Tertiary Amines Market 2025–2034: $5.8 Billion to $9.6 Billion at 5.8% CAGR Driven by Regional Capacity Build-Out, Coatings Integration, and Low-Emission Synthesis

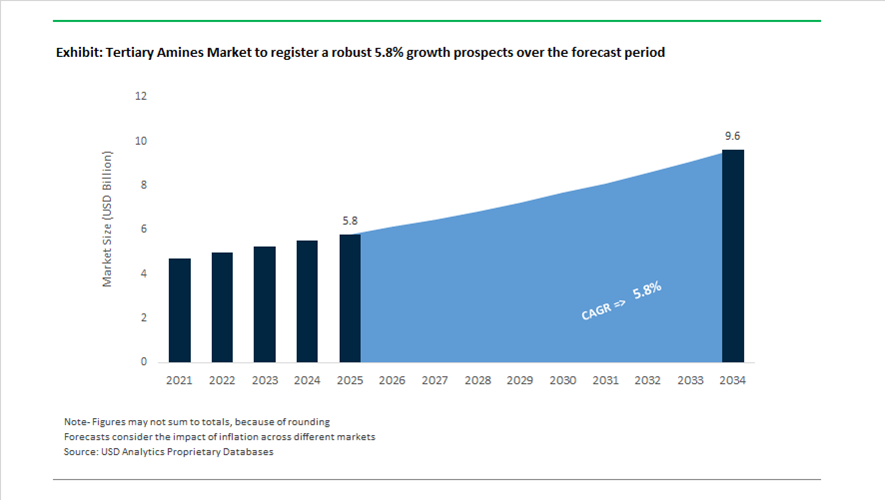

The global tertiary amines market is valued at $5.8 billion in 2025 and is projected to reach $9.6 billion by 2034, expanding at a CAGR of 5.8%. Tertiary amines remain critical intermediates in surfactants, epoxy curing agents, polyurethanes, oilfield chemicals, water treatment, agrochemicals, and pharmaceutical formulations. Structural growth is being shaped by three forces: (1) regional capacity localization in North America and India, (2) tightening sustainability regulations in Europe driving low-emission amine synthesis, and (3) premiumization of tertiary amine derivatives for personal care and high-performance coatings. Market participants are repositioning portfolios away from low-margin commodity amines toward specialty, high-purity, and application-tailored intermediates with compliance certifications.

North America witnessed a significant supply-side shift in 2025. In August 2025, Kao Corporation inaugurated a world-scale tertiary amine facility in Pasadena, Texas. The plant is designed to reduce import dependency from Asia and secure domestic supply for surfactants and sterilization agents used in home care and industrial disinfection. In June 2025, Aditya Birla Chemicals completed the acquisition of Cargill’s Dalton, Georgia site and announced plans to double capacity to 40,000 tons by early 2026, targeting tertiary amine-based epoxy curing agents. In February 2026, Aditya Birla introduced poly-aspartic ester resins at the Dalton facility, utilizing specialized tertiary amine catalysts to enable rapid-curing, UV-stable industrial coatings. These investments reinforce the trend toward vertically integrated amine-to-coatings value chains within the U.S. and India.

European producers are prioritizing decarbonization and portfolio optimization. Throughout 2025, BASF SE accelerated modernization of its Ludwigshafen intermediates complex, scaling low-emission amine synthesis using renewable electricity and bio-based feedstocks to align with EU 2026 sustainability reporting mandates. In 2024, Nouryon operationalized expanded capacity for high-purity tertiary amines in Asia and Europe, strengthening its position in oilfield and water treatment segments. Clariant AG confirmed ZDHC Level 3 compliance in 2025 for its tertiary amine-based textile auxiliaries, meeting global fashion supply chain requirements ahead of 2026 regulatory tightening. Meanwhile, Evonik Industries restructured its pharma amino business during 2024–2025 to focus on high-value tertiary amine intermediates for advanced drug delivery systems. In November 2025, Lotte Chemical Corporation exited its Pakistani PTA/amine exposure, signaling continued Asian portfolio migration toward electronics and specialty materials.

Structural Demand Reconfiguration and High-Value Specialization in the Tertiary Amines Market

Integrated World-Scale Tertiary Amine Platforms Securing the Global Biocides Value Chain

The tertiary amines market is moving decisively toward vertically integrated, regionally balanced production architectures as chemical producers seek to de-risk the supply of cationic surfactant intermediates. Alkyl tertiary amines such as dimethyl lauryl amine are foundational to Quaternary Ammonium Compounds, which remain non-substitutable across healthcare disinfection, institutional cleaning, fabric softeners, and industrial sanitization. Supply reliability and purity consistency have become procurement-critical, particularly as regulatory scrutiny on biocide efficacy and formulation stability intensifies.

A defining capacity milestone occurred in August 2025 when Kao Corporation commissioned its 20,000-ton-per-year tertiary amine facility in Pasadena, Texas. This investment completes Kao’s three-hub global manufacturing model spanning North America, Europe, and Asia. The strategic intent is not incremental volume but operational resilience, allowing uninterrupted Quat precursor supply to North American healthcare and consumer markets under its Global Sharp Top strategy. The facility leverages proprietary synthesis routes to deliver narrow-spec, high-purity amines that improve downstream Quat yield and reduce byproduct formation, a growing concern as formulators optimize active loading while managing regulatory exposure.

In parallel, European feedstock integration is reshaping competitive positioning. In September 2024, BASF brought online a world-scale alkyl ethanolamines expansion in Antwerp, lifting global capacity by roughly 30% to over 140,000 tons annually. The expansion targets tertiary alkanolamines such as dimethylethanolamine and methyldiethanolamine, which are increasingly specified in water treatment, gas sweetening, and industrial neutralization. By colocating amine synthesis with upstream feedstocks and logistics infrastructure, BASF is structurally lowering unit costs and strengthening long-term supply contracts with utilities, refiners, and municipal operators through 2026 and beyond.

Tertiary Alkanolamines Becoming Core Enablers of CCUS and Blue Hydrogen Economics

A second structural trend is the elevation of tertiary alkanolamines from mature gas-treating chemicals to mission-critical inputs in Carbon Capture, Utilization, and Storage and blue hydrogen infrastructure. Methyldiethanolamine has become the solvent of choice for large-scale CO₂ separation because of its high selectivity, lower regeneration energy demand, and reduced corrosion profile compared with primary and secondary amines. As national decarbonization roadmaps shift from pilot to asset-scale deployment, amine qualification is moving into multi-year procurement frameworks rather than project-based purchasing.

In March 2025, Saudi Aramco advanced this transition by acquiring a 50% stake in the Blue Hydrogen Industrial Gases Company at Jubail. The facility integrates MDEA-based amine scrubbing within a large CCS hub designed to decarbonize hydrogen supplied to the Jubail industrial cluster. Projects of this scale lock in sustained demand for specialty tertiary amine formulations optimized for low solvent loss, thermal stability, and minimal degradation under continuous operation.

Technology licensing is further reinforcing this trend. Throughout 2025, BASF expanded the global footprint of its OASE® blue gas treatment platform, including an October 2025 agreement with ANDRITZ for a Danish waste-to-energy facility targeting 435,000 tons of annual CO₂ capture. These systems rely on customized tertiary amine blends to reduce energy penalties during post-combustion capture, positioning amine suppliers as indirect beneficiaries of CCUS capital expenditure cycles.

Low-Emission and Reactive Tertiary Amine Catalysts for Circular Polyurethane Systems

The polyurethane sector is undergoing a chemistry reset as automotive, furniture, and electronics OEMs push toward circular materials and ultra-low interior emissions. Conventional volatile tertiary amine catalysts are increasingly incompatible with Vehicle Interior Air Quality requirements, creating a strong pull for reactive or non-fugitive tertiary amines that chemically bind into the polymer matrix. These catalysts maintain foam reactivity while eliminating long-term VOC release, a key differentiator in EV interiors and enclosed living spaces.

By mid-2025, Evonik had transitioned its global polyurethane amine catalyst portfolio to green electricity, aligning catalyst production with OEM sustainability audits. The company’s POLYCAT® SA series and digitally enabled TEGO® RISE optimization platform are being positioned for applications such as EV battery thermal insulation and low-emission seating foams. The strategic value lies not only in catalyst sales but in co-development partnerships with OEMs, where catalyst selection is embedded early in platform design cycles.

R&D momentum is accelerating around catalysts that balance reactivity with permanence. Reactive tertiary amines that covalently bond into the PU network are now being specified to eliminate odor complaints and meet tightening OEM standards from manufacturers such as Volkswagen and BMW. This shifts tertiary amines from commoditized accelerators into performance-critical enablers of recyclable, low-emission polymer systems.

Specialty Tertiary Amines for Hydrogen, E-Fuels, and Corrosion-Sensitive Systems

The expansion of hydrogen transport, storage, and synthetic fuels is opening a niche but high-value opportunity for specialty tertiary amines as corrosion inhibitors and stabilizing additives. Hydrogen environments introduce unique degradation mechanisms, including embrittlement of legacy carbon-steel pipelines and oxidative instability in synthetic fuels. Conventional inhibitors are often incompatible with hydrogen purity or fuel cell systems, elevating the role of tailored amine chemistries.

Industry pilots in mid-2025, including expansions linked to the Haru Oni e-fuel program, have begun evaluating tertiary amine-based metal deactivators to suppress oxidation in e-fuels and stabilize fuel blends during storage and transport. These amines form protective molecular layers on metal surfaces, reducing corrosion without introducing contaminants that interfere with downstream combustion or electrochemical systems.

Tertiary Amines Market Share and Segmentation Insights

C12 Tertiary Amines Lead Market with Optimal Surfactant Intermediate Properties

C12 tertiary amines accounted for 32.80% of the tertiary amines market in 2025, supported by their role as key intermediates in producing quaternary ammonium compounds, surfactants, and conditioning agents. Derived primarily from lauric acid sourced from coconut oil, C12 amines provide an optimal balance of performance, mildness, and biodegradability for personal care and cleaning formulations. Their versatility across applications ensures strong market penetration. The 2025 market dynamic emphasizes feedstock dependency on coconut oil supply, where fluctuations in coconut production and competing demand influence pricing and availability of C12-based amines in global markets.

Personal Care and Cosmetics Segment Drives Demand for Tertiary Amines in Conditioning and Emulsification

Personal care and cosmetics accounted for 32.80% of tertiary amines market demand in 2025, driven by their use in hair conditioners, shampoos, skincare emulsifiers, and antistatic agents. Tertiary amines serve as key intermediates for quaternary ammonium compounds that deliver conditioning and softening performance in premium formulations. The expansion of global beauty and personal care markets supports consistent demand growth. The 2025 trend highlights sustainable and traceable feedstock sourcing, where manufacturers adopt RSPO-certified palm kernel oil and coconut-based raw materials, enabling brands to meet clean beauty, renewable sourcing, and ethical supply chain commitments.

Tertiary Amines Market Competitive Landscape

The tertiary amines market in 2026 is shaped by local-for-local manufacturing strategies, renewable-powered amination processes, and rising demand for high-purity fatty amines. Producers are optimizing supply chains, reducing Scope 3 emissions, and advancing sustainable intermediates for surfactants, disinfectants, and personal care formulations.

Kao Corporation Expands Global Tertiary Amine Capacity with Three-Continent Supply Strategy

Kao Corporation leads the global tertiary amines market with its "Global Sharp Top" strategy under K27, strengthening supply resilience through geographic diversification. The 20,000-ton Pasadena plant, commissioned in August 2025, completes a three-continent production network spanning the U.S., Europe, and Asia. This localized production model reduces transportation emissions and improves supply reliability for North American customers. The facility also supports specialty derivative manufacturing through strategic partnerships. Kao’s tertiary amines are key intermediates for quaternary ammonium compounds used in disinfectants and industrial cleaning. Strong integration into surfactant value chains reinforces its global leadership.

BASF Advances Low-Carbon Amines Portfolio with 100% Renewable Electricity and Verbund Integration

BASF is transforming the tertiary amines market through its "Winning Ways" strategy, focusing on decarbonization and operational efficiency. The full transition of European amine production to 100% renewable electricity has reduced CO2 emissions by 188,000 tons annually. BASF achieved an average 8% reduction in Product Carbon Footprint across its amines portfolio, supporting downstream Scope 3 targets. The expansion of its Zhanjiang Verbund site strengthens regional supply for Asia-Pacific demand. With €59.7 billion in 2025 sales, BASF continues to invest in green transformation initiatives. Its integrated Verbund model ensures cost efficiency and consistent supply of specialty amine intermediates.

Arkema Scales Specialty Amine Production for Electronics and Battery Applications in Asia

Arkema is positioning itself as a specialty materials leader, expanding its tertiary amine capabilities for high-growth electronics and energy storage markets. The new Singapore production unit, operational in January 2026, significantly increases global capacity for advanced materials. A 20% expansion of Kynar® PVDF production in China supports demand for battery-grade materials utilizing amine-based additives. Under its 2028 Ambition, Arkema is shifting toward high-margin applications in AR/VR devices, filtration systems, and healthcare technologies. Integration with the Virtucycle® recycling platform enables circular material solutions. Focus on specialty amines strengthens Arkema’s role in next-generation industrial applications.

Eastman Strengthens Specialty Amine Portfolio with Cost Optimization and DIMLA Production Expansion

Eastman Chemical Company is enhancing competitiveness in the tertiary amines market through structural cost reductions and specialty product optimization. The company achieved $100 million in savings in 2025, entering 2026 with a lean operational model. Its DIMLA tertiary amine production facilities in Belgium and Florida are being optimized for agricultural and personal care applications. Strong operating cash flow nearing $1 billion underscores financial resilience. Eastman is leveraging methanolysis-based recycled feedstocks to support sustainable chemical production. Focus on high-purity specialty amines ensures consistent demand across performance-driven end markets.

Albemarle Streamlines Specialty Chemicals Portfolio While Maintaining High-Value Amine Intermediates Supply

Albemarle Corporation is restructuring its portfolio, divesting the Ketjen business to focus on core energy and specialty chemical segments. Despite this transition, its Specialties division recorded $349 million in Q4 2025 sales, driven by strong demand for high-performance amine intermediates. Operational disruptions at the Jordan Bromine Company were resolved quickly, restoring full production by early 2026. The company is targeting $300–$400 million in productivity improvements to enhance operational efficiency. Bromine-based amine intermediates remain critical for industrial and catalyst applications. Strategic portfolio optimization ensures continued focus on high-margin specialty chemicals.

Global Amines Company Strengthens Bio-Based Tertiary Amine Supply with Integrated Oleochemical Feedstock Model

Global Amines Company (GAC), a joint venture between Clariant and Wilmar, exemplifies raw material integration in the tertiary amines market. Leveraging Wilmar’s palm and coconut oil assets, GAC ensures a stable supply of bio-based feedstocks. The company is advancing mass balance-certified tertiary amines to meet sustainability requirements in Europe and North America. Its products are widely used in betaines and amine oxides, essential for sulfate-free personal care formulations. Strong positioning in biodegradable surfactants supports growth in eco-friendly home care markets. Integrated production capabilities enhance supply security and cost efficiency.

United States Tertiary Amines Market Accelerated by On-Shoring and Hygiene-Centric Demand

The United States tertiary amines market in 2025–2026 is being reshaped by capacity localization and structurally higher demand from hygiene, polyurethane, and oilfield chemical applications. In August 2025, Kao Corporation inaugurated a world-scale tertiary amine production facility in Pasadena, Texas, with an annual capacity of 20,000 tons. This investment was explicitly designed to shorten lead times and de-risk North American supply chains serving disinfectants, personal care surfactants, and institutional hygiene formulations. The move reflects a broader shift toward regionalized amine production following post-2024 logistics volatility and regulatory scrutiny of imported intermediates.

Parallel capacity strengthening has occurred in specialty catalysts. In early 2025, BASF SE completed its specialty amines expansion at Geismar, Louisiana, targeting Lupragen™ tertiary amines used as high-efficiency catalysts in polyurethane foams and elastomers. Trade policy has further reinforced domestic production economics. Higher U.S. tariffs imposed in 2025 on chemical intermediates from Belgium and the Netherlands have accelerated on-shoring of tertiary amine synthesis for agrochemical and pharmaceutical formulators. Downstream, oilfield activity in the Permian Basin continues to support demand for C-12 and C-14 tertiary amine-based corrosion inhibitors engineered for deep-well stability. By 2026, U.S. producers are also embedding real-time carbon tracking into operations to comply with tightening state-level ESG reporting requirements, positioning sustainability transparency as a commercial differentiator.

China Tertiary Amines Market Anchored in Scale, Self-Sufficiency, and Digital Manufacturing

China remains the global volume anchor for tertiary amines, with 2025 marking a transition from scale-led growth to technology-enabled efficiency. Integrated chemical mega-projects commissioned in Hunan and Hubei reached full operational status in 2025, with Sinopec and peers optimizing these clusters for C-14 tertiary amines, currently the fastest-growing segment due to their role in disinfectants, fabric softeners, and quaternary ammonium compounds. These assets reinforce China’s leadership in hygiene chemicals while supporting export flows into Southeast Asia entering 2026.

Policy-driven self-sufficiency has become equally important. Under updated industrial modernization guidelines, China has prioritized domestic production of pharmaceutical-grade tertiary amines to reduce dependence on European high-purity imports used in antiviral and oncology drug synthesis. This push is supported by rapid digitalization. In 2025, leading producers deployed AI-driven batch control systems and automated microreactor technologies, delivering yield improvements in high-chain tertiary amines while cutting process waste by approximately 12%. The combination of scale, automation, and regulatory alignment continues to consolidate China’s position as both a cost-efficient and increasingly quality-driven supplier.

India Tertiary Amines Market Strengthened by Import Substitution and Export Competitiveness

India’s tertiary amines market is advancing through targeted policy support and capacity specialization. The 2025–2026 Notification No. 50 introduced strategic import restrictions on select amine salts, including tertiary butylamine derivatives, to incentivize domestic manufacturing under the Make in India framework. This policy has directly benefited agrochemical formulators and intermediate producers, reducing exposure to volatile overseas supply.

On the production front, Balaji Amines reported substantial progress in late 2025 on its specialized amine units, focusing on DMAE and related tertiary derivatives for water treatment, pharmaceuticals, and resins. Environmental infrastructure has also emerged as a demand driver. As India accelerates commissioning of more than 50 Zero Liquid Discharge treatment plants across Gujarat and Maharashtra, tertiary amine-based flocculants are seeing increased uptake. Export competitiveness has improved in parallel. Indian producers expanded tertiary amine exports to Europe by 18% during FY2025, leveraging optimized raw material sourcing and pricing dislocations in Western markets.

Germany Tertiary Amines Market Defined by Bio-Based Transition and Regulatory Leadership

Germany’s tertiary amines market is characterized by regulatory alignment and early adoption of green chemistry pathways. The strategic distribution alliance formed between BASF SE and OQEMA, which reached full operational scale in 2025, has streamlined market access for both standard and specialty amines across Europe, with a particular focus on the UK and Ireland. This has strengthened supply reliability while allowing producers to concentrate on higher-value formulations.

Sustainability is the defining competitive axis. German refiners are leading the shift toward bio-based tertiary amines derived from plant oils, supported by closed-loop water systems deployed across Rhine-Ruhr facilities by 2026. Regulatory compliance further reinforces market positioning. By late 2025, German manufacturers completed the transition to ZDHC MRSL V3.1 Level 3 standards, ensuring tertiary amines supplied to textile, leather, and personal care sectors meet the most stringent global hazardous substance benchmarks. This regulatory foresight is enabling German suppliers to command preference in premium European value chains.

Comparative Snapshot: Tertiary Amines Market by Country

Tertiary Amines Market County Level Snapshot

|

Country

|

Strategic Emphasis

|

Key Demand Driver

|

Market Implication

|

|

United States

|

On-shoring and specialty catalysts

|

Hygiene, PU foams, oilfield chemicals

|

Reduced import exposure and higher value-added output

|

|

China

|

Scale with digital optimization

|

Disinfectants and pharma intermediates

|

Cost-efficient, high-volume, quality-improving supply

|

|

India

|

Import substitution and exports

|

Agrochemicals and wastewater treatment

|

Rapid capacity utilization and export-led growth

|

|

Germany

|

Bio-based transition and compliance

|

Textiles, leather, specialty formulations

|

Premium positioning through regulatory leadership

|

Tertiary Amines Market Report Scope

Tertiary Amines Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.8 Billion

|

|

Market Size (2034)

|

$9.6 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Product Type (C8 Tertiary Amines, C10 Tertiary Amines, C12 Tertiary Amines, C14 Tertiary Amines, C16 Tertiary Amines, Other Tertiary Amines), By Chemical Classification (Aliphatic Tertiary Amines, Aromatic Tertiary Amines, Heterocyclic Tertiary Amines), By Synthesis Process (Reductive Amination, Alkylation of Amines, Hydrogenation of Nitriles), By Application (Surfactants and Emulsifiers, Biocides and Disinfectants, Chemical Intermediates, Corrosion Inhibitors, Polyurethane Catalysts, Flotation Agents), By End-Use Industry (Personal Care and Cosmetics, Home and Institutional Cleaning, Agrochemicals, Pharmaceuticals, Petroleum and Oilfield, Water Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Eastman Chemical Company, Kao Corporation, Arkema S.A., BASF SE, Albemarle Corporation, Lonza Group Ltd, Balaji Amines Ltd., Indo Amines Ltd., KLK OLEO, Solvay S.A., Dow Chemical Company, Temix Oleo S.r.l., Evonik Industries AG, Global Amines Company Pte. Ltd., Hunan Gomeet Biotechnology Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tertiary Amines Market Segmentation

By Product Type

- C8 Tertiary Amines

- C10 Tertiary Amines

- C12 Tertiary Amines

- C14 Tertiary Amines

- C16 Tertiary Amines

- Other Tertiary Amines

By Chemical Classification

- Aliphatic Tertiary Amines

- Aromatic Tertiary Amines

- Heterocyclic Tertiary Amines

By Synthesis Process

- Reductive Amination

- Alkylation of Amines

- Hydrogenation of Nitriles

By Application

- Surfactants and Emulsifiers

- Biocides and Disinfectants

- Chemical Intermediates

- Corrosion Inhibitors

- Polyurethane Catalysts

- Flotation Agents

By End-Use Industry

- Personal Care and Cosmetics

- Home and Institutional Cleaning

- Agrochemicals

- Pharmaceuticals

- Petroleum and Oilfield

- Water Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Tertiary Amines Industry

- Eastman Chemical Company

- Kao Corporation

- Arkema S.A.

- BASF SE

- Albemarle Corporation

- Lonza Group Ltd

- Balaji Amines Ltd.

- Indo Amines Ltd.

- KLK OLEO

- Solvay S.A.

- Dow Chemical Company

- Temix Oleo S.r.l.

- Evonik Industries AG

- Global Amines Company Pte. Ltd.

- Hunan Gomeet Biotechnology Co., Ltd.

*- List not Exhaustive