Organic Coatings Market Size, Bio-Based Resin Innovation, and High-Performance Protective Coatings Outlook

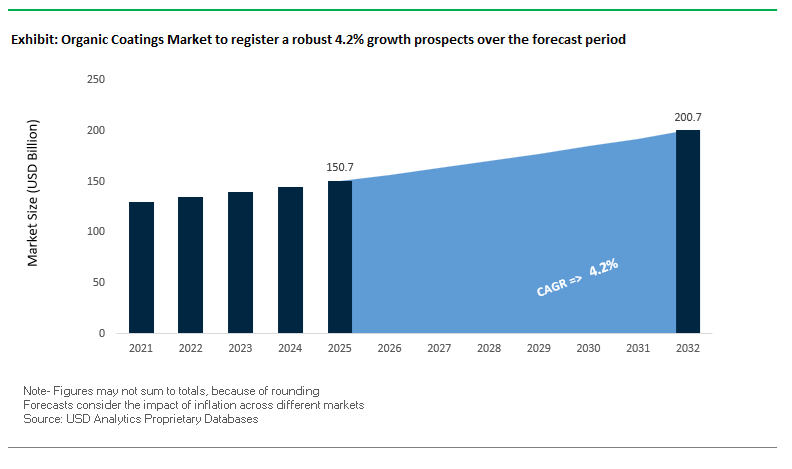

The global organic coatings market was valued at $150.7 billion in 2025 and is projected to reach $201 billion by 2032, expanding at a CAGR of 4.2%. Growth is supported by rising demand for organic coatings, waterborne coatings, solvent-borne coatings, powder coatings, epoxy coatings, polyurethane coatings, and acrylic-based coatings across construction, automotive, marine, aerospace, packaging, and industrial applications. These coatings rely on organic binders and polymer resins to deliver corrosion protection, surface durability, chemical resistance, and aesthetic performance, making them essential across both protective and decorative segments.

A key growth driver is the global transition toward low-VOC, sustainable, and bio-based coating systems, driven by tightening environmental regulations and corporate decarbonization goals. Increasing adoption of waterborne and high-solids coatings is reducing solvent emissions while maintaining performance standards. Additionally, the growing need for high-performance coatings in infrastructure, mobility, and energy sectors is driving innovation in resin chemistry, durability, and lifecycle performance.

The market is also benefiting from advancements in functional coatings, including anti-corrosion, anti-microbial, UV-resistant, and chemical-resistant formulations, which extend asset lifespan and reduce maintenance costs. Demand for aesthetic differentiation, particularly in automotive and architectural applications, is driving the adoption of advanced pigments, special effect coatings, and customizable finishes. Regionally, Asia-Pacific leads due to strong construction and manufacturing activity, while Europe and North America focus on sustainability-driven innovation and regulatory compliance.

Market Analysis: Bio-Based Coating Breakthroughs, and Sustainability-Driven Innovation Shaping Market Dynamics

The organic coatings industry is undergoing a structural shift driven by major consolidation, sustainability initiatives, and advancements in resin technology. The most significant development occurred in February 2026, when AkzoNobel and Axalta announced a merger of equals, creating a global powerhouse that combines architectural, decorative, industrial, and mobility coatings expertise. This consolidation is expected to reshape global resin procurement, R&D investment, and competitive dynamics across the organic coatings value chain.

Financial performance across leading companies highlights a strategic focus on profitability and high-value segments. AkzoNobel reported 2025 revenue of €10.16 billion with a 14.2% EBITDA margin, driven by a price-over-volume strategy and portfolio optimization, including the divestment of lower-margin operations. Similarly, PPG Industries achieved record net sales of $15.9 billion, supported by strong growth in aerospace and protective coatings, while Sherwin-Williams reported $23.57 billion in sales, bolstered by the integration of Suvinil and increasing demand for specialized performance coatings.

Sustainability and bio-based innovation are emerging as central growth pillars. A major milestone was achieved in January 2026, when Mitsui Chemicals and Chugoku successfully scaled a bio-based epoxy resin coating (CMP NOVA 2000 Bio) for use in a liquefied ammonia tanker, demonstrating the viability of 100% plant-derived organic binders in large-scale industrial applications. This aligns with the September 2025 partnership between AkzoNobel, Arkema, and BASF, which focuses on developing low-carbon coatings using mass-balance organic resins to reduce Scope 3 emissions.

Product innovation is also enhancing performance and aesthetics. BASF Coatings’ October 2025 “DRIVING THE PROXY” collection introduces advanced multi-color pigments and liquid-metal effects, incorporating renewable and recycled raw materials to meet both aesthetic and sustainability requirements. Meanwhile, PPG Industries’ PPG INNOVEL®, highlighted in its July 2025 sustainability report, has become a global standard for PFAS-free organic coatings in metal packaging, reflecting the growing demand for safe and compliant coating solutions.

Strategic expansions and acquisitions are strengthening global market presence. Kansai Helios’ May 2024 acquisition of Weilburger Coatings expands its portfolio in specialized organic coatings, including non-stick and industrial applications, while Nippon Paint’s 2024–2026 regional strategy focuses on eco-friendly and anti-viral coatings for Southeast Asia’s rapidly growing construction and healthcare sectors.

Market Trend: Waterborne Acrylic-Alkyd Hybrid Coatings Driving Low-VOC Architectural Enamel Performance and Fast Drying Cycles

The organic coatings industry is witnessing a decisive transition toward waterborne acrylic-alkyd hybrid coatings in architectural enamels, as manufacturers address the long-standing trade-off between performance and environmental compliance. Traditional solvent-borne alkyd coatings are rapidly losing share in regulated markets due to high VOC emissions and extended drying times, prompting a shift toward hybrid resin technologies that combine alkyd durability with acrylic efficiency.

Waterborne acrylic-alkyd hybrid coatings deliver a strong balance of hardness, gloss retention, and drying speed. These formulations achieve dry-to-touch times of 30 to 60 minutes, a substantial improvement over the 6 to 12 hours typically required for conventional alkyd enamels. At the same time, they maintain high 60-degree gloss retention comparable to oil-based systems, ensuring premium finish quality for doors, trims, and cabinetry applications.

VOC compliance is a central driver of adoption. Hybrid coatings typically operate below 50 g/L VOC, allowing manufacturers to meet stringent regulatory frameworks such as SCAQMD Rule 1113 in the United States and the EU Decopaint Directive without sacrificing film performance. This regulatory alignment is accelerating market penetration, with approximately 38% to 42% of global resin producers redirecting R&D investments toward hybrid technologies as of early 2026. In parallel, solvent-borne alkyd usage has declined by approximately 9% in regulated markets over the past two years, indicating a clear structural shift toward waterborne organic coatings.

The convergence of regulatory compliance, performance parity, and faster production cycles is positioning acrylic-alkyd hybrid coatings as a dominant solution in the architectural segment, particularly in premium and professional-grade applications where both durability and environmental credentials are critical.

Market Trend: Ultra-High Solids Epoxy Primers Enhancing Efficiency and Corrosion Protection in Industrial Organic Coatings

Industrial OEMs and infrastructure asset owners are increasingly adopting ultra-high solids epoxy coatings as a strategy to improve application efficiency and reduce lifecycle emissions. These systems, with solids content ranging from 90% to 95%, are redefining performance benchmarks in heavy-duty protective coatings for sectors such as agriculture, construction, and marine infrastructure.

Ultra-high solids epoxy primers offer significantly improved coverage efficiency. A 95% solids formulation provides nearly double the square-foot coverage per gallon compared to conventional 50% solids primers, reducing logistics requirements, storage costs, and overall material consumption by approximately 45% in large-scale operations. This efficiency gain is particularly valuable in high-volume coating applications where throughput and cost control are critical.

Corrosion resistance performance has also advanced substantially. Modern ultra-high solids epoxy coatings are engineered to exceed 2,000 hours of Neutral Salt Spray testing under ASTM B117 conditions, delivering C5-M level protection in a single coat. This eliminates the need for multi-coat systems and extended curing cycles, reducing downtime and simplifying application processes in industrial environments.

From an environmental standpoint, ultra-high solids coatings significantly reduce VOC emissions, typically maintaining levels below 100 g/L. This enables facilities to comply with evolving environmental regulations while minimizing the need for emission control infrastructure. As industrial operators increasingly prioritize efficiency-per-gallon and carbon footprint reduction, ultra-high solids epoxy coatings are becoming a core technology in modern organic coating systems.

Market Opportunity: EU Industrial Emissions Directive Revision Driving Mandatory Transition to Low-VOC and Zero-VOC Organic Coatings

The revision of the EU Industrial Emissions Directive is creating a major inflection point for the organic coatings industry, particularly as member states move toward full implementation by July 2026. The updated directive enforces stricter emission limit values based on Best Available Techniques, effectively requiring facilities to operate at the lowest achievable VOC emission levels.

This regulatory shift is forcing approximately 20% of industrial coating facilities currently operating at the upper end of permissible VOC ranges to undergo immediate upgrades. Manufacturers are increasingly transitioning to waterborne, high-solids, or powder-based organic coatings to achieve compliance while maintaining operational efficiency. The directive also introduces enhanced legal accountability, including provisions for compensation related to health impacts from non-compliance, significantly increasing the risk exposure for operators relying on legacy solvent-based systems.

Financial penalties further reinforce this transition. Non-compliance can result in fines of at least 3% of annual EU turnover, creating a strong economic incentive for rapid adoption of low-VOC coating technologies. This regulatory environment is driving accelerated investment in sustainable coating solutions and creating substantial opportunities for suppliers offering compliant, high-performance organic coatings tailored to industrial applications.

Market Opportunity: China GB/T 38597-2025 Enforcement Accelerating Demand for Ultra-Low VOC Organic Coatings in Infrastructure and Manufacturing

China’s implementation of GB/T 38597-2025 is reshaping the organic coatings market by enforcing strict VOC limits and expanding regulatory oversight across industrial and infrastructure applications. The standard mandates that coatings used in government-backed projects meet ultra-low VOC thresholds, typically below 250 g/L for waterborne systems and below 100 g/L for powder coatings.

This requirement is driving mandatory recertification across the coatings value chain, creating a large-scale transition toward compliant formulations. The regulation also expands the list of controlled substances from 105 to 346, significantly increasing the complexity of formulation and favoring suppliers with advanced, high-purity chemistries. This expansion is opening new design-in opportunities for global resin manufacturers capable of meeting stringent environmental and safety criteria.

Monitoring and enforcement mechanisms are also becoming more rigorous. Integration of the standard into China’s Pollutant Discharge Permit System requires real-time emissions reporting, increasing transparency and compliance pressure on coating manufacturers and end users. This is expected to drive a 25% increase in demand for waterborne and high-solids organic coatings in key industrial regions such as the Pearl River Delta and Yangtze River Delta.

The scale of China’s manufacturing and infrastructure sectors amplifies the impact of these regulations, positioning the country as a major growth engine for ultra-low VOC organic coatings. Suppliers aligned with regulatory requirements and capable of delivering high-performance, environmentally compliant solutions are expected to benefit from sustained market expansion.

Organic Coatings Market Share and Segmentation Insights

Basecoats Capture 35.8% Share Driven by Color Performance and Large-Scale Application Needs

The organic coatings market by type of formulation is led by basecoats, accounting for 35.8% of the global market share in 2025, due to their critical role in delivering color, visual aesthetics, and functional surface effects. Basecoats are responsible for metallic finishes, pearlescent effects, and color depth in key industries such as automotive coatings, architectural coatings, and industrial finishes, making them the most value-added and formulation-intensive coating layer. Additionally, basecoats are applied at film thicknesses of 15–25 microns across large surface areas, including vehicle bodies, building panels, and appliances, resulting in the highest material consumption among organic coatings. With increasing demand for customized coatings, premium finishes, and durable color retention, basecoats continue to dominate the global organic coatings market.

Direct Sales Hold 48.6% Share Driven by Technical Customization and Bulk Industrial Demand

In the organic coatings market by sales channel, direct sales dominate with a 48.6% market share in 2025, reflecting the need for close technical collaboration and consistent supply for large-scale buyers. Industrial and automotive OEMs require precise color matching, batch-to-batch consistency, and optimized application parameters, including viscosity control, pot life, and curing schedules, which can only be ensured through direct manufacturer engagement. Furthermore, major end-users such as automotive assembly plants and coil coating operations rely on multi-year supply agreements to guarantee formulation stability, quality assurance, and cost efficiency. This direct relationship enables suppliers to provide customized coating solutions, technical support, and process optimization, which are critical for high-performance applications. As a result, direct sales remain the preferred channel in the global organic coatings market.

Competitive Landscape of the Organic Coatings Market

AkzoNobel Advances Bio-Based Organic Coatings Through Profit-Led Growth Strategy

AkzoNobel N.V. is strengthening its position in the European organic coatings market through a profit-over-volume strategy designed to navigate weak construction demand. In Q1 2026, the company reported adjusted EBITDA of €345 million and expanded its margin to 14.5%, supported by 9% revenue optimization after divesting South Asian assets. Its planned merger with Axalta, expected to close in late 2026 or early 2027, is projected to generate €600 million in annual synergies. AkzoNobel is also advancing bio-based architectural paints under Dulux, using up to 35% plant-based resins, while its €20 million Italian powder coatings expansion targets premium organic-hybrid metallic finishes.

PPG Leads High-Margin Organic Coatings for Aerospace, Automotive, and Energy Assets

PPG Industries, Inc. is leveraging its global R&D scale to lead innovation in aerospace organic coatings, automotive OEM finishes, and industrial protective coatings. In 2026, the company reported record Q1 earnings, driven by double-digit aerospace growth and the launch of iPura™ for monobloc aerosol cans. After divesting its U.S. and Canadian architectural coatings business worth $2 billion in revenue, PPG is refocusing on high-margin performance coatings. Its low-bake organic automotive clearcoat cures at 80°C, reducing paint-line energy use while preserving Class A gloss and DOI. PPG also remains a leader in high-solids organic epoxy mastics for corrosion under insulation protection.

Sherwin-Williams Strengthens Waterborne Organic Coatings with Digital Asset Monitoring

The Sherwin-Williams Company remains a dominant force in the North American organic coatings market, supported by its extensive retail and professional contractor network. The company forecasted full-year 2026 adjusted EPS of $11.50 to $11.90, reflecting resilience in architectural coatings despite elevated interest rates. Its Syntha Pulvin® organic powder coating range for architectural aluminum now meets AAMA 2605 specifications with zero-VOC formulations. In 2026, Sherwin-Williams launched SHIFT, an industrial color trend forecast using organic pigment technology for vibrant, UV-stable outdoor metal coatings. Its Sher-Loram™ digital platform further strengthens asset integrity management by tracking degradation of organic protective coatings in real time.

Axalta Expands Mobility and Wood OEM Organic Coatings Ahead of AkzoNobel Integration

Axalta Coating Systems is a major player in refinish, mobility, and industrial organic coatings, with strong momentum ahead of its planned integration with AkzoNobel. In 2026, the company earned three Edison Awards for AI-powered color technology and EV safety coatings, including its Alesta® e-PRO range for battery-cell electrical insulation. Axalta achieved a record 22.0% adjusted EBITDA margin in fiscal 2025, reinforcing its valuation strength before the merger. Its Zencore™ Cabinet Coating System, launched in April 2026, targets the wood OEM market with a high-performance waterborne organic coating that matches solvent-based urethane durability.

BASF Drives Green Transformation with Bio-Attributed Resins and Functional Organic Coatings

BASF SE remains a leading chemical innovator in the organic coatings market, supplying both advanced resins and finished coatings for heavy industrial and automotive applications. In 2026, the company maintained €2.0 billion in R&D spending, with a strong focus on green transformation dispersions and bio-attributed acrylates. At the American Coatings Show 2026, BASF introduced a waterborne 2K direct-to-metal organic coating that eliminates primer use and reduces total system VOCs by 65%. Its ChemCycling initiative converts plastic waste into organic monomers for premium automotive OEM coatings. BASF also leads in functional organic ED-coat systems, supporting 30% of global vehicle production in 2026.

United States Organic Coatings Market: PFAS-Free Transition and Smart Functional Coatings

The United States organic coatings market is defined by a “compliance-performance” dual strategy, driven by strict environmental regulations and high-performance industrial requirements. The EPA’s TSCA Section 8(a)(7) update (2026) has accelerated the phase-out of PFAS, resulting in a 22% surge in demand for silicone-alkyd and bio-epoxy alternatives.

Technological advancements include self-healing organic primers, which use micro-encapsulated linseed oil to repair micro-cracks in pipeline coatings, enhancing durability and reducing maintenance costs. Government support through the Inflation Reduction Act (IRA) is promoting cool roof coatings with NIR-reflective pigments, reducing urban heat effects. Strategic expansions by companies like Sherwin-Williams in waterborne resin production are supporting EV battery and semiconductor applications requiring ultra-low outgassing (ULOG) coatings. Additionally, innovations in PFAS-free hybrid coatings for aerospace MRO are reinforcing the U.S. position as a leader in advanced organic coatings.

Germany Organic Coatings Market: Bio-Based Chemistry and Circular Economy Leadership

Germany is a global leader in bio-based organic coatings, focusing on reducing dependence on fossil fuels through innovations in renewable binder chemistry. The development of 100% bio-based polyurethane resins, derived from lignin and castor oil, is achieving performance comparable to conventional petroleum-based systems.

Technological leadership includes the use of digital twin simulations, enabling accelerated testing of coating durability over decades within hours. Germany’s alignment with the EU’s Safe and Sustainable by Design (SSbD) framework is pushing the elimination of hazardous additives such as cobalt driers and certain biocides. Investments like Henkel’s acquisition of Stahl Holdings (2026) are strengthening the country’s leadership in high-value organic coatings for automotive and textile applications. Additionally, innovations such as carbon-capture coatings are being deployed in smart city projects, actively reducing atmospheric CO₂.

China Organic Coatings Market: Green Manufacturing and High-Volume Industrial Transition

China is transitioning from a volume-driven to a “green-first” organic coatings market, supported by strict VOC regulations under the “Blue Sky Defense” policy (2026). This policy effectively bans coatings with VOC levels above 250 g/L in urban areas, accelerating the shift toward waterborne organic coatings.

Technological advancements include graphene-modified organic primers, providing enhanced corrosion protection for offshore wind infrastructure. China is also expanding AI-driven, carbon-neutral coating plants, such as Nippon Paint’s facility that reduces water waste by 45%. Key applications include coatings for 6G telecommunications infrastructure, requiring high electromagnetic transparency, and high-speed rail systems, where UV-resistant coatings ensure durability in extreme conditions. These developments reinforce China’s dominance in both scale and sustainable innovation.

India Organic Coatings Market: Infrastructure Expansion and Domestic Manufacturing Growth

India is the fastest-growing market for organic coatings, driven by rapid urbanization and strong government initiatives such as the National Infrastructure Pipeline and PLI schemes. These initiatives are boosting demand for high-performance epoxy coatings, particularly in bridge rehabilitation and infrastructure projects.

The market is seeing increasing adoption of monomer-free organic coatings, designed for India’s tropical climate, along with innovations in antimicrobial wall coatings for healthcare infrastructure. Growth in consumer electronics manufacturing is also driving demand for premium organic finishes in smartphones and tablets. Additionally, applications such as heat-reflective coatings for railway systems like Vande Bharat are improving energy efficiency and passenger comfort. Localized R&D centers are further strengthening India’s capability to develop region-specific coating solutions.

Japan Organic Coatings Market: Precision Aesthetics and Smart Functional Surfaces

Japan’s organic coatings market is characterized by high-performance, functionalized coatings, combining aesthetics with advanced material science. Innovations such as photocatalytic organic-hybrid coatings enable self-cleaning surfaces by decomposing pollutants under visible light, maintaining long-term durability and appearance.

Technological advancements include ultra-thin organic coatings, achieving full opacity at minimal thickness, reducing material usage and cost. Japan is also advancing coatings for robotics and medical applications, offering resistance to aggressive disinfectants while maintaining a premium tactile feel. Regulatory compliance under CSCL 2026 updates is driving safer material formulations. Additionally, innovations such as anti-condensation coatings for Maglev rail systems highlight Japan’s leadership in specialized infrastructure applications.

South Korea Organic Coatings Market: Energy Storage and Flexible Electronics Innovation

South Korea is emerging as a key hub for advanced organic coatings, driven by its dominance in EV batteries and flexible electronics. The development of high-dielectric organic coatings is enabling improved insulation and performance in battery separators and energy storage systems.

Innovations such as “flexi-organic” coatings, capable of withstanding over 300,000 fold cycles, are supporting next-generation foldable devices. Government initiatives like the K-Battery Strategy are promoting the development of solvent-free organic coatings, enhancing sustainability and performance. Investments in advanced R&D facilities, including KCC Corporation’s centers, are accelerating innovation in silicone-organic hybrid coatings. Additionally, the adoption of bio-renewable soy-based primers reflects South Korea’s commitment to sustainable materials.

Organic Coatings Market Report Scope

Organic Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$150.7 Billion

|

|

Market Size (2032)

|

$201 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Resin Type (Acrylic, Epoxy, Polyurethane, Alkyd, Polyester, Vinyl and Chlorinated Rubber, Bio-based Resins, Amino Resins), By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, Radiation-Cured, High-Solids Liquid Coatings), By End-Use Industry (Building and Construction, Automotive and Transportation, Industrial, Marine, Packaging, Energy and Power), By Function (Protective Coatings, Decorative Coatings, Functional), By Substrate (Metals, Wood, Concrete and Masonry, Plastics and Polymers, Composites), By Type of Formulation (Primers, Basecoats, Topcoats, Clearcoats), By Sales Channel (Direct Sales, Specialty Distributors and Wholesalers, Retail, Online)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., The Sherwin-Williams Company, Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., Axalta Coating Systems Ltd., BASF SE, Kansai Paint Co., Ltd., Asian Paints Limited, Jotun A/S, Hempel A/S, Masco Corporation, KCC Corporation, Beckers Group, Berger Paints India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Coatings Market Segmentation

By Resin Type

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- Polyester

- Vinyl and Chlorinated Rubber

- Bio-based Resins

- Amino Resins

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- Radiation-Cured

- High-Solids Liquid Coatings

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- Industrial

- Marine

- Packaging

- Energy and Power

By Function

- Protective Coatings

- Decorative Coatings

- Functional

By Substrate

- Metals

- Wood

- Concrete and Masonry

- Plastics and Polymers

- Composites

By Type of Formulation

- Primers

- Basecoats

- Topcoats

- Clearcoats

By Sales Channel

- Direct Sales

- Specialty Distributors and Wholesalers

- Retail

- Online

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Organic Coatings Industry

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Axalta Coating Systems Ltd.

- BASF SE

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- Jotun A/S

- Hempel A/S

- Masco Corporation

- KCC Corporation

- Beckers Group

- Berger Paints India Limited

*- List not Exhaustive