Market Overview: Biocides and Disinfectants Market Growth Driven by Chlorine-Free Chemistries, Digital Hygiene Systems, and Regulatory Shifts (2025–2034)

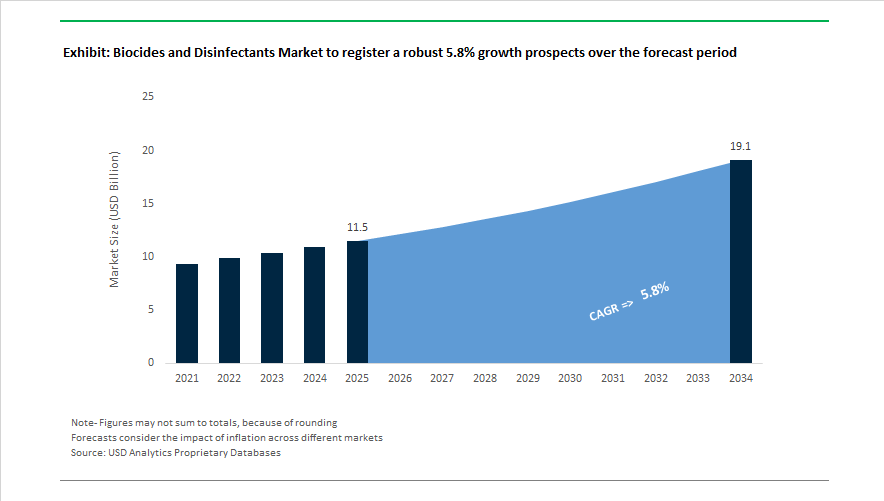

The biocides and disinfectants market is projected to expand from USD 11.5 billion in 2025 to USD 19.1 billion by 2034, reflecting a CAGR of 5.8% supported by rising demand for antimicrobial coatings, water treatment biocides, infection control disinfectants, and food processing sanitation systems. Market dynamics began shifting in 2024 as sustainability and regulatory compliance became central to product development. In April 2024, Solvay partnered with an agricultural organization to develop biodegradable crop protection biocides, emphasizing soil-safe antimicrobial solutions. In August 2024, Ecolab introduced an enzyme-based Clean-in-Place system for protein processors, reducing reliance on harsh disinfectant chemistries while lowering wastewater load. In September 2024, the U.S. EPA approved new chlorine-free biocides from LANXESS, enabling broader adoption of next-generation oxidizing antimicrobial agents.

Product innovation accelerated through 2025 as manufacturers targeted environmental and health performance. In March 2025, LANXESS launched Preventol OX, a chlorine-free oxidizing biocide designed to replace DBNPA in industrial water systems while aligning with tightening environmental restrictions. The same month, LANXESS introduced Klarix XIT, a non-biocidal additive allowing removal of CIT/MIT residues from coatings to deliver biocide-free end products. In October 2024, BASF launched eco-resilient Irgaguard preservative solutions for packaging and coatings, and in January 2026 the company expanded further with near-zero SVOC antimicrobial dispersion technology for interior paints used in schools and healthcare facilities. Digitalization is also influencing dosing and system efficiency. In September 2025, Ecolab released CIP IQ, a data-driven Clean-in-Place monitoring system developed with 4T2 Sensors to optimize disinfectant use in food and beverage processing.

Mergers, acquisitions, and regulatory developments are reshaping competitive positioning. In November 2024, Ecolab acquired Barclay Water Management, strengthening expertise in Legionella control and cooling tower treatment. The company expanded further in August 2025 through a $1.8 billion acquisition of Ovivo’s ultrapure water business, targeting semiconductor and data center liquid cooling systems where precision biocide dosing is critical. In November 2025, LANXESS entered the medical disinfection sector at Medica, promoting Rely+On infection control solutions to address antimicrobial resistance. Regulatory uncertainty remains a factor in Europe. In November 2025, the European Chemicals Agency postponed a final decision on ethanol as an active disinfectant substance, extending transitional conditions for suppliers until discussions resume in February 2026.

Trends and Opportunities Reshaping the Biocides and Disinfectants Market

Market Trend: Phase-Out Pressure on QACs and Volatile Active Ingredients

The Biocides and Disinfectants Market is undergoing a regulatory-driven structural reset. Quaternary Ammonium Compounds (QACs), historically core ingredients across healthcare, household cleaning, and industrial surface disinfection, are now facing global reassessment due to concerns over environmental persistence, antimicrobial resistance linkage, and chronic toxicity.

In September 2025, the European Chemicals Agency (ECHA) Biocidal Products Committee (BPC) rejected approvals for silver-based quaternary ammonium precursors used in disinfectants (PT 2) and preservatives (PT 7 & 9), citing a lack of validated analytical standards for long-term environmental safety. This action effectively freezes new registrations in the EU and forces suppliers to pursue alternative molecules or invest in costly regulatory data packages. The United States is simultaneously tightening oversight: as of August 19, 2025, the U.S. FDA added QACs to its "Select Chemicals Under Review," while California’s DTSC 2024–2025 Priority Product Work Plan formally classifies QAC-containing consumer cleaners as substances of concern. These developments are already influencing procurement in healthcare tenders, where RFPs increasingly require non-QAC or low-residue solutions.

Market Trend: Continuous, Residual and Self-Disinfecting Coatings Gain Long-Term Strategic Importance

End-users are shifting toward solutions that deliver sustained microbial protection, reducing labor cycles and reinforcing perceived hygiene standards in public spaces. This trend is especially strong in public transport systems, smart-city projects, and critical infrastructure where hygiene is now considered a resilience metric.

At CMS Berlin (late 2025), global cleaning and disinfection providers showcased photocatalytic TiO2 and nano-silver aerosol coatings that deliver residual antimicrobial efficacy for hours or days after application. Metro and airport authorities are piloting low-maintenance disinfectant coatings that neutralize pathogenic loads between manual interventions. Complementing this are hybrid antimicrobial coatings that combine anti-graffiti, UV protection, and water-repellent functionality, designed to withstand high-touch abrasion while extending maintenance cycles. For manufacturers, this signals an expansion into engineered film systems with multi-property performance, rather than single-action biocidal liquids.

Market Opportunity: Livestock Disease Control and Mandated Biosecurity Protocols Expand Industrial Demand

Biosecurity is no longer discretionary. The prolonged spread of African Swine Fever (ASF) and the historic 2024–2025 H5N1 detection events in U.S. dairy cattle have elevated biocide demand into a regulated category across animal health and livestock agriculture.

In December 2025, USDA APHIS expanded its cost-sharing program for poultry operations, covering up to 75% of investments required to meet biosecurity standards, including fixed-cycle disinfection checkpoints, tire-washing units, and chemical-resistant facility line separations. The FAO’s November 2025 data further shows ASF across 20 Asia-Pacific countries, triggering national "Emergency Prevention Systems" requiring high-volume, cold-stable disinfectants that continue performing in manure-heavy and mud-rich environments. These conditions favor iodine complexes, peracetic acid (PAA), and stabilized hydrogen peroxide blends engineered to retain efficacy under organic load. Suppliers able to deliver large-container, bulk transport formats with temperature-stable chemistry are best positioned for institutional tenders and long-term supply agreements.

Market Opportunity: HOCl Electrolyzed Water Systems Transform Food Safety and Plant-Level Sanitation

On-site generation of hypochlorous acid (HOCl) represents a major cost and safety breakthrough for food processors, where FSMA and HACCP requirements increasingly mandate both residue-free sanitation and minimized chemical handling risk.

Electrolyzed Water (EW) technology now enables plants to produce HOCl at 50–100 ppm using only water, salt, and electricity, eliminating the storage of hazardous chemicals and reducing transportation emissions. Scientific assessments confirm HOCl delivers up to 99.9% microbial reduction on produce, dairy equipment, and conveyor belts—while being up to 100 times more effective than chlorine bleach at comparable concentrations. Germany, the Netherlands, and the UK are reporting significant reductions in Total Cost of Ownership (TCO), tied to freed warehouse space, lower PPE requirements, and uninterrupted sanitation cycles.

The adoption rate for on-site HOCl systems is projected to expand above 20% annually through 2030, driven by ESG mandates, food safety audits, and retailer-driven sustainability scorecards. Companies that pair on-site systems with IoT validation dashboards and real-time concentration monitoring will gain an upper hand in GFSI-certified food processing markets.

Biocides and Disinfectants Market Share and Segmentation Insights

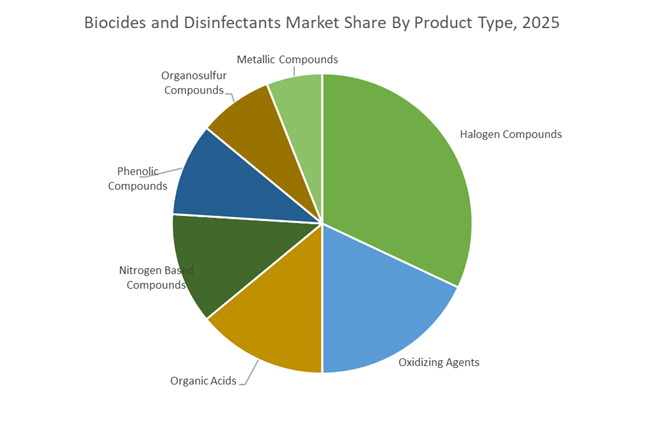

Market Share by Product Type: Halogen Compounds Lead Volume While Oxidizing Agents Capture Sustainability-Driven Growth

Halogen compounds account for 32% of the Biocides and Disinfectants Market in 2025, maintaining leadership through high-volume deployment of chlorine and chlorine dioxide in municipal water treatment and swimming pool sanitation, alongside bromine in industrial cooling towers and iodophors in healthcare and food-contact disinfection. Oxidizing agents, including hydrogen peroxide, peracetic acid, and ozone, represent the fastest-growing category, favored for their environmentally benign breakdown products and expanding use in food processing, healthcare sterilization, and wastewater treatment, with peracetic acid now standard for cold pasteurization. Organic acids such as benzoic, propionic, sorbic, and lactic acids sustain steady demand in food preservation and animal feed. Nitrogen-based compounds, led by benzalkonium chloride, dominate surface disinfectants due to residual antimicrobial activity. Phenolics and organosulfur compounds remain critical for institutional and industrial preservation, while metallic biocides like silver and copper expand selectively in wound care and antimicrobial surfaces.

Market Share by End Use Industry: Water Treatment Dominates as Healthcare and Food Safety Intensify Consumption

Water treatment represents 28% of end-use demand in 2025, driven by municipal drinking water disinfection, industrial cooling systems, and rising wastewater reuse, accelerating adoption of chlorine-based chemistries and advanced oxidation processes. Healthcare follows as the most value-intensive segment, supported by sustained post-pandemic hygiene standards across hospitals and clinics, boosting consumption of surface disinfectants, antiseptics, and medical device sterilants. Food and beverage applications utilize biocides for equipment sanitation, conveyor lubrication, and food-contact surfaces, with peracetic acid and quaternary ammonium compounds widely adopted amid stricter safety regulations and cold-chain expansion. Consumer and residential markets remain high-volume through bleach and disinfectant wipes, reshaped by e-commerce and private labels. Agriculture favors organic acids and hydrogen peroxide for antibiotic-free systems, while paints and coatings, pulp and paper, and oil and gas sustain niche demand through in-can preservation, slime control, and drilling fluid biocides.

Competitive Landscape Analysis of the Biocides and Disinfectants Market

The biocides and disinfectants market in 2026 is being reshaped by digital hygiene platforms, regulatory-driven reformulation, and the accelerating shift toward bio-based and low-toxicity antimicrobial systems. Market leaders are moving beyond commodity actives into integrated contamination control ecosystems that combine chemistry, real-time monitoring, and service models. Competitive advantage now hinges on EU BPR compliance readiness, controlled-release technologies, chlorine-free disinfection, and AI-enabled supply chain optimization. High-growth segments include life sciences contamination control, food and beverage sanitation, clean beauty preservation, and indoor air quality, with sustainability credentials and digital attach rates increasingly determining supplier selection.

Ecolab leads digital-first hygiene systems for life sciences and industry

Ecolab remains the global benchmark in water treatment, hygiene, and infection prevention, operating increasingly as a technology-enabled services provider. Through its One Ecolab initiative, the company is cross-selling integrated hygiene programs to its top global accounts, targeting three billion dollars in incremental revenue via bundled solutions. Following its acquisition of Barclay Water Management, Ecolab is scaling the iChlor Monochloramine System across healthcare and pharmaceutical facilities in India and the Middle East. Its ECOLAB3D platform delivers real-time pest intelligence and water safety analytics for data centers and microelectronics sites. Strategically, Ecolab is prioritizing life sciences contamination control, aiming for twenty% operating margins through digital attach rates.

LANXESS strengthens microbial control leadership through regulatory-first innovation

LANXESS has transformed into a premier microbial control specialist within consumer protection and industrial preservation. In early 2026, the company finalized its Roadmap 2024/26, withdrawing formulations containing more than 0.1% substances of very high concern unless sustainable substitutes exist. Its Preventol and Oxone portfolios dominate animal health and wood preservation, now marketed as climate-neutral via ISCC PLUS mass balance certification. LANXESS differentiates through one of the industry’s strongest internal regulatory teams, enabling faster navigation of the 2026 phase of the EU Biocidal Products Regulation. The company’s 2026 strategy emphasizes resilient growth and cash generation from specialty preservatives for coatings and personal care.

Arxada pioneers controlled-release preservatives and multifunctional additives

Arxada, formerly Lonza Specialty Ingredients, operates as a pure-play microbial control innovator focused on advanced delivery technologies. Its LEAP platform introduced Polyboost multifunctional additives, enabling paint formulators to reduce preservative loading while maintaining viscosity and pH stability. Arxada also leads in TIME micro-encapsulation systems such as Polyphase 862CR, designed to prevent environmental leaching and support EU Eco-Label compliance. In January 2026, its Salto facility in Brazil earned a second Social Seal Certification, reflecting progress toward zero-effluent CCA manufacturing. Through integration with Enviro Tech’s peracetic acid portfolio, Arxada is addressing rising demand for chlorine-free disinfectants in food and beverage processing.

BASF integrates bio-based protection through digital Verbund optimization

BASF addresses the biocides market via its Nutrition & Care and Agricultural Solutions divisions, emphasizing holistic and bio-based protection strategies. In early 2026, BASF acquired AgBiTech to expand its biological insect control capabilities, reducing dependence on conventional chemical actives. Its Tinosan and Irgafos ranges are being unified under the Circle of Care sustainability platform, while Near-Zero SVOC dispersion technology targets healthier indoor environments in schools and hospitals. BASF is also opening a Global Digital Hub in Hyderabad to deploy AI for real-time optimization of biocide and performance materials supply chains, reinforcing its Digitalized Verbund approach to global antimicrobial delivery.

Syensqo pivots from fossil biocides toward biotech-driven hygiene solutions

Syensqo, the specialty spin-off from Solvay, is redefining its biocide strategy around biotechnology and renewable materials. In January 2026, the company divested its Oil & Gas business to SNF Group, completing its exit from fossil-heavy industrial biocides. Syensqo opened a state-of-the-art microbiology laboratory in Lyon to accelerate biodegradable antimicrobial development and eco-toxicology validation. Leveraging its syensqo.ai platform, the company is fast-tracking discovery of next-generation antimicrobial molecules aligned with natural labeling standards. Its portfolio emphasizes biocide-free preservation boosters and bio-based surfactants such as Naternal and Miracare, targeting clean beauty and professional hygiene markets.

Lonza supports biopharma contamination control through CDMO-scale microbial expertise

Although Lonza divested its industrial microbial control operations into Arxada, it remains a critical player in high-end disinfectants used within biopharmaceutical manufacturing. In early 2026, Lonza completed integration of its Vacaville facility, reinforcing its position as a pure-play CDMO while carving out its Capsules & Health Ingredients unit. Lonza’s core strength lies in large-scale microbial tech transfer, where contamination control is mission-critical for complex biologics. The company is constructing a near-zero greenhouse gas facility in Portsmouth to support sustainable cell therapy production. Its Sustainable Design Standard ensures all bioprocessing operations meet stringent 2026 environmental benchmarks.

United States Biocides and Disinfectants Market: Enforcement-Led Market Discipline and Advanced Antimicrobial Platforms

The United States biocides and disinfectants industry is entering a phase of tighter regulatory enforcement combined with targeted innovation in devices and sustainable chemistries. In May 2025, the U.S. Environmental Protection Agency secured a USD 3.07 million settlement against a major national retailer for distributing unregistered pesticides and misbranded disinfectant devices. This action has sent a clear signal that 2026 will see intensified scrutiny of imported hygiene products and online marketplace compliance under FIFRA. Regulatory depth expanded further in December 2025, when the EPA released final guidance integrating Endangered Species Act reviews into antimicrobial pesticide approvals, compelling manufacturers to add ecological mitigation statements and reassess formulation impacts on sensitive habitats.

Innovation is being shaped directly by policy. Under the PRIA 5 mandate, the EPA allocated USD 500,000 for FY2026 to establish the first public health performance standards for antimicrobial air purifiers and UV-C devices, a move that formalizes efficacy benchmarks in a fast-growing device subsegment. On the product side, Corteva expanded its portfolio in 2025 with Viatude™, a bio-based biocide positioned for agricultural and industrial preservation. Infrastructure optimization is also evident as specialty chemical producers such as Albemarle improved bromine extraction efficiency to lower energy intensity per unit, aligning halogenated biocides with lower-carbon procurement criteria. In healthcare, large hospital networks began adopting nanotechnology-based surface coatings in mid-2025 that deliver up to 90-day residual antimicrobial activity, reducing labor-intensive wipe-down cycles and reshaping institutional disinfection protocols.

India Biocides and Disinfectants Market: BioE3 Enablement, Water Security Programs, and Digital Dosing

India’s biocides and disinfectants landscape is being driven by public health infrastructure, sustainability policy, and a fast-maturing industrial ecosystem. Following the August 2024 rollout of the BioE3 Policy, the government has prioritized bio-based chemicals, resulting in the creation of Bio-Enabler Hubs focused on precision fermentation of organic acid-based disinfectants. This has accelerated domestic capability in alternatives to traditional chlorine and aldehyde chemistries, particularly for healthcare and food-contact applications.

Agriculture and water treatment remain powerful demand anchors. At the AgroChem Summit 2025 in New Delhi, provisional registrations were announced for new biological strains, significantly shortening approval timelines for botanical and fungal-based biocides. Under the Jal Jeevan Mission 2025–2026 phase, procurement of chlorine dioxide and sodium hypochlorite scaled up sharply to support rural drinking water projects, with the objective of full coverage in high waterborne-disease zones. Industrial regulation is adding another layer of momentum. In late 2025, the Central Pollution Control Board enforced stricter microbial discharge norms for textile and leather units, driving increased use of oxidizing biocides in effluent treatment. Supporting this shift, industrial automation startups such as Quintrans received government-backed seed funding in December 2025 to deploy AI-driven dosing systems in cooling towers, improving precision and reducing chemical overuse.

Germany Biocides and Disinfectants Market: Regulatory Rebalancing and Low-Carbon Disinfectant Chemistry

Germany represents a compliance-intensive but innovation-friendly market, shaped by consumer safety expectations and EU-level regulatory recalibration. In July 2025, Lonza launched a new range of MIT-free preservatives in Germany, aligning in-can preservation with Blue Angel eco-label criteria and rising consumer intolerance for isothiazolinones. At the policy level, the European Commission convened a high-level dialogue on July 15, 2025 to reassess the EU Biocides Regulation, with a stated objective of simplifying active substance approvals to encourage SME participation without diluting safety standards.

Decarbonization is emerging as a competitive differentiator. Evonik Industries expanded its PERSYNT high-purity hydrogen peroxide production in Essen during 2025, integrating green hydrogen to position disinfectants as low-carbon solutions for pharmaceutical manufacturing. Regulatory uncertainty persists in parallel. The European Chemicals Agency postponed its final opinion on ethanol as an active substance to 2026, creating a temporary holding pattern for sanitizer producers. Meanwhile, German manufacturers are preparing for the May 1, 2026 deadline requiring full compliance with updated CLP hazard classes for endocrine disruptors, prompting reformulation and relabeling across biocidal mixtures.

China Biocides and Disinfectants Market: Consolidation, Precision Dosing, and Export-Oriented Bio-Based Biocides

China’s biocides and disinfectants industry is undergoing structural consolidation combined with rapid digitalization. The 2025 Chemical Consolidation Policies have led to the shutdown of smaller, high-pollution precursor plants, shifting production toward large, vertically integrated players such as SinoHarvest. This has improved consistency and compliance while reducing environmental incidents in upstream synthesis.

Downstream demand patterns are also evolving. With paper production growing at approximately 3.5% annually in 2025, pulp and paper operators are increasingly adopting halogen-free slimicides to prevent corrosion and align with sustainable packaging requirements. In Shandong province, large industrial plants deployed smart sensor systems in late 2025 to enable real-time monitoring and precision dosing of glutaraldehyde, cutting chemical waste by around 30%. Export strategy is shifting toward greener portfolios as well, with Chinese manufacturers scaling botanically derived antimicrobials to meet clean-label expectations from European food packaging converters.

Saudi Arabia Biocides and Disinfectants Market: Energy-Sector Biocides and Desalination-Centric Demand

Saudi Arabia’s biocides and disinfectants market is closely linked to energy infrastructure and water security under Vision 2030. In 2025, Saudi Aramco implemented a new Microbial Corrosion Management standard, mandating the use of high-stability organic sulfur biocides in deep-well drilling and hydrocarbon storage. This has elevated demand for formulations capable of withstanding high temperature and salinity environments.

Water infrastructure is the second major pillar. As part of Vision 2030, the Kingdom accelerated investment in desalination capacity during 2025, favoring in-situ chlorine dioxide generation systems over bulk chemical transport. This approach reduces logistics risk for remote coastal facilities while improving operational safety, positioning advanced on-site disinfection technologies as a strategic growth avenue.

Country-Level Strategic Snapshot: Biocides and Disinfectants Industry

Biocides and Disinfectants Market County Level Snapshot

|

Country / Region

|

Strategic Orientation

|

Key 2025–2026 Developments

|

|

United States

|

Enforcement and device standardization

|

FIFRA settlements, ESA integration, PRIA 5 device standards, bio-based launches

|

|

India

|

Bio-based scale and water security

|

BioE3 hubs, Jal Jeevan Mission demand, stricter CPCB norms, AI dosing startups

|

|

Germany

|

Compliance-led innovation

|

MIT-free preservatives, green hydrogen peroxide, CLP and ethanol regulatory shifts

|

|

China

|

Consolidation and digital precision

|

Plant closures, smart dosing in Shandong, bio-based export push

|

|

Saudi Arabia

|

Energy and desalination-driven demand

|

Aramco corrosion standards, in-situ ClO₂ systems under Vision 2030

|

Biocides and Disinfectants Market Report Scope

Biocides and Disinfectants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.5 Billion

|

|

Market Size (2034)

|

$19.1 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Product Type (Halogen Compounds, Metallic Compounds, Organic Acids, Organosulfur Compounds, Nitrogen Based Compounds, Phenolic Compounds, Oxidizing Agents), By Function (Disinfectants and Sanitizers, Preservatives, Pest Control, Antifouling Agents), By End Use Industry (Water Treatment, Healthcare, Food and Beverage, Pulp and Paper, Paints and Coatings, Oil and Gas, Agriculture, Consumer and Residential)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Ecolab, LANXESS, Lonza Group, Solvay, Veolia, Reckitt, Clorox, Diversey, Evonik Industries, DuPont, Albemarle Corporation, Nouryon, Thor Group, Buckman Laboratories

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biocides and Disinfectants Market Segmentation

By Product Type

- Halogen Compounds

- Metallic Compounds

- Organic Acids

- Organosulfur Compounds

- Nitrogen Based Compounds

- Phenolic Compounds

- Oxidizing Agents

By Function

- Disinfectants and Sanitizers

- Preservatives

- Pest Control

- Antifouling Agents

By End Use Industry

- Water Treatment

- Healthcare

- Food and Beverage

- Pulp and Paper

- Paints and Coatings

- Oil and Gas

- Agriculture

- Consumer and Residential

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Biocides and Disinfectants Industry

- BASF SE

- Ecolab

- LANXESS

- Lonza Group

- Solvay

- Veolia

- Reckitt

- Clorox

- Diversey

- Evonik Industries

- DuPont

- Albemarle Corporation

- Nouryon

- Thor Group

- Buckman Laboratories

*- List not Exhaustive