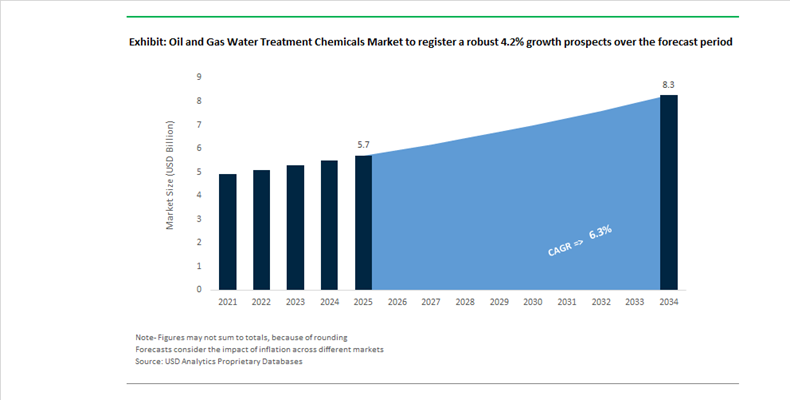

Oil and Gas Water Treatment Chemicals Market Valued at $5.7 Billion in 2025, Projected to Reach $8.3 Billion by 2034 at 4.2% CAGR Amid Water Reuse and Chemical Digitalization

The Oil and Gas Water Treatment Chemicals Market is valued at $5.7 billion in 2025 and is forecast to reach $8.3 billion by 2034, expanding at a CAGR of 4.2%. Market growth is anchored in rising produced water volumes, stricter discharge standards, and the increasing reuse of flowback water in unconventional shale basins. Operators are prioritizing high-performance scale inhibitors, corrosion inhibitors, demulsifiers, flocculants, and biocides to maintain asset integrity and optimize hydrocarbon recovery. Produced water management in basins such as the Permian and Delaware has shifted from disposal-centric strategies to integrated recycling and midstream water handling models, driving demand for advanced chemical treatment packages that operate effectively under high salinity and elevated total dissolved solids conditions.

In July 2025, SLB completed its landmark acquisition of ChampionX Corporation, integrating ChampionX’s production chemicals portfolio into SLB’s digital production and artificial lift platforms. To address antitrust concerns in the U.S. and Norway, divestments and long-term licensing agreements were executed for specific quartz sensor and chemical technologies. This consolidation strengthens SLB’s ability to deploy digital dosing systems alongside water treatment chemistries, enhancing corrosion monitoring and microbial control efficiency. In October 2025, SNF Group signed a definitive agreement to acquire the Oil & Gas division of Syensqo for €135 million, adding more than 700 specialty formulations and reinforcing its dominance in high-molecular-weight water-soluble polymers used in flocculation and enhanced oil recovery.

Service-led consolidation accelerated through 2025. In June 2025, Solenis announced an agreement to acquire NCH Corporation, expanding its footprint in localized industrial water treatment programs. In October 2025, Kemira acquired Water Engineering, Inc., followed by the acquisition of AquaBlue in early 2026, aligning with its objective to double water solutions revenue by 2030. In February 2026, Kemira further strengthened its European position through the acquisition of SIDRA Wasserchemie, enhancing its inorganic coagulant production base. Meanwhile, in October 2025, Western Midstream completed a $1.25 billion acquisition of Aris Water Solutions, forming one of the largest integrated produced water recycling platforms in the Delaware Basin.

Technology innovation is reshaping on-site treatment efficiency and chemical logistics. In July 2024, Kurita America partnered with Solugen to launch the carbon-negative Tower NG cooling water treatment series, replacing traditional phosphonate chemistries with bio-derived alternatives. In May 2025, Ecolab introduced 3D TRASAR™ technology for direct-to-chip cooling, leveraging machine learning to optimize corrosion and scaling control in high-thermal-load systems. In 2025, AMS began full commercial deployment of SafeGuard™ H2O, generating treatment reagents electrolytically on-site, reducing bulk chemical transport costs in remote oilfields. In January 2026, Sumitomo Electric Industries launched a compact POREFLON™ membrane-based oily wastewater treatment system capable of reducing waste volumes by up to 90%, enabling on-site water reuse.

Sustainability and feedstock decarbonization remain central to competitive strategy. In November 2025, BASF and ExxonMobil signed a joint development agreement to scale methane pyrolysis technology, targeting lower-carbon hydrogen and chemical intermediates. This advancement has downstream implications for corrosion inhibitors, biocides, and dispersants used in oil and gas water treatment programs, as producers seek lower-carbon specialty chemical formulations aligned with ESG reporting and Scope 3 emission reduction targets.

Oil and Gas Water Treatment Chemicals Market Trends and Opportunities

Trend: Industrial-Scale Produced Water Recycling Reshapes Shale Water Management Economics

Produced water recycling has shifted from an operational experiment to a structural pillar of shale development economics in the United States. Water scarcity, tightening disposal regulations, and rising seismicity linked to deep-well injection are forcing operators to treat produced water as a reusable asset rather than a liability. This transition is fundamentally expanding demand for oil and gas water treatment chemicals, particularly biocides, scale inhibitors, coagulants, friction reducers, and oxidizing agents designed for high-throughput reuse systems.

The scale of this shift is unprecedented. In 2024 alone, centralized recycling infrastructure in the Permian Basin processed tens of billions of gallons of produced water, with year-on-year growth driven by the buildout of fixed and mobile treatment hubs. The basin generates roughly 12 million barrels of produced water per day, creating sustained chemical demand for iron sulfide control, sulfate reduction, and hydrocarbon removal prior to reuse in hydraulic fracturing. Advanced treatment trains increasingly rely on silicon-carbide ceramic ultrafiltration combined with high-rate chemical oxidation, both of which are chemical-intensive processes requiring consistent dosing and performance reliability.

Economics remain the dominant catalyst. In seismic-sensitive zones, disposal costs can reach several dollars per barrel, while chemically treated reuse costs remain a fraction of that level. This cost differential exceeding 90% has accelerated deployment of mobile chemical treatment units across unconventional plays. As reuse volumes increase, operators are shifting from commodity chemical programs to performance-optimized formulations capable of handling variable water chemistries, high total dissolved solids, and fluctuating microbial loads. As a result, produced water recycling is now a long-term structural demand driver rather than a cyclical activity tied to drilling intensity.

Trend: Mandatory Transition to Environmentally Acceptable Offshore Chemical Programs

Offshore oil and gas operations are undergoing a parallel regulatory-driven transformation, with water treatment chemicals increasingly governed by environmental acceptability rather than cost alone. Global maritime and offshore frameworks are tightening restrictions on persistent, bioaccumulative, and toxic substances, effectively mandating a transition toward certified Environmentally Acceptable Chemicals across production, workover, and water handling operations.

In the North Sea, updated offshore chemical notification frameworks coming into force by late 2025 are accelerating the phase-out of substances listed for priority action. Chemical suppliers are now required to demonstrate rapid biodegradability, low bioaccumulation, and minimal aquatic toxicity, pushing operators toward next-generation scale inhibitors, corrosion inhibitors, and coagulants. In the Gulf of Mexico, revised discharge permits finalized in 2024 impose stricter toxicity thresholds and visible sheen requirements, directly influencing chemical selection for produced water treatment and well intervention fluids.

Technological validation is reinforcing this regulatory momentum. Field data from 2024 and 2025 shows that pairing silicon-carbide membrane systems with low-toxicity coagulants can reduce oil-in-water concentrations to single-digit parts per million, far exceeding compliance requirements. This has repositioned high-performance green chemicals as enablers of extended asset life for aging offshore platforms. As offshore fields mature, regulatory compliance and water treatment efficiency are converging, making environmentally acceptable water treatment chemicals a non-negotiable component of offshore operations.

Opportunity: High-Performance Inhibitors for High-Temperature High-Salinity Carbonate Reservoirs

The development of deeper carbonate reservoirs, particularly in the Middle East, is creating a premium growth opportunity for advanced oil and gas water treatment chemicals engineered for extreme conditions. These High-Temperature High-Salinity reservoirs expose water treatment systems to temperatures above 150°C and salinities approaching 200,000 ppm total dissolved solids, environments where conventional inhibitors rapidly degrade or lose effectiveness.

National water reuse targets and large-scale seawater injection programs are amplifying this demand. Massive investments in water infrastructure across the region are prioritizing advanced antiscalants capable of preventing calcium sulfate and barite deposition under high pressure and temperature. Polymer chemistry is evolving in response, with ATBS-based scale inhibitors increasingly displacing traditional hydrolyzed polyacrylamides due to superior thermal stability and brine tolerance. These formulations maintain viscosity and inhibition performance in conditions where legacy products fail, reducing unplanned shutdowns and extending injection system lifespans.

A secondary opportunity is emerging in bio-based and hybrid polymer systems. Recent research has demonstrated that natural polymers derived from agricultural sources can exhibit shear-thinning behavior and thermal stability suitable for carbonate flooding applications. These bio-polymers align with regional sustainability mandates while offering performance parity in selected reservoir conditions. Together, these developments are creating a high-margin specialty chemical segment focused on extreme reservoir environments rather than volume-driven commoditization.

Opportunity: On-Site, On-Demand Chemical Generation and Smart Dosing Platforms

Operational risk, logistics costs, and safety concerns associated with transporting bulk chemicals are accelerating adoption of On-Site Generation technologies across both offshore and onshore assets. On-site electrochemical generation of oxidants and disinfectants is transforming water treatment strategies by eliminating the need for chlorine gas, concentrated bleach, and other hazardous bulk chemicals.

By 2025, on-site sodium hypochlorite generation systems have gained traction on remote offshore platforms, producing dilute solutions on demand from seawater or brine. These systems significantly reduce spill risk while cutting logistics costs by up to 30%, making them especially attractive for isolated installations with limited storage capacity. In parallel, modular produced water recycling systems capable of treating hundreds of thousands of barrels per day are integrating on-site chemical generation as a core design feature, enabling near-total water reuse in shale basins.

The next phase of this opportunity lies in digital integration. Smart dosing platforms combining IoT sensors with AI-driven optimization are allowing operators to dynamically adjust chemical generation and injection based on real-time microbial activity, scaling indices, and water chemistry fluctuations. Early deployments in the Middle East demonstrate chemical consumption reductions approaching 25% without compromising treatment effectiveness. As water treatment moves toward closed-loop, data-driven control systems, on-site generation coupled with intelligent dosing is positioned as a defining growth avenue within the oil and gas water treatment chemicals market.

Oil and Gas Water Treatment Chemicals Market Share and Segmentation Insights

Scale and Corrosion Inhibitors Lead Chemical Type Consumption in High-TDS Oilfield Water Systems

Scale and corrosion inhibitors accounted for 32.80% of the Oil and Gas Water Treatment Chemicals Market in 2025, making them the largest chemical type segment. Their dominance reflects the critical need to protect pipelines, injection wells, and production infrastructure from scaling and corrosion damage in high-salinity oilfield environments. As unconventional oil and gas production expands, shale and tight oil operators are re-injecting large volumes of produced water for enhanced oil recovery, creating high-temperature, high-TDS scaling conditions that significantly increase inhibitor demand. Advanced phosphonate, polymer-based, and multifunctional inhibitor chemistries are increasingly deployed to stabilize incompatible water mixing, mitigate mineral deposition, and maintain flow assurance across complex oilfield water management systems.

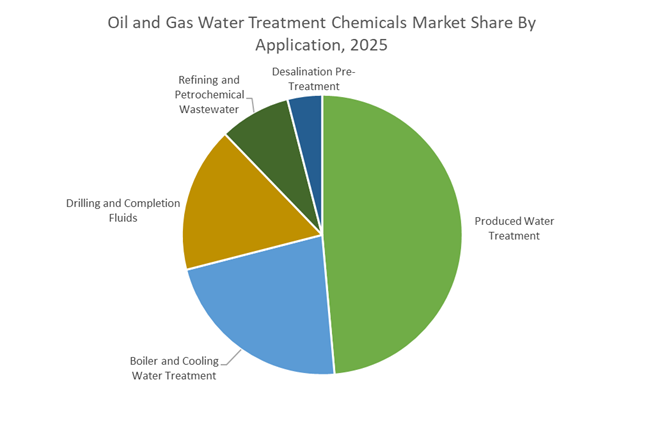

Produced Water Treatment Commands Largest Application Share in Oilfield Water Management

Produced water treatment held 48.60% of the Oil and Gas Water Treatment Chemicals Market by application in 2025, representing the largest consumption segment across upstream and midstream operations. Oil and gas wells typically generate three to seven barrels of produced water per barrel of oil, making water handling and treatment a fundamental operational requirement. Chemical programs including demulsifiers, biocides, corrosion inhibitors, and flocculants are widely used to enable safe disposal or reuse. The accelerating shift toward produced water recycling for hydraulic fracturing and enhanced recovery is increasing demand for high-performance chemical treatment systems capable of managing high-TDS water streams while preventing scaling, microbial contamination, and corrosion in closed-loop reuse infrastructure.

Oil and Gas Water Treatment Chemicals Market Competitive Landscape

The oil and gas water treatment chemicals market in 2026 is driven by ZLD compliance, high-TDS produced water reuse, and decentralized mobile treatment systems. Competitive advantage lies in advanced molecular polishing, biodegradable chemistries, and AI-enabled dosing platforms that optimize water recycling, reduce operational costs, and support circular water management strategies.

Solenis scales circular water treatment platform through NCH integration and sustainability-driven innovation

Solenis has emerged as a global leader following its integration of NCH Corporation, creating a unified platform delivering water treatment chemicals across 160 countries. Its Delaware Global Research Center is accelerating development of advanced molecular polishing chemistries targeting recalcitrant organics and high-TDS water reuse. The ValueAdvantageSM program delivered $349 million in customer value, with 91% of innovations focused on sustainability and circularity. The company is strengthening localized supply chains and pricing strategies to ensure availability of process chemicals in volatile markets. Its Diversey-integrated portfolio enhances hygiene and water treatment synergies. Solenis’ circular water stewardship model positions it at the forefront of ZLD-driven oilfield operations.

Veolia strengthens global leadership with mobile water treatment and large-scale desalination integration

Veolia Water Technologies & Solutions is expanding its dominance through full ownership consolidation and €90 million in cost synergies, enabling seamless delivery of integrated water-energy solutions. Its offshore desalination systems for Brazil’s FPSOs utilize advanced membrane technologies to prevent sulfate scaling and enhance reservoir integrity. Strategic expansion into mobile treatment services under new leadership supports decentralized, wellpad-level chemical deployment. The SATORP project in Saudi Arabia highlights Veolia’s capability in large-scale industrial water recycling and ZLD compliance. Its focus on ecological transformation and water reuse reinforces its leadership in sustainable oilfield water management.

ChampionX integrates digital oilfield technologies with chemical treatment for real-time water quality optimization

ChampionX, backed by SLB, is redefining oilfield water treatment through its “Pore to Point of Sale” strategy, integrating chemical solutions with real-time digital monitoring. Its ESP Digital Ecosystem optimizes dosing of scale inhibitors and corrosion control agents, reducing pump failures and operational downtime. The company’s development of biodegradable friction reducers and low-toxicity biocides supports environmentally compliant hydraulic fracturing. Its collaboration with Gold H2 demonstrates advanced microbial management in subsurface environments. ChampionX’s digital-chemical integration enhances efficiency in produced water reuse and asset integrity management.

SNF dominates polymer-based water treatment with large-scale production and EOR-focused innovation

SNF Group remains the global leader in water-soluble polymers, supported by its acquisition of Syensqo’s oil and gas division, strengthening its position in enhanced oil recovery (EOR) and completion chemicals. Expansion of its Riceboro facility increased ADAM monomer capacity by 80%, ensuring feedstock security for wastewater treatment polymers. With over 1,670 kilotons annual capacity and 1,100+ products, SNF delivers high-performance flocculants and friction reducers for produced water treatment. Its EcoVadis Platinum rating and alignment with UN SDGs highlight strong sustainability performance. SNF’s scale and polymer expertise underpin its dominance in water-intensive oilfield operations.

Ecolab drives intelligent water management with AI-based dosing and refinery optimization technologies

Ecolab, through Nalco Water, leads with its ECOLAB3D™ platform, enabling predictive analytics and automated chemical dosing across complex oilfield systems. Its 3D TRASAR™ technology improves refinery efficiency by managing high-solids variability and reducing total cost of operations. A 10–14% energy surcharge in 2026 reflects rising input costs, while strategic partnerships with CDP enhance water risk benchmarking for operators. The acquisition of Ovivo’s ultrapure water business strengthens its membrane and filtration capabilities for high-precision reuse applications. Ecolab’s data-driven approach positions it as a leader in intelligent, circular water treatment solutions.

United States – Regulatory Reset and Digital Water Management Scale-Up

The United States oil and gas water treatment chemicals market is entering a structurally transformative phase, led by regulatory modernization and capital-backed digital adoption. In March 2025, the U.S. Environmental Protection Agency initiated a comprehensive overhaul of decades-old wastewater discharge regulations, introducing revised Effluent Limitations Guidelines that explicitly enable beneficial reuse of produced water. This policy shift expands the addressable scope of oilfield water treatment chemicals beyond compliance-driven disposal toward reuse applications such as data center cooling, fire suppression systems, and mineral recovery operations. As a result, demand is rising for advanced chemical programs that ensure consistent water quality, including high-performance scale inhibitors, biocides, and selective separation chemistries.

Investment activity underscores this transition. Solenis committed over $42 million through late 2024 and 2025 toward environmental safety infrastructure and AI-driven dosing platforms, reinforcing the move toward precision water chemistry management. Pricing dynamics also reflect tightening supply conditions. Ecolab implemented a 5% trade surcharge in May 2025 to offset raw material inflation and tariff exposure while preserving its domestic manufacturing footprint. Technologically, large-scale adoption of membrane systems and PFAS remediation chemicals accelerated following the EPA’s intensified focus on persistent contaminants. Strategic consolidation further reshaped the landscape, with Ecolab’s acquisition of Barclay Water Management enhancing its digital monitoring and water safety offerings for energy operators. Notably, the EPA’s 2025 Interim Final Rule is projected to significantly reduce long-term compliance costs by extending state-level planning timelines, indirectly freeing capital for advanced water treatment chemical deployment.

China – Standards Enforcement and Zero-Liquid Discharge Acceleration

China’s oil and gas water treatment chemicals market is being propelled by stringent national standards and aggressive wastewater treatment mandates. In August 2025, the State Administration for Market Regulation released GB 15308-2025, part of its latest national standards package, imposing tighter controls on the formulation and performance of industrial foam and aqueous treatment agents. This regulatory clarity is reinforcing demand for high-purity, performance-certified chemicals across upstream and midstream operations. Simultaneously, enforcement of the Water Ten Plan continues to require that a substantial majority of industrial wastewater undergo advanced treatment prior to discharge, making Zero-Liquid Discharge chemical systems a core requirement rather than a niche solution.

Infrastructure investments are aligning with these mandates. BASF expanded its Caojing, Shanghai operations in 2025 while commissioning pilot wastewater treatment capabilities to support production of technical-grade additives tailored for industrial water treatment. Supply chain governance is also evolving, with Chinese chemical producers adopting product traceability platforms such as Circularise to validate recycled polymer inputs used in flocculants and dispersants. Looking ahead, new hazardous substance standards effective June 2026 will further restrict aromatic compounds in oilfield formulations, accelerating reformulation activity. Strategic research partnerships, including joint ventures involving Mitsui Chemicals, are strengthening domestic access to ethylene-based intermediates critical for next-generation high-performance flocculants.

Brazil – Offshore Produced Water Complexity and Bio-Based Transition

Brazil’s oil and gas water treatment chemicals demand is deeply influenced by offshore production dynamics and fuel policy alignment. The nationwide transition to E30 gasoline blends in 2025 increased the moisture load across fuel distribution systems, driving the need for advanced water scavengers, corrosion inhibitors, and phase-stability chemical packages. Offshore, Petrobras continues to prioritize produced water treatment investments in Pre-salt fields, where extreme salinity and pressure conditions necessitate specialized scale inhibitors, oxygen scavengers, and corrosion control chemistries to protect subsea assets.

Regulatory oversight remains a defining factor. Updates by the National Agency of Petroleum during 2024–2025 tightened specifications for produced water reinjection, elevating the importance of microbial control and souring prevention additives. Environmental permitting requirements enforced by IBAMA are simultaneously encouraging the use of bio-based surfactants and biodegradable biocides, particularly in sensitive offshore and Amazon-adjacent regions. Supporting this growth, Brazil is expanding localized blending and storage capacity at the Port of Santos, enabling faster turnaround and customization of oilfield water treatment formulations for offshore operators.

India – Zero-Liquid Discharge Policy and Resource Recovery Integration

India’s oil and gas water treatment chemicals market is being reshaped by national wastewater mandates and indigenous innovation. The 2025–2026 National Water Policy strongly incentivizes Zero-Liquid Discharge adoption across refineries and petrochemical facilities, elevating demand for evaporation chemicals, antiscalants, and high-efficiency coagulants. Technological innovation is emerging from domestic startups, with companies such as Earthy scaling biomimetic membrane systems using aquaporin proteins to improve energy efficiency in produced water desalination for agricultural reuse.

Strategic sourcing initiatives are reinforcing domestic supply resilience. Indian chemical majors are expanding local production of coagulants and flocculants to support the E20 ethanol blending ecosystem, where water treatment plays a critical role in fuel-grade ethanol processing. Government guidelines promoting mineral recovery from oilfield wastewater are creating incremental demand for chelating agents and selective extraction chemistries, particularly for lithium and other critical elements. Additionally, convergence between water treatment chemicals and agrochemical wetting agents is gaining traction in oil-producing rural regions such as Rajasthan, reflecting cross-sector formulation synergies.

Germany – Compliance-Driven Optimization and Advanced Oxidation Uptake

Germany’s oil and gas water treatment chemicals market is characterized by regulatory rigor and advanced process integration. Ongoing compliance adjustments to Regulation (EU) 2025/1490 are prompting manufacturers to streamline portfolios and enhance efficacy documentation for industrial water system biocides. At the same time, circular chemistry initiatives are gaining operational relevance. BASF SE is piloting PFAS removal technologies across its European facilities, with 2025 investments focused on activated carbon reactivation to enable closed-loop water treatment.

Refineries are increasingly adopting advanced oxidation processes such as UV disinfection and electrochemical oxidation to reduce reliance on conventional chemical dosing. Strategic growth priorities are evident at Kemira, which has positioned its Water Solutions division as a core revenue engine, targeting significant expansion in renewable and sustainable water treatment offerings by 2030. Regional infrastructure development is also strengthening supply chains, with final investment approval granted in late 2025 for a large activated carbon reactivation facility in Sweden to serve the broader European oil and gas water treatment network.

Country-Level Strategic Comparison – Oil and Gas Water Treatment Chemicals

Oil and Gas Water Treatment Chemicals Market County Level Snapshot

|

Country

|

Primary Policy Driver

|

Technology Emphasis

|

Strategic Market Direction

|

|

United States

|

Updated ELGs and reuse incentives

|

Digital dosing, PFAS remediation

|

Produced water reuse and cost optimization

|

|

China

|

National standards and Water Ten Plan

|

ZLD chemicals, traceability systems

|

Compliance-led scale expansion

|

|

Brazil

|

Offshore reinjection rules and E30 fuel

|

Scale inhibitors, bio-based surfactants

|

Offshore resilience and sustainability

|

|

India

|

ZLD incentives and resource recovery

|

Biomimetic membranes, chelants

|

Domestic innovation and mineral extraction

|

|

Germany

|

EU biocide regulation and PFAS limits

|

Advanced oxidation, circular carbon

|

Compliance optimization and low-chemical systems

|

Oil and Gas Water Treatment Chemicals Market Report Scope

Oil and Gas Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.7 Billion

|

|

Market Size (2034)

|

$8.3 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Chemical Type (Scale and Corrosion Inhibitors, Biocides and Disinfectants, Flocculants and Coagulants, Demulsifiers and Deoilers, pH Adjusters and Softeners, Oxygen Scavengers, Chelating Agents), By Application (Produced Water Treatment, Boiler and Cooling Water Treatment, Drilling and Completion Fluids, Desalination Pre-Treatment, Refining and Petrochemical Wastewater), By Technology Integration (Chemical Treatment, Hybrid Treatment Systems, Digital Monitoring and Automated Dosing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab, Solenis, BASF, Kemira, Veolia, SUEZ, SLB, Baker Hughes, Halliburton, Kurita Water Industries, DuPont, SNF Floerger, Innospec, Nouryon, Dow

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oil and Gas Water Treatment Chemicals Market Segmentation

By Chemical Type

- Scale and Corrosion Inhibitors

- Biocides and Disinfectants

- Flocculants and Coagulants

- Demulsifiers and Deoilers

- pH Adjusters and Softeners

- Oxygen Scavengers

- Chelating Agents

By Application

- Produced Water Treatment

- Boiler and Cooling Water Treatment

- Drilling and Completion Fluids

- Desalination Pre-Treatment

- Refining and Petrochemical Wastewater

By Technology Integration

- Chemical Treatment

- Hybrid Treatment Systems

- Digital Monitoring and Automated Dosing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oil and Gas Water Treatment Chemicals Industry

- Ecolab

- Solenis

- BASF

- Kemira

- Veolia

- SUEZ

- SLB

- Baker Hughes

- Halliburton

- Kurita Water Industries

- DuPont

- SNF Floerger

- Innospec

- Nouryon

- Dow

*- List not Exhaustive