 2026 medium-term strategy, the company is aligning growth with regional economic expansion, particularly in China’s renovation and urban development sectors. Its Perfect Silver Ion series offers antiviral and antibacterial low VOC coatings, increasingly mandated in healthcare and public infrastructure projects. Nippon Paint is also expanding its portfolio beyond paints to include sealants, adhesives, and waterproofing solutions, creating integrated green building systems. Its development of bio-based wall paints, replacing up to 30% of petroleum-derived resins, reinforces its commitment to sustainable innovation without compromising product performance.

Asian Paints strengthens low VOC coatings with climate-adaptive and aesthetic innovations

Asian Paints dominates the low VOC paint market in developing economies, particularly India, with a market share exceeding 50% supported by a robust distribution network of over 70,000 retail outlets. The company’s 2026 “Moonlit Silk” collection integrates premium texture finishes with zero-VOC, water-based formulations designed for humid climates. Its SmartCare waterproofing systems utilize low-VOC liquid membranes to protect structures from extreme weather conditions such as monsoons while maintaining indoor air quality. Asian Paints has also introduced self-cleaning, low-dust exterior coatings that reduce maintenance requirements and extend product lifespan. By combining aesthetic innovation with functional performance, the company continues to redefine low VOC coatings for emerging markets.

China Low VOC Paint Market: Scaling Green Infrastructure and Industrial Decarbonization

China leads the low VOC paint market globally, driven by aggressive environmental regulations and rapid expansion in green infrastructure and high-tech manufacturing sectors. Under the “14th Five-Year Plan”, the government has mandated a reduction in VOC emissions across industrial coating applications, particularly targeting major industrial clusters such as the Yangtze River Delta and Pearl River Delta. This regulatory push is accelerating the shift from solvent-based coatings to waterborne polyurethane (WPU) and UV-curable low VOC paints, especially in electronics and consumer durables manufacturing.

Large-scale urban renewal and infrastructure programs are further fueling demand, with over $1.1 trillion allocated for green infrastructure projects, where low VOC coatings are mandatory. Domestic players such as Nippon Paint China and 3trees are expanding production capacity to meet demand for high-performance net-zero architectural coatings. The adoption of anti-formaldehyde and air-purifying paints in healthcare and education sectors, aligned with updated safety standards, is reinforcing China’s leadership in environmentally sustainable coatings. Additionally, the implementation of Green Credit policies is incentivizing developers to prioritize eco-labeled, low-emission paint solutions.

United States Low VOC Paint Market: Regulatory Leadership and Bio-Based Coating Innovation

The United States represents a high-value low VOC paint market, defined by stringent environmental regulations and continuous innovation in sustainable coatings. Policies such as SCAQMD Rule 1113, which limits VOC content in architectural coatings to extremely low levels, are setting global benchmarks and driving manufacturers toward near-zero emission formulations.

Leading companies like Sherwin-Williams and PPG are pioneering paints with over 40% bio-based content, derived from renewable sources such as agricultural waste. Investments under the Inflation Reduction Act (IRA) are accelerating adoption of low VOC coatings in commercial and residential retrofitting projects. Technological advancements include smart odor-neutralizing additives that actively eliminate indoor pollutants, enhancing indoor air quality. The market is also witnessing strong adoption in LEED-certified construction projects and automotive refinish applications, where waterborne coatings are becoming standard to comply with state-level environmental regulations.

Germany Low VOC Paint Market: Circular Economy Leadership and Advanced Eco-Labeling Standards

Germany stands as a European leader in low VOC paint adoption, driven by its commitment to sustainability, circular economy principles, and strict eco-labeling frameworks. Initiatives led by the German Sustainable Building Council (DGNB) are pushing manufacturers to adopt life-cycle assessment (LCA)-based product development, favoring coatings with cradle-to-cradle certifications.

Technological innovations such as self-healing and antimicrobial low VOC coatings are reducing maintenance cycles and overall material consumption. The expansion of the Blue Angel (Blauer Engel) eco-label is further raising industry standards by incorporating strict testing for semi-volatile organic compounds (SVOCs), encouraging the development of 100% solids and waterborne coatings. Germany’s dominance in the industrial wood coatings segment is supported by its strong furniture export industry, which is transitioning to low-emission UV-curable systems. Additionally, R&D investments by companies like AkzoNobel and BASF SE are driving the development of VOC-free catalysts and high-durability coatings for emerging sectors such as hydrogen infrastructure.

India Low VOC Paint Market: Rapid Urbanization and Green Building Certifications Driving Growth

India is emerging as the fastest-growing low VOC paint market, supported by increasing urbanization, rising environmental awareness, and strong government initiatives. Certification programs such as CII-GreenPro are becoming critical in the construction sector, with developers increasingly mandating low VOC or zero-VOC paints for residential and commercial projects.

The government’s ambitious plan to invest $1.3 trillion in housing development is creating substantial demand for eco-friendly coatings. Domestic manufacturers like Asian Paints and Berger Paints are expanding production facilities to deliver affordable, localized low VOC emulsions. The market is also benefiting from growth in the electric vehicle manufacturing sector, where low VOC coatings are used to meet global ESG standards. Innovations such as natural paints derived from traditional materials and anti-fungal, moisture-resistant coatings tailored for India’s monsoon climate are further expanding product adoption across both urban and rural segments.

Japan Low VOC Paint Market: Precision Innovation and Wellness-Oriented Coating Technologies

Japan’s low VOC paint market is characterized by advanced material science, precision manufacturing, and a strong focus on indoor environmental quality. The country is pioneering visible-light photocatalytic coatings, which actively decompose VOCs and pathogens under indoor lighting conditions, making them ideal for healthcare facilities and eldercare environments.

Strict regulatory compliance with the Building Standard Law, including adherence to F☆☆☆☆ (F-Four Star) emission standards, ensures minimal indoor air pollution. In the automotive sector, Japanese manufacturers are leading the adoption of waterborne multi-layer coating systems, significantly reducing solvent usage in production processes. Innovations in nano-silica-based coatings are delivering superior durability and stain resistance, particularly for urban infrastructure. Additionally, the integration of low VOC coatings into Society 5.0 smart city initiatives highlights Japan’s commitment to sustainable and health-focused urban development.

UAE Low VOC Paint Market: Net-Zero Construction and Sustainable Urban Development

The United Arab Emirates is rapidly emerging as a key market for low VOC paints in the Middle East, driven by ambitious sustainability goals and large-scale infrastructure projects. Initiatives such as Dubai’s Net Zero by 2050 strategy and the Al Sa’fat Green Building System are mandating the use of low-emission coatings in construction and development projects.

The adoption of low heat-absorption and high solar reflectance coatings is playing a critical role in reducing urban heat island effects in mega projects such as the Dubai 2040 Urban Master Plan. Low VOC paints are extensively used in aviation, hospitality, and commercial sectors, where rapid-drying, low-odor coatings are essential for minimizing operational downtime. Product innovations such as cool-roof coatings and bio-renewable maritime paints are further expanding application areas. Regulatory frameworks like the Estidama Pearl Rating System are reinforcing the adoption of environmentally friendly coatings across public infrastructure and real estate developments.

Low VOC Paint Market Report Scope

Low VOC Paint Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.8 Billion

|

|

Market Size (2032)

|

$36.6 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By VOC Content Type (Low-VOC, Zero-VOC, Natural, Ultra-Low VOC), By Resin Type (Acrylic, Alkyd, Epoxy, Polyurethane, Vinyl Acetate Ethylene, Natural Binders), By Formulation Technology (Water-borne, High-Solids Solvent-borne, Powder Coatings, Radiation-Cured), By Product Category (Architectural and Decorative, Industrial Coatings, Automotive and Transportation Coatings, Marine Coatings, Wood and Furniture Coatings), By End-Use Sector (Residential, Commercial, Industrial and Infrastructure, Government and Institutional), By Surface (Interior Walls and Ceilings, Exterior Facades, Flooring Systems, Trim, Doors and Cabinetry), By Functional Property (Anti-Microbial, Odor-Absorbing, Stain and Scrub Resistant, Mold and Mildew Resistant), By Sales Channel (Specialty Paint Stores, Home Improvement, E-commerce, Direct Sales), By Price Tier (Economy, Mid-Range, Premium)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., BASF SE, Axalta Coating Systems Ltd., Asian Paints Limited, Jotun A/S, Kansai Paint Co., Ltd., Benjamin Moore and Co., RPM International Inc., Hempel A/S, Behr Process Corporation, Dunn-Edwards Corporation, Grasim Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Low VOC Paint Market Segmentation

By VOC Content Type

- Low-VOC

- Zero-VOC

- Natural

- Ultra-Low VOC

By Resin Type

- Acrylic

- Alkyd

- Epoxy

- Polyurethane

- Vinyl Acetate Ethylene

- Natural Binders

By Formulation Technology

- Water-borne

- High-Solids Solvent-borne

- Powder Coatings

- Radiation-Cured

By Product Category

- Architectural and Decorative

- Industrial Coatings

- Automotive and Transportation Coatings

- Marine Coatings

- Wood and Furniture Coatings

By End-Use Sector

- Residential

- Commercial

- Industrial and Infrastructure

- Government and Institutional

By Surface

- Interior Walls and Ceilings

- Exterior Facades

- Flooring Systems

- Trim, Doors and Cabinetry

By Functional Property

- Anti-Microbial

- Odor-Absorbing

- Stain and Scrub Resistant

- Mold and Mildew Resistant

By Sales Channel

- Specialty Paint Stores

- Home Improvement

- E-commerce

- Direct Sales

By Price Tier

- Economy

- Mid-Range

- Premium

Top Companies in Low VOC Paint Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- BASF SE

- Axalta Coating Systems Ltd.

- Asian Paints Limited

- Jotun A/S

- Kansai Paint Co., Ltd.

- Benjamin Moore & Co.

- RPM International Inc.

- Hempel A/S

- Behr Process Corporation

- Dunn-Edwards Corporation

- Grasim Industries Limited

*- List not Exhaustive