Market Overview: Bio-Based Feedstocks, U.S. Capacity Expansion, and PFAS-Free Transition Accelerate Cationic Surfactants Market

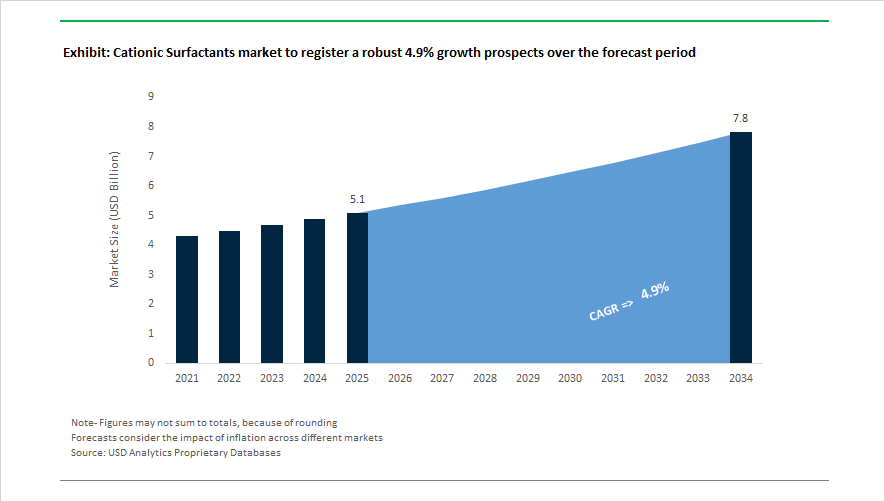

The Cationic Surfactants Market is projected to rise from USD 5.1 billion in 2025 to USD 7.8 billion by 2034, registering a CAGR of 4.9% , supported by expanding demand for fabric softeners, hair conditioners, disinfectants, and industrial antistatic agents. Market dynamics shifted in May 2024 when Clariant completed the acquisition of Huntsman’s specialty surfactants business, strengthening its portfolio of cationic intermediates and reinforcing its position in global care chemicals. In March 2024, Dow and DuPont initiated collaboration on advanced surfactant technologies for agrochemicals, introducing cationic wetting agents that enhance adhesion and bio-efficacy in sustainable crop protection formulations.

Feedstock strategy and regional capacity additions became central through 2025. In March 2025, Kao secured an agreement to source NALO bio-based fatty alcohols, reducing dependence on palm-derived raw materials in cationic synthesis. This sustainability drive continued in August 2025, when Kao opened a world-scale tertiary amine plant in the United States, strengthening North American supply for quaternary ammonium surfactants used in home care disinfectants. Lonza received EU regulatory approval in February 2025 for a new Antwerp site dedicated to high-purity surfactants and biocidal actives. BASF advanced complementary blending strategies during 2025 to 2026, expanding Alkyl Polyglucoside production in Thailand and preparing its Cincinnati facility for start-up in 2026, enabling hybrid formulations that combine mild non-ionic APGs with conditioning cationic systems.

Product innovation and environmental compliance dominated late 2025 and early 2026. Croda introduced Natrineo CR8 in October 2025, a naturally derived cationic emulsifier aimed at replacing traditional quaternary ammonium compounds in hair care. The same month Croda launched NeutraFresh BD, a biodegradable odor-neutralizing cationic ingredient for fabric care. Nouryon expanded textile chemical distribution with IMCD in December 2025, strengthening its presence in sustainable fashion processing. In January 2026, Clariant appointed new leadership for its Care Chemicals unit, reinforcing innovation focus after integration of its expanded surfactant portfolio. Solvay confirmed that by 2026 nearly all fluoropolymer production will shift to non-fluorosurfactant processes, accelerating PFAS-free chemistry adoption across surfactant manufacturing.

Trends and Opportunities Reshaping the Cationic Surfactants Market

Reformulation Toward ADBAC and DDAC as Regulatory Scrutiny on BAC Intensifies

The strongest market-defining development is the accelerated shift away from Benzalkonium Chloride (BAC) toward alternative quats such as ADBAC and DDAC. This is not a cosmetic trend but a protective industry response to regulatory ambiguity and toxicology surveillance.

In the U.S., the FDA has continued its review of antiseptic actives through 2024–2025, leaving BAC in a deferred regulatory category. Leading antimicrobial brands are therefore pre-emptively reformulating to ensure uninterrupted registrations. Benchmark hand rubs historically leaned on BAC 0.13 percent, but next-generation healthcare and industrial formulations now combine DDAC for broader virucidal spectra and improved lifecycle risk profiles.

In Europe, the regulatory obligation is more direct. Commission Regulation (EU) 2025/1090 formally restricts specific nitrogen-containing compounds under REACH Annex XVII, requiring tighter stewardship, traceability, and dose-control data. States in the U.S. are mirroring this stance: Massachusetts proposed DDAC and ADBAC for addition to its 2025 TURA hazardous list, pressuring suppliers to document exposure pathways and invest in upstream compliance systems. The result is a major procurement shift as buyers favor suppliers with REACH-compliant dossiers and ESG-aligned formulations.

Esterquats and Sustainable Cationics Accelerate as Home Care Brands Target Biodegradability

Sustainability has moved beyond a marketing narrative toward a financial and regulatory obligation. Esterquats, engineered with ester bonds that degrade faster in wastewater environments, are now defining new long-term procurement standards in home and fabric care chemicals.

Evonik’s disclosure that 45% of total revenue in 2025 stems from “Next Generation Solutions” signals a scale-level market pivot. BASF and Evonik’s joint mass-balance agreement on biomass ammonia in 2024 provides a 65% documented Product Carbon Footprint (PCF) reduction. These advancements align with ISCC PLUS-certified supply chains demanded by major FMCG buyers, especially top-five global fabric care brands transitioning toward “biodegradable surfactant-only” SKUs by 2030.

Ionizable Cationic Lipids – A High-Margin Transformation Within mRNA-LNP Therapeutics

Pharmaceutical adoption represents the most margin-lucrative growth frontier. Cationic surfactants, particularly ionizable lipids, are core to lipid nanoparticle (LNP) drug delivery platforms enabling mRNA vaccines, gene therapies, and precision oncology drugs.

A July 2025 clinical study demonstrated that substituting standard ionizable lipids with 10–25% DODAP or DOTAP increased localized mRNA expression and reduced liver off-target expression. This is highly material: reduced hepatic expression improves safety outcomes and broadens patient eligibility for chronic mRNA therapies.

Corporate strategy is converging: VION Biosciences’ 2024 acquisition of Echelon Biosciences indicates a shift toward vertical integration, where pharmaceutical developers seek guaranteed cGMP-grade lipid supply. With the LNP manufacturing market expected to surpass USD 2.5 billion by 2034, producers of high-purity ionizable cationics will control premium pricing power and multi-year supply agreements.

Cationic Demulsifiers – Critical for Heavy Oil, Pyrolysis Oil and Renewable Refining

The transition to heavier crude slates and the rise of plastic-to-oil pyrolysis are reshaping refinery chemistry requirements. These feedstocks form stubborn water-in-oil emulsions that disrupt desalting systems and cause corrosion events in crude units and FCC trains.

Baker Hughes expanded its XERIC heavy-oil demulsifier program in 2024 to address these problems. Technical trials in October 2025 demonstrated that specialized cationic demulsifiers using alkoxylated resin blends delivered 92.89% water removal efficiency at only 27 ppm dosing. This is strategically relevant for operators integrating renewable feedstocks, where operational disruptions cascade into catalyst losses, environmental fines, and unplanned shutdowns.

Cationic Surfactants Market Share and Segmentation Insights

Market Share by Type: Quaternary Ammonium Salts Dominate as Esterquats Post Fastest Growth

Quaternary ammonium salts command 58% of cationic surfactant demand in 2025, driven by broad biocidal efficacy and versatility across fabric softeners, disinfectants, antistatics, and emulsifiers, sustaining leadership in home care and institutional cleaning. Esterquats are the second-largest and fastest-growing class, benefiting from improved biodegradability and a favorable environmental profile that has displaced legacy dialkyldimethylammonium systems in rinse-cycle conditioners and fabric softeners. Amine salts maintain a stable industrial footprint in corrosion inhibition, flotation, and pigment dispersion. Cationic imidazolines occupy a premium niche in hair conditioning and metalworking fluids, while cationic biosurfactants remain emerging due to higher production costs, despite momentum from clean-label personal care and corporate sustainability targets.

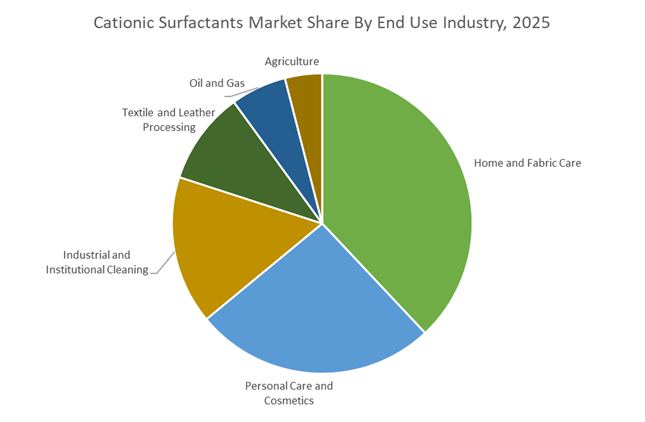

Market Share by End Use Industry: Fabric Care Leads as Personal Care and Hygiene Sustain Structural Demand

Home and fabric care represents 38% of market consumption in 2025, led by esterquat-based softeners and antistatic formulations, with premiumization via concentrated products, cold-wash compatibility, and biodegradable sourcing reshaping brand strategies. Personal care and cosmetics is the second-largest and fastest-growing segment, relying on cationic conditioners for detangling and softness in hair care, alongside cationic emulsifiers in skin care, supported by sulfate-free and clean beauty reformulation. Industrial and institutional cleaning remains a high-volume channel for quats in disinfectants and hard-surface cleaners, sustained by post-pandemic hygiene baselines across healthcare and food service. Textile and leather processing continues a mature trajectory amid tighter effluent standards, while oil and gas and agriculture persist as niche, cycle-driven outlets for corrosion inhibition, biocidal control, and spray adjuvancy.

Competitive Landscape of the Cationic Surfactants Market

The global cationic surfactants market in 2026 is being reshaped by rising demand for biodegradable quats, esterquats, antimicrobial surfactants, fabric softeners, hair conditioning agents, and agricultural adjuvants. Competition is centered on bio-based cationics, silicone-free conditioning systems, smart surface technologies, and ultra-concentrated low-water detergent formulations. Leading manufacturers are differentiating through vertical integration, renewable electricity adoption, RSPO-compliant supply chains, and advanced molecular engineering. Strong growth across personal care, home care, institutional cleaning, oilfield chemicals, and crop protection is accelerating innovation in eco-certified cationic surfactants, positioning sustainability, performance, and traceability as core purchasing criteria for global formulators.

High-purity salon-grade cationic surfactants powered by Kao Corporation

Kao enters 2026 as the benchmark supplier of high-purity cationic surfactants for premium hair care, led by its QUARTAMIN® series engineered for anti-static performance and superior slip in silicone-free conditioners. Under its FY2026 “K27” Mid-term Plan, Kao is rolling out environment-adaptive cationics optimized for ultra-concentrated, low-water liquid detergents. Its core strength lies in precision selective cleansing, enabling targeted deposition on damaged hair fibers without buildup, a critical requirement for professional salons. With full vertical integration across tertiary amines, surfactants, and finished consumer brands, Kao rapidly prototypes next-generation molecules, reinforcing leadership in conditioning agents, fabric care surfactants, and sustainable home care chemistry.

Esterquat and biosurfactant leadership from Evonik Industries AG

Evonik dominates the 2026 shift toward esterquats and biosolutions, replacing traditional petrochemical quats with highly biodegradable alternatives such as REWOQUAT®. Its award-winning TEGO® Wet 580 Terra underscores Evonik’s role in bio-based cationic surfactants for smart surfaces and advanced cleaning. Strategic investments in Japan and Singapore support growing demand for cationic-stabilized dispersions in electronics and battery coatings. Evonik has transitioned surfactant production to renewable electricity, meeting zero-carbon ingredient requirements from global brands. With strong traction in home care, antimicrobial applications, and anti-static technologies, Evonik positions itself as a sustainability-first partner across fabric softeners, disinfectants, and next-generation cleaning systems.

Local-for-local personal care cationics driven by Clariant AG

Clariant is accelerating growth in 2026 through localized manufacturing and specialty cationic surfactants for Asia’s booming clean beauty sector. Its CHF 80 million Daya Bay expansion strengthens output of ethylene oxide derivatives and Genamin® cationics, enabling energy-saving cold-process cosmetic formulations. Following the integration of Lucas Meyer Cosmetics, Clariant now delivers active surfactant systems, where cationic carriers also transport skin-brightening peptides and anti-aging actives. A new Care Chemicals leadership team signals deeper focus on premium conditioners, emulsifiers, and multifunctional bio-actives. Clariant’s strategy combines performance surfactants, cosmetic actives, and regional supply resilience for fast-growing personal care markets.

Antimicrobial and industrial cationic surfactants from Nouryon

Nouryon leads the 2026 industrial segment with antimicrobial cationics and asphalt emulsifiers, anchored by its Arquad® series used in hospitals and food processing to eliminate 99.9% of resistant microbes. The company recently launched 100% bio-based, biodegradable surfactants aimed at removing persistent quats from wastewater streams. Expansion of its Brazil innovation hub supports customized cationic asphalt systems for regional infrastructure. Nouryon’s co-creation model, powered by 15 global innovation centers, enables rapid localization of formulations for laundry, agriculture, oilfield chemicals, and institutional cleaning, reinforcing its position in high-performance disinfectants and industrial surfactant platforms.

Bio-renewable prestige cationics engineered by Croda International Plc

Croda operates as the 2026 boutique powerhouse in bio-renewable cationic surfactants for prestige beauty and healthcare. Its ICIS award-winning Star Polymer technology delivers high emulsion stability without greasy residue, while the ECO Range provides the industry’s broadest portfolio of 100% bio-based cationics. Croda has transitioned its Atlas Point facility to naturally derived ethylene oxide, achieving one of North America’s lowest carbon footprints for ethoxylated surfactants. With strong penetration in medical skin grafts, green hair repair serums, and eco-certified cosmetics, Croda excels at matching petrochemical performance with plant-derived conditioning agents.

High-volume fabric care and agri-adjuvants from Stepan Company

Stepan anchors the North American market with high-capacity cationic surfactants for fabric softeners and agricultural delivery systems. Its Pasadena alkoxylation plant significantly boosts 2026 output of cationic emulsifiers for pesticide applications. The AMMONYX® and ACCOSOFT® brands dominate retail softener sheets and liquid concentrates, supported by Stepan’s automated One-Drum pre-blended systems that simplify formulation for regional producers. Strategically, Stepan is prioritizing cationic agricultural adjuvants that improve herbicide adhesion on waxy leaves, reducing spray drift and runoff. This positions Stepan at the intersection of fabric care, crop protection, and regulatory-driven efficiency.

United States: Alkoxylation Capacity Expansion, Safer Choice Tightening, and Bio-Propellant Integration Strengthen Cationic Surfactant Leadership

The United States cationic surfactants market is expanding on the back of infrastructure upgrades, regulatory recalibration, and sustainable formulation innovation. In mid-2025, Stepan Company reached a key milestone at its Pasadena, Texas facility with the commissioning of a state-of-the-art alkoxylation plant. This expansion significantly enhances domestic production capacity for cationic surfactant blends, including quaternary ammonium compounds (quats) and specialty amine derivatives used in fabric softeners, disinfectants, oilfield chemicals, and hair conditioners.

Regulatory frameworks are tightening performance thresholds. In July 2025, the U.S. Environmental Protection Agency updated Safer Choice Criteria for Surfactants, requiring faster biodegradation (mineralization to CO₂ and water within 10 days) for cationic surfactants with elevated aquatic toxicity to retain eco-label status. In late 2024, Stepan integrated assets from PerformanX Specialty Chemicals, strengthening its intellectual property portfolio for high-purity cationic surfactants tailored to specialty oilfield and industrial applications. In April 2025, Nouryon introduced Demeon® ReNu100, a 100% bio-based propellant designed to synergize with cationic hair-styling formulations in aerosol systems. Evonik streamlined Midwest and East Coast distribution through an exclusive agreement with Sea-Land Chemical in March 2025, improving access to sustainable cleaning formulations. Meanwhile, proposed Significant New Use Rules (SNURs) in November 2025 mandate 90-day advance notification for new cationic chemical substances, reinforcing pre-market oversight under TSCA.

China: Shanghai Innovation Scaling, Eco-Protection Mandates, and Semiconductor-Grade Cationic Applications

China’s cationic surfactants industry is defined by rapid localization of R&D, eco-regulatory enforcement, and advanced electronics integration. In November 2025, Nouryon inaugurated a major Innovation Center in Shanghai to accelerate development of localized cationic surfactants for home care, fabric softeners, and personal care formulations tailored to Chinese consumer preferences.

Capacity expansions in polymer specialties have strengthened upstream integration, with metal alkyl and organic peroxide innovation centers supporting synthesis of cationic-active polymers for plastics processing. The BASF–Hannong Chemicals joint venture entered full commercial production in 2025, scaling specialty surfactant output for APAC textile and electronics sectors. Under China’s Ecological and Environmental Protection Plan (2024–2025), stricter controls on non-biodegradable surfactants are driving adoption of ester-based cationic softening agents in the Yangtze River Delta. Semiconductor-grade chemical suppliers reported a 12% rise in high-purity cationic surfactant consumption in 2025 for chemical mechanical planarization (CMP) slurries and photoresist stripping. In parallel, China’s $53+ billion agrochemical industry has integrated advanced cationic adjuvants to improve rain-fastness and leaf adhesion in systemic fungicides.

Germany: Industry Superforce Re-Alignment, Bio-Surfactant Scaling, and Digital Product Passport Leadership

Germany’s cationic surfactants market is pivoting toward high-margin, sustainable biosolutions aligned with EU regulatory leadership. In May 2025, Evonik Industries announced its “Industry Superforce” strategy, outlining plans to divest Performance Intermediates by 2027 and intensify focus on sustainable cationic biosurfactants. Evonik’s rhamnolipid production facility in Slovakia, serving the German market, reached full capacity in 2025, enabling bio-based alternatives for premium personal care formulations.

At the 2025 SEPAWA Congress, German manufacturers introduced sulfate-free, biodegradable fabric softener surfactants delivering 20% higher conditioning efficiency versus traditional quaternary ammonium compounds. Chemical clusters implemented AI-driven Advanced Process Control (APC) systems in late 2025, achieving average IRRs of 25% on process redesign for fatty amine and cationic amine production. Germany continues to spearhead EU REACH 2025 reforms, including the Digital Product Passport requirement mandating granular carbon footprint disclosure for raw fatty amine feedstocks, reinforcing transparency across the cationic surfactant value chain.

India: Alpha-Olefin Feedstock Growth, DGFT Restrictions, and Urban Hygiene Demand Propel Cationic Consumption

India’s cationic surfactants market is experiencing accelerated growth due to refining feedstock integration, regulatory import controls, and urban hygiene expansion. Nouryon India secured 2025 Great Place to Work Certification, reflecting the rapid institutionalization of global chemical R&D hubs in Mumbai and Bengaluru. The $2.09 billion Gujarat refinery expansion has increased alpha-olefin production, a critical precursor for domestic synthesis of cationic surfactants and quats.

In December 2025, the Directorate General of Foreign Trade issued Notification No. 50/2025-26, placing restricted status on selected chemical intermediates through November 2026 to promote local specialty surfactant manufacturing under the “Make in India” initiative. With over 52% urban population penetration by early 2025, demand for cationic disinfectants, antimicrobial laundry additives, and institutional cleaning chemicals has surged. India’s textile sector—one of the world’s largest—remains a leading consumer of cationic dye-fixing agents, with 2025 witnessing adoption of cold-process surfactants that cut energy usage in dye houses by 15% .

The Netherlands: ISCC PLUS Hair-Care Innovation, Lignin-to-Surfactant Pathways, and Green Chelate Integration

The Netherlands continues to lead in sustainable cationic surfactant innovation, particularly in hair care and detergent co-formulations. In April 2025, Nouryon launched Armocare® Aqua 12 at in-cosmetics Global in Amsterdam, an ISCC PLUS-certified, readily biodegradable cationic surfactant positioned as a non-quat alternative for premium hair care formulations.

The Herkenbosch manufacturing site achieved ISCC PLUS certification in January 2025, enabling production of green chelating agents frequently co-formulated with cationic surfactants in premium detergents. The development of Structure® M3 co-surfactant in late 2024 allowed formulators to substitute petrochemical surfactants with mild, plant-derived alternatives in salon-grade products. Dutch circular economy initiatives have advanced the world’s first pilot-scale lignin-to-surfactant pathway, providing renewable aromatic precursors for next-generation cationic compounds aligned with Circular Carbon Economy goals.

Brazil: South American Innovation Hub, Pulp & Paper Integration, and Bio-Based Green Quats Export Growth

Brazil’s cationic surfactants market is strengthening through regional innovation expansion and bio-based feedstock advantages. In December 2025, a new Customer Experience and Innovation Center was inaugurated to serve South American home and personal care manufacturers, enhancing localized formulation development.

A 20% capacity increase in sodium chlorate and related processing aids in 2025, linked to the new Arauco pulp mill, has driven demand for cationic de-inking and pulp-processing surfactants. Leveraging extensive sugar cane and soybean production, Brazil has emerged as a global exporter of bio-based fatty alcohols and amines used in the synthesis of “Green Quats.” This bio-feedstock integration supports sustainable quaternary ammonium compound production for fabric softeners, disinfectants, and industrial cleaners, reinforcing Brazil’s competitiveness in the global cationic surfactants value chain.

Cationic Surfactants Market Report Scope

Cationic Surfactants market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2034)

|

$7.8 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Type (Quaternary Ammonium Salts, Amine Salts, Esterquats, Cationic Imidazolines, Cationic Biosurfactants), By Source (Synthetic, Bio Based), By Function (Emulsifiers and Dispersants, Conditioning Agents, Antimicrobial Agents, Antistatic and Fabric Softening Agents, Corrosion Inhibitors), By End Use Industry (Home and Fabric Care, Personal Care and Cosmetics, Industrial and Institutional Cleaning, Oil and Gas, Agriculture, Textile and Leather Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries, Clariant AG, Stepan Company, Nouryon, Kao Corporation, Croda International, Syensqo, Galaxy Surfactants, Global Amines Company, DuPont, Innospec, Lion Specialty Chemicals, Arkema, Godrej Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cationic Surfactants Market Segmentation

By Type

- Quaternary Ammonium Salts

- Amine Salts

- Esterquats

- Cationic Imidazolines

- Cationic Biosurfactants

By Source

By Function

- Emulsifiers and Dispersants

- Conditioning Agents

- Antimicrobial Agents

- Antistatic and Fabric Softening Agents

- Corrosion Inhibitors

By End Use Industry

- Home and Fabric Care

- Personal Care and Cosmetics

- Industrial and Institutional Cleaning

- Oil and Gas

- Agriculture

- Textile and Leather Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Cationic Surfactants Industry

- BASF SE

- Evonik Industries

- Clariant AG

- Stepan Company

- Nouryon

- Kao Corporation

- Croda International

- Syensqo

- Galaxy Surfactants

- Global Amines Company

- DuPont

- Innospec

- Lion Specialty Chemicals

- Arkema

- Godrej Industries

*- List not Exhaustive