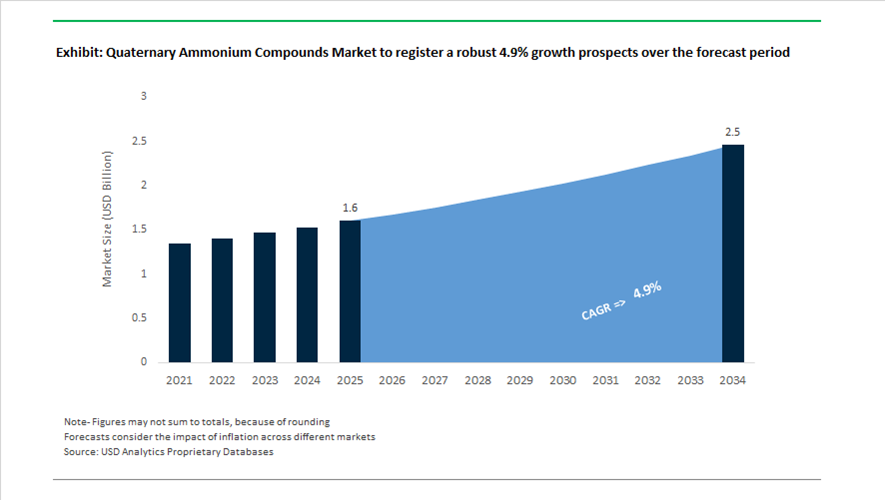

Quaternary Ammonium Compounds Market Valued at $1.6 Billion in 2025, Projected to Reach $2.5 Billion by 2034 at 4.9% CAGR

The global quaternary ammonium compounds (QACs) market is valued at $1.6 billion in 2025 and is projected to reach $2.5 billion by 2034, expanding at a CAGR of 4.9%. Demand remains anchored in benzalkonium chloride, didecyldimethyl ammonium chloride (DDAC), cationic surfactants, disinfectant-grade QAC formulations, antimicrobial preservatives, bioprocessing surfactants, and industrial anti-static agents. Healthcare disinfection, home and personal care, paints and coatings preservation, pharmaceutical excipients, and vaccine manufacturing continue to represent core growth verticals. Regulatory validation, patent expansion, and sustainability-driven feedstock transitions are reshaping the competitive environment.

Regulatory reinforcement and product innovation defined 2024. The U.S. Environmental Protection Agency expanded its List N disinfectants registry during 2024, adding over 500 products approved for use against SARS-CoV-2. QAC-based actives such as DDAC and benzalkonium chloride benefited from this expansion due to their favorable surface compatibility and safety profiles. In 2024, Croda Pharma launched Virodex™, a portfolio of high-purity QAC-based surfactants for viral inactivation and cell lysis in biologics and vaccine production. These materials address stringent purity specifications required in biopharmaceutical manufacturing. The regulatory backdrop and life sciences demand reinforced QAC positioning as essential antimicrobial agents across healthcare and institutional sanitation.

Momentum intensified in 2025 with strategic product launches and IP activity. In January 2025, Croda marked its centenary with a brand evolution strategy targeting Climate, Land, and People Positive operations by 2030, including transition toward bio-based feedstocks in quaternary compound synthesis. The same month, Arxada reported doubling its patent filings in 2024, focusing heavily on cleaner synthesis pathways and sustainable microbial control technologies. In February 2025, Arxada received EPA registration for Quanticare™, a QAC-based sporicidal disinfectant engineered to combat healthcare-acquired infections while offering broader material compatibility than traditional chlorine-based chemistries. In April 2025, Arxada introduced NUGEN® HLD-CD, a high-level disinfectant designed to eliminate microbial presence in “shadow areas” within healthcare facilities. Also in February 2025, Arxada unveiled Polyboost™, leveraging quaternary ammonium chemistry to enhance antimicrobial efficacy and improve physical stability in paints and coatings formulations.

Strategic partnerships and manufacturing expansions extend into 2026. In December 2025, Croda entered a strategic supply partnership with Amino GmbH, operational from January 2026, strengthening pharmaceutical-grade ingredient integration with QAC-based excipient lines. Evonik’s Tailor Made efficiency program, announced in late 2025, reorganized specialty units to prioritize high-margin cationic surfactants for home and personal care markets, improving capital flexibility for 2026. In February 2026, BASF confirmed a new production line at its Mangalore site to supply dispersions and additives for Indian architectural and paper industries where QACs serve as preservatives and anti-static agents. In January 2026, Arxada’s Salto manufacturing facility achieved Social Seal Certification for the second consecutive year, reinforcing sustainability credentials for its QAC-based preservatives across South America.

The quaternary ammonium compounds market is increasingly characterized by EPA-registered disinfectant growth, sporicidal healthcare solutions, high-purity bioprocessing surfactants, antimicrobial coatings additives, bio-based cationic feedstocks, sustainable synthesis IP expansion, and regional production scaling in Asia and Latin America. Healthcare compliance standards, pharmaceutical-grade purity requirements, and institutional hygiene mandates continue to define competitive positioning across the global QAC value chain.

Strategic Trends and Growth Opportunities in the Quaternary Ammonium Compounds (QACs) Market

Strategic Pivot Toward Residual Efficacy and Pathogen-Specific Performance Claims

The quaternary ammonium compounds market has moved decisively beyond pandemic-era volume growth into a phase defined by performance verification and regulatory precision. Institutional buyers in healthcare, commercial facilities, and public infrastructure are no longer prioritizing rapid kill alone. Instead, purchasing decisions are increasingly tied to residual self-sanitizing performance, surface compatibility, and pathogen-specific efficacy that can withstand real-world abrasion and recontamination cycles.

This shift was formalized in September 2025, when United States Environmental Protection Agency issued updated guidance governing antimicrobial products seeking residual efficacy claims. To qualify for a 24-hour residual disinfectant label, formulations must now pass a stringent 12-wear cycle test incorporating alternating wet and dry abrasion, while still delivering a minimum 5-log reduction in qualifying bacteria. This regulatory threshold has fundamentally altered product development economics, favoring suppliers capable of advanced formulation chemistry and robust validation data over low-cost commodity producers.

At the same time, differentiation is increasingly pathogen-specific. Policy reviews published in September 2025 under state-level toxics reduction frameworks reaffirmed that compounds such as didecyl dimethyl ammonium chloride remain indispensable in hospital-grade disinfectants due to their broad-spectrum efficacy at low active concentrations. Manufacturers are responding by launching no-rinse, fragrance-free, and material-safe formulations designed for sensitive environments such as intensive care units and dialysis centers. These targeted products allow healthcare providers to meet infection control protocols while reducing occupational exposure risks, reinforcing QACs’ role as a cornerstone chemistry in professional hygiene markets.

Agricultural Integration as Biostimulant Carriers and Contact Fungicides

A parallel structural trend is unfolding in agriculture, where quaternary ammonium chemistry is expanding beyond traditional livestock and facility sanitation into crop protection and nutrient delivery. In high-value horticulture, QACs are increasingly utilized as cationic surfactants that enhance the adhesion, penetration, and bioavailability of active ingredients, particularly under high-humidity conditions where runoff and dilution reduce conventional efficacy.

In early 2025, Croda International introduced biodegradable quaternary ammonium portfolios designed specifically for food-safe disinfection and agricultural biocides. These products are engineered to comply with the EU Biocidal Products Regulation while offering improved environmental profiles suitable for Integrated Pest Management programs. Their adoption reflects a broader industry push to reconcile efficacy with regulatory and sustainability pressures.

This trend is especially pronounced in Latin America, where industrial filings from late 2024 documented an 18% increase in QAC usage across crop protection programs. In tropical and subtropical production zones, quaternary salts are being deployed as biostimulant carriers that improve nutrient uptake and fungicide performance, supporting yield stability in export-oriented fruit and vegetable supply chains. For chemical suppliers, this represents a meaningful diversification of QAC demand beyond mature hygiene markets.

High-Purity Medical-Grade QACs for Pharmaceutical Sterility and Advanced Therapies

One of the most attractive margin opportunities in the quaternary ammonium compounds market lies in pharmaceutical-grade production. The global expansion of biologics, vaccines, and injectable therapies has created sustained demand for ultra-high-purity quats used as preservatives, excipients, and antimicrobial coatings. Unlike industrial or institutional grades, medical-grade QACs must be manufactured under cGMP conditions with strict controls on endotoxins, trace amines, and residual solvents.

By December 2025, suppliers such as Novo Nordisk Pharmatech and Evonik publicly emphasized the strategic importance of high-purity benzalkonium chloride within sterile drug manufacturing. In response, new investments in amines and quaternization capacity, including advanced refining infrastructure in China, are being directed specifically toward electronic- and medical-grade output. These facilities increasingly rely on high-resolution spectroscopic analytics capable of detecting trace impurities with greater than 99.5% accuracy.

Beyond preservatives, pharmaceutical-grade QACs are gaining traction in cell culture media and antimicrobial medical device coatings. Research published in late 2024 confirmed the effectiveness of specialized QAC-based films in preventing biofilm formation on catheters and implants, a critical requirement in infection-sensitive applications. This validation-ready segment rewards suppliers that can provide comprehensive toxicological dossiers, regulatory support, and long-term supply assurance.

Cationic Surfactants for Enhanced Oil Recovery and Advanced Water Treatment

While healthcare and pharma offer margin expansion, the energy and water treatment sectors continue to represent the largest volume opportunity for quaternary ammonium compounds. In oilfield applications, QACs perform a dual function as biocides controlling sulfate-reducing bacteria and as surfactants that reduce interfacial tension in complex reservoir environments.

Regulatory and operational data indicate that DDAC-based products account for approximately 39% of all registered quaternary ammonium disinfectants, a dominance that extends into energy applications. Their stability in hard water, high salinity, and elevated temperatures makes them the preferred choice for produced water treatment in regions such as the Permian Basin, where microbial souring can severely impair well productivity.

At the same time, tightening environmental discharge standards are reshaping industrial water treatment. Across Asia-Pacific, demand for biodegradable quaternary ammonium biocides used in biofilm control grew by 18% during 2025, driven by stricter wastewater compliance requirements and increased industrial reuse. This creates a clear opportunity for next-generation QACs that combine high antimicrobial performance with improved biodegradability, positioning quats as a critical tool in both resource efficiency and infrastructure resilience.

Quaternary Ammonium Compounds Market Share and Segmentation Insights

Benzalkonium Chloride Leads Disinfectant and Antimicrobial Applications Across Multiple Industries

Benzalkonium chloride accounted for 38.60% of the Quaternary Ammonium Compounds Market by type in 2025, reflecting its widespread use as a broad spectrum antimicrobial agent in disinfectants, personal care products, pharmaceutical formulations, and water treatment chemicals. The compound provides effective bactericidal and virucidal performance while maintaining formulation stability across liquid and surface cleaning products. Its compatibility with non alcohol formulations and residual antimicrobial activity supports extensive use in healthcare and consumer hygiene applications. In 2025, sustained demand for quat based disinfectants continues across healthcare facilities and sanitation products, with benzalkonium chloride widely used in hospital surface disinfectants, antiseptic solutions, and institutional cleaning formulations.

Healthcare and Pharmaceutical Sector Drives Quaternary Ammonium Compound Consumption

Healthcare and pharmaceutical applications represented 34.80% of the Quaternary Ammonium Compounds Market by end user industry in 2025, supported by strong demand for effective antimicrobial agents in hospitals, clinical laboratories, and pharmaceutical manufacturing environments. Quaternary ammonium compounds are widely used for surface disinfection, equipment sanitation, and as preservatives in pharmaceutical and ophthalmic formulations. Infection prevention protocols across healthcare infrastructure continue to support consistent demand for high efficacy disinfectant chemistries. In 2025, expanding infection control standards in hospitals and medical facilities are reinforcing the role of quat based disinfectants, with EPA registered products used to control pathogens including norovirus, Clostridioides difficile, and other healthcare associated infection risks.

Quaternary Ammonium Compounds Market Competitive Landscape

The 2026 quaternary ammonium compounds market is shifting toward biodegradable surfactants, pharmaceutical-grade biocides, and low-VOC formulations. Growth is driven by antimicrobial resistance regulations, green chemistry mandates, and rising demand across agrochemicals, EV batteries, and high-purity healthcare applications.

Lonza sharpens CDMO focus with high-purity quats and strong biopharma growth trajectory

Lonza Group Ltd. is strengthening its leadership in pharmaceutical-grade quaternary ammonium compounds through its transition to a pure-play CDMO model. The company reported CHF 6.5 billion in 2025 sales with 21.7% CER growth and projects 11–12% growth in 2026 alongside EBITDA margins above 32%. Divestment of its Capsules & Health Ingredients business for CHF 2.3 billion enables capital reallocation toward high-margin biologics and small molecule synthesis. Integration of the Vacaville site expands capacity for advanced therapies and high-spec biocides. Sustainability performance includes over 50% reduction in GHG emissions and waste intensity compared to 2018 levels. Focus on cGMP manufacturing supports demand for pharmaceutical-grade quats in regulated markets.

Stepan expands specialty surfactants capacity with alkoxylation focus and industrial cleaning growth

Stepan Company is advancing its quaternary ammonium compounds portfolio through expansion of specialty alkoxylation capabilities and portfolio optimization. The company reported $208.0 million EBITDA in 2025, reflecting 11% year-over-year growth supported by strong industrial cleaning demand. The Pasadena, Texas facility enhances production of high-value surfactants for diverse end-use markets. Divestment of non-core assets streamlines operations and strengthens focus on performance chemistries. Growth in agricultural and oilfield applications highlights increasing use of cationic surfactants in pesticide formulations and enhanced oil recovery. Strategic positioning emphasizes industrial and specialty chemical segments over commodity consumer products.

Evonik drives sustainable quat innovation with bio-based formulations and operational efficiency programs

Evonik Industries AG is focusing on bio-based quaternary ammonium compounds within its Care division while improving operational efficiency. The company reported €1.87 billion adjusted EBITDA in 2025, maintaining stable performance despite lower sales volumes. Its restructuring program targets workforce optimization and faster decision-making across business units. Product development emphasizes low aquatic toxicity quats for personal care and cosmetic applications. Capital allocation strategy supports investment in green transformation projects across key production sites. Financial discipline and sustainability integration support competitiveness in specialty surfactants and high-value chemical markets.

Nouryon advances biodegradable surfactants with renewable energy integration and non-quat alternatives

Nouryon is expanding its presence in the quaternary ammonium compounds market through renewable surfactant technologies and bio-based alternatives. Solar energy integration at its Jurong Island facility reduces Scope 2 emissions in quat and alkoxylation production. The launch of Armocare® Aqua 12 introduces a biodegradable, non-quat conditioning agent for cosmetic applications. Strong position in textile and industrial markets supports demand for antistatic agents and fabric softeners. Expansion into agricultural adjuvants and enhanced oil recovery leverages its expertise in cationic surfactants. Focus on sustainable formulations aligns with tightening environmental regulations and demand for green chemistry solutions.

BASF expands global quat supply through Verbund integration and Asia-Pacific capacity growth

BASF SE is strengthening its quaternary ammonium compounds portfolio through large-scale Verbund integration and regional expansion. Startup of the Zhanjiang site in China increases production capacity for chemical intermediates supporting quat applications. Expansion at the Mangalore site in India supports demand for coatings and construction chemicals in South Asia. The company forecasts 2026 EBITDA between €6.2 billion and €7.0 billion, with growth driven by the Nutrition & Care segment. Decarbonization efforts include renewable electricity adoption to offset emissions from new facilities. Integrated production model supports cost efficiency and supply reliability across global markets.

Novo Nordisk Pharmatech leads high-purity benzalkonium chloride production for pharmaceutical applications

Novo Nordisk Pharmatech A/S is a leading supplier of high-purity benzalkonium chloride (FeF® Quats) for pharmaceutical and bioprocessing applications. Expansion of the Athlone facility with €400 million investment strengthens global manufacturing capacity for high-spec preservatives. cGMP-compliant production ensures low-endotoxin quats for ophthalmic, injectable, and nasal drug formulations. Growth is supported by rising demand from obesity and diabetes therapies within the parent company’s portfolio. Focus on customer-specific bioprocess solutions enhances stability of biologics during large-scale manufacturing. Strong regulatory compliance and purity standards support leadership in pharmaceutical-grade quat applications.

Germany: Semiconductor Purity, AI-Led Chemistry, and Circular Feedstock Leadership

Germany is consolidating its leadership in high-value quaternary ammonium compounds through a combination of semiconductor-grade purity, advanced process intelligence, and circular economy integration. In October 2025, BASF confirmed the construction of a dedicated Electronic Grade Ammonium Hydroxide facility in Ludwigshafen, designed to meet the ultra-low impurity thresholds required for wafer etching and cleaning in advanced-node semiconductor manufacturing. This investment positions Germany at the core of Europe’s semiconductor chemicals value chain, particularly as chipmakers tighten specifications for nitrogen-based quaternary derivatives. Parallel to capacity expansion, BASF’s December 2025 deployment of an AI Reactor across German research hubs marks a structural shift in quaternary formulation development, enabling autonomous experiment planning to optimize yield, safety, and impurity control in complex amine systems.

Sustainability and energy transition are increasingly embedded in German quaternary production economics. The November 2025 joint development agreement between BASF and ExxonMobil to scale methane pyrolysis introduces low-emission hydrogen as a cleaner precursor for nitrogen chemistry, materially reducing lifecycle emissions of quaternary ammonium synthesis. The adoption of X3D catalyst shaping in late 2025 further improved reactor throughput and energy efficiency by more than 10%, reinforcing Germany’s process-intensity advantage. At the same time, ISCC PLUS certification achieved by German sites producing fabric softeners and surfactants enables mass-balance use of bio-circular feedstocks, aligning quaternary portfolios with the EU Chemicals Strategy for Sustainability under the “Winning Ways” framework.

China: Export-Oriented Reform, AI-Enabled Scale, and Environmental Cost Rebalancing

China’s quaternary ammonium compounds industry is undergoing a decisive reorientation toward export efficiency and accelerated time-to-market. In November 2025, the Ministry of Agriculture and Rural Affairs released draft reforms to streamline registration of export-only pesticides, materially lowering regulatory friction for quaternary-based herbicides incorporating novel active ingredients not yet approved domestically. These reforms, coupled with reduced toxicological data requirements for export-bound technical materials, have shortened commercialization cycles for Chinese manufacturers targeting Latin America, Africa, and Southeast Asia. Capacity expansion continues in parallel, with BASF commissioning a 500-metric-ton loopamid facility at its Caojing site in early 2025, supporting downstream polyamide and quaternary intermediate supply.

Operational efficiency is increasingly driven by digitalization and environmental compliance. Major chemical clusters in Shandong and Jiangsu integrated AI-based real-time monitoring in 2025 to optimize benzalkonium chloride synthesis, reducing byproduct formation and improving yield stability. However, sustainability compliance has raised the cost floor. New Zero Liquid Discharge mandates enforced in the Pearl River Delta since late 2025 require full wastewater recovery at specialty chemical plants. While this increases operating expenditure, it materially improves the environmental acceptability of Chinese quaternary ammonium compounds in export markets where ESG scrutiny is intensifying.

United States: Regulatory Spillover, Alkoxylation Capacity, and Distribution Consolidation

The U.S. quaternary ammonium compounds market is being reshaped by environmental regulation spillover and strategic capacity investments. The anticipated April 2026 finalization by the Environmental Protection Agency to classify additional PFAS compounds as hazardous under RCRA has triggered a surge in R&D focused on quaternary-based performance substitutes for fluorinated surfactants. This regulatory momentum is accelerating reformulation across coatings, industrial cleaners, and specialty applications where quaternary ammonium compounds can replicate wetting and antimicrobial performance without PFAS exposure.

On the supply side, Stepan Company strengthened domestic availability of quaternary and non-ionic surfactants through the mid-2025 start-up of its Pasadena, Texas alkoxylation facility, targeting oilfield, agricultural, and industrial cleaning segments. Regulatory transparency is also increasing. Updated Toxics Release Inventory rules effective January 2026 impose immediate disclosure requirements for newly listed chemicals, raising compliance expectations across the quaternary value chain. Distribution efficiency has become a competitive lever, illustrated by Evonik entering an exclusive U.S. distribution agreement with Sea-Land Chemical Company in March 2025 to streamline Midwest access to high-performance quaternary disinfectants and cleaning solutions. Industry-wide investments in leak detection and repair systems following EPA enforcement settlements in 2024–2025 further reflect a structural tightening of operational standards.

India: API Localization, Import Substitution, and Export-Oriented Scale-Up

India’s quaternary ammonium compounds landscape is being structurally transformed by pharmaceutical localization and policy-backed capacity build-out. Under the Production Linked Incentive Scheme for Bulk Drugs, the government reported in December 2025 that domestic manufacturing had been established for 26 critical KSMs and APIs, including several quaternary intermediates used as catalysts and phase-transfer agents in respiratory and chronic therapies. This localization drive translated into tangible trade outcomes, with import substitution worth ₹3,591 crore achieved by September 2025, materially reducing exposure to external supply disruptions.

Infrastructure development is reinforcing this shift. By October 2025, approximately 30% of construction work at designated Bulk Drug Parks in Andhra Pradesh, Gujarat, and Himachal Pradesh was completed, creating integrated zones for high-volume quaternary synthesis with centralized effluent treatment and utilities. The structural payoff is already visible in trade balances. The Ministry of Commerce and Industry reported in August 2025 that India transitioned into a net exporter of bulk drugs, reaching ₹2,280 crore compared with net importer status in FY2022. This transition signals a broader realignment of global sourcing for quaternary ammonium derivatives toward India, particularly for regulated pharmaceutical and specialty chemical applications.

Comparative Snapshot: Quaternary Ammonium Compounds by Country

Quaternary Ammonium Compounds Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Structural Industry Shift

|

|

Germany

|

Semiconductor-grade purity and AI-led synthesis

|

Ultra-pure quaternaries, circular feedstocks, energy-efficient reactors

|

|

China

|

Export acceleration and digital manufacturing

|

Faster registrations, AI optimization, ZLD-driven cost rebalancing

|

|

United States

|

Regulatory-driven reformulation and capacity

|

PFAS substitution, alkoxylation expansion, tighter compliance

|

|

India

|

API self-reliance and trade balance correction

|

PLI-led localization, bulk drug parks, net export transition

|

Quaternary Ammonium Compounds Market Report Scope

Quaternary Ammonium Compounds Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$2.5 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Type (Benzalkonium Chloride, Didecyl Dimethyl Ammonium Chloride, Alkyl Trimethyl Ammonium Chloride, Dialkyl Dimethyl Ammonium Chloride, Specialty Quaternary Ammonium Compounds), By Application (Disinfectants & Sanitizers, Surfactants & Emulsifiers, Fabric Softeners, Wood Preservatives, Personal Care, Water Treatment), By End-User Industry (Healthcare & Pharmaceutical, Consumer Goods, Agriculture & Agrochemicals, Oil & Gas, Textiles & Leather, Food & Beverage Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Stepan Company, Evonik Industries AG, Kao Corporation, Lonza Group AG, Global Amines Company Pte. Ltd., SACHEM Inc., Croda International Plc, Dow Chemical Company, Novo Nordisk Pharmatech A/S, Ecolab Inc., Jubilant Ingrevia Limited, Shandong Luba Chemical Co. Ltd., Thor Group Limited, Dishman Carbogen Amcis Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Quaternary Ammonium Compounds Market Segmentation

By Type

- Benzalkonium Chloride

- Didecyl Dimethyl Ammonium Chloride

- Alkyl Trimethyl Ammonium Chloride

- Dialkyl Dimethyl Ammonium Chloride

- Specialty Quaternary Ammonium Compounds

By Application

- Disinfectants & Sanitizers

- Surfactants & Emulsifiers

- Fabric Softeners

- Wood Preservatives

- Personal Care

- Water Treatment

By End-User Industry

- Healthcare & Pharmaceutical

- Consumer Goods

- Agriculture & Agrochemicals

- Oil & Gas

- Textiles & Leather

- Food & Beverage Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Quaternary Ammonium Compounds Industry

- BASF SE

- Stepan Company

- Evonik Industries AG

- Kao Corporation

- Lonza Group AG

- Global Amines Company Pte. Ltd.

- SACHEM Inc.

- Croda International Plc

- Dow Chemical Company

- Novo Nordisk Pharmatech A/S

- Ecolab Inc.

- Jubilant Ingrevia Limited

- Shandong Luba Chemical Co. Ltd.

- Thor Group Limited

- Dishman Carbogen Amcis Limited

*- List not Exhaustive