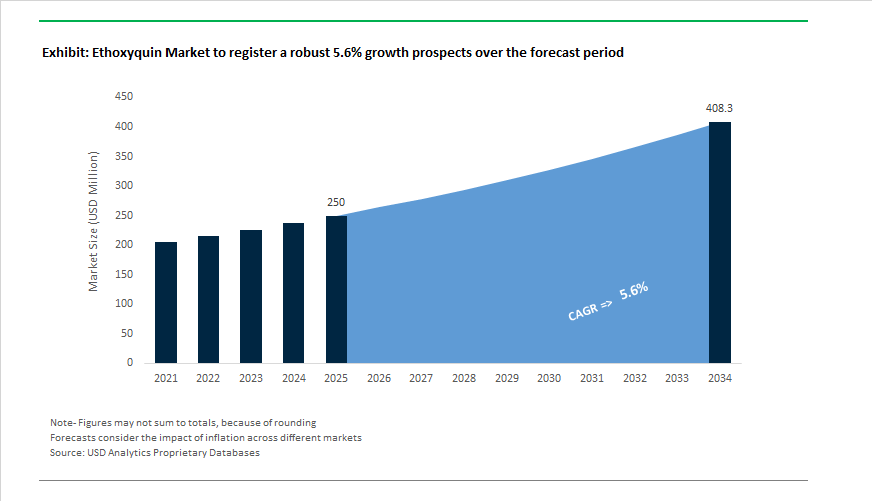

Ethoxyquin Market to Reach $408.2 Million by 2034 Amid Regulatory Fragmentation and Shift Toward Natural Antioxidants

The Ethoxyquin Market is projected to expand from $250 Million in 2025 to $408.2 Million by 2034, registering a CAGR of 5.6%. Historically used as a synthetic antioxidant in animal feed, aquaculture, pet food, and select pharmaceutical stabilization applications, ethoxyquin is undergoing structural transformation due to regulatory divergence and consumer-driven reformulation pressures. The global market is now characterized by a sharp geographic split: continued utilization in North America and select emerging economies versus accelerated phase-outs across Europe and parts of Africa.

A major regulatory inflection point occurred in May 2025 when Nigeria’s National Agency for Food and Drug Administration and Control (NAFDAC) implemented a full ban on ethoxyquin in feed for food-producing animals. The directive, effective May 20, 2025, cited concerns about residue transfer into poultry, eggs, and fish. This decision has had ripple effects across West Africa, where exporters increasingly require ethoxyquin-free certifications to maintain trade flows. In contrast, the U.S. Food and Drug Administration reaffirmed in April 2024 that ethoxyquin remains permitted in U.S. animal feed under Title 21 CFR, capped at 150 ppm. This regulatory reaffirmation stabilized North American feed formulations, although consumer brands continue to pivot toward natural tocopherols and rosemary extracts to maintain premium positioning.

The European regulatory landscape tightened further in January 2026 when the European Commission introduced a revised risk-based evaluation framework for feed additives and pesticide co-formulants. Although ethoxyquin was already banned as a feed additive in the EU, the updated system accelerates scrutiny on chemically related antioxidants, effectively forcing multinational feed and aquaculture players to validate alternative preservation systems. As a result, large distributors such as Brenntag, in partnership with BTSA, showcased organic antioxidant portfolios in September 2025 positioned as direct replacements for ethoxyquin, BHA, and BHT. These solutions are gaining traction in pet food and rendering segments seeking clean label credentials ahead of anticipated 2026 compliance shifts.

Corporate strategy across the value chain reflects this transition. Nutreco, through its Skretting division, launched next-generation shrimp feeds in October 2025 engineered for oxidative stability without suspended synthetic antioxidants. Meanwhile, Syensqo introduced its Riza antioxidant range in 2024, targeting food and feed customers requiring high thermal stability but compliant with stricter 2025–2026 safety frameworks. In the United States, Feedworks USA introduced the Elife natural polyphenol blend in March 2025, directly responding to premium livestock producers seeking synthetic-free preservation solutions.

China remains a critical production and export hub. By early 2025, ethoxyquin capacity consolidated among major producers such as Jiangsu Litian Technology and Jiangsu Zhongdan Group, each operating approximately 10,000 tons of annual output. However, Chinese feed mills face mounting pressure from global seafood retailers demanding ethoxyquin-free labeling, particularly for fishmeal imports from Peru. This has triggered a gradual substitution toward BHT and natural tocopherols in export-oriented aquaculture supply chains.

The pharmaceutical and excipient niche remains comparatively stable. Roquette’s acquisition of IFF Pharma Solutions in May 2025 strengthened its position in high-purity antioxidant stabilization systems used in vitamin preservation and select pharmaceutical applications. These specialized segments continue to value ethoxyquin’s oxidation control performance under controlled dosage conditions.

Trends and Opportunities in the Ethoxyquin Market

Mandatory Regulatory Phase-Out Across Global Animal Feed Supply Chains

- The regulatory phase-out of ethoxyquin in animal feed has moved from policy intent to active enforcement, fundamentally altering global feed additive trade flows. Under Regulation (EU) 2022/1375, the European Union’s prohibition of ethoxyquin as a feed antioxidant is now fully implemented. By mid-2025, customs authorities across the EU began rejecting fishmeal and fish oil imports that could not demonstrate ethoxyquin-free status, forcing exporters in Latin America and Southeast Asia to reformulate preservation systems at the origin level.

- This enforcement has triggered a global substitution cycle. Leading aquaculture nutrition companies such as Skretting, operating under Nutreco’s RoadMap 2025, have completed a full transition to natural-origin antioxidant systems. In October 2025, Skretting introduced its Necto health diet range, built around proprietary phyto-complexes rather than synthetic antioxidants, effectively setting a new benchmark for clean-label aquafeed formulations.

- In the United States, ethoxyquin remains technically permitted at restricted levels under FDA guidance, including limits of 150 ppm in poultry feed. However, commercial pressure from integrators and retailers has accelerated voluntary reduction. By late 2025, a growing share of U.S. feed producers had shifted to blended antioxidant systems combining butylated hydroxytoluene and natural tocopherols, primarily to mitigate bioaccumulation risk perceptions and safeguard export eligibility into ethoxyquin-restricted markets.

Strategic Consolidation and Pivot Toward High-Value Specialty Blends

- As feed-related demand contracts, ethoxyquin producers are consolidating operations and redirecting capital toward higher-margin specialty antioxidant blends and technical applications. In June 2024, Camlin Fine Sciences acquired Vitafor Invest NV, a strategic move aimed at accelerating its transition away from commodity-grade ethoxyquin. By Q2 FY2026, the company reported approximately 8% growth in its blends and specialty solutions segment, even as traditional feed antioxidant volumes declined.

- At the production level, merchant capacity is increasingly concentrated in technical-grade Ethoxyquin-95 Oil, supplied to industrial customers where regulatory exposure is lower and inclusion levels are tightly controlled. Producers are investing in improved distillation and purification systems to meet the needs of these applications, where consistency, oxidative performance, and trace impurity control matter more than bulk pricing.

- This consolidation is reshaping the competitive landscape. Smaller, feed-focused producers are exiting the market, while diversified antioxidant suppliers are integrating ethoxyquin into broader performance packages that combine multiple stabilizers to meet application-specific requirements.

Stabilization of High-Performance Synthetic Lubricants Under Extreme Thermal Loads

- One of the most resilient growth avenues for ethoxyquin lies in its role as a high-efficiency antioxidant for synthetic lubricants and industrial fluids exposed to severe thermal and oxidative stress. Industrial performance studies conducted during 2024–2025 consistently highlight ethoxyquin’s superior radical scavenging capability, driven by intramolecular resonance stabilization that suppresses oxidation chain reactions in ester- and lipid-based fluids.

- In synthetic lubricant base stocks, ethoxyquin has demonstrated superior protection against viscosity breakdown and sludge formation compared with conventional aromatic amines, particularly under sustained high-temperature operation. This makes it attractive for industrial gear oils, turbine lubricants, and specialty aviation fluids where extended drain intervals and oxidation stability directly influence lifecycle cost.

- The rapid expansion of electric vehicle thermal management systems further reinforces this opportunity. As EV platforms increasingly rely on synthetic ester-based coolants and lubricants, the need for antioxidants that can protect these fluids at low treat rates becomes critical. Ethoxyquin’s effectiveness at minimal inclusion levels positions it as a cost-efficient stabilizer for long-service-life formulations, particularly in applications where fluid replacement is complex or expensive.

Preservation of Oxygen-Sensitive Bio-Actives in Pharmaceutical and Technical Processing

- A second high-value niche is emerging for ultra-pure ethoxyquin used as a process aid in the stabilization of oxygen-sensitive intermediates. In pharmaceutical manufacturing, ethoxyquin continues to play a critical role during the synthesis and concentration of lipid-rich vitamins and carotenoids. An August 2025 lipid oxidation study confirmed that ethoxyquin remains among the most effective inhibitors of hydroperoxide decomposition during the processing of vitamin A, vitamin E, and carotenoid intermediates.

- Importantly, in these applications ethoxyquin is not present in the final dosage form. Instead, it is used transiently during processing and subsequently removed or reduced to non-detectable levels, allowing manufacturers to preserve product integrity without compromising regulatory or labeling requirements.

- A similar model is emerging in the luxury cosmetics supply chain. Producers of high-value botanical extracts are increasingly using refined ethoxyquin to stabilize sensitive raw materials during long-distance transport. By confining its use to intermediate stages, manufacturers can ensure potency retention of bio-actives while delivering final consumer products that remain aligned with clean-label and natural positioning.

Ethoxyquin Market Share and Segmentation Insights

Feed Grade Ethoxyquin Anchors Antioxidant Demand Across Livestock and Aquaculture Supply Chains

Feed grade ethoxyquin commands 72% of total market share in 2025, driven by its critical role in preserving fats, proteins, and fat-soluble vitamins in compound feed for poultry, swine, and ruminants. Its proven antioxidant performance prevents oxidative rancidity during storage and long-distance transport, safeguarding nutritional value and feed palatability while reducing waste across global feed operations. Low p-phenetidine grade represents a high-purity, premium segment, increasingly specified in pet food and aquaculture feed as manufacturers respond to tighter regulatory scrutiny and consumer expectations for cleaner ingredient profiles. This grade supports extended shelf life for oil-rich formulations, particularly in salmon and shrimp diets. Industrial grade remains a niche category, supplying rubber stabilization, pesticide formulations, and specialty antioxidant applications where pharmaceutical-level purity is unnecessary but oxidation control is essential for material integrity and product performance.

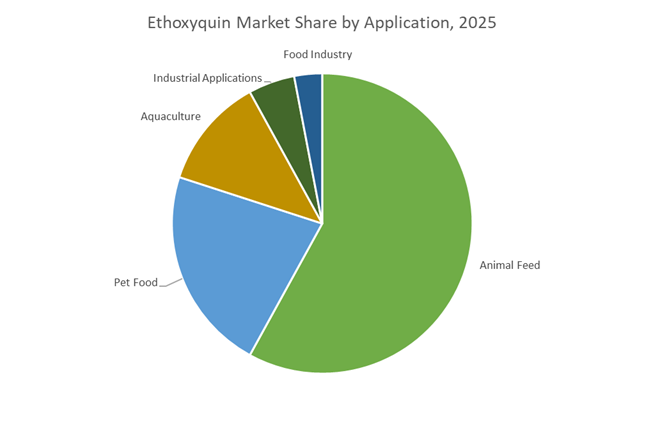

Animal Feed Drives the Majority of Ethoxyquin Consumption Worldwide

Animal feed accounts for 58% of global ethoxyquin demand in 2025, reinforcing its position as the primary application segment. Feed producers rely on ethoxyquin to stabilize vitamin A, D, and E and prevent lipid oxidation in rendered meals and oil-rich ingredients prior to consumption. Pet food follows as a major growth area, with premium brands increasingly adopting low p-phenetidine grades to maintain fat quality in dry and semi-moist formulations. Aquaculture represents an important segment, where ethoxyquin preserves highly unsaturated fish oils essential for marine species nutrition, supporting feed acceptance and growth performance. Industrial applications maintain steady demand across rubber processing and agrochemical stabilization. Food industry usage remains limited due to regulatory constraints, though select applications persist in spices and specialty ingredients where antioxidant protection is still permitted.

Competitive Landscape of the Ethoxyquin Market

The global ethoxyquin market in 2026 is shaped by vertical integration, regulatory divergence between regions, and rapid innovation in feed antioxidants, with leading players balancing synthetic ethoxyquin portfolios alongside natural and hybrid antioxidant systems for aquaculture, poultry, and food stability.

Camlin Fine Sciences drives ethoxyquin leadership through full vertical integration and specialty ingredients

Camlin Fine Sciences Ltd. stands out as the only fully integrated ethoxyquin manufacturer globally, controlling production from hydroquinone and catechol through finished antioxidant blends. In Q3 FY26, Camlin reported consolidated revenue of ₹457.2 crores, with Specialty Ingredients contributing 56%, highlighting its shift toward higher-margin value-added blends. During late 2025 and early 2026, the company acquired a controlling stake in Vinpai (France), diversifying into natural functional ingredients to mitigate regulatory risk tied to synthetic antioxidants. Its 2026 R&D-to-market launches focus on aroma ingredients and emulsifier-based stability solutions, reinforcing Camlin’s position across feed preservation, food antioxidants, and specialty chemical applications.

Kemin Industries advances low-dose ethoxyquin with patented encapsulation technologies

Kemin Industries, Inc. anchors the science-led segment of the ethoxyquin market through proprietary delivery systems that dramatically reduce required inclusion rates. Between 2024 and 2025, Kemin secured multiple patents for encapsulation and nanocarrier platforms, enabling ethoxyquin efficacy below 50 ppm, far under traditional 150 ppm benchmarks. Its Termox™ and Endox™ brands are now positioned as hybrid antioxidant systems, blending ethoxyquin with natural extracts such as rosemary to meet varying global compliance standards. Supported by Customer Laboratory Services for real-time oxidative testing, Kemin continues expanding innovation hubs in South Asia and Brazil to capture 2026 growth in APAC aquaculture and Latin American poultry nutrition.

Impextraco builds synergistic ethoxyquin blends for extended feed shelf life

Impextraco N.V. operates as a specialist feed additive supplier, offering IMPEXQUIN® (99% liquid and 66.6% powder) alongside FEEDOX® synergistic blends combining ethoxyquin and BHA. With R&D centers in Belgium and Brazil, Impextraco serves both EU markets transitioning away from ethoxyquin and South American regions where ethoxyquin remains dominant. In 2025 and 2026, the company emphasized “antioxidant regeneration,” designing formulations that recycle antioxidant molecules and extend fishmeal shelf life by up to 20%. While maintaining global ethoxyquin sales, Impextraco is simultaneously promoting FEEDOX® NE as a one-to-one non-ethoxyquin replacement for manufacturers preparing for tighter regulations.

Novus International protects high-value lipids with the globally trusted SANTOQUIN brand

Novus International, Inc. remains a cornerstone of ethoxyquin usage in livestock and aquaculture through its long-established SANTOQUIN® portfolio. The company’s strategy centers on preserving nutritional integrity, particularly safeguarding omega-3 rich fishmeal during long-distance shipping where ethoxyquin prevents oxidative degradation and spontaneous combustion. In 2025 and 2026, Novus strengthened its Global Regulatory & Compliance unit to guide customers through updated maximum residue limits across the US and Japan. Its deep expertise in carotenoid and vitamin stabilization ensures expensive pigments and fat-soluble nutrients retain potency, reinforcing Novus’ relevance in premium poultry feed and aquaculture antioxidant solutions.

BASF pivots toward post-ethoxyquin stabilization with advanced carotenoid technologies

BASF SE has repositioned itself for the post-ethoxyquin era, proactively removing ethoxyquin from its vitamin and carotenoid systems in response to EU restrictions. The company now favors high-performance BHT and propyl gallate combinations, complemented by its Lucantin® stabilized carotenoid series launched in 2025 using proprietary beadlet technology. In February 2026, BASF expanded its specialty ingredients footprint in Brazil through a strategic partnership with Caldic, targeting sustainable and high-performance formulations. Its global standardization strategy aims to deliver single vitamin formulations compliant with the strictest regulations worldwide, simplifying multinational supply chains while maintaining antioxidant stability.

China: Scale Leadership Under Rising Export and Food-Safety Scrutiny

China remains the structural backbone of the global ethoxyquin supply chain in 2025, with production concentrated in specialized chemical parks across Zhejiang and Jiangsu that directly serve the country’s vast swine, poultry, and aquaculture feed sectors. As of 2025, China accounts for more than 21.7% of global ethoxyquin output, reinforcing its role as the primary price and volume setter for this antioxidant. Capacity advantages are increasingly complemented by process sophistication. BASF integrated advanced Controlled Free Radical Polymerization technology into its Nanjing specialty chemicals expansion in late 2025, creating a localized benchmark for high-performance stabilizers and dispersants used in industrial coatings and feed additive formulations.

Export-facing quality compliance has become a defining theme. In response to tightening international scrutiny around p-phenetidine residues, Chinese producers such as Jiaxing Jinyan implemented low-p-phenetidine protocols in 2025 to retain access to non-EU destinations including Japan and Southeast Asia. Regulatory oversight is also intensifying domestically. The Ministry of Agriculture and Rural Development launched a 2026 surveillance program focused on antioxidant residues in aquaculture, signaling China’s intent to align feed safety practices with international trade expectations rather than purely internal demand growth.

Vietnam: Aquaculture-Led Phase-Out and Bio-Based Replacement Momentum

Vietnam’s ethoxyquin exposure is increasingly shaped by export dependency rather than domestic production. During 2025–2026, the Vietnam Association of Seafood Exporters and Producers intensified its Clean Feed campaign, testing more than 150 shrimp feed samples to eliminate ethoxyquin traces and safeguard access to premium EU seafood markets. This compliance-driven pivot reflects the sensitivity of Vietnam’s shrimp export economy to European feed additive regulations.

At the policy level, the Ministry of Agriculture and Rural Development convened a high-level summit in November 2025 aimed at reducing dependence on imported fishmeal stabilized with ethoxyquin, particularly from Peru. This has accelerated substitution toward natural antioxidants such as tocopherols. Infrastructure investment is following policy intent. Two large-scale bio-additive refineries scheduled for commissioning in the Mekong Delta in 2026 will focus on rice-bran-derived antioxidants, positioning Vietnam as an emerging regional hub for ethoxyquin alternatives rather than a downstream consumer of the synthetic compound.

United States: Regulatory Stability Coupled with Market-Led Reformulation

The United States presents a dual-track ethoxyquin landscape characterized by regulatory continuity and market-driven reformulation. In 2025, the U.S. Food and Drug Administration reaffirmed ethoxyquin’s status in the Inactive Ingredient Database and its limited authorization as a secondary direct food additive for specific applications such as color preservation in paprika. This decision preserves ethoxyquin’s legal use in poultry feed and pet food through 2026, maintaining its relevance as a cost-efficient antioxidant.

However, commercial dynamics are shifting faster than regulation. Major pet food brands are accelerating moves toward natural-preserved positioning, triggering a reported 30% increase in R&D spending on ethoxyquin-free stabilization systems during the 2025 fiscal year. On the supply side, BASF announced investments across its Puebla and North American affiliate sites in March 2025 to expand aminic antioxidant production, targeting lubricant and feed markets with higher stability requirements. This suggests that while ethoxyquin remains permitted, U.S. demand is gradually migrating toward alternative antioxidant chemistries.

European Union (Germany and Norway Focus): Enforcement-Driven Market Exit

The European Union represents the most restrictive regulatory environment for ethoxyquin. Under Commission Implementing Regulation (EU) 2022/1375, the compound was denied re-authorisation as a feed additive, and 2025–2026 has marked the transition from policy to enforcement. Zero-tolerance audits are now being applied to imported fishmeal and finished animal proteins, significantly constraining any residual ethoxyquin trade into EU member states.

In response, industry efforts are focused on replacement technologies rather than regulatory reversal. IFFO and European feed producers are investing in 2026 pilot programs for encapsulated antioxidant systems designed to replicate ethoxyquin’s role in preventing spontaneous combustion of fishmeal during maritime transport without generating p-phenetidine risk. Parallel to this, German chemical companies are reallocating assets away from ethoxyquin synthesis toward bio-attributed ethylene oxide derivatives and green surfactants, aligning with EU Green Deal objectives for a non-toxic chemical ecosystem by 2026.

India: Import Substitution and Downstream Chemical Diversification

India’s ethoxyquin profile is evolving through industrial policy rather than feed regulation. Under the Rs. 28,602 crore Production Linked Incentive scheme for specialty chemicals, domestic manufacturers are accelerating the localization of high-performance antioxidants with the explicit goal of reducing reliance on imported feed stabilizers by mid-2026. This policy support is strengthening India’s position as a competitive manufacturing base for antioxidant intermediates.

Beyond feed applications, ethoxyquin-derived intermediates are gaining traction in India’s rubber processing and agrochemical formulation sectors. The Department of Chemicals and Petrochemicals reported increased volumes of specialty amine exports in the third quarter of 2025, reflecting price-competitive production and diversified end-use demand. For India, the ethoxyquin value chain is therefore less about direct feed use and more about leveraging downstream chemical versatility within a protected domestic manufacturing framework.

Strategic Snapshot: Ethoxyquin Market by Country

Ethoxyquin Market County Level Snapshot

|

Country / Region

|

Regulatory Posture

|

Primary Driver

|

Strategic Direction

|

|

China

|

Controlled use with tighter surveillance

|

Feed scale and export compliance

|

Process upgrades and LPP protocols

|

|

Vietnam

|

Export-led restriction

|

EU seafood access

|

Rapid shift to bio-based antioxidants

|

|

United States

|

Permitted with market pressure

|

Pet food and lubricants

|

Gradual reformulation toward naturals

|

|

European Union

|

Prohibited in feed

|

Food safety enforcement

|

Full substitution and green chemistry

|

|

India

|

Neutral, policy-driven

|

Import substitution and intermediates

|

Domestic antioxidant manufacturing

|

Ethoxyquin Market Report Scope

Ethoxyquin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$250 Million

|

|

Market Size (2034)

|

$408.2 Million

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Grade (Feed Grade, Low p-Phenetidine Grade, Industrial Grade), By Application (Animal Feed, Aquaculture, Pet Food, Industrial Applications, Food Industry), By Function (Antioxidants, Anti-Scald Agents, Heat Stabilizers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Archer Daniels Midland Company, Cargill, Incorporated, Skretting, Kemin Industries, Inc., Jiaxing Jinyan Chemical Co., Ltd., Camlin Fine Sciences Ltd., Huntsman Corporation, Merck KGaA, China Petroleum & Chemical Corporation, Impextraco NV, UPL Limited, Vinh Hoan Corporation, Alltech, Inc., Perstorp Holding AB

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethoxyquin Market Segmentation

By Product Grade

- Feed Grade

- Low p-Phenetidine Grade

- Industrial Grade

By Application

- Animal Feed

- Aquaculture

- Pet Food

- Industrial Applications

- Food Industry

By Function

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethoxyquin Industry

- BASF SE

- Archer Daniels Midland Company

- Cargill, Incorporated

- Skretting

- Kemin Industries, Inc.

- Jiaxing Jinyan Chemical Co., Ltd.

- Camlin Fine Sciences Ltd.

- Huntsman Corporation

- Merck KGaA

- China Petroleum & Chemical Corporation

- Impextraco NV

- UPL Limited

- Vinh Hoan Corporation

- Alltech, Inc.

- Perstorp Holding AB

*- List not Exhaustive