Market Overview: PFAS-Free Innovation and Power Infrastructure Demand Push Antistatic Agents Market Toward $2.26 Trillion by 2034

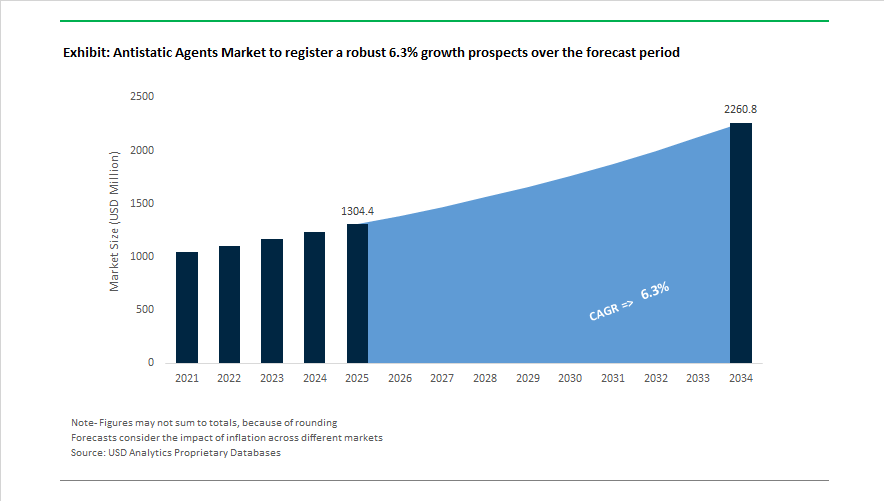

The antistatic agents market stands at $1,304.4 Million in 2025 and is projected to reach $2,260.5 Million by 2034, advancing at a 6.3% CAGR. Market momentum is driven by rising demand for permanent antistatic additives, inherently dissipative polymers, conductive polymer modifiers, static control agents for packaging, XLPE cable stabilizers, and dust-repellent agricultural films. A major regulatory inflection occurred during 2024–2025 when Clariant completed its transition to a fully PFAS-free additive portfolio, replacing legacy processing aids with AddWorks® PPA solutions that provide melt fracture control and static dissipation without persistent fluorochemicals. This shift established a new sustainability benchmark across polymer processing, coatings, and packaging applications.

Infrastructure electrification and electronics protection accelerated innovation in 2025–2026. At Plastindia in February 2026, BASF introduced Irgastab® Cable KV 10, designed for peroxide-crosslinked polyethylene in high-voltage cable manufacturing, addressing scorch prevention and electrostatic stability during extrusion. Croda International reinforced its permanent antistatic leadership in January 2026 following successful integration of IonPhasE technology based on inherently dissipative polymers for electronics packaging. In December 2025, Arkema announced the divestment of certain plastic additive assets, enabling strategic concentration on high-margin antistatic and flame-retardant specialty materials.

Sustainable surface engineering and recycled polymer compatibility emerged as dominant themes. Songwon Industrial announced a Saudi Arabia OPS plant in November 2025 to produce integrated additive pellets combining antioxidants and antistatic components for regional petrochemical customers. In September 2025, Songwon debuted XP2121 to improve static performance in recycled polypropylene streams. Evonik Industries advanced its polymer additives strategy in January 2026 with TROGAMID® R recycled transparent polyamide grades incorporating non-migratory antistatic systems for optical and electronic housings, followed by confirmation in February 2026 that its restructuring program would prioritize semiconductor and lithium-ion battery applications. Distribution and formulation ecosystems expanded when Nouryon partnered with IMCD in December 2025 to scale textile and leather antistatic chemistries, while simultaneously breaking ground on a Brazil innovation center for sustainable surfactant-based static control. Meanwhile, Clariant introduced bio-based Ceridust® 8170 M in 2025, and BASF showcased Tinuvin® NOR® for greenhouse films in February 2026, demonstrating how PFAS-free static control, recycled polymer enhancement, electronics protection, and power infrastructure modernization are reshaping the global antistatic additives landscape.

Trends and Opportunities Redefining the Antistatic Agents Market

The Global Antistatic Agents Market is entering a technology-driven expansion phase, powered by explosive semiconductor growth, stricter food-contact regulations, and rapid adoption of permanent ESD-safe polymers. Demand is accelerating for non-migratory antistatic additives, inherently dissipative polymers (IDPs), and carbon-based conductive agents as manufacturers across electronics, packaging, automotive, and additive manufacturing pivot away from legacy surfactant systems. These shifts are reshaping material science priorities and creating premium growth segments tied directly to ultra-clean manufacturing, regulatory compliance, and next-generation mobility.

Semiconductor Scale-Up Forces Precision ESD Control and High-Performance Antistatic Materials

The global electronics boom is fundamentally redefining antistatic performance standards. According to World Semiconductor Trade Statistics (February 2026), worldwide semiconductor sales are projected to reach $975 billion in 2026, representing a 25% year-on-year increase fueled by GenAI data centers and advanced computing infrastructure. This historic production peak is directly translating into surging demand for ESD-safe packaging, antistatic trays, and cleanroom-compatible polymer components.

At advanced nodes approaching 3nm and 2nm, devices are now vulnerable to electrostatic discharge events as low as 5 volts, forcing a transition from conventional static-dissipative additives toward conductive antistatic coatings capable of near-instant charge neutralization. Institutional procurement data from early 2026 indicates that roughly 30% of electronic component failures remain ESD-related, making yield loss a critical economic driver. As a result, major fabs, including facilities supported under India Semiconductor Mission 2.0, are mandating certified antistatic substrates as default standards, accelerating adoption of permanent antistatic polymers and high-reliability ESD protection systems.

Food Contact Regulations Accelerate the Phase-Out of Migratory Antistatic Agents

Parallel regulatory pressure is reshaping antistatic chemistry in food packaging. The EU Regulation (EU) 2025/351 introduced strict limits on Non-Intentionally Added Substances (NIAS), capping migration of non-evaluated additives at 0.01 mg/kg, effectively sidelining many fatty amine-based migratory antistats. This was reinforced by Regulation (EU) 2026/245, issued February 2, 2026, which restricted oxidized wax antistatic aids to 0.3% in food-contact PET and PLA, narrowing the viability of traditional formulations.

In the United States, the U.S. Food and Drug Administration intensified post-market surveillance in late 2025, targeting long-chain antistatic agents in flexible packaging. This regulatory momentum, combined with April 2026 chemical reporting requirements, is pushing global food brands toward PFAS-free, non-blooming antistatic additives that remain embedded within polymer matrices. As a result, packaging converters are rapidly migrating to permanent antistatic masterbatches to ensure compliance while maintaining transparency and mechanical performance.

Inherently Dissipative Polymers Unlock Premium Applications in Electronics, Automotive, and 3D Printing

A high-value opportunity is emerging around Inherently Dissipative Polymers (IDPs) and polymer alloys that provide permanent static control without humidity dependence or surface migration. Market intelligence from February 2026 confirms a decisive industrial shift toward these materials, which deliver stable surface resistivity across wide environmental conditions, a critical requirement for aerospace electronics, ADAS modules, and medical device housings.

To address this demand, Arkema expanded production capacity of its Pebax Rnew bio-circular elastomers by 40%, positioning these materials as next-generation permanent antistatic masterbatches for electronics and healthcare packaging. Additive manufacturing is also opening new revenue channels. A 2025 collaboration between Croda and Essentium introduced the first color-capable 3D-printing filaments with built-in antistatic functionality, enabling on-demand fabrication of ESD-safe robotic grippers, jigs, and cleanroom tooling. This convergence of IDPs and advanced manufacturing is creating a specialized growth lane for customized antistatic components.

Carbon Nanotubes and Graphene Redefine Antistatic Performance at Ultra-Low Loadings

Conductive carbon additives are redefining the performance ceiling of antistatic agents. Carbon Nanotubes (CNTs) and graphene enable electrical conductivity at extremely low concentrations, preserving polymer strength and optical clarity. Industry outlooks project the CNT market to reach $6.82 billion in 2026, driven largely by EV batteries, with this scale-up reducing costs for antistatic deployment in battery enclosures and high-voltage components.

R&D disclosures from OCSiAl (2025) demonstrate that single-wall carbon nanotubes can achieve antistatic thresholds at loadings as low as 0.01% to 0.1%, compared with over 15% for traditional carbon black. This efficiency is accelerating adoption in transparent electronics packaging and precision housings. Manufacturing capacity is also expanding. In April 2024, Canatu and DENSO launched a high-throughput CNT reactor, tripling output to support Advanced Driver-Assistance Systems (ADAS), where antistatic CNT films prevent dust accumulation on optical sensors without degrading signal clarity. These developments position graphene and CNT-based antistatic agents as cornerstone technologies for next-generation electronics and mobility platforms.

Antistatic Agents Market Share and Segmentation Insights

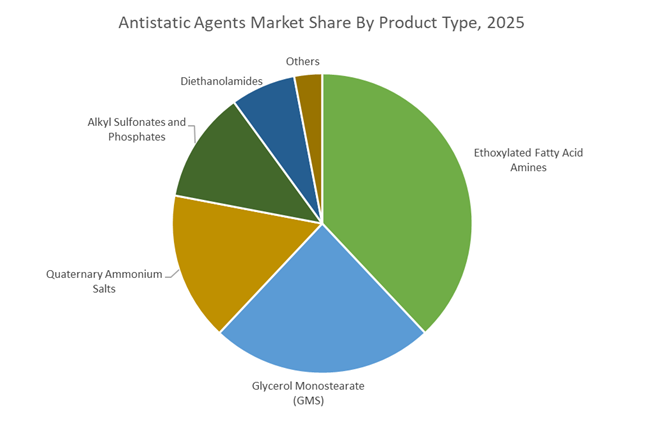

Market Share by Product Type: Ethoxylated Fatty Acid Amines Hold 38% as GMS and Quats Gain in High-Clarity and ESD Applications

Ethoxylated fatty acid amines account for roughly 38% of the global antistatic agents market in 2025, remaining the dominant chemistry due to their excellent cost-performance and FDA food-contact approval. These non-ionic migratory antistatic additives bloom to PE and PP film surfaces, attract atmospheric moisture, and dissipate static charge, making them indispensable in packaging films, industrial liners, and agricultural films (commercial grades include Crodamide, Atmer, and Armostat). Glycerol monostearate (GMS) follows as a preferred low-toxicity option for rigid PVC, polystyrene, and thermoformed containers, also delivering lubrication and antifog benefits in food packaging and medical devices. Quaternary ammonium salts serve premium ESD-safe applications in ABS, PC, and POM, providing permanent, humidity-independent conductivity for electronics housings and cleanroom components. Alkyl sulfonates and phosphates address high-temperature polymers like PET and nylon, while diethanolamides decline in textiles and detergents due to nitrosamine concerns. Industry momentum is shifting toward permanent polymeric antistatic agents for cleanroom and electronics reliability.

Market Share by End-Use Industry: Packaging Commands 44% as Electronics Drives High-Value ESD Adoption

Packaging represents approximately 44% of antistatic agent consumption in 2025, led by food packaging films, industrial FIBCs and stretch hoods, ESD-safe electronics packaging, and agricultural greenhouse films where dust attraction impairs light transmission and line efficiency. Static control is critical on high-speed form-fill-seal lines and in powder filling operations to reduce dust explosion risk. Electronics and electricals form the fastest-growing, highest-value segment, using permanent antistatic additives in carrier tapes, PCB trays, cable jacketing, and cleanroom infrastructure, with miniaturization and 5G components demanding surface resistivity below 10⁹ Ω. Automotive integrates antistatics in interiors, fuel systems, and EV battery housings to prevent ignition and dust accumulation. Textiles rely on antistatic finishes for uniforms, carpets, and sportswear, while medical and healthcare requires ISO 10993 and USP Class VI compliant additives for OR garments, IV tubing, and device packaging. Asia-Pacific leads volume (55%+), while North America and Europe drive permanent ESD and medical-grade innovation.

Antistatic Agents Market Competitive Landscape

The global antistatic agents market is increasingly shaped by permanent antistatic technologies, PFAS-free formulations, bio-based ESD solutions, and masterbatch integration, driven by rising demand from electronics packaging, EV components, medical devices, cleanroom manufacturing, and e-commerce logistics. Market leaders are competing on humidity-independent performance, non-migratory conductive networks, ISCC PLUS mass-balance certification, and AI-assisted molecule design. Strategic priorities now center on sustainable antistatic additives, internal antistatic agents for ultra-low RH environments, and multifunctional additive systems that combine static control with thermal stabilization, slip, and antiblock properties. The competitive edge lies in regulatory-ready portfolios, localized APAC production, and permanent ESD protection across high-value polymer applications.

Permanent antistatic innovation and cleanroom-grade ESD leadership by Croda International plc

Croda leads the antistatic agents market with its Ionphas™ permanent antistatic technology, creating conductive networks inside polymers rather than relying on surface migration. In April 2025, Croda launched color-capable 3D-printing filaments incorporating Ionphas™, enabling ESD-safe aerospace and electronics housings with lifetime conductivity. Its Atmer™ migratory line complements Ionphas™ for flexible packaging, while Ionphas dominates 2026 cleanroom applications due to its non-leaching profile for semiconductor manufacturing. Strategically, Croda is advancing bio-based ESD solutions using plant-derived ethoxylated amines. The company’s strength lies in precision ESD engineering, delivering tailored molecular weights that preserve film transparency and mechanical integrity.

AI-driven antistatic molecule design and EV-ready additives from BASF SE

BASF commands high-volume industrial and automotive antistatic demand through AI-powered formulation platforms and multifunctional additive systems. During 2025 to 2026, BASF embedded AI simulations into additive discovery, accelerating custom antistatic development for high-temperature EV battery trays. Its Irgafos® and Irganox® portfolios integrate antistatic performance with thermal stabilization for high-speed extrusion. BASF expanded production at its Pudong site in late 2025 to supply APAC e-commerce packaging markets. Under its Green Transformation strategy, BASF is converting additive manufacturing to green electricity, targeting a 25% reduction in Scope 1 and 2 emissions by 2030.

PFAS-free and regulatory-ready antistatic solutions pioneered by Clariant AG

Clariant is redefining regulatory compliance in antistatic additives through PFAS-free and water-based systems. Its AddWorks® PPA replaces fluorinated processing aids while delivering antistatic performance and surface smoothness in polyolefin films. The Hostastat® range targets rigid packaging and electronics, with internal antistatic agents designed for immediate effect even below 15% relative humidity. Strategically, Clariant is executing a China-first approach, aiming for 14% of global sales from China via its Shanghai Innovation Hub. Through EcoTain® certification, Clariant embeds lifecycle sustainability data directly into technical documentation for electronics and packaging customers.

Silicone and amine chemistry excellence for specialty antistatics at Evonik Industries AG

Evonik specializes in high-performance antistatic agents for polyurethane foams, coatings, and niche applications including medical films and aerospace fuels. In early 2025, Evonik introduced “Debonding on Demand,” combining conductive and antistatic additives to enable end-of-life adhesive release for improved recyclability. The company streamlined North American distribution in May 2026 to deepen technical support for coating additives. Evonik’s silicone and amine chemistry platforms are widely adopted in automotive seating and compressed PU foams. With ISCC PLUS certification at its Essen site, Evonik now supplies mass-balance bio-based antistatics as drop-in replacements for fossil-derived products.

Non-migratory medical-grade antistatics engineered by Arkema S.A.

Arkema dominates permanent antistatic applications in medical and high-performance polymers using block-copolymer chemistry. Its Pebax® MV1074 SA01 MED delivers plasticizer-free, permanent antistatic performance in inhalers, surgical tools, and biopharmaceutical tubing. Following the acquisition of PI Advanced Materials, Arkema expanded into polyimide films for flexible electronics requiring rigorous static control. Unlike migratory surfactants, Arkema’s additives form internal 3D conductive networks that last the full device lifecycle. Key applications include face masks and pharmaceutical components, where antistatic protection must coexist with strict biocompatibility and particle-control requirements.

Masterbatch-based antistatic systems for e-commerce packaging from Ampacet Corporation

Ampacet leads customized antistatic masterbatch solutions for packaging and consumer goods, anchored by its Permastat® line for humidity-independent PE and PP protection. In 2025, Ampacet expanded its Syn-Tech portfolio, combining antistatic, slip, and antiblock agents into single pellets to simplify film converter operations. Strategically focused on e-commerce optimization, Ampacet addresses last-mile packaging challenges by preventing dust accumulation on premium electronics during long shipping cycles. Its sustainability assessment services help converters select antistatic additives compatible with infrared recycling systems, reinforcing Ampacet’s role as a technical partner in circular packaging design.

United States Antistatic Agents Market: Semiconductor Sovereignty and Non-PFAS Static Control

The United States has positioned antistatic agents as a strategic enabler for semiconductor and energy infrastructure security. In late 2025, the U.S. Department of Energy expanded its Critical Materials Innovation funding, allocating USD 355 million toward high-performance chemical additives that ensure electrostatic discharge safety in domestic semiconductor fabs and cleanroom ecosystems. This funding aligns directly with CHIPS Act implementation, which led to the construction of three new static-controlled fabrication facilities in the Southwest during 2025, driving a documented surge in demand for ultra-pure antistatic flooring, garments, and polymer additives.

Regulatory pressure is equally decisive. Under the EPA’s 2024 rule enforced through 2026, manufacturers have accelerated the phase-out of persistent bioaccumulative substances such as PIP (3:1). Major suppliers including 3M and Avient have transitioned to fluoro-free antistatic masterbatches to maintain access to electronics, fashion, and medical supply chains. Beyond electronics, U.S. research programs are prioritizing antistatic stabilizers for liquid metal batteries and long-duration grid storage, focusing on additives that preserve conductivity profiles over 20-year operational lifecycles. In October 2025, Fraser Anti-Static Techniques launched its Model 4825 24V DC Ionised Airgun, reinforcing the shift toward precision static neutralization in high-speed medical and electronics production lines.

India Antistatic Agents Market: Domestic Capability Building and PCR-Compatible Antistatic Systems

India’s antistatic agents landscape is being reshaped by value-chain localization and recycled plastics mandates. In July 2025, NITI Aayog released its “Powering India’s Participation in Global Value Chains” framework, introducing Opex subsidies to incentivize domestic production of critical additives such as ethoxylated fatty acid amines. This policy underpins the government’s authorization of eight high-potential chemical clusters with dedicated R&D funding, aimed at achieving self-sufficiency in high-grade antistatic polymers for electronics and appliance exports.

Regulation is a major demand driver. The amended Plastic Waste Management Rules, effective April 2025, mandate a minimum of 30% recycled content in Category I packaging. This has forced formulators to develop new antistatic stabilizers capable of preventing degradation and static build-up in post-consumer recycled resins. India’s growing prominence as a manufacturing hub is further reflected in global supplier participation at PLASTINDIA 2026, where smart static control systems for automotive interiors, textiles, and consumer electronics are expected to dominate technical showcases.

China Antistatic Agents Market: Environmental Consolidation and Precision Application Technologies

China continues to dominate volume consumption of antistatic agents while tightening environmental oversight. Under the updated 14th Five-Year Plan, the Ministry of Ecology and Environment initiated a new round of Blue Sky audits in mid-2025, consolidating antistatic agent production into five state-monitored Green Chemical Zones to reduce hazardous runoff and improve compliance transparency.

At the application level, Chinese textile clusters in Jiangsu have adopted digital precision dyeing and finishing systems that apply antistatic agents with up to 95% less wastewater. This capability supports high-end apparel exports to the European Union, where traceability and environmental performance are increasingly scrutinized. In parallel, China’s solar industry is deploying high-purity antimony-based and organic antistatic finessing agents to enhance dust repellence and surface conductivity control on photovoltaic glass, improving operational efficiency in large-scale solar farms.

South Korea Antistatic Agents Market: Non-Migratory Platforms and Global Standard Setting

South Korea has emerged as a technology benchmark for non-migratory antistatic solutions. In late 2025, LG Electronics reported that B2B sales of its PuroTec™ glass-matrix additive platform doubled year-over-year, positioning the technology as a core growth pillar for antistatic coatings in home appliances and advanced display panels. Production capacity at the LG Smart Park in Changwon now stands at 4,500 tons annually, serving global demand for low-leaching, long-life static control.

Standardization is a strategic differentiator. In September 2025, South Korean manufacturers signed a memorandum of understanding with SGS Korea to establish global low-leaching benchmarks for antistatic agents used in food-contact plastics. This move addresses buyer demand for verifiable performance and regulatory clarity across export markets.

Germany Antistatic Agents Market: Circular Chemistry and Aerospace-Grade Certification

Germany’s antistatic agents industry is defined by circular economy compliance and high-specification applications. In 2025, BASF integrated AI-powered molecular simulations to accelerate the design of biodegradable antistatic surfactants, cutting R&D timelines by an estimated 30%. Sustainability milestones were reinforced earlier with the launch of biosurfactant solutions by Evonik, aligned with the EU’s 2026 Green Deal chemical targets.

Germany also plays a critical role in aerospace certification. In 2025, material scientists finalized the certification of low-conductivity antistatic sheets for the Airbus supply chain, meeting stringent fire safety, toxicity, and enclosed-cabin performance requirements. This positions German suppliers at the intersection of sustainability and mission-critical reliability.

Strategic Positioning of the Antistatic Agents Industry by Country

Antistatic Agents Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Industry Implications

|

|

United States

|

Semiconductor localization and non-PFAS reformulation

|

Ultra-pure cleanroom, EV storage, and medical manufacturing

|

|

India

|

Value-chain localization and PCR mandates

|

Electronics exports and recycled packaging compatibility

|

|

China

|

Environmental consolidation and precision finishing

|

Apparel exports and solar glass performance

|

|

South Korea

|

Non-migratory platforms and global standards

|

Appliances, displays, and food-contact plastics

|

|

Germany

|

Circular chemistry and aerospace certification

|

Sustainable coatings and high-spec transport materials

|

Antistatic Agents Market Report Scope

Antistatic Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1304.4 Million

|

|

Market Size (2034)

|

$2260.5 Million

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Form Type (Liquid, Powder, Masterbatch, Concentrate), By Product Type (Ethoxylated Fatty Acid Amines, Glycerol Monostearate, Diethanolamides, Quaternary Ammonium Salts, Alkyl Sulfonates and Phosphates), By Polymer Type (Polypropylene, Polyethylene, Polyvinyl Chloride, Acrylonitrile Butadiene Styrene, Engineering Plastics), By End Use Industry (Packaging, Electronics and Electricals, Automotive, Textiles, Medical and Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc, Evonik Industries AG, Clariant AG, Croda International Plc, Arkema SA, LG Chem Ltd, 3M Company, Kao Corporation, Solvay SA, Mitsubishi Chemical Group, ADEKA Corporation, Ampacet Corporation, Avient Corporation, LyondellBasell Industries NV

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Antistatic Agents Market Segmentation

By Form Type

- Liquid

- Powder

- Masterbatch

- Concentrate

By Product Type

- Ethoxylated Fatty Acid Amines

- Glycerol Monostearate

- Diethanolamides

- Quaternary Ammonium Salts

- Alkyl Sulfonates and Phosphates

By Polymer Type

- Polypropylene

- Polyethylene

- Polyvinyl Chloride

- Acrylonitrile Butadiene Styrene

- Engineering Plastics

By End Use Industry

- Packaging

- Electronics and Electricals

- Automotive

- Textiles

- Medical and Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Antistatic Agents Industry

- BASF SE

- Dow Inc

- Evonik Industries AG

- Clariant AG

- Croda International Plc

- Arkema SA

- LG Chem Ltd

- 3M Company

- Kao Corporation

- Solvay SA

- Mitsubishi Chemical Group

- ADEKA Corporation

- Ampacet Corporation

- Avient Corporation

- LyondellBasell Industries NV

*- List not Exhaustive