Market Overview: BASF Capacity Expansion and Clean Label Food Trends Propel Antioxidants Market Toward $8.8 Billion by 2034

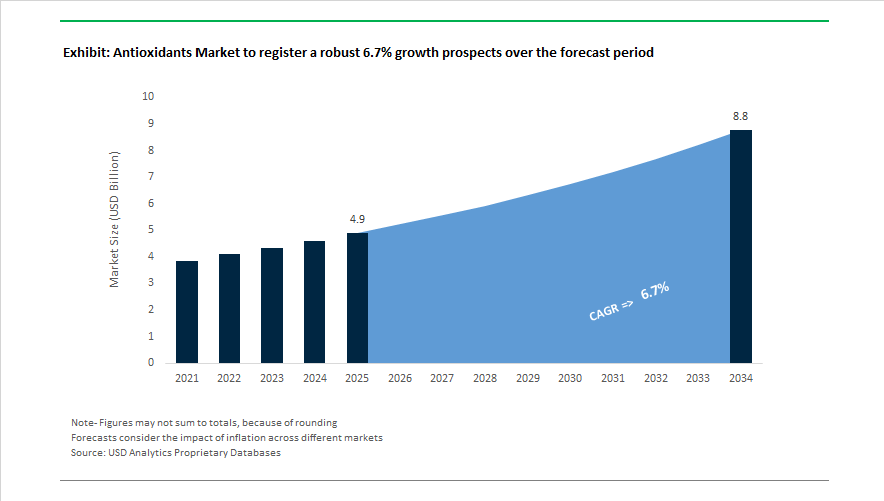

The antioxidants market is valued at $4.9 billion in 2025 and is forecast to reach $8.8 billion by 2034, registering a 6.7% CAGR. Growth is anchored in expanding applications across food antioxidants, feed antioxidants, polymer stabilizers, lubricant antioxidants, personal care actives, and shelf-life extension technologies. Structural momentum intensified in May 2024 when Songwon Industrial launched SONGNOX® 9228, a secondary phosphite antioxidant for polyolefins and engineering resins that enhances thermal stability and color retention in high-temperature plastic processing. In September 2024, Syensqo introduced the Riza™ antioxidant range for food and feed premixes, supporting formulation flexibility across liquid and powder systems. Portfolio integration expanded further in June 2024 when Camlin Fine Sciences acquired Vitafor Invest NV in Belgium, strengthening its presence in the European animal nutrition antioxidant segment.

Industrial lubricant stabilization and polymer protection demand accelerated in March 2025 as BASF invested in expanding aminic antioxidant capacity at its Puebla, Mexico site, with completion targeted for 2026 to support high-stability engine oils and industrial lubricants. Feed and pet nutrition became a central growth engine during October 2025 when dsm-firmenich opened a fully automated premix facility in Kansas focused on antioxidant-rich formulations. The shift toward natural and label-friendly solutions strengthened in October 2025 as Kemin Industries introduced OLESSENCE™ G Liquid to prevent oxidation in sauces and dips, aligning with European clean label demand. Sustainability leadership deepened in December 2025 when Kemin confirmed major progress in its rosemary supply program, securing large-scale natural carnosic acid sourcing.

Market consolidation and performance ingredient innovation continued through 2025–2026. Brenntag and BTSA presented an organic-certified antioxidant portfolio in September 2025, targeting rendering and pet food sectors with tocopherols and rosemary extracts. Givaudan expanded PlanetCaps™ encapsulation to personal care in November 2025, enabling oxidation-sensitive actives to maintain efficacy. ADM reported 8% nutrition segment growth in February 2026, supported by antioxidant blend demand in feed. Feedworks USA added a natural polyphenol blend in March 2025. By December 2025, Camlin Fine Sciences completed European restructuring to focus on high-growth shelf-life solutions.

Trends and Opportunities Reshaping Antioxidant Strategy, Margin Pools, and Technology Roadmaps

Market Trend: High-Molecular-Weight Antioxidants Becoming the Default Specification for Medical, Packaging and Lubricant Markets

Across 2025, regulatory tightening has shifted antioxidants from being commodity stabilizers to engineered specification-critical additives. Medical-grade and food-contact applications now require "anchored" antioxidant chemistries that never migrate from the polymer matrix.

In August 2025, Clariant expanded production capacity in China to commercialize AddWorks® LXR 548, a phenol-free solution engineered for gamma-sterilized medical plastics such as IV drip bags and disposable syringes. Its formulation is designed to maintain color stability and prevent extractables, supporting regulatory dossiers under FDA MoCRA and ISO-10993.

Packaging players are similarly upgrading. Under EU Annex V and U.S. MoCRA-aligned requirements active in 2025, low-extractability stabilizers became mandatory for flexible food-contact packaging. This has pushed adoption of graftable Hindered Phenolic Antioxidants (HPAO) which bind chemically to polyethylene and polypropylene backbones, cutting additive migration by up to 90% versus legacy BHT or low-molecular-weight phenols.

High-molecular-weight antioxidants are also becoming a core enabler for modern engine fluids. BASF’s March 2025 aminic antioxidant expansion in Puebla, Mexico targets high-temperature automotive lubricants used in hybrid and turbocharged engines, where oxidative sludge formation directly impacts OEM warranty claims.

Market Trend: One-Pack Systems and Multi-Functional Antioxidants Restructuring Cost Economics

Manufacturers are consolidating additive systems to reduce logistics, dosing errors and reformulation timelines. The shift is toward One-Pack Systems (OPS) that integrate antioxidants, HALS UV stabilizers and antistatic agents into a single pelletized feedstock.

SONGWON’s October 2025 OPS investment in Saudi Arabia positions the Gulf as a supply anchor for polymer converters, providing 100% active dispersions that improve compounding accuracy and downstream consistency.

In performance construction polymers, multifunctional stabilizers are being used to expand product lifecycles and extend maintenance windows. AddWorks® IBC 760, showcased in March 2025, increased the service life of Silyl Modified Polymer coatings by approximately 50 percent, reaching 3,000 hours in accelerated weathering protocols without yellowing.

Agricultural film manufacturers are also upgrading. HALS + phosphite combinations released in 2025 deliver 20% longer film longevity under sulfur-based pesticide exposure, directly improving greenhouse ROI metrics for growers.

Market Opportunity: Antioxidant Stabilizers for Lithium-Ion Battery Cells and High-Voltage Components

The electrification economy is generating a non-cyclical demand stream for antioxidant systems that protect cell components under thermal, oxidative and electrochemical stress.

Polymeric separators made of PP and PE degrade during high-amp charging cycles. By integrating thiodipropionate secondary antioxidants, suppliers are maintaining membrane integrity at temperatures exceeding 80°C, improving charge-cycle durability in EV-grade cells.

Electrolytes are another emerging margin pocket. Research at UNIST has shown that adding 1% malonic-acid decorated fullerene suppresses LiPF6 hydrolysis, blocking generation of hydrofluoric acid and boosting cycle life by over 15%.

The shift toward 800V EV platforms requires stabilizers that remain effective beyond 4.3V electrode potentials, a specification now under priority development by specialty chemical innovators as OEMs move to solid-state and high-voltage chemistries.

Market Opportunity: Tailored Antioxidants for Recycled and Bio-Based Polymer Circularity

Recycling and sustainability mandates are creating a stabilization problem that legacy additives cannot solve. Post-consumer recycled resin often contains metal catalysts, chain scission defects and oxidative residues and must be chemically "re-stabilized" before re-extrusion.

At NPE 2024/2025, SONGWON introduced SONGNOX® binary blends engineered to restore melt-flow consistency of recycled PE and PP, preventing radical-induced brittleness across second and third melt cycles—critical for achieving brand-owner PCR targets above 30%.

Bio-polymers present a separate challenge. PLA and PHA degrade thermally during extrusion. A 2024/2025 ACS Omega publication demonstrated that polyphenol extracts from grape marc and pomegranate improve PLA oxidative stability while supporting upcoming EU circularity directives calling for "fully bio-based plastic systems."

Chemical recycling operators are now requesting antioxidants formulated to stabilize pyrolysis oil during transport and intermediate storage. Without stabilization, oils polymerize into gums, preventing reintegration into steam crackers. This niche represents a premium-price segment where formulation expertise determines contract wins.

Antioxidants Market Share and Segmentation Insights

Market Share by Type: Synthetic Antioxidants Retain 68% Share as Natural Alternatives Gain Premium Momentum

Synthetic antioxidants command approximately 68% of the global antioxidants market in 2025, driven by their unmatched thermal stability, high radical-scavenging efficiency, and superior cost-performance in plastics, rubber, and lubricant formulations. Primary antioxidants (hindered phenolics such as BHT, BHA, and Irganox 1010) neutralize free radicals, while secondary antioxidants (phosphites and thioesters like tris(2,4-di-tert-butylphenyl) phosphite and dilauryl thiodipropionate) decompose hydroperoxides during melt processing. These chemistries are indispensable for polymer stabilization in PE, PP, ABS, and tire compounds. Natural antioxidants represent the fastest-growing segment, fueled by clean-label food, cosmetic premiumization, and regulatory pressure on synthetic preservatives. Tocopherols (vitamin E) lead, followed by rosemary extract, ascorbic acid, and botanical extracts. Despite commanding 2 to 5x higher pricing and lower heat resistance, natural antioxidants are rapidly penetrating food, feed, and personal care, where sustainability credentials outweigh processing constraints.

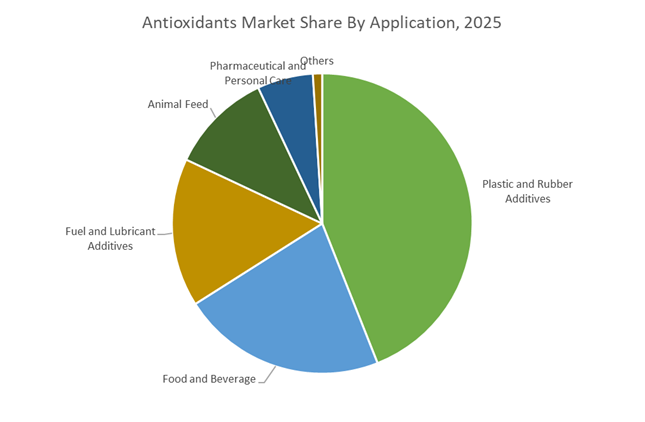

Market Share by Application: Plastics and Rubber Lead at 44% as Food and Lubricants Drive Diversified Growth

Plastic and rubber additives account for roughly 44% of antioxidant consumption in 2025, reflecting the critical role of phenolic antioxidants and phosphite processing stabilizers in preventing thermal-oxidative degradation during extrusion and injection molding. Demand is anchored by packaging, automotive components, construction materials, and wire and cable insulation. Food and beverage ranks second, with TBHQ, BHA, BHT, and propyl gallate protecting frying oils and processed foods, while tocopherols and rosemary extract power clean-label growth in premium products. Fuel and lubricant additives rely on diphenylamine (DPA), PAN, and hindered phenolics to prevent sludge formation and viscosity rise; EV adoption will reduce engine oil volumes but increase demand for advanced thermal management fluids. Animal feed uses ethoxyquin, BHT, and tocopherols, with EU restrictions accelerating natural substitution, especially in aquaculture. Pharmaceutical and personal care remain high-margin niches, led by USP-grade BHT and vitamin E. Asia-Pacific dominates volume, while Europe and North America lead natural antioxidant adoption.

Antioxidants Market Competitive Landscape

The global antioxidants market is characterized by dual-track demand for synthetic performance stabilizers and clean-label natural antioxidants, driven by plastics durability requirements, EV lubricants, food shelf-life extension, and cosmetic anti-aging applications. Competition increasingly centers on mass-balance certified production, plant-based extracts, validated product carbon footprints (PCF), and vertically integrated agricultural sourcing. Leading manufacturers are differentiating through ISCC PLUS compliance, multifunctional antioxidant systems, AI-driven shelf-life modeling, and localized blending hubs, while customers prioritize traceability, regulatory readiness, and low-carbon supply chains. Market leadership is now defined by the ability to deliver high-efficacy oxidative stability across food, polymers, fuels, and personal care, supported by ESG-aligned manufacturing and application-specific innovation.

Mass-balance antioxidants and Verbund-driven scale leadership by BASF SE

BASF remains the dominant global supplier of industrial and food-grade antioxidants, leveraging its Verbund integration to deliver sustainability-certified additives at scale. Its Irganox® and Irgastab® portfolios anchor polymer stabilization, while GLYSANTIN®-aligned additives support lubricant performance, including the Irgastab® PUR 71 anti-scorch solution for polyurethane foams. In March 2025, BASF expanded aminic antioxidant capacity at its Puebla, Mexico site to meet rising automotive lubricant demand. Through its VALERAS® platform, BASF now provides validated Product Carbon Footprints for core antioxidants. Strategically, the company is transitioning Kaisten and McIntosh facilities to ISCC PLUS renewable feedstocks, accelerating its mass-balance transformation.

Plant-based antioxidant leadership powered by agri-integration at Archer Daniels Midland

ADM leads the natural antioxidants segment by converting its vast agricultural supply chain into clean-label preservation solutions. The company dominates food, beverage, and animal nutrition applications with rosemary, tocopherols, and green tea extracts that replace synthetic preservatives. In preparation for 2026, ADM announced a joint venture with Alltech focused on next-generation nutrition and biosolutions. Recent innovations include concentrated plant-derived antioxidant blends and novel pigments for snacks and bakery. ADM’s strategic focus centers on decarbonization and byproduct valorization, transforming agricultural side-streams into high-value antioxidant extracts, reinforcing its position as a circular-economy pioneer in natural shelf-life extension.

Seed-to-shelf antioxidant consistency delivered by Kemin Industries

Kemin differentiates through full vertical integration, controlling antioxidant potency from proprietary crop genetics to finished ingredients. Its Specialty Crop Improvement program manages clonal rosemary and spearmint lines to ensure consistent carnosic acid levels. The FORTIUM® R range is widely used to preserve color and flavor in meat and poultry without BHA or BHT. In late 2025, Kemin expanded its antioxidant platform into bakery and textile auxiliaries, broadening beyond pet food. Guided by its Blueprint for Sustainable Agriculture, Kemin is scaling perennial cropping systems across the US and APAC to protect supply continuity against climate-driven raw material volatility.

Multifunctional antioxidant systems engineered by International Flavors & Fragrances

IFF integrates antioxidants with flavor and scent stabilization, positioning preservation as part of holistic product performance. Its GUARDIAN® natural extracts and GRINDOX® solutions serve high-fat matrices, while GUARDIAN® AQUAROX™ delivers upcycled-certified rosemary protection for beverages. Recent innovations include SYNEROX for Frying, extending oil life while improving sensory quality. IFF leverages a proprietary Rancimat database spanning thousands of oil tests to provide AI-driven shelf-life predictions. Under its Wholistic Health strategy, the company frames antioxidants as tools for reducing food waste, supporting minimally processed products, and enabling sustainable consumption across global food systems.

Synthetic antioxidant scale combined with clean-label expansion at Camlin Fine Sciences

Camlin Fine Sciences is the world’s largest integrated producer of traditional synthetic antioxidants, while rapidly expanding into natural extracts. It leads global TBHQ and BHA supply through its Xtendra portfolio, complemented by NaSure natural solutions, offering over 100 shelf-life products for snacks, pet food, and biodiesel. With blending facilities across Brazil, Mexico, the USA, China, and India, CFS operates a localized manufacturing model for custom antioxidant formulations. In 2025–2026, the company achieved full traceability across aroma and antioxidant production. Its backward integration into guaiacol and catechol underpins its status as the lowest-cost high-purity TBHQ producer.

Botanical efficacy and active beauty antioxidants advanced by Givaudan

Following the Naturex acquisition, Givaudan has become a premium supplier of botanical antioxidants for cosmetics and functional nutrition. In late 2025, it launched microbiome-safe antioxidants for personal care, preserving formulations without disrupting beneficial skin bacteria. Strategically focused on Active Beauty, Givaudan is shifting antioxidants from passive preservation toward active cellular protection against environmental oxidative stress. Its polyphenol and carotenoid solutions are widely adopted in cosmeceuticals and wellness beverages, enabling “beauty-from-within” positioning. Through global co-creation centers, Givaudan tests antioxidant performance directly within customer flavor and fragrance systems, accelerating development of high-end, efficacy-driven applications.

Mexico Antioxidants Market: Lubricant-Centric Capacity and North American EV Corridor Alignment

Mexico is strengthening its position as a strategic antioxidants manufacturing base for North America, driven by lubricant and polymer additive demand. In March 2025, BASF SE announced a major capital investment to expand aminic antioxidant production at its Puebla facility, with operations scheduled to come fully online by early 2026. This expansion is tightly aligned with demand from high-temperature lubricant formulations, particularly those used in next-generation drivetrains and thermal management fluids.

The Puebla site benefits from direct integration into the North American EV supply chain, supplying antioxidants engineered for oxidative stability under extreme thermal loads. Beyond lubricants, Mexico’s role as a regional export hub for the U.S. and Canada is influencing packaging innovation. Mexican film producers are increasingly adopting time-release antioxidant systems to protect flexible food packaging during cross-border transit. Complementing this shift, Avient Corporation launched its Hiformer Non-PFAS Process Aid with integrated antioxidant functionality in January 2026, enabling PE and PP processors to meet tightening non-fluorinated material requirements.

India Antioxidants Market: Import Substitution, Clean-Label Enforcement, and Polymer Additive Scale-Up

India’s antioxidants landscape is defined by import substitution and regulatory-driven formulation changes. In late 2024, Clean Fino-Chem, a subsidiary of Clean Science and Technology, began commercial-scale production of Butylated Hydroxy Toluene (BHT). This development significantly reduces reliance on imported synthetic antioxidants used across food, cosmetics, and plastics.

Regulation has become a primary demand catalyst. The Food Safety and Standards Authority of India implemented the 2025 Additive Safety Compendium, enforcing strict labeling and usage differentiation between natural and synthetic antioxidants. This has accelerated adoption of rosemary extracts and tocopherol-based systems in retail food and nutraceutical products. On the industrial side, the Gujarat chemical corridor commissioned new plants in 2025 dedicated to hindered amine light stabilizers and antioxidant blends, supporting domestic automotive and construction polymers. Parallel government incentives under Make in India and nutraceutical export programs are also driving R&D into botanical antioxidants such as curcumin and polyphenols.

United States Antioxidants Market: Research-Driven Nutraceuticals and Bio-Based Procurement Standards

In the United States, the antioxidants industry is being shaped by federal research funding and sustainability-focused procurement. The National Institutes of Health Office of Dietary Supplements released its Strategic Plan FY 2025–2029, allocating funding to study antioxidants’ role in human resilience and lifespan. This is directly influencing innovation pipelines in premium nutraceuticals and clinical-grade antioxidant formulations.

Policy alignment is equally important. Updated federal procurement guidelines in mid-2025 now prioritize bio-based antioxidant additives in lubricants used for government-contracted machinery, favoring plant-derived tocopherols. In late 2024, Louis Dreyfus Company introduced new non-GMO, plant-based Vitamin E derivatives for pharmaceutical and functional food applications. Additionally, the implementation of PRIA 5 in 2025 has significantly reduced approval timelines for antimicrobial-antioxidant synergistic coatings used on food-contact surfaces, accelerating commercialization of multifunctional protection systems.

China Antioxidants Market: Environmental Consolidation and High-Performance Materials Focus

China’s antioxidants sector is undergoing consolidation under environmental governance rather than capacity expansion. In line with the 14th Five-Year Plan updates, 2025 environmental audits concentrated synthetic antioxidant production into five designated Green Chemical Zones, reducing hazardous effluent and raising compliance thresholds for BHA and BHT manufacturers.

Demand-side pull is coming from advanced materials. China’s rapid solar energy expansion has increased the use of antimony trioxide and specialty antioxidant fining agents to enhance optical clarity and UV resistance in photovoltaic glass. At the same time, SI Group expanded production of ETHANOX™ 4716 and NAUGARD™ PS48 at its Jinshan facility to serve high-performance plastics in automotive, electronics, and infrastructure applications across Asia-Pacific.

Japan Antioxidants Market: Fuel Stability Solutions and Precision Cosmetics Innovation

Japan’s antioxidants industry is closely tied to fuel stability and high-end consumer applications. In May 2025, NYK Group launched BioxiGuard, a specialized antioxidant designed to prevent oxidation in marine biodiesel during long-haul shipping. Commercial availability from August 2025 supports Japan’s broader decarbonization and alternative fuel logistics strategy.

In parallel, cosmetics innovation is driving antioxidant differentiation. Leading brands such as Shiseido and Kose reported a 2025 shift toward slow-release, nano-encapsulated antioxidant serums. These formulations maintain Vitamin C stability for over 24 hours, reflecting Japan’s emphasis on precision delivery and performance longevity in skincare.

Country-Level Strategic Positioning in the Antioxidants Industry

Antioxidants Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Industry Impact

|

|

Mexico

|

Aminic antioxidants for lubricants

|

EV drivetrain fluids and regional packaging exports

|

|

India

|

Import substitution and clean-label shift

|

Food, nutraceuticals, and polymer additives

|

|

United States

|

Research-backed and bio-based systems

|

Premium nutraceuticals and sustainable lubricants

|

|

China

|

Environmental consolidation

|

High-performance plastics and solar glass

|

|

Japan

|

Fuel stability and precision cosmetics

|

Marine biofuels and advanced skincare

|

Antioxidants Market Report Scope

Antioxidants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.9 Billion

|

|

Market Size (2034)

|

$8.8 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Type (Natural Antioxidants, Synthetic Antioxidants), By Form (Dry, Liquid), By Source (Petroleum Derived, Plant Based, Biotechnology Derived), By Application (Food and Beverage, Fuel and Lubricant Additives, Plastic and Rubber Additives, Pharmaceutical and Personal Care, Animal Feed)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Archer Daniels Midland Company, Cargill Incorporated, DSM-Firmenich AG, Eastman Chemical Company, Givaudan, Kemin Industries Inc, Camlin Fine Sciences Ltd, Barentz International BV, Aland Nutraceutical, Naturex SA, SI Group Inc, Evonik Industries AG, Avient Corporation, Kalsec Inc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Antioxidants Market Segmentation

By Type

- Natural Antioxidants

- Synthetic Antioxidants

By Form

By Source

- Petroleum Derived

- Plant Based

- Biotechnology Derived

By Application

- Food and Beverage

- Fuel and Lubricant Additives

- Plastic and Rubber Additives

- Pharmaceutical and Personal Care

- Animal Feed

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Antioxidants Industry

- BASF SE

- Archer Daniels Midland Company

- Cargill Incorporated

- DSM-Firmenich AG

- Eastman Chemical Company

- Givaudan

- Kemin Industries Inc

- Camlin Fine Sciences Ltd

- Barentz International BV

- Aland Nutraceutical

- Naturex SA

- SI Group Inc

- Evonik Industries AG

- Avient Corporation

- Kalsec Inc

*- List not Exhaustive