Market Overview: Axens Consolidation, Sulfuric Acid Regeneration Focus, and Circular Catalyst Technologies Reshape Catalyst Regeneration Market

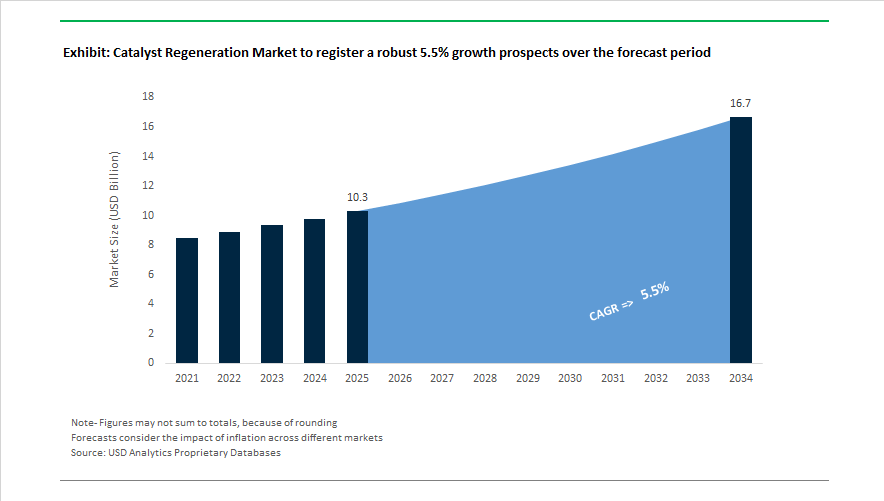

The Catalyst Regeneration Market is projected to grow from USD 10.3 billion in 2025 to USD 16.7 billion by 2034, expanding at a CAGR of 5.5% as refiners and petrochemical operators prioritize catalyst lifecycle optimization, sulfur recovery efficiency, and circular chemical processing. In March 2024, Evonik Industries launched Octamax, a regenerated CoMo and NiMo catalyst line engineered for deep sulfur removal in refinery streams while maintaining gasoline octane performance. During 2024, Eurecat recorded a 15% rise in industrial property filings, registering 30 new patents focused on catalyst rejuvenation and sustainability technologies that restore spent hydroprocessing catalysts to near-original activity. Regulatory momentum also strengthened in India across 2024 to 2025 as the Central Pollution Control Board tightened hazardous waste rules governing metal-bearing spent catalysts, prompting refiners to rely on licensed domestic regeneration hubs rather than disposal routes.

Industry consolidation accelerated in October 2025 when Axens moved to become sole owner of Eurecat after acquiring Ketjen’s stake, a transaction expected to conclude in the first half of 2026. That same month, Albemarle Corporation divested retained catalyst interests, including its position linked to Eurecat, raising approximately USD 660 million as it refocused on lithium. Ketjen simultaneously signed a long-term collaboration agreement with Eurecat in October 2025 to secure continued access to specialized regeneration services for hydroprocessing catalysts. In November 2025, Global Standard Air introduced a palladium-catalyst hydrogen dryer in Seoul, embedding catalyst longevity protocols for ultra-high-purity hydrogen systems. Recognition of circular innovation followed in December 2025 when Topsoe received the S&P Platts Global Energy Award for chemical excellence, highlighting regeneration-enabled carbon footprint reductions.

Strategic portfolio realignment continued into 2026. On January 2, 2026, Ecovyst completed the sale of its Advanced Materials and Catalysts segment to Technip Energies for approximately USD 530 million, sharpening its focus on sulfuric acid regeneration services in North America. Evonik’s site service restructuring became effective January 2026 with SYNEQT GmbH operating independently, streamlining infrastructure and logistics for major German regeneration facilities. The low-carbon hydrogen transition further influenced regeneration practices after the November 2024 agreement between Aramco and Topsoe on eREACT technology, which includes specialized protocols to maintain catalyst stability in electrified reactors. Momentum extended to Asia in February 2026 when BPCL signed multiple refinery efficiency agreements during India Energy Week, incorporating next-generation off-site catalyst regeneration to support throughput expansion.

Catalyst Regeneration Market Trends and Opportunities Driving Lifecycle Optimization Across Refining, Chemicals, and Hydrogen

The Catalyst Regeneration Market is shifting from maintenance-driven services to strategic performance management as refiners and chemical producers respond to margin pressure, volatile specialty catalyst pricing, and tighter ESG mandates. Operators now treat regeneration as a core asset optimization tool, embedding catalyst lifecycle planning into refinery economics, circularity targets, and energy transition roadmaps.

Rising precious metal costs, alternative feedstock adoption, and distributed hydrogen assets are accelerating demand for high-frequency regeneration, regeneration-as-a-service models, and advanced in-situ technologies. Together, these forces are reshaping procurement strategies, OEM partnerships, and regional infrastructure investments across refining, petrochemicals, chemical recycling, and low-carbon hydrogen value chains.

Market Trend: Refiners Accelerate Regeneration Cycles to Counter Specialty Catalyst Costs and Supply Chain Risk

Escalating platinum, palladium, and rare-earth prices have made fresh catalyst procurement a capital risk. Industrial benchmarks show lightly fouled hydroprocessing catalysts can recover 80% to 90% activity at roughly half the cost of replacement, positioning regeneration as a primary EBITDA lever. In 2025, Axens acquired Eurecat, signaling OEM alignment around lifecycle value rather than volume sales.

Operational innovation reinforces this shift. In-situ ozone oxidation now cuts CCR reactor turnaround by up to ten days versus off-site processing, reducing total maintenance costs by nearly 15%. These gains are driving adoption of CCR catalyst lifecycle management, precious metal recovery, and regeneration-as-a-service contracts.

Market Trend: Regeneration Technologies Adapt for Bio-Feedstocks and Plastic Pyrolysis Oil

Green refinery feedstocks introduce faster poisoning and complex fouling from silicon, chlorine, metals, and coke precursors. In 2024, Honeywell UOP confirmed Ecofining™ units use specialized catalysts optimized for regeneration under high-contaminant renewable diesel and SAF conditions. Parallelly, Topsoe’s HydroFlex™ platform shows advanced hydroprocessing catalysts retain selectivity during bio co-processing when paired with strict regeneration protocols.

Chemical recycling adds urgency. Plastic pyrolysis oil accelerates fouling up to threefold versus fossil feeds, creating strong demand for specialized oxidative regeneration and heavy contaminant removal. This is expanding markets for bio-feedstock catalyst regeneration and PPO catalyst cleaning services.

Market Opportunity: Developing Middle East Regeneration Hubs for Giga-Scale Chemical Complexes

Saudi Arabia’s shift toward integrated refining and chemicals is creating a localization window for catalyst regeneration providers. Vision 2030 targets seventy percent oil and gas supply-chain localization, supporting Aramco–SABIC crude-to-chemicals operations processing four hundred thousand barrels per day. Saudi Aramco’s iktva program reached sixty-seven percent local content in 2024, encouraging regional regeneration capacity.

Projects like Yanbu’s mixed-feed cracker will generate sustained demand for reforming and hydrotreating catalyst services. For international players, this opens multi-year opportunities in Middle East regeneration hubs, mobile processing units, and localized catalyst logistics.

Market Opportunity: Regeneration-as-a-Service for Distributed Blue Hydrogen Assets

Blue hydrogen scale-up introduces high-performance ATR and GHR catalysts that materially impact Levelized Cost of Hydrogen. Johnson Matthey’s LCH™ systems achieve over ninety-nine percent carbon capture, making regeneration contracts essential to preserving roughly twenty percent yield advantages over SMR.

In late 2025, Clariant and Technip Energies emphasized structured catalysts in EARTH platforms, which require precision cleaning to avoid pressure drops and protect CO2 reduction targets. Distributed hydrogen plants lack on-site facilities, creating demand for modular regeneration units and factory-grade restoration services.

Catalyst Regeneration Market Share and Segmentation Insights

Market Share by Type/Grade: Industrial Regeneration Dominates Volume While Semiconductor Grades Accelerate

Industrial grade accounts for 76% of catalyst regeneration demand in 2025, anchored by high-volume hydroprocessing (CoMo, NiMo), FCC catalysts, and precious metal systems used across petroleum refining, petrochemicals, and bulk chemical manufacturing. Refineries and large chemical plants favor regeneration because it delivers 50–70% cost savings versus fresh catalyst while reducing hazardous waste liabilities, supported by mature logistics networks and continuous process optimization. Pharmaceutical grade represents the second-largest, value-intensive segment, regenerating Pd/C, Pt/C, Rh/C, and Ru catalysts used in API synthesis under strict cGMP controls, impurity profiling, and batch traceability requirements. Electronic and semiconductor grade is the smallest but fastest-growing category, driven by ultra-high-purity regeneration for deposition and etching catalysts in advanced fabs, LEDs, and displays, where parts-per-billion contamination control, cleanroom processing, and full material characterization are mandatory. Domestic supply chain security and geopolitical risk mitigation are accelerating investment in North America and Europe.

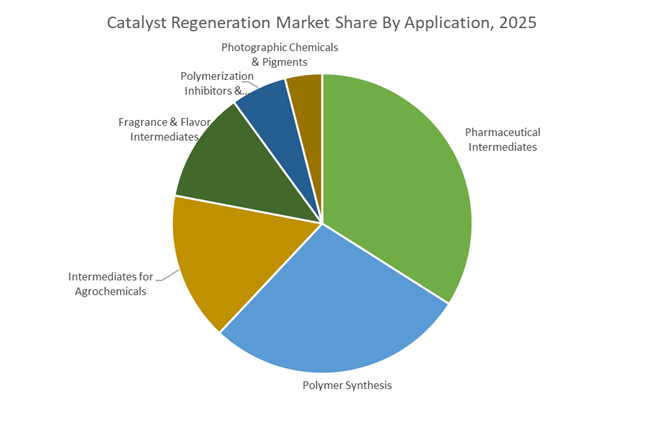

Market Share by Application: API Intermediates Lead as Polymers and Agrochemicals Optimize Costs

Pharmaceutical intermediates account for 34% of regenerated catalyst demand in 2025, reflecting heavy use of Pd, Pt, Rh, Ru systems in hydrogenation and cross-coupling reactions, with regeneration securing precious metal supply and lowering API manufacturing costs, especially across generic hubs in India and China. Polymer synthesis forms the second-largest segment, spanning Ziegler–Natta and metallocene polyolefin catalysts, polyester polymerization systems, molecular sieves, and supported metal oxides, closely tracking global polymer output and recycling initiatives. Agrochemical intermediates rely on regenerated hydrogenation and coupling catalysts for herbicides and fungicides, driven by patent expiries and cost optimization. Fragrance and flavor intermediates represent a growing specialty niche, preserving sensory purity in menthol, vanillin, and citral synthesis. Polymerization inhibitors and stabilizers remain steady, while photographic chemicals and pigments continue structural decline.

Competitive Landscape of the Catalyst Regeneration Market

The global catalyst regeneration market in 2026 is increasingly defined by closed-loop metals recovery, AI-driven regeneration control, subscription-based catalyst cycles, and energy-transition readiness. Competition centers on FCC and hydroprocessing catalyst regeneration, ex situ toll processing, presulphurization services, and digital lifecycle management. Market leaders are differentiating through precious metal reuse, modular CCR regenerators, renewable diesel and SAF catalyst handling, and advanced foulant mitigation, enabling refiners and chemical producers to extend catalyst life, reduce operating costs, and meet decarbonization targets. Rapid refinery modernization in Asia, renewable fuels expansion, and tighter ESG mandates are accelerating demand for high-efficiency catalyst reactivation, grading, and circular regeneration services worldwide.

Closed-loop catalyst circularity leadership from Axens Group / Eurecat

Axens transformed the 2026 catalyst regeneration landscape after acquiring 100% of Eurecat, creating the industry’s most vertically integrated catalyst lifecycle platform. Its strategy centers on metals reuse and circularity, recovering precious and base metals from spent catalysts and feeding them directly back into fresh catalyst production. The RAISE® reactivation process now leads palladium and nickel hydrogenation regeneration, outperforming traditional thermal burn-off. Axens also commercializes the SAS (Sample-Analyze-Segregate) service, allowing bin-level catalyst assessment to maximize reuse. With upgraded facilities across the Americas, Europe, the Middle East, and Asia, Axens is scaling regeneration for renewable diesel and SAF catalysts, strengthening its position in sustainable refining.

Subscription-based regeneration models pioneered by Ketjen Corporation

Ketjen emerged in 2026 as a standalone catalyst regeneration powerhouse following its separation from Albemarle under KPS Capital Partners. Its core strength lies in Refining Catalyst Solutions (RCS) for FCC and hydroprocessing units, supporting crude-to-chemicals optimization. Ketjen introduced a subscription-based regeneration model, enabling refiners to pay for active catalyst cycles instead of purchasing fresh material, shifting lifecycle risk to Ketjen. The company retained its Performance Catalyst Solutions plant in Texas while expanding regeneration hubs in India and Southeast Asia. By combining in-house manufacturing with toll regeneration and swap programs, Ketjen minimizes refinery downtime while delivering rapid access to regenerated catalyst inventory.

AI-enabled continuous regeneration platforms from Honeywell UOP

Honeywell UOP continues to dominate technology-driven catalyst regeneration through its CCR platforms and Everystep lifecycle services. The UOP Catalyst Regeneration Control System uses AI to manage catalyst transitions between reactor and regenerator atmospheres, maximizing uptime and safety. In 2026, UOP launched predictive regeneration capabilities that allow Platforming™ and Oleflex™ units to adapt regeneration rates based on real-time feedstock impurities. Its modular CCR regenerators are increasingly adopted as fixed-price, fixed-schedule refinery upgrades. Through Everystep digital twins, UOP integrates catalyst loading, startup, regeneration, and performance tracking into one ecosystem, positioning itself as a leader in smart, automated regeneration.

Ex situ hydroprocessing regeneration expertise from Porocel

Operating under Evonik, Porocel remains the global benchmark for ex situ catalyst regeneration and activated alumina services. Its 2026 strength lies in handling complex NiMo, CoMo, and NiCoMo hydroprocessing catalysts with precision grading and presulphurization. Porocel expanded digital operations using MPulse across five sites, improving technician productivity and turnaround speed. Its toll processing portfolio includes calcination, size reduction, and classification, enabling refiners to reclaim active pellets while removing fines. The actiCAT® presulphurization platform is now the industry standard, allowing faster hydrotreating startups with lower emissions and reduced operational risk.

Energy transition regeneration driven by Topsoe A/S

Topsoe leads the 2026 energy-transition segment of the catalyst regeneration market, focusing on SAF, green ammonia, and renewables hydrotreating. Following the appointment of Elena Scaltritti as CEO, Topsoe accelerated deployment of advanced regeneration-ready catalysts, including TK-3000 PhosTrap™, engineered for high-fouling renewable feedstocks. Its selection for major SAF projects in China highlights its dominance in renewables regeneration. Topsoe’s competitive edge lies in technology-catalyst synergy, designing both process units such as HydroFlex™ and the catalysts themselves. This integrated approach enables regeneration protocols precisely tailored to each unit’s operating history, improving reuse rates and lifecycle economics.

Foulant mitigation and pre-regeneration optimization by Crystaphase

Crystaphase differentiates as a “cat-nostic” specialist, operating at the intersection of filtration and catalyst regeneration. Its CatTrap® materials and internal filtration systems remove poisons and foulants before permanent deactivation, doubling reactor run times in some applications. Crystaphase applies forensic diagnostics using SEM and X-ray microtomography to identify root causes of catalyst failure, enabling targeted intervention. Rather than focusing on catalyst chemistry, the company optimizes the physical reactor environment to prevent crusting and hotspots. In 2026, Crystaphase plays a critical pre-regeneration role, ensuring catalysts reach recovery in optimal condition, regardless of brand or formulation.

United States: Excel® Rejuvenation Breakthroughs, 70% Cost Savings, and ESG-Driven Catalyst Life Extension

The United States catalyst regeneration industry is characterized by technological leadership in hydroprocessing catalyst rejuvenation, strong ESG alignment, and structured compliance timelines under federal regulation. In late 2024, Evonik Industries, through its Porocel acquisition, achieved a commercial milestone with its Excel® Rejuvenation technology. The process restores spent hydroprocessing catalysts to near-fresh activity by redistributing active metals such as molybdenum and cobalt across the support matrix, significantly extending catalyst life cycles in hydrotreating and hydrocracking units.

Economic benchmarks underscore the value proposition: 2025 industry data shows that U.S. refiners choosing catalyst rejuvenation instead of fresh catalyst procurement are achieving cost savings of up to 70% , equating to approximately $350,000 per $500,000 catalyst load. In July 2025, the U.S. Environmental Protection Agency issued an interim final rule extending Clean Air Act (NSPS OOOOb/c) compliance deadlines by 18 months, stabilizing catalyst change-out scheduling across refineries. Gulf Coast refiners increasingly favor rejuvenated catalysts to reduce greenhouse gas emissions associated with virgin catalyst manufacturing by nearly 60% , aligning with corporate decarbonization mandates. In December 2024, Ecovyst Inc. initiated a strategic review of its Advanced Materials & Catalysts segment, prioritizing high-performance zeolites and silica-based materials for sustainable fuels. Concurrently, U.S. academic-industrial collaborations have advanced Strong Metal-Support Interaction (SMSI) mechanisms to stabilize metallic nanoparticles during regeneration of magnetic catalysts, strengthening performance durability.

India: 310 MMTPA Refining Target, PLI Incentives, and National Catalyst R&D Drive Regeneration Capacity

India’s catalyst regeneration market is expanding in parallel with aggressive refining and petrochemical growth targets. The Ministry of Petroleum and Natural Gas confirmed in late 2025 that national refining capacity is on track to reach 310 MMTPA by 2030. Indian Oil Corporation is advancing a $2.09 billion Gujarat refinery expansion targeted for mid-2026 commissioning, further intensifying demand for hydrotreating catalyst regeneration and precious metal recovery services.

The establishment of the National Centre for Catalyst Research reflects a strategic push toward domestic manufacturing and life-cycle catalyst management for integrated refinery-petrochemical complexes. Under the Production Linked Incentive (PLI) scheme, the government is incentivizing recovery and regeneration of platinum group metals from spent automotive and industrial catalysts, reinforcing circular economy objectives. With India achieving 10% ethanol blending ahead of schedule, policy attention is shifting toward Sustainable Aviation Fuel (SAF), stimulating demand for bio-catalyst regeneration services in renewable diesel and aviation fuel units. State-owned refineries are upgrading crude units and expanding secondary petrochemical capacities in early 2026, generating consistent off-site regeneration requirements. In October 2025, Minister Hardeep Singh Puri reiterated India’s ambition to become the world’s second-largest refining power by 2035, necessitating large-scale third-party regeneration infrastructure.

China: Ethylene Oversupply, ETS Expansion, and Morphological Catalyst Engineering Accelerate Regeneration Demand

China’s catalyst regeneration industry is scaling in response to rapid ethylene expansion, emission control mandates, and coal-to-chemical (CTX) intensity. Ethylene capacity is forecast to reach an excess of 11.5 million tonnes in 2025, representing a 121% year-on-year increase. This polymerization surge is driving high-volume management and regeneration of Ziegler-Natta and metallocene catalysts used in polyethylene and polypropylene production.

In March 2025, China expanded its National Emissions Trading Scheme (ETS) to include steel, cement, and aluminum sectors, adding over 1,300 entities. This regulatory tightening elevates demand for high-efficiency SCR catalyst regeneration to maintain NOx compliance. The Ministry of Ecology and Environment indicated that national CO₂ emissions could peak in 2025, supported by circular carbon economy integration within chemicals manufacturing. In January 2026, Topsoe signed a landmark agreement with Tangshan Jinlihai for a major Sustainable Aviation Fuel project, emphasizing renewable catalyst systems. Coal consumption in the chemicals sector rose 20% year-on-year in H1 2025, expanding regeneration requirements for coal gasification and CTX catalysts. Chinese researchers have also piloted Ni/Ca3AlO catalysts with foliated morphologies, achieving a 65% reduction in carbon deposition during biomass gasification, enhancing regeneration cycles and catalyst longevity.

European Union: SOEC Manufacturing Scale-Up, REACH 2025 Reform, and Green Ammonia Catalyst Deployment

The European Union is emerging as a net-zero catalyst technology hub, combining regulatory reform with large-scale green hydrogen and ammonia investments. In early 2026, Topsoe inaugurated Europe’s largest Solid Oxide Electrolyzer Cell (SOEC) manufacturing facility and upgraded its 2025 EBIT guidance to 8.9% , reflecting surging demand for energy transition catalysts. The revised REACH Regulation, scheduled for release in Q4 2025 by the European Commission, will introduce Digital Product Passports and stricter biodegradability standards for catalyst additives, increasing traceability in regeneration supply chains.

In December 2025, the world’s first dynamic green ammonia plant commenced operations in Denmark through collaboration among Skovgaard Energy, Topsoe, and Vestas, utilizing next-generation catalysts optimized for intermittent renewable power input. Topsoe’s partnership with Maersk Training is setting new safety benchmarks for catalyst handling and regeneration in Power-to-X systems. Recognition through the S&P Platts Global Energy Award for Excellence in Chemicals in late 2025 underscores Europe’s leadership in circular catalyst regeneration solutions for energy-intensive industries.

Saudi Arabia: Green Hydrogen Mega-Projects and Circular Carbon Economy Drive Regeneration Services

Saudi Arabia’s catalyst regeneration market is expanding under Vision 2030 and Circular Carbon Economy (CCE) frameworks. In January 2026, Topsoe was selected to support green ammonia production at ACWA Power’s Yanbu Green Hydrogen Project, highlighting the Kingdom’s commitment to renewable catalyst systems.

The 2025 national budget continues substantial investment in the Saudi Green Initiative (SGI), activating more than 85 programs with a combined investment of SAR 705 billion. Saudi Arabia is prioritizing regeneration of catalysts used in carbon capture, utilization, and storage (CCUS) projects as part of its CCE strategy. A $182 million mineral exploration incentive launched in 2025 aims to secure domestic supplies of catalyst-critical minerals, strengthening feedstock security for refinery and petrochemical regeneration hubs. These integrated policies position Saudi Arabia as a major growth center for catalyst life-cycle management services across refining and green hydrogen sectors.

South Korea: Record R&D Funding and Hydrogen Economy Transition Expand Catalyst Life-Cycle Services

South Korea’s catalyst regeneration industry is supported by record public R&D investment and a national hydrogen economy strategy. The government allocated KRW 24.8 trillion to R&D in 2025, the highest in its history, prioritizing advanced biotechnology and carbon-free energy technologies that require sophisticated catalyst management.

Hydrogen production, storage, and utilization projects demand specialized regeneration services for reforming, ammonia cracking, and fuel cell catalysts. During Korea Green Innovation Days (KGID) 2025, South Korea reaffirmed its technology partnership role with the World Bank, showcasing AI-driven pollution control and waste minimization solutions applicable to catalyst regeneration operations. The integration of digital monitoring, carbon-neutral hydrogen production, and AI-enhanced regeneration processes positions South Korea as a technologically advanced catalyst life-cycle services market within Asia-Pacific.

Catalyst Regeneration Market Report Scope

Catalyst Regeneration Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.3 Billion

|

|

Market Size (2034)

|

$16.7 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Type/Grade (Industrial Grade, Pharmaceutical Grade, Electronic/Semiconductor Grade), By Form (Crystalline/Flakes, Molten), By Production Method (Phenol Hydroxylation, Cumene Process, Bio-based/Microbial Fermentation), By Application (Intermediates for Agrochemicals, Fragrance & Flavor Intermediates, Pharmaceutical Intermediates, Polymerization Inhibitors & Stabilizers, Polymer Synthesis, Photographic Chemicals & Pigments), By End-User (Agriculture, Pharmaceuticals & Healthcare, Food & Beverages, Cosmetics & Personal Care, Electronics & Electrical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Solvay, UBE Industries, Ltd., Camlin Fine Sciences Ltd., Jiangsu Sanjili Chemical Co., Ltd., Lianyungang Sanjili Chemical Industry Co., Ltd., Hubei YuanCheng Saichuang Technology Co., Ltd., Brother Enterprises Holding Co., Ltd., Mitsui Chemicals, Inc., Merck KGaA, Tokyo Chemical Industry Co., Ltd., Alfa Aesar, Huntsman Corporation, Zhejiang Zhongxin Fluoride Materials Co., Ltd., Eni S.p.A., Sisco Research Laboratories Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Catalyst Regeneration Market Segmentation

By Type/Grade

- Industrial Grade

- Pharmaceutical Grade

- Electronic/Semiconductor Grade

By Form

- Crystalline/Flakes

- Molten

By Production Method

- Phenol Hydroxylation

- Cumene Process

- Bio-based/Microbial Fermentation

By Application

- Intermediates for Agrochemicals

- Fragrance & Flavor Intermediates

- Pharmaceutical Intermediates

- Polymerization Inhibitors & Stabilizers

- Polymer Synthesis

- Photographic Chemicals & Pigments

By End-User

- Agriculture

- Pharmaceuticals & Healthcare

- Food & Beverages

- Cosmetics & Personal Care

- Electronics & Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Catalyst Regeneration Industry

- Solvay, UBE Industries, Ltd.

- Camlin Fine Sciences Ltd.

- Jiangsu Sanjili Chemical Co., Ltd.

- Lianyungang Sanjili Chemical Industry Co., Ltd.

- Hubei YuanCheng Saichuang Technology Co., Ltd.

- Brother Enterprises Holding Co., Ltd.

- Mitsui Chemicals, Inc.

- Merck KGaA

- Tokyo Chemical Industry Co., Ltd.

- Alfa Aesar

- Huntsman Corporation

- Zhejiang Zhongxin Fluoride Materials Co., Ltd.

- Eni S.p.A.

- Sisco Research Laboratories Pvt. Ltd.

*- List not Exhaustive