Hydroquinone Market to Reach $14.9 Billion by 2034 at 5.8% CAGR Amid Supply Shocks, Regulatory Tightening, and Specialty Chemical Expansion

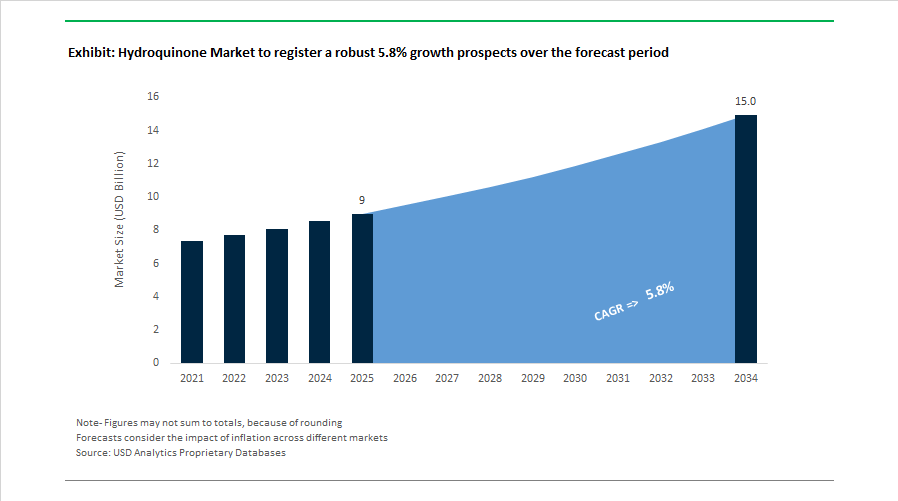

The Hydroquinone Market is projected to grow from $9 billion in 2025 to $14.9 billion by 2034, registering a CAGR of 5.8%. Market expansion is being shaped by increasing demand for hydroquinone in polymerization inhibitors, photographic chemicals, antioxidant intermediates such as TBHQ, dermatological formulations, and electronic-grade specialty chemicals. At the same time, regulatory tightening in cosmetics, geopolitical supply disruptions, and strategic corporate restructuring across Europe and Asia are redefining global supply chains for both industrial-grade and USP-grade hydroquinone.

In 2024, structural realignments and portfolio expansions reshaped competitive positioning. Following the late 2023 corporate split of Solvay, Syensqo emerged as an independent specialty chemicals player in 2024, managing high-growth hydroquinone applications in aerospace composites and electronic-grade materials. In June 2024, Camlin Fine Sciences (CFS) acquired Vitafor Invest NV in Belgium through its Mexican subsidiary, strengthening integration of hydroquinone-derived TBHQ antioxidants into European animal nutrition and food shelf-life stabilization markets. During the same year, Eastman Chemical Company reinforced its leadership in USP-grade hydroquinone, emphasizing its dioxin-free production and cGMP-compliant processes tailored for pharmaceutical-grade hyperpigmentation treatments. In August 2024, a specialty manufacturer introduced stabilized hydroquinone derivatives engineered to address oxidation challenges during storage, enhancing shelf life in polymer stabilization and high-performance photographic applications.

The market faced significant volatility in early 2025. In January 2025, hydroquinone prices surged by 45% within a single month due to Red Sea geopolitical disruptions that extended delivery timelines by 14 days and increased freight costs by 30% for producers in France, China, and Japan. Responding to this supply shock, Solvay, Europe’s largest hydroquinone manufacturer, boosted production capacity at its French facilities by 20% during 2025 to stabilize regional availability for skincare and industrial end-use sectors. Regulatory pressures intensified on February 1, 2025, when Regulation (EU) 2024/996 came into force, limiting alpha-arbutin to 2% and arbutin to 7% in cosmetic formulations and restricting hydroquinone to unavoidable trace levels. This directly affected the dermatological and cosmetic ingredient supply chain across Europe.

Further strategic shifts unfolded throughout 2025. In May 2025, Mitsui Chemicals Group announced the split-off of its Basic & Green Materials segment, pivoting toward specialty chemical applications such as polymerization inhibitors where hydroquinone remains a core stabilizer in high-precision electronics manufacturing. During 2025, producers accelerated adoption of the hydrogen-peroxide hydroxylation pathway, a production route projected to grow at 4.46% CAGR through 2031 due to up to 50% lower greenhouse gas emissions compared to the conventional cumene process. In August 2025, India’s National Medical Products Administration released a roadmap for updated cosmetic safety standards, including in-vitro skin absorption and toxicological assessment requirements, scheduled for implementation in March 2026. These standards compel hydroquinone manufacturers supplying dermatological markets to provide higher-tier safety validation data. In December 2025, Clean Science and Technology, through Clean Fino-Chem, commenced commercial production of hydroquinone and catechol at a new 10,000 MTPA facility in India, aiming to reduce import dependence and expand its footprint in the global performance chemicals market.

Hydroquinone Market Trends and Opportunities

Regulatory Phase-Outs Accelerating the Shift Toward Clean Beauty Actives

The hydroquinone market is undergoing a structural contraction in cosmetic and dermatological applications as regulators tighten enforcement and global beauty brands realign portfolios toward clean-label positioning. In the United States, the Food and Drug Administration finalized the reclassification of over-the-counter hydroquinone skin-lightening products as unapproved new drugs, following the CARES Act mandate. During 2024 and 2025, the FDA issued warning letters to more than a dozen major distributors, effectively eliminating non-prescription 2% hydroquinone formulations from the U.S. retail channel. This enforcement wave has rapidly collapsed OTC demand and redirected formulators toward alternatives such as alpha-arbutin, kojic acid, and niacinamide.

In Europe, Regulation (EU) 2024/996 has further tightened compliance requirements. Effective February 2025, the regulation mandates that residual hydroquinone in arbutin-based cosmetic formulations be limited to unavoidable trace levels only. This has forced chemical suppliers to invest in dedicated production lines, advanced purification systems, and cross-contamination controls to support hydroquinone-free labeling claims. The compliance burden has raised production costs and extended qualification timelines for cosmetic ingredient suppliers.

Beyond Western markets, the clean beauty movement is gaining traction across China and Southeast Asia. Although hydroquinone still represents an estimated 55% of skin-lightening active volume in less regulated regions, early-2025 industry indicators suggest cosmetic-grade hydroquinone demand in Asia is declining at an estimated 15% annually as multinational brands pivot to botanical and fermentation-derived brighteners. As a result, cosmetic applications are transitioning from a volume-driven segment to a regulated, declining niche within the broader hydroquinone market.

Supply Consolidation and Pricing Discipline in Polymer Stabilization Applications

While cosmetic demand is contracting, hydroquinone remains indispensable as a polymerization inhibitor in acrylic monomers such as methyl methacrylate and in synthetic rubber production. This demand is structurally inelastic, driven by safety requirements in monomer storage, transport, and processing. However, the supply side of the market is highly concentrated. As of December 2025, the top three producers, Syensqo, Mitsui Chemicals, and Eastman, collectively controlled approximately 61% of global capacity.

Strategic restructuring among these producers is tightening spot availability. In May 2025, Mitsui Chemicals announced a major internal split separating its Basic and Green Materials business from higher-margin specialty domains. This shift signals a prioritization of value-added stabilization chemistries over commoditized inhibitor volumes, potentially constraining flexible supply for bulk monomer markets. In parallel, U.S. hydroquinone prices trended upward through late 2025 as producers maintained disciplined operating rates and extended lead times for Asian imports.

Rising energy costs in Europe and increased environmental compliance expenses in China, which accounts for roughly 38% of global hydroquinone demand, are establishing a higher structural floor price. Producers are increasingly passing carbon-related and energy premiums downstream, reinforcing hydroquinone’s positioning as a strategic, safety-critical input rather than a low-cost commodity.

Electronic-Grade Hydroquinone for Advanced OLED and Semiconductor Materials

One of the most compelling growth opportunities in the hydroquinone market lies in ultra-high-purity electronic-grade material for advanced display and semiconductor applications. The transition toward large-area OLED panels for laptops, tablets, and automotive displays is driving demand for 99.9% and higher purity hydroquinone used as a precursor in hole-transport layers and host materials.

In December 2024, Sumitomo Chemical publicly emphasized its strategic pivot toward OLED and automotive display materials, reducing exposure to conventional LCD film businesses. This shift requires highly consistent, metal-free chemical intermediates, positioning electronic-grade hydroquinone as a critical upstream input. Eighth-generation OLED manufacturing imposes sub-parts-per-billion impurity thresholds, creating a significant barrier to entry and allowing established suppliers to command price premiums of two to three times industrial-grade material.

This opportunity is reinforced by broader semiconductor ecosystem expansion in Japan and South Korea. Capacity investments in synthetic silica and anode materials, including 2025 expansions by Mitsubishi Chemical in Kyushu, signal rising demand for specialty electronic chemicals where hydroquinone derivatives are increasingly used as photo-stabilizers and process control additives in advanced lithography environments.

Persistent Demand in Technical Imaging and Medical X-Ray Development

Despite the widespread adoption of digital imaging, hydroquinone continues to serve critical roles in high-contrast technical photography and medical imaging, where its reducing power and tonal control remain unmatched. In emerging economies across South Asia and Africa, healthcare systems continue to rely on analog X-ray film due to lower infrastructure and maintenance costs. This sustains steady demand for hydroquinone-based developer concentrates used in diagnostic radiography.

Industrial non-destructive testing also provides long-term stability. Aerospace, oil and gas, and heavy engineering sectors frequently specify film-based X-ray inspection for weld integrity and pressure vessel certification due to archival reliability and resolution requirements. These standards preserve a high-value technical niche for hydroquinone developers through at least the 2030 horizon.

Additionally, a small but resilient professional and artistic photography segment is supporting premium formulations. Boutique chemical suppliers are marketing stabilized hydroquinone developers designed to resist auto-oxidation and discoloration, catering to professional laboratories and fine-art photographers. While limited in volume, this segment offers attractive margins and reinforces hydroquinone’s continued relevance in specialized imaging applications.

Hydroquinone Market Share and Segmentation Insights

Industrial Grade Hydroquinone Dominates Through Polymerization Inhibitor Demand in Monomer Production

Industrial grade hydroquinone accounted for 58.60% of the Hydroquinone Market share in 2025, making it the largest grade segment due to its widespread use in high-volume industrial chemical processes. Industrial grade hydroquinone is extensively used as a polymerization inhibitor during the storage and transportation of reactive monomers, including acrylic acid, methacrylic acid, styrene, and other vinyl monomers, preventing premature polymer formation that could cause operational hazards and product loss. Because these applications do not require ultra-high purity specifications, industrial grade material provides the most cost-effective solution for chemical manufacturers and monomer producers. The segment’s growth is closely linked to global monomer production capacity utilization, particularly in regions with expanding petrochemical and acrylic monomer manufacturing. In 2025, increasing demand for acrylate polymers, coatings resins, adhesives, and superabsorbent materials continues to drive monomer production, reinforcing the need for reliable inhibitor systems. As a result, hydroquinone remains an essential chemical stabilizer in global monomer logistics, ensuring safe storage, transportation, and processing across the polymer manufacturing supply chain.

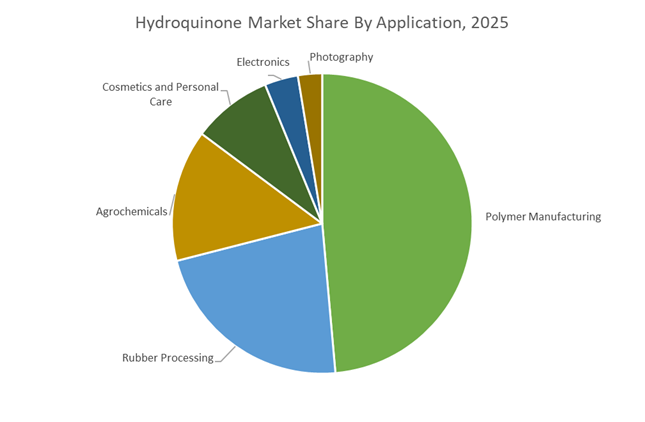

Polymer Manufacturing Drives the Largest Hydroquinone Consumption

Polymer Manufacturing represented 48.60% of the Hydroquinone Market share in 2025, establishing it as the largest application segment for hydroquinone-based chemicals. Hydroquinone plays a critical role in polymer production by functioning both as a polymerization inhibitor for reactive monomers and as a chemical intermediate used in the synthesis of polymer additives. In large-scale petrochemical operations, hydroquinone prevents uncontrolled polymer formation during monomer storage, pipeline transport, and processing, protecting equipment integrity and ensuring consistent product quality. Beyond inhibitor applications, hydroquinone is also used as a key intermediate in the production of polymer antioxidants, including hindered phenolic antioxidants and phosphite stabilizers, which protect plastics and rubber from oxidative degradation during processing and long-term use. This downstream integration connects hydroquinone demand directly to the global plastics additives, synthetic rubber, and polymer stabilization markets. In 2025, the continued expansion of polyethylene, polypropylene, acrylic polymers, and specialty resins across packaging, automotive, and construction sectors has strengthened hydroquinone consumption, as polymer producers require reliable inhibitor and antioxidant chemistry to maintain production stability and material performance.

Competitive Landscape in Hydroquinone Market

Syensqo Advances Circular Phenolics and High-Purity Hydroquinone Production

Following the Solvay demerger, Syensqo now leads the European hydroquinone and specialty diphenol segment with a focus on high-margin performance materials. In 2025 and 2026, the company initiated upgrades to its European production lines, transitioning toward the hydrogen peroxide hydroxylation route to reduce waste-treatment costs by approximately 25% while improving process efficiency. Its Circular Phenolics roadmap integrates bio-attributed feedstocks to lower carbon intensity across diphenol production. Distribution expansion in the DACH region and Baltics through Oqema strengthens localized supply for pharmaceutical and cosmetic intermediates. Syensqo remains a benchmark supplier of high-purity hydroquinone for regulated pharmaceutical synthesis and specialized inhibitor applications.

Eastman Chemical Strengthens cGMP and Stabilizer Leadership

Eastman Chemical Company maintains a strong position in the Western hemisphere with pharmaceutical-grade and photographic-quality hydroquinone. Its Eastman Hydroquinone USP is produced under current Good Manufacturing Practices, positioning it among the limited global suppliers meeting strict dermatological and pharmaceutical standards. In 2025, Eastman introduced Dioxin-Free certification across its hydroquinone derivatives portfolio to address safety requirements in personal care markets. The company is capitalizing on rising demand for hydroquinone-based stabilizers in polymer packaging and expanded TBHQ production to serve biodiesel and animal feed antioxidants. Vertical integration into acrylic stabilizers provides additional resilience against raw material volatility.

Camlin Fine Sciences Expands Vertical Integration in Diphenols

Camlin Fine Sciences operates one of the most vertically integrated hydroquinone value chains globally, controlling production from diphenols to downstream antioxidants. The ramp-up of its Dahej world-scale diphenol facility strengthened its status as a major global hydroquinone and catechol producer. CFS holds its dominance in food preservation and polymer stabilization markets. In early 2026, the company reported a 17% sales CAGR in its Performance Chemicals segment, supported by strong acrylic acid inhibitor demand across Asia. Its integrated pathway to vanillin production provides a strategic hedge against phenolic market fluctuations.

Mitsui Chemicals Positions Hydroquinone as Specialty Performance Input

Mitsui Chemicals is repositioning hydroquinone as a specialty performance chemical under its Vision 2030 framework, targeting ICT and mobility sectors. The company achieved Platinum status in the Responsible Business Alliance audit for its chemical materials division, enhancing its appeal to ESG-focused technology manufacturers. R&D investment in hydroquinone dipalmitate expands its footprint in regions imposing restrictions on traditional hydroquinone usage. With Asia-Pacific representing nearly half of global hydroquinone revenue, Mitsui leverages its regional supply strength to serve synthetic rubber and polymer stabilization markets in China and Japan.

UBE Corporation Focuses on Engineering Plastics and UV-Curable Resins

UBE Corporation concentrates on high-purity solid hydroquinone used in engineering plastics, polyethers, and aromatic polyamides. Its 2026 strategy emphasizes value-added monomers, particularly hydroquinone’s role as an inhibitor in UV-curable resins for electronics and advanced coatings. Integration of Green Phenol initiatives in 2025 enhanced waste-reduction performance and alignment with Japan’s carbon neutrality objectives. UBE maintains long-term supply agreements with global tire and rubber manufacturers, ensuring stable demand for antioxidant intermediates in high-performance elastomers.

Brother Technology Expands Global Footprint in Fine Chemicals

Brother Technology has emerged as a competitive Asian producer, operating one of China’s most efficient hydroquinone facilities. The company supports the expansion of hydroquinone applications in advanced polymers and vitamin synthesis through its integrated antioxidant industrial park. Completion of the second development phase in late 2025 strengthened its pharmaceutical-grade intermediate capabilities. In 2026, Brother Technology is expanding direct sales offices in Europe and North America to compete with established Western suppliers on cost efficiency and logistical responsiveness, accelerating the globalization of Chinese hydroquinone capacity.

United States: Prescription-Only Cosmetics, Semiconductor Purity, and Industrial Rebalancing

The United States hydroquinone industry has entered a decisive regulatory and application-driven transition. Following its reclassification as a “new drug,” the U.S. Food and Drug Administration maintained strict enforcement through 2025, resulting in the complete removal of over-the-counter skin-lightening products. This action structurally redirected an estimated 42% of cosmetic-related demand into prescription-only dermatology channels, reshaping downstream distribution models and tightening compliance requirements for formulators. At the same time, industrial demand has become more technically sophisticated. Domestic producers reported a 19% rise in launches of ultra-high-purity hydroquinone grades since late 2024, largely driven by semiconductor photolithography and advanced electronics packaging, where impurity control directly affects yield stability.

On the supply side, Eastman Chemical Company confirmed material progress in its 2025 cost-optimization program, targeting structural cost reductions across polymer additives and rubber antioxidants that rely on hydroquinone chemistry. Inventory strategies also shifted in late 2025, as U.S. industrial buyers initiated large-scale destocking to manage tariff exposure, contributing to a reported $200 million inventory reduction among major chemical suppliers. In parallel, automotive rubber manufacturers introduced new hydroquinone-based antioxidant systems engineered to withstand the higher torque and thermal loads associated with electric vehicle tires, reinforcing the compound’s relevance in next-generation mobility materials.

India: Integrated Diphenols, Antioxidant Leadership, and Margin Discipline

India has consolidated its position as a structurally important producer and exporter within the global hydroquinone value chain, supported by scale, integration, and downstream antioxidant leadership. Camlin Fine Sciences reported strong operational momentum in 2025, supported by an installed specialty chemicals capacity of 49,000 MTPA and integrated diphenol production encompassing both hydroquinone and catechol. The company’s sharp year-on-year sales growth in the September 2025 quarter reflects rising global demand for food-grade and performance antioxidants derived from hydroquinone.

Strategic expansion has also taken an inorganic route. The late-2025 regulatory clearance for Camlin Fine Sciences’ majority acquisition of Vinpai in France signals a move to combine hydroquinone-based shelf-life enhancement with natural functional ingredient platforms. At an industry level, India has reinforced its dominance in tert-Butylhydroquinone production, exporting TBHQ to more than 80 countries and anchoring its role in global food preservation systems. However, producers faced margin pressure in late 2025 due to a 12.5% rise in benzene and toluene costs, accelerating the adoption of higher-efficiency catalytic synthesis routes to protect profitability in performance chemical applications.

China: Cosmetic Standardization, Semiconductor Localization, and Export Substitution

China’s hydroquinone industry is being reshaped by tighter cosmetic oversight, electronics self-sufficiency goals, and shifting global trade flows. The National Medical Products Administration issued its 2025 cosmetic standards work plan, introducing new safety testing methods effective March 2026 to align hydroquinone purity and toxicology thresholds with international benchmarks. This regulatory clarity is reinforcing demand for compliant, high-purity material in premium functional skincare, even as overall cosmetic formulations adapt to stricter controls.

Beyond cosmetics, industrial policy is the dominant driver. Under the Ministry of Industry and Information Technology 2026 digital transformation blueprint, China has prioritized domestic production of electronic-grade hydroquinone to support 12-inch wafer fabrication lines. Trade dynamics have further strengthened Chinese suppliers’ export position. A 50% tariff imposed on certain Indian chemical exports to the U.S. in 2025 created a supply gap that Chinese producers rapidly filled, particularly in vanillin synthesis and polymer stabilizer segments. This shift is occurring against the backdrop of resilient domestic consumption, with China’s cosmetics retail market sustaining strong growth and underpinning steady demand for hydroquinone derivatives used in high-end formulations.

European Union: Cosmetic Prohibition, Environmental Scrutiny, and Pharmaceutical Reorientation

The European Union represents the most restrictive regulatory environment for hydroquinone, fundamentally redefining its end-use mix. Commission Regulation (EU) 2025/877 finalized the prohibition of hydroquinone in cosmetic products across the bloc, effectively eliminating retail skincare applications within a region that accounts for roughly 35% of the global cosmetics footprint. This ban has permanently altered demand structures, forcing producers to pivot toward pharmaceutical, industrial, and specialty chemical uses.

Environmental oversight has intensified in parallel. The European Commission’s 2025 water policy watch list placed hydroquinone derivatives under closer aquatic monitoring, compelling manufacturers to invest in advanced effluent treatment systems by 2026. Despite these constraints, industrial demand has not collapsed. Solvay expanded its high-purity hydroquinone portfolio in late 2024 to meet growing pharmaceutical requirements, offsetting the decline in traditional photographic developer applications. Compliance with updated REACH obligations has raised operating costs across the region, establishing a price floor that keeps European hydroquinone structurally more expensive than Asian imports.

Saudi Arabia: Drug Reclassification and Demand Suppression Through Enforcement

Saudi Arabia’s hydroquinone market is being reshaped almost entirely by public health policy and enforcement. In 2025, the Saudi Food and Drug Authority classified all hydroquinone-containing products as drugs, irrespective of concentration. Subsequent studies revealing illegally high hydroquinone levels in unregulated skin-lightening creams triggered a broad regulatory crackdown that intensified through 2026.

Complementing enforcement, the Ministry of Health launched nationwide awareness campaigns highlighting carcinogenic risks associated with misuse. These measures have sharply reduced demand for informal and black-market cosmetic products, compressing retail consumption while reinforcing the requirement for pharmaceutical-grade compliance. As a result, Saudi Arabia’s hydroquinone demand profile is narrowing toward regulated medical channels, with limited scope for recovery in consumer-facing segments.

Comparative Snapshot: Hydroquinone Industry Dynamics by Country

Hydroquinone Market County Level Snapshot

|

Region

|

Primary Policy Driver

|

Demand Shift

|

Strategic Implication

|

|

United States

|

FDA drug reclassification

|

OTC cosmetics to prescription and electronics

|

Higher purity focus, regulated distribution

|

|

India

|

Integrated manufacturing and exports

|

Growth in food-grade and performance antioxidants

|

Scale-driven global supplier role

|

|

China

|

Cosmetic standards and semiconductor localization

|

Premium skincare and electronic-grade materials

|

Export substitution and domestic self-reliance

|

|

European Union

|

Cosmetic bans and REACH compliance

|

Pivot to pharma and specialty uses

|

Higher costs, constrained volumes

|

|

Saudi Arabia

|

Drug classification and enforcement

|

Collapse of informal cosmetic demand

|

Narrow, compliance-led market structure

|

Hydroquinone Market Report Scope

Hydroquinone Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9 Billion

|

|

Market Size (2034)

|

$14.9 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Grade (Industrial Grade, Pharmaceutical Grade, Photographic Grade, Electronic Grade), By Function (Antioxidant, Polymerization Inhibitor, Reducing Agent, Chemical Intermediate, Depigmenting Agent), By Application (Polymer Manufacturing, Rubber Processing, Cosmetics and Personal Care, Agrochemicals, Photography, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Eastman Chemical Company, Camlin Fine Sciences Ltd., Solvay S.A., Mitsui Chemicals, Inc., UBE Corporation, Hubei Zhenhua Chemical, Yanfeng Group, Clean Science and Technology Ltd., Celanese Corporation, Indspec Chemical Corporation, Sanonda Group, Gennex Laboratories Ltd., Merck KGaA, Thermo Fisher Scientific, Atul Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydroquinone Market Segmentation

By Grade

- Industrial Grade

- Pharmaceutical Grade

- Photographic Grade

- Electronic Grade

By Function

- Antioxidant

- Polymerization Inhibitor

- Reducing Agent

- Chemical Intermediate

- Depigmenting Agent

By Application

- Polymer Manufacturing

- Rubber Processing

- Cosmetics and Personal Care

- Agrochemicals

- Photography

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hydroquinone Industry

- Eastman Chemical Company

- Camlin Fine Sciences Ltd.

- Solvay S.A.

- Mitsui Chemicals, Inc.

- UBE Corporation

- Hubei Zhenhua Chemical

- Yanfeng Group

- Clean Science and Technology Ltd.

- Celanese Corporation

- Indspec Chemical Corporation

- Sanonda Group

- Gennex Laboratories Ltd.

- Merck KGaA

- Thermo Fisher Scientific

- Atul Ltd.

*- List not Exhaustive