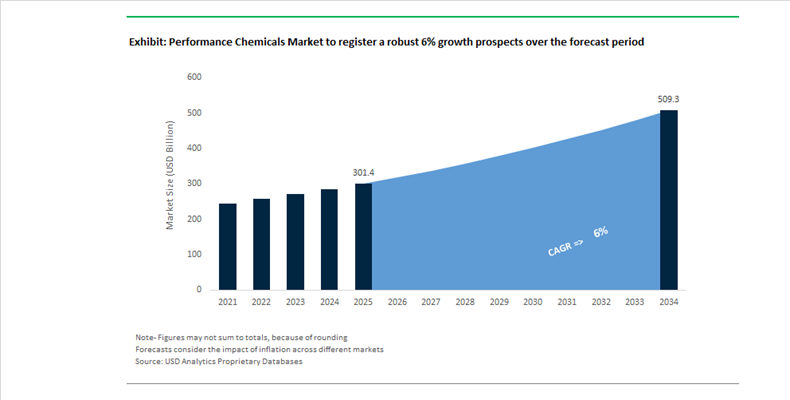

Performance Chemicals Market Size 2025–2034: $301.4 Billion to $509.2 Billion at 6% CAGR Driven by Portfolio Consolidation, Circular Raw Materials, and Digital Manufacturing

The global performance chemicals market is projected to expand from $301.4 billion in 2025 to $509.2 billion by 2034, registering a steady CAGR of 6%. Growth is anchored in rising demand for high-performance coatings, advanced dispersions, specialty silica, catalysts, and functional additives across automotive, construction, aerospace, electronics, and industrial manufacturing. Unlike commodity chemicals, performance chemicals compete on technical differentiation, lifecycle durability, sustainability compliance, and application-specific customization. From electronic-grade peroxides to aerospace primers and circular silica fillers, the sector is undergoing structural transformation through consolidation, digitalization, and ESG-driven capital reallocation.

Strategic mega-mergers and asset rebalancing are reshaping global leadership structures in 2026. In February 2026, AkzoNobel proposed an all-stock merger with Axalta Coating Systems, targeting completion by late 2026 or early 2027. The transaction aims to create a dominant global player in performance coatings and architectural finishes, combining automotive OEM, industrial, and refinish portfolios under a consolidated R&D framework. In parallel, AkzoNobel finalized the €922 million divestment of its stake in Akzo Nobel India Ltd in February 2026, a move designed to strengthen its balance sheet and sharpen focus on globally integrated performance materials. At the same time, investment firm Wendel agreed in early 2026 to sell its stake in Stahl to Henkel for €2.1 billion, strengthening Henkel’s footprint in high-performance surface treatments for automotive interiors and luxury substrates.

Capacity expansion in high-growth regions is accelerating supply chain localization. In February 2026, BASF India launched a new production line at its Mangalore site dedicated to advanced dispersions under Acronal and Basonal technologies. These high-performance dispersions serve architectural paints, construction chemicals, and paper coatings, aligning with India’s infrastructure expansion and urbanization pipeline. In January 2026, BASF announced the establishment of a Global Digital Hub in Hyderabad, integrating AI and data science into manufacturing optimization and supply chain analytics for performance chemicals across Asia-Pacific. This digitalization push reflects broader industry adoption of predictive maintenance, yield optimization, and carbon tracking in specialty production environments.

Circularity and energy efficiency are redefining competitive positioning in Europe and Asia. In September 2025, Solvay confirmed that by 2026 its Highly Dispersible Silica plants in Qingdao and Gunsan would switch to ISCC+ certified waste sand, converting more than half of its regional HDS capacity to circular raw materials. This shift directly supports tire manufacturers targeting over 40% circular content by 2030. In November 2025, Solvay reported a €50 million gain from optimizing its CO2 emissions rights portfolio, leveraging reduced European production and energy transition progress to generate liquidity for reinvestment into electronic-grade peroxide and rare earth applications.

Operational restructuring is being implemented to protect margins amid volatile energy costs and uneven industrial demand. Throughout 2025, Evonik executed its “Tailor Made” efficiency program across performance materials divisions, and in February 2026 confirmed continuation of restructuring measures including elimination of 2,000 positions globally. Clariant followed with leadership and governance restructuring in December 2025, appointing a new President Designate for Care Chemicals & Americas effective January 2026 and reducing board size ahead of the 2026 AGM to streamline specialty operations.

Application-level innovation remains a central growth lever. In early 2026, AkzoNobel introduced Aerobase, a single-coat aerospace primer engineered to reduce aircraft weight and improve Maintenance, Repair, and Overhaul efficiency by lowering application steps. In catalyst performance, Axens completed the acquisition of Eurecat in early 2026, strengthening capabilities in catalyst regeneration and recycling services essential for refining and petrochemical decarbonization strategies.

Structural Trends and Growth Opportunities Reshaping the Global Performance Chemicals Market

Strategic Portfolio Realignment Toward Circularity and Carbon-Reduced Chemistry

The performance chemicals market is undergoing a fundamental capital reallocation as leading producers actively exit high-carbon, volume-driven chemistries and double down on circular, value-added solutions. This is no longer incremental sustainability positioning but a structural reshaping of portfolios to align with long-term carbon regulation, investor scrutiny, and downstream customer decarbonization targets. A defining example is BASF, which during 2024–2025 accelerated the restructuring of its Ludwigshafen Verbund by shutting down emissions-intensive ammonia, melamine, and fertilizer units while simultaneously integrating its catalyst operations into the Performance Chemicals division effective January 2025. This strategic consolidation reflects a shift toward low-carbon enablers such as catalysts, additives, and functional intermediates that directly support circular industrial systems.

Mass-balance and bio-attributed feedstocks are now being deployed at industrial scale rather than pilot levels. In 2024, Evonik and BASF executed a landmark agreement for ammonia BMBcert™, a feedstock with at least 65% lower product carbon footprint than conventional grades. This ammonia is already being used to manufacture high-performance VESTAMIN® eCO curing agents for industrial coatings and wind turbine blades, enabling customers to reduce Scope 3 emissions without reformulating products. Parallel to this, specialty producer Kensing partnered with AmphiStar in late 2025 to onshore biosurfactant production from upcycled biowaste such as used cooking oil, targeting the elimination of fossil-based surfactants from North American personal care formulations by 2030. These moves signal that performance chemicals are becoming the preferred vehicle for chemical industry decarbonization.

Deepening Co-Development Partnerships With End-User Industries

The market is rapidly shifting away from standardized product supply toward embedded, solution-oriented collaboration models. Performance chemical suppliers are increasingly acting as long-term R&D partners, co-developing materials directly within customer value chains. In the automotive sector, circularity-driven partnerships are setting new benchmarks. In September 2025, Mitsubishi Chemical Group and Honda successfully implemented recycled PMMA acrylic resin in the N-ONE e: electric vehicle platform. This closed-loop system integrates resin formulation, component manufacturing, and end-of-life recycling under a single lifecycle framework managed by the chemical supplier.

Artificial intelligence is further accelerating this collaborative model. In 2025, Kemira entered a strategic partnership with CuspAI to embed AI-driven material discovery into its R&D pipeline. This approach reduces development timelines for new water treatment and performance chemistries from multiple years to a matter of months, enabling rapid compliance with tightening industrial effluent and water reuse regulations. Construction materials are also being decarbonized through co-development. A 2025 agreement between Covestro and Selena Group replaced traditional cement mortar with high-performance polyurethane foam adhesives for bricklaying, delivering an estimated 90% carbon footprint reduction compared to mineral binders. These partnerships illustrate how performance chemicals are increasingly co-designed around customer process economics, sustainability targets, and regulatory constraints.

Formulation Platforms for Next-Generation Battery Manufacturing

As battery markets scale globally, competitive differentiation is shifting from active materials to the chemical interfaces that govern safety, durability, and charging performance. Performance chemicals now play a central role in electrolyte systems, binders, encapsulants, and high-voltage polymers. In December 2025, Mitsubishi Chemical transferred its battery electrolyte manufacturing assets in the United States and United Kingdom to Green E Origin, allowing it to concentrate on electrolyte licensing and high-purity additive innovation through MU Ionic Solutions. This IP-centric strategy was recognized with the Asia IP Elite 2025 award, underscoring the rising strategic value of proprietary electrolyte formulations.

On the component side, BASF has expanded its Ultramid® DC performance polyamide portfolio to address the safety and identification requirements of 800V EV architectures. These materials retain laser-markable, high-visibility orange coloration throughout the vehicle lifecycle, ensuring compliance and safety in high-voltage connectors. Complementing this, Huntsman Corporation launched SHOKLESS™ polyurethane encapsulation systems during 2024–2025, providing structural reinforcement, vibration damping, and thermal protection for EV battery packs. These developments highlight a growing opportunity for multifunctional performance polymers that integrate mechanical, thermal, and fire-protection properties into a single material platform.

Digitalization-Enabling Chemicals for Smart and Precision Agriculture

The digital transformation of agriculture is opening a distinct growth pathway for performance chemicals engineered to function within variable-rate application systems, autonomous sprayers, and drone-based delivery platforms. The specialty fertilizers market reached USD 46.2 billion in 2024, with controlled-release fertilizers accounting for over 40% of revenue. This growth is driven by advanced encapsulation polymers that modulate nutrient release based on soil moisture and temperature, dramatically reducing nitrogen runoff and improving nutrient-use efficiency.

Strategic M&A is accelerating customization capabilities. In July 2024, ICL acquired Custom Ag Formulators for USD 60 million, enabling the development of tailored tank-mix compatibilizers that prevent precipitation, phase separation, and nozzle clogging during multi-input applications. Government policy is further amplifying demand. India’s 2025–2026 Union Budget allocated over USD 18 billion to the Ministry of Chemicals and Fertilizers, with targeted support for Nano-DAP and bio-based crop protection products. This funding is accelerating the adoption of high-performance surfactants, adhesion promoters, and drift-control agents that ensure precise delivery of high-value nano-nutrients. Collectively, these trends position performance chemicals as essential enablers of data-driven, resource-efficient agriculture rather than passive formulation components.

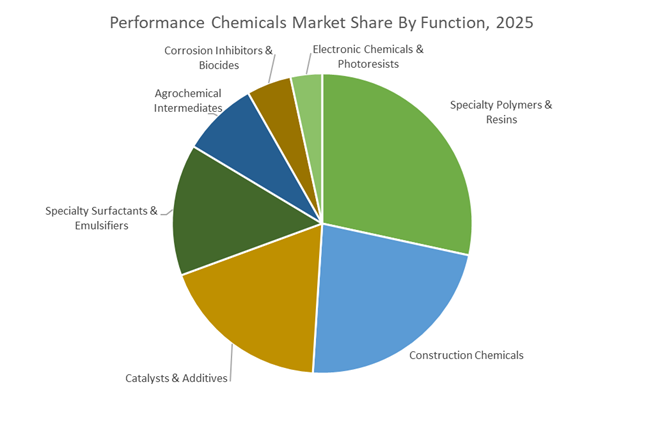

Performance Chemicals Market Share and Segmentation Insights

Specialty Polymers and Resins Lead Performance Chemicals Demand in Advanced Industrial Materials

Specialty polymers and resins accounted for 28.40% of the Performance Chemicals Market by function in 2025, reflecting their critical role in enabling advanced material performance across multiple industries. These materials provide tailored properties such as mechanical strength, chemical resistance, adhesion, flexibility, and thermal stability required in automotive components, electronic devices, packaging materials, and construction systems. Specialty polymer technologies include engineering thermoplastics, high-performance resins, and advanced composite materials used in demanding industrial applications. In 2025, sustainable polymer innovation within specialty materials development is accelerating, with chemical producers introducing bio-based, recyclable, and biodegradable polymer solutions that support circular economy strategies while maintaining the performance requirements of high-value industrial applications.

Mobility and Transportation Sector Drives Performance Chemical Consumption in Vehicle Manufacturing

Mobility and transportation represented 32.80% of the Performance Chemicals Market by application in 2025, reflecting the extensive use of advanced chemicals in automotive, aerospace, rail, and marine manufacturing. Performance chemicals are integrated into vehicle production through coatings, composite materials, adhesives, lubricant additives, and thermal management fluids that improve durability and operational efficiency. The scale of global vehicle manufacturing continues to sustain strong demand for specialized chemical formulations. In 2025, transportation electrification trends are reshaping chemical demand patterns, increasing consumption of battery materials, dielectric fluids, and lightweight composite polymers while gradually reducing demand for traditional engine-related additives and exhaust treatment chemicals.

Performance Chemicals Market Competitive Landscape

The Performance Chemicals Market is transitioning toward value-driven growth, characterized by AI-enabled innovation, circular feedstock integration, and portfolio optimization. Leading players are evolving into solution providers for EV batteries, electronics, and sustainable packaging, while navigating demand volatility and regional competitive shifts toward Asia-Pacific.

BASF strengthens performance chemicals leadership through Verbund expansion and portfolio realignment

BASF SE is reinforcing its leadership in the performance chemicals market through its “Winning Ways” strategy and large-scale Verbund integration. The full-scale startup of the Zhanjiang site in China in Q1 2026 is central to supplying high-performance plastics and dispersions to automotive and electronics sectors. The integration of Chemical and Refining Catalysts into the Performance Chemicals division enhances its specialty additives portfolio. BASF reported €6.6 billion EBITDA in 2025 and targets up to €7.0 billion in 2026, supported by cost reductions of €2.3 billion. Its shareholder-focused capital strategy, including €12 billion distribution by 2028, reflects financial strength. This combination of scale, integration, and restructuring strengthens BASF’s competitive edge.

Dow accelerates AI-driven transformation and bio-circular materials strategy under Transform to Outperform program

Dow Inc. is executing a major transformation strategy aimed at improving efficiency and profitability through automation and AI integration. The company targets $2 billion in additional EBITDA improvement, focusing on streamlined operations and digital customer engagement. Its ISCC PLUS-certified Freeport facility enables production of bio-circular polymers for construction and appliances. Dow’s Cooling Science Studio in Shanghai supports innovation in thermal management for data centers and electronics. Despite a decline to $40 billion in sales in 2025, the company achieved growth in high-value silicones. Its feedstock advantage in the U.S. Gulf Coast continues to underpin cost competitiveness.

Evonik advances specialty additives and high-performance polymers with ROCE-focused strategy

Evonik Industries AG is focusing on high-margin specialty chemicals through its Advanced Technologies and Custom Solutions segments. The company reported €1.87 billion EBITDA in 2025 and maintains a 2026 outlook of €1.7–€2.0 billion, with a target ROCE of 11%. Its High-Performance Polymers segment is benefiting from strong demand in gas separation membranes and green hydrogen applications. Strategic pricing actions, including a 2% increase in late 2025, have helped protect margins. Evonik’s new dividend policy links payouts to profitability, reinforcing financial discipline. This focus on specialty innovation and capital efficiency enhances its competitive positioning.

Solvay drives decarbonization and industrial restructuring to align with energy transition demand

Solvay S.A. is transforming its performance chemicals portfolio under its “Essential Chemistry” strategy, focusing on decarbonization and industrial optimization. The company is phasing out coal-based energy and investing in bio-based silica production and alternative fuel systems across Europe. It has restructured its asset base by closing underperforming sites and reducing capacity in Spain. Solvay expanded its electronic-grade hydrogen peroxide capacity in China and rare earth processing in France, targeting EV and renewable energy markets. Despite a 13% EBITDA decline to €881 million in 2025, it maintained a strong margin near 21%. This strategic repositioning supports long-term competitiveness in sustainable chemicals.

Clariant innovates metal-free catalysts and low-VOC additives to lead circular performance chemicals transition

Clariant AG is positioning itself as a sustainability-driven innovator in the performance chemicals market. Its AddWorks™ titanium-based catalysts eliminate reliance on antimony, addressing supply chain risks and regulatory pressures. The expansion of its Hostagliss™ lubricant portfolio introduces water-based, low-emission solutions for industrial applications. Clariant is prioritizing circularity in polyester production, enabling easier PET recycling and compliance with global environmental regulations. The company is also strengthening its presence in China through localized R&D and market-specific product development. This focus on sustainable innovation and regional expansion enhances its role as a specialty chemicals leader.

India – Policy-Led Scale-Up and Biomanufacturing Acceleration

India’s performance chemicals industry is being reshaped by a rare combination of scale-focused infrastructure policy and targeted operating incentives. Under the Petroleum, Chemicals and Petrochemicals Investment Regions (PCPIR) Policy 2020–2035, the government is targeting cumulative investments of ₹10 lakh crore by the end of 2025, creating tightly integrated mega-clusters that co-locate feedstocks, utilities, and downstream performance chemical units. This cluster-based model is structurally reducing scope 2 emissions while improving asset utilization for specialty surfactants, functional polymers, and electronic-grade additives. Complementing this, the 2025 introduction of an Opex-linked subsidy scheme is explicitly designed to encourage incremental domestic production of high-import-dependence performance chemicals, particularly those critical to electronics manufacturing and advanced materials supply chains.

Private capital deployment is reinforcing this momentum. SNF Flopam announced a ₹800 crore capital expenditure program in 2025 to expand capacity for water-soluble polymers serving municipal water treatment and industrial processing. Parallelly, the BioE3 Policy has unlocked fresh R&D funding for high-performance biomanufacturing, accelerating the substitution of petrochemical surfactants with bio-based enzymes and renewable functional additives. Structural enablers such as mandatory digital tracking of fertilizer and specialty chemical flows and port-led development initiatives are further tightening India’s export competitiveness, with logistics reforms targeting a 15% reduction in lead times to Southeast Asian markets by 2026.

China – High-End Substitution and AI-Enabled Manufacturing Discipline

China’s performance chemicals sector is operating under a tightly managed growth framework. The Ministry of Industry and Information Technology’s Work Plan for Stabilizing Growth (2025–2026) mandates annual value-added growth above 5%, but explicitly prioritizes high-end polyolefins, semiconductor process chemicals, and advanced functional polymers over volume-led expansion. This is paired with strict capacity controls on new refining projects, preventing oversupply while channeling tax rebates toward green technology upgrades in specialty chemical production. As a result, capital is flowing toward semiconductor-grade wet chemicals, advanced polyimides, and electronic materials with a stated objective of exceeding 90% domestic self-sufficiency by 2026.

A defining structural shift is the national rollout of the “AI + Petrochemicals” initiative in 2025. This program embeds AI-driven process optimization and blockchain-based traceability across fine chemical platforms, directly improving yield stability and compliance transparency. At the regional level, SME-focused advanced material clusters in Ningxia and Shanxi are emerging as centers for bio-based polymers and high-performance fibers tailored for aerospace and defense applications. Collectively, these measures indicate a deliberate transition from scale-driven petrochemicals toward disciplined, technology-intensive performance chemical manufacturing.

United States – Feedstock Advantage and Portfolio Recomposition

The United States continues to benefit from a structural cost advantage in performance chemicals due to abundant shale-derived natural gas liquids. This feedstock position underpins global competitiveness in ethylene-based specialty derivatives and functional intermediates. However, 2025 has marked a strategic inflection point, with majors such as Dow, DuPont, and Corteva executing carve-outs and divestitures to exit lower-margin commoditized assets and concentrate on formulation-intensive, application-specific performance chemicals. This portfolio simplification is sharpening capital allocation toward defensible niches.

Technology-driven demand is reinforcing this shift. Chemours successfully qualified PFA-compatible immersion cooling fluids for AI servers in Q3 2025, addressing thermal management constraints in hyperscale data centers. Simultaneously, U.S. producers are expanding battery-grade electrolytes and lithium salt portfolios to align with federal policies supporting domestic electric vehicle supply chains through 2026. These dynamics position the U.S. performance chemicals market as innovation-led, with growth anchored in energy transition and digital infrastructure.

Japan – Consolidation, Green Feedstocks, and Semiconductor Reach

Japan’s performance chemicals landscape is undergoing structural consolidation to restore capital efficiency. A landmark agreement among Mitsui Chemicals, Idemitsu Kosan, and Sumitomo Chemical will integrate their domestic polyolefin businesses into Prime Polymer by April 2026, directly addressing regional oversupply while freeing resources for higher-value performance materials. In parallel, Sumitomo Chemical strengthened its semiconductor materials position in November 2025 through the acquisition of a Taiwanese process chemicals firm, signaling aggressive expansion into U.S. and Asian chip fabrication markets.

Technological differentiation remains a core theme. Sumitomo’s successful scale-up of propylene-from-ethanol technology in mid-2025 provides a lower-carbon pathway for high-performance plastics, aligning with customer decarbonization targets. Mitsubishi Chemical Group’s adoption of the Circularise traceability platform in 2025 further supports circular economy strategies, particularly for acrylic resins used in automotive applications. Japan’s approach emphasizes consolidation, green feedstock innovation, and deep integration with semiconductor value chains.

Germany – Energy Cost Pressure and Selective Resilience

Germany’s performance chemicals sector is navigating structural energy cost disadvantages alongside tightening regulatory frameworks. In response, producers are accelerating hydrogen integration into ethylene production and adopting carbon-neutral feedstocks, including Way to GO2-certified hydrogen peroxide, to stabilize long-term operating viability. Despite contraction in basic chemicals during 2025, the pharmaceutical performance chemicals segment demonstrated resilience, growing by 3% on the back of sustained investment in high-purity intermediates for oncology and immunology applications.

At the same time, regulatory complexity is influencing geographic decisions. A late-2025 survey by the VCI indicated that roughly 20% of German chemical companies are considering relocation or domestic capacity shutdowns, driven by PFAS restrictions and compliance burdens. This bifurcation highlights a market increasingly polarized between globally competitive, innovation-driven niches and structurally challenged commodity-adjacent operations.

Comparative Overview – Performance Chemicals by Country

Performance Chemicals Market County Level Snapshot

|

Country

|

Structural Driver

|

Strategic Focus

|

Market Character

|

|

India

|

PCPIR clusters and Opex subsidies

|

Import substitution, biomanufacturing

|

Scale-up with policy backing

|

|

China

|

Capacity discipline and AI adoption

|

Semiconductor and high-end materials

|

Technology-controlled growth

|

|

United States

|

Shale feedstock advantage

|

AI cooling, EV materials

|

Innovation-led specialization

|

|

Japan

|

Polyolefin consolidation

|

Green feedstocks, semiconductors

|

Capital-efficient, high value

|

|

Germany

|

Energy transition pressure

|

Pharma intermediates, hydrogen

|

Selective resilience

|

Performance Chemicals Market Report Scope

Performance Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$301.4 Billion

|

|

Market Size (2034)

|

$509.2 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Function (Specialty Polymers & Resins, Catalysts & Additives, Electronic Chemicals & Photoresists, Specialty Surfactants & Emulsifiers, Construction Chemicals, Agrochemical Intermediates, Corrosion Inhibitors & Biocides), By Product Class (Advanced Materials, Electronic Materials, Green & Bio-based Chemicals, Performance Pigments & Masterbatches, Flavors & Fragrances), By Application (Mobility & Transportation, Electronics & Telecommunications, Infrastructure & Construction, Health & Personal Care, Industrial & Water Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., DuPont de Nemours Inc., SABIC, Mitsubishi Chemical Group Corporation, Sumitomo Chemical Co. Ltd., Evonik Industries AG, Solvay SA, Mitsui Chemicals Inc., Reliance Industries Limited, Wanhua Chemical Group, Chemours Company, Huntsman Corporation, Arkema SA, Clariant AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Performance Chemicals Market Segmentation

By Function

- Specialty Polymers & Resins

- Catalysts & Additives

- Electronic Chemicals & Photoresists

- Specialty Surfactants & Emulsifiers

- Construction Chemicals

- Agrochemical Intermediates

- Corrosion Inhibitors & Biocides

By Product Class

- Advanced Materials

- Electronic Materials

- Green & Bio-based Chemicals

- Performance Pigments & Masterbatches

- Flavors & Fragrances

By Application

- Mobility & Transportation

- Electronics & Telecommunications

- Infrastructure & Construction

- Health & Personal Care

- Industrial & Water Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Performance Chemicals Industry

- BASF SE

- Dow Inc.

- DuPont de Nemours Inc.

- SABIC

- Mitsubishi Chemical Group Corporation

- Sumitomo Chemical Co. Ltd.

- Evonik Industries AG

- Solvay SA

- Mitsui Chemicals Inc.

- Reliance Industries Limited

- Wanhua Chemical Group

- Chemours Company

- Huntsman Corporation

- Arkema SA

- Clariant AG

*- List not Exhaustive