Market Overview: Performance Benchmarks Reshaping the Functional Printing Consumables Market

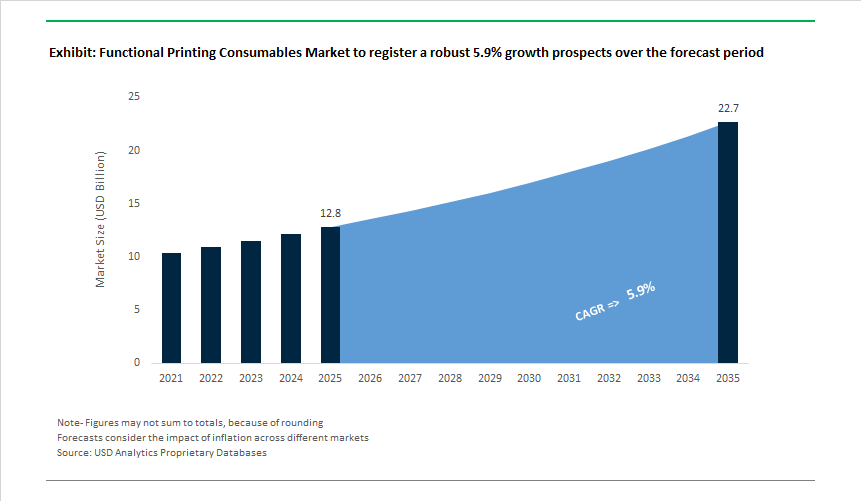

The Functional Printing Consumables Market, valued at USD 12.8 billion in 2025 and forecast to reach USD 22.7 billion by 2035 at a 5.9% CAGR, has become strategically critical as electronics manufacturing shifts from subtractive, material-intensive processes toward additive, thin-film, and digitally enabled production architectures. Functional printing consumables-spanning conductive and dielectric inks, photosensitive polyimides, UV-curable functional coatings, and engineered substrates-now sit directly on the critical path of innovation in printed electronics, advanced semiconductor packaging, smart packaging, sensors, and IoT devices. For OEMs and Tier-1 suppliers, these materials are no longer interchangeable inputs; they define achievable line widths, signal integrity, device yield, and long-term reliability in increasingly compact and flexible form factors.

Market demand is being reshaped by a structural convergence of miniaturization, high-volume manufacturability, and sustainability mandates. Device architectures are moving toward finer geometries, multilayer stackups, and heterogeneous integration, forcing consumable suppliers to engineer inks and coatings with tightly controlled particle size distributions, impurity thresholds, and rheological windows compatible with inkjet, gravure, screen, and aerosol jet printing. Conductive inks based on silver, copper, and emerging carbon systems must balance low resistivity after low-temperature sintering with oxidation stability and adhesion to polymer substrates, while dielectric inks and photosensitive polyimides are increasingly specified for low dielectric constant (low-k), high breakdown voltage, and dimensional stability during thermal cycling. At the same time, OEMs are pushing suppliers toward low-VOC, solvent-reduced, and UV-curable formulations to align with cleaner fab operations and regulatory frameworks governing emissions and worker exposure.

Legacy subtractive metallization and rigid PCB processes are being displaced in targeted applications by printed, roll-to-roll compatible consumables that enable faster design iteration, reduced material waste, and scalable production of flexible and hybrid electronics. From a business performance perspective, consumables that deliver consistent deposition accuracy, predictable sintering behavior, and high registration fidelity across multilayer builds directly translate into higher yields, lower scrap rates, and improved equipment uptime in high-volume lines. Looking ahead, competitive advantage in the functional printing consumables market will hinge on manufacturers’ ability to co-develop materials with equipment OEMs and device designers, ensure supply stability for critical raw materials, and certify formulations against evolving semiconductor and electronics qualification standards-positioning consumables not as commodities, but as enabling technologies within next-generation electronics manufacturing ecosystems.

Market Analysis: Strategic Developments in Printed Electronics & Advanced Consumables

The global functional printing consumables landscape experienced accelerated innovation and capacity expansion, driven by semiconductor packaging, flexible electronics manufacturing, and the rapid scale-up of smart retail and IoT applications. A major milestone was the Dec 2025 launch of Fujifilm’s ZEMATES™ photosensitive insulating materials, signaling a strategic shift toward high-reliability dielectrics for AI semiconductors and advanced chip packaging. Nov 2025 saw BASF significantly increase R&D investment across Asia-Pacific to advance bio-based and low-VOC polymer chemistries, strengthening the supply base for sustainable printed coatings and industrial inks. On the other hand, Henkel introduced new sub-100°C-processable silver inks in Oct 2025, directly addressing demand from wearables and smart textiles, where low-temperature sintering is mandatory for polymer compatibility.

In Sep 2025, E Ink Holdings confirmed its electrophoretic display materials were used in 85% of global ESL installations, reinforcing the dominance of functional materials in Retail IoT infrastructure. Complementing this, Aug 2025 saw Dupont Teijin Films expand polyester substrate capacity used in flexible electronics and EV battery sensors, signaling a long-term demand trajectory for mechanically stable, heat-resistant films. Sustainability remained a core driver, with Jun 2025 ACTEGA’s ECOLEAF metallization gaining rapid traction as a low-waste alternative to foil stamping. Medical diagnostics also surged: Mar 2025 global conductive ink suppliers reported a 15% volume increase in carbon and Ag/AgCl inks for disposable biosensors, reflecting growth in point-of-care medical devices. Academic innovation continued to shape future material pathways, highlighted by Jan 2025 research demonstrating stable, graphene-based inks with silver-comparable conductivity - a potential cost disruptor for printed electronics relying on scarce metals.

Functional Printing Consumables Market Trends and Opportunities

High-Conductivity, Low-Temperature Curable Inks Powering Flexible Hybrid Electronics

The functional printing consumables market is being structurally reshaped by the rapid commercialization of flexible hybrid electronics (FHE), where conductive performance must coexist with temperature-sensitive substrates. Manufacturers are increasingly specifying low-temperature curable conductive inks that sinter below 150 °C, enabling direct printing on PET, paper, TPU, and stretchable elastomers without warping or delamination. This shift is not incremental—it is unlocking entirely new product classes in RFID antennas, wearable biosensors, smart packaging, and in-mold electronics (IME).

By 2025, industrial benchmarks show that low-cure ink formulations reduce oven energy consumption by up to 40%, while also shortening takt time and improving line throughput. At global additive manufacturing showcases such as Formnext 2024–2025, suppliers demonstrated inks curing at ~120 °C, a meaningful reduction from the legacy 160 °C baseline that historically constrained substrate choice. Electrically, advances in silver nanoparticle (AgNP) inks have narrowed the performance gap with bulk silver, achieving resistivities only 3–5× higher after low-temperature sintering—sufficient for high-frequency signal paths in automotive HMI panels exposed to UV, flexing, and vibration.

Cost pressure, however, is accelerating parallel innovation in copper-based conductive inks. With engineered anti-oxidation shells and sintering aids, copper inks are becoming viable for high-volume, short-lifecycle electronics such as smart labels and disposable sensor arrays. Strategically, this dual-track development—premium AgNP inks for performance-critical circuits and copper inks for scale-driven applications—is expanding the addressable market for functional printing consumables across consumer electronics, logistics, and industrial IoT.

Bio-Inks and Biocompatible Resins Redefining Medical and 4D Printing

A second, high-value transformation is unfolding in bio-inks and biocompatible photopolymer resins, driven by healthcare’s shift toward patient-specific and bioactive devices. Unlike traditional medical polymers, next-generation consumables are engineered to replicate the extracellular matrix (ECM) while maintaining print fidelity, sterilization resistance, and predictable degradation profiles.

In May 2025, BIO INX introduced READYPCL INX, the first commercially available polyester-based resin compatible with volumetric bioprinting, enabling rapid fabrication of biodegradable scaffolds with embedded cellular viability. In parallel, its gelatin-based BIORES INX addressed long-standing constraints in DLP bioprinting, including water evaporation and thermal instability during long build cycles. These launches signal a transition from experimental bio-inks to off-the-shelf clinical consumables.

On the device side, high-resolution SLA and DLP resins—such as the Loctite 3D MED series—are now achieving 25–50 µm feature resolution while surviving 25+ autoclave cycles without dimensional drift. This reliability is critical for customized surgical guides, dental frameworks, and permanent orthopedic implants. Meanwhile, research institutions including IMDEA Materials Institute are advancing bioresorbable magnesium alloys and 4D-printable polymers that gradually dissolve or morph post-implantation. For pediatric and trauma care, these consumables eliminate secondary removal surgeries, aligning clinical outcomes with cost-efficiency—a powerful adoption driver for hospitals and device OEMs.

Sustainable and Covert Security Inks as a Core Anti-Counterfeiting Layer

Escalating global counterfeiting has elevated security inks from a niche application to a strategic necessity in pharmaceuticals, government documents, and premium consumer goods. Brands are increasingly embedding covert functional markers—optically variable inks (OVIs), up-converting phosphors, magnetic taggants—directly into packaging and printed electronics to ensure end-to-end traceability.

In March 2025, scientists at Bhabha Atomic Research Centre unveiled a nanoparticle-based security ink using strontium bismuth fluoride, creating a high-complexity optical signature that is effectively non-reproducible at scale. This level of material sophistication is particularly relevant for high-value pharmaceuticals and official credentials, where traditional visible markers are easily mimicked.

Commercially, firms such as Avery Dennison and Sun Chemical are integrating security inks with NFC- and QR-enabled smart labels, blending consumer-facing authentication with forensic-grade back-end verification. Regulatory momentum is reinforcing this opportunity: tax banderols, excise labels, and national ID programs increasingly mandate inks with defined magnetic, infrared, or spectral responses compatible with automated inspection systems. For consumable suppliers, security inks represent a high-margin, regulation-anchored growth avenue with strong customer lock-in.

Functional Inks Enabling Printed Sensors for Smart Infrastructure and Industry 4.0

The emergence of the “Internet of Surfaces” (IoS) marks a fundamental shift in sensing architectures—from discrete, centralized devices to distributed, printed, and often disposable sensors embedded directly onto assets. Functional printing consumables are at the core of this transition, enabling low-cost deployment across agriculture, infrastructure, and industrial operations.

In 2025, the NASA–ISRO NISAR Mission has catalyzed adoption of ground-level printed sensors that complement satellite radar data. High-speed roll-to-roll (R2R) printed moisture and nutrient sensors are being deployed across U.S. and Indian farmlands, delivering hyper-local soil intelligence that optimizes irrigation and fertilizer use while reducing input waste.

Industrial applications are equally compelling. European process plants are adopting screen-printed gas sensor arrays based on PANI/MoS₂ composites, capable of detecting ammonia at concentrations as low as ~122 ppb at room temperature—without pumps or moving parts. This solid-state simplicity lowers maintenance costs and enables predictive maintenance strategies aligned with Industry 4.0. Beyond factories, the ability to print strain, humidity, and corrosion sensors directly onto curved or inaccessible surfaces—such as turbine blades, storage tanks, and bridges—supports continuous structural health monitoring. Stretchable silver inks and transparent conductive films maintain functionality across extreme thermal cycling (−40 °C to 85 °C), positioning functional printing consumables as a foundational technology for smart infrastructure at scale.

Market Share Analysis: Functional Printing Consumables Market

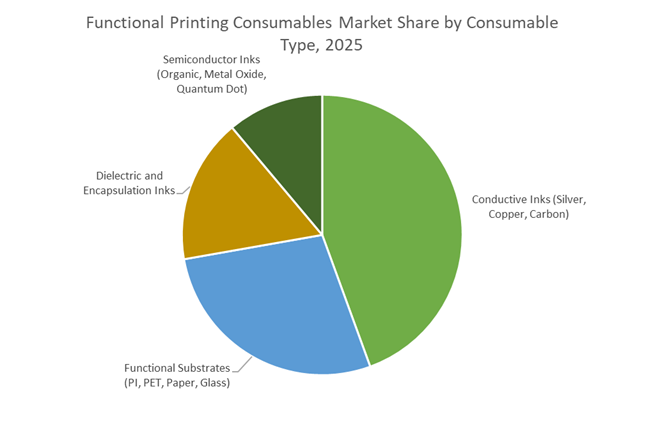

Market Share by Consumable Type: Conductive Inks Form the Backbone of Printed Electronics Manufacturing

Conductive inks account for approximately 40% of the global Functional Printing Consumables Market, reflecting their central role as the enabling material for printed electronics, smart surfaces, and flexible circuitry. This dominance is driven by conductive inks’ ability to deliver electrical functionality through scalable, additive manufacturing processes, replacing etched copper and rigid printed circuit boards in cost- and design-sensitive applications. In 2025, market leadership is being reinforced by advances in high-efficiency sintering technologies, which have dramatically lowered sheet resistance and narrowed the performance gap with traditional conductors while preserving the flexibility and lightweight advantages of printing. Improved coverage efficiency has further strengthened adoption, as manufacturers can achieve larger printable areas with lower material usage, directly improving unit economics for high-volume consumer and industrial production. Reliability has become a decisive purchasing criterion, with leading conductive inks now validated for long-term thermal and humidity stability, supporting multi-year device lifetimes in real-world environments. At the same time, the emergence of silver-plated copper and pure copper inks is reshaping cost structures by reducing exposure to silver price volatility, expanding adoption beyond premium electronics into mass-market applications such as RFID, membrane switches, and sensors. Together, these performance, cost, and scalability drivers position conductive inks as the functional core of the printed electronics value chain, securing their leading market share.

Market Share by Application: Consumer Electronics Drive Volume and Innovation in Functional Printing

The consumer electronics segment represents approximately 35% of total demand in the Functional Printing Consumables Market, making it the largest and most innovation-driven application area. This leadership is anchored in the sector’s relentless push toward thinner, lighter, and more integrated device designs, where functional printing enables capabilities that rigid electronics cannot economically deliver. Technologies such as in-mold electronics allow circuits, sensors, and touch interfaces to be printed directly onto structural components, reducing part count, eliminating wiring, and delivering substantial weight and space savings. Market share is further reinforced by assembly cost reductions, as printed conductive pathways replace mechanical buttons and complex harnesses, simplifying manufacturing and improving yield. The rapid expansion of wearables and smart textiles has added momentum, with stretchable conductive inks now meeting durability requirements for repeated washing and mechanical deformation without electrical failure. Fast digital curing and processing technologies also accelerate product development cycles, enabling consumer electronics brands to prototype, iterate, and launch new designs far more quickly than with conventional electronics fabrication. As device manufacturers compete on form factor, speed-to-market, and user experience, consumer electronics remain the primary demand engine for functional printing consumables, sustaining their dominant share in the global market.

Competitive Landscape: Leading Suppliers Of Functional Printing Consumables

The competitive landscape is defined by companies that integrate chemistry, materials science, and high-precision deposition technologies. Leadership is closely tied to innovation velocity, semiconductor packaging compatibility, sustainable formulations, and the ability to support high-volume roll-to-roll and digital printing platforms. Below is the structured competitive overview.

Henkel AG & Co. Kgaa - Global Leader in Conductive & Dielectric Ink Systems

Henkel dominates the market for conductive, dielectric, and resistive inks through advanced formulations developed for screen, gravure, and inkjet printing. Its Loctite® silver/silver-chloride inks hold a leading share in ECG electrodes and printed biosensors, making Henkel a critical supplier for global medical device manufacturing. The company’s strategic push into E-Mobility through PTC resistive inks strengthens its footprint in seat heaters and EV thermal management systems. Henkel also invests heavily in UV-curable conductive materials, which enable high-speed, low-energy roll-to-roll production with excellent adhesion to polymer substrates.

Dupont De Nemours, Inc. - Pioneer in Polymer Thick Film Inks & Photovoltaic Materials

DuPont offers one of the broadest portfolios supporting flexographic, digital, and specialty printed electronics. Its polymer thick film (PTF) inks are industry benchmarks for membrane switches, resistors, and low-resistance circuits used in industrial and consumer electronics. Leveraging deep chemical expertise, DuPont also supplies advanced photovoltaic pastes critical for solar cell electrode efficiency. Its strategic emphasis on automotive sensors and ADAS systems is driving the development of inks that retain electrical and mechanical performance across extreme temperature cycles.

BASF SE - Advanced Polymer Provider For Functional Coatings & High-Purity Inks

BASF plays a crucial role in supplying polymers, dispersions, and additives that enable critical ink properties such as adhesion, flexibility, heat resistance, and controlled viscosity. Its sustainability roadmap emphasizes bio-based and renewable-carbon ink components, aligning with rising global demand for environmentally compliant packaging consumables. BASF’s materials are also foundational in inkjet inks for OLED displays, where ultralow particle size, controlled rheology, and high stability are essential for micro-circuit precision. Its global scale ensures consistent pigment dispersion performance across major regional manufacturing hubs.

Fujifilm Corporation - Rising Powerhouse in Photosensitive Materials & High-Precision Inkjet Fluids

Fujifilm’s ZEMATES™ launch marks a strategic elevation of its semiconductor materials portfolio, targeting 5× sales growth in back-end packaging films by FY2030. The company is already a global leader in functional inkjet fluids, leveraging imaging science to engineer inks with controlled particle size and high jetting stability. Fujifilm also contributes essential materials for image sensors, micro-lenses, and color filter fabrication, reinforcing its position in the high-value optoelectronics ecosystem. Its development of PLP-compatible polyimide films aligns with industry migration to larger substrate formats.

E Ink Holdings Inc. - Dominant Supplier Of Electrophoretic Display Consumables

E Ink maintains unrivaled leadership in electrophoretic display films, controlling the majority share of functional consumables used in ePaper displays and ESL systems. Its micro-capsule/micro-cup technologies enable ultra-low-power reflective displays suited for IoT, signage, and wearables. Engineered for durability, E Ink’s materials withstand hundreds of thousands of flex cycles, making them ideal for flexible smart cards and ruggedized devices. Strategic collaborations with retail technology providers ensure continued ESL market penetration and next-generation display innovations.

The United States functional printing consumables market in 2025 is anchored to advanced semiconductor packaging, medical diagnostics, and printed electronics reshoring. Under the CHIPS and Science Act, the U.S. Department of Commerce has rolled out a $1.6 billion funding opportunity supporting ultra-high-purity conductive pastes, dielectric inks, and functional coatings for silicon-core and glass-core substrates. This policy framework is accelerating domestic demand for silver nanoparticle inks, low-loss dielectric formulations, and additive manufacturing consumables compatible with advanced IC packaging and heterogeneous integration.

Trade dynamics further reinforce localization. Targeted tariffs on imported printed electronic components in early 2025 have redirected procurement toward U.S. suppliers such as DuPont and PPG Industries, stimulating investments in CVD-grown materials, bio-derived solvents, and PFAS-free functional inks. Momentum is visible across the PCB ecosystem, with North American shipments posting double-digit growth and a strong book-to-bill ratio-directly translating into higher consumption of conductive, resistive, and insulating printing consumables for high-reliability electronics and point-of-care diagnostics.

China - Overcapacity Control and High-Value Printed Electronics

China remains the world’s largest producer of functional printing consumables, but 2025 marks a decisive pivot from volume expansion to value-added printed photovoltaics, RFID, and graphene inks. The government’s plan to establish a dedicated functional printing industrial park in Wuxi centralizes OLED materials, RFID antennas, and advanced carbon-based inks, strengthening vertical integration across the printed electronics value chain.

Regulatory tightening is reshaping exports. Enhanced oversight by the Ministry of Commerce of the People's Republic of China on graphite and specialty carbon pigment exports-where China controls a majority share-has tightened global supply, increasing strategic importance for graphene and carbon conductive inks. Simultaneously, the Ministry of Industry and Information Technology is subsidizing aqueous and low-VOC functional inks to align with “Dual Carbon” goals, accelerating adoption of water-based dielectric and conductive systems across high-speed industrial printing lines.

India - Semiconductor Mission Spillover and Solar Ink Localization

India’s functional printing consumables market is scaling rapidly on the back of the India Semiconductor Mission (ISM) and Production Linked Incentive (PLI) momentum. With a sanctioned ₹1.6 trillion outlay for high-tech manufacturing, downstream ecosystems are expanding for silver conductive pastes, printed sensors, and membrane switch inks-particularly for domestic solar and electronics manufacturing.

Solar deployment under the PM-Surya Ghar initiative has sharply increased demand for N-type cell silver pastes, encouraging local sourcing to reduce import exposure. Beyond energy, India’s fast-growing consumer electronics sector is generating sustained volumes for functional inks used in touch panels, appliance interfaces, and RFID tagging, positioning the country as a cost-competitive hub for both conductive and dielectric printing consumables.

Japan - Precision Hardware–Consumable Co-Design

Japan dominates the high-precision segment of functional printing consumables through tight integration between print heads, substrates, and specialty chemistries. Innovations from Seiko Epson and Mimaki Engineering in industrial print heads-optimized for solvent-based functional inks-are enabling ultra-fine feature resolution for automotive, medical, and electronics applications.

Material science leadership remains central. Japanese firms are advancing ceramic and hybrid substrates for high-temperature functional printing, critical for 5G/6G RF components and power modules. Under the economic security agenda of the Ministry of Economy, Trade and Industry, printed electronics R&D is being channeled toward silver-nanowire transparent heaters and precision conductive inks for EV and aerospace systems.

Germany - PFAS-Free Chemistry and Industrie 4.0 Diagnostics

Germany leads Europe’s transition to environmentally compliant functional printing consumables, driven by REACH and RoHS3 updates. As a top global exporter of printing inks, German manufacturers such as BASF and Henkel are accelerating PFAS-free conductive and barrier inks, delivering performance gains while meeting stringent chemical regulations.

Industrie 4.0 initiatives are opening new demand corridors. Inkjet-printed microfluidic channels and bio-functional coatings for rapid diagnostics are gaining traction, supported by Horizon Europe funding streams. This convergence of automation, diagnostics, and sustainable chemistry is positioning Germany as Europe’s innovation nucleus for green functional printing systems.

South Korea - MPE 2030 and Smart Healthcare Printing

South Korea’s strategy centers on wearable electronics, biosensors, and thin-film energy storage, supported by the Materials, Parts, and Equipment (MPE) 2030 roadmap. Generous R&D tax credits are accelerating development of bio-inks, stretchable conductive formulations, and printed sensor arrays for smart healthcare and remote monitoring.

Breakthroughs in 3D-printed bio-inks for regenerative medicine-backed by the government’s K-Sensor program-are expanding clinical applications of functional printing. Parallel investments in high-purity substrates are strengthening domestic supply chains for printing consumables used in high-power and medical electronics.

2025 National Strategic Matrix: Functional Printing Consumables

Functional Printing Consumables Matrix

|

Country

|

Primary Consumable Focus

|

Strategic Policy / Event

|

Key Indicator

|

|

United States

|

Conductive pastes, UHP dielectric inks

|

CHIPS Act advanced packaging funding

|

Strong PCB book-to-bill

|

|

China

|

RFID, PV, graphene inks

|

Wuxi functional printing park

|

Majority share in graphite exports

|

|

India

|

Solar silver pastes, printed sensors

|

ISM ₹1.6T package

|

Rapid electronics demand growth

|

|

Japan

|

Precision solvent inks, ceramic substrates

|

METI economic security agenda

|

Dominance in industrial print heads

|

|

Germany

|

PFAS-free, bio-based functional inks

|

REACH / RoHS3 compliance

|

Leading EU ink exporter

|

|

South Korea

|

Bio-inks, wearable sensor materials

|

MPE 2030 roadmap

|

High R&D tax incentives

|

Functional Printing Consumables Market Report Scope

Functional Printing Consumables Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.8 Billion

|

|

Market Size (2035)

|

$22.7 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Consumable Type (Conductive Inks, Dielectric Inks, Semiconductor Inks, Functional Substrates, Protective & Encapsulation Materials), By Technology (Inkjet Printing, Screen Printing, Flexography & Gravure, Aerosol Jet Printing, Additive Manufacturing), By Application (Photovoltaics, Displays & Touchscreens, RFID & Smart Labels, Automotive Electronics, Medical & Wearables, AI & Data Centers), By End-User Industry (Consumer Electronics, Automotive & Transportation, Energy & Utilities, Healthcare & Life Sciences, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, DuPont de Nemours Inc., FUJIFILM Corporation, Henkel AG & Co. KGaA, DIC Corporation, Heraeus Holding GmbH, NovaCentrix Inc., Vorbeck Materials Corp., Inkron Oy, Creative Materials Inc., Appvion Operations Inc., Conductive Compounds Inc., Nagase & Co., Ltd., Toyo Ink SC Holdings Co., Ltd., Avery Dennison Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Functional Printing Consumables Market Segmentation

By Consumable Type

- Conductive Inks

- Dielectric Inks

- Semiconductor Inks

- Functional Substrates

- Protective and Encapsulation Materials

By Technology

- Inkjet Printing

- Screen Printing

- Flexography and Gravure

- Aerosol Jet Printing

- Additive Manufacturing

By Application

- Photovoltaics

- Displays and Touchscreens

- RFID and Smart Labels

- Automotive Electronics

- Medical and Wearables

- Artificial Intelligence and Data Centers

By End-User Industry

- Consumer Electronics

- Automotive and Transportation

- Energy and Utilities

- Healthcare and Life Sciences

- Aerospace and Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Functional Printing Consumables Market

- BASF SE

- DuPont de Nemours, Inc.

- FUJIFILM Corporation

- Henkel AG & Co. KGaA

- DIC Corporation

- Heraeus Holding GmbH

- NovaCentrix, Inc.

- Vorbeck Materials Corp.

- Inkron Oy

- Creative Materials, Inc.

- Appvion Operations, Inc.

- Conductive Compounds, Inc.

- Nagase & Co., Ltd.

- Toyo Ink SC Holdings Co., Ltd.

- Avery Dennison Corporation

*- List not Exhaustive