Phosphate Esters Market Size, Flame Retardant Demand, and Specialty Chemical Expansion

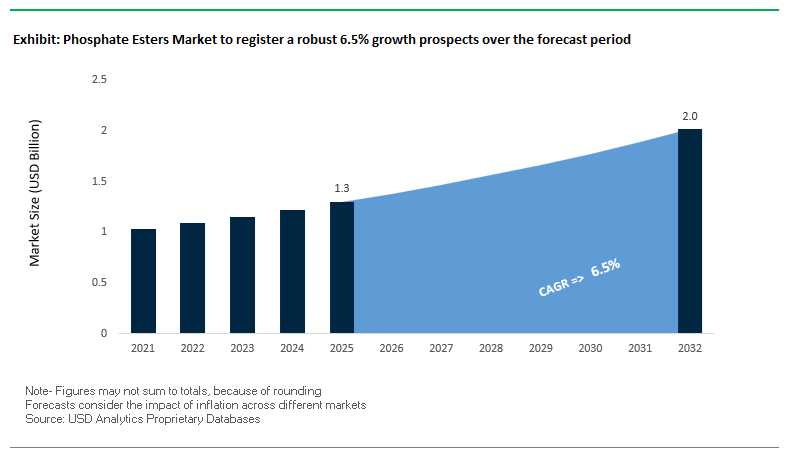

The global Phosphate Esters Market was valued at $1.3 billion in 2025 and is projected to grow at a CAGR of 6.5% through 2032, reaching $2 billion by 2032. This growth is underpinned by rising demand for non-halogenated flame retardants, high-performance lubricants, plasticizers, and specialty additives across coatings, electronics, automotive, and industrial applications.

Phosphate esters are increasingly critical in applications requiring thermal stability, flame resistance, and anti-wear properties, particularly in high-risk environments such as electrical systems, aerospace components, hydraulic fluids, and industrial coatings. The global shift away from halogenated flame retardants, driven by environmental and health concerns, is significantly accelerating the adoption of phosphorus-based alternatives, positioning phosphate esters as a preferred solution under evolving regulatory frameworks such as the EU Green Deal and US environmental policies.

Another major growth driver is the increasing use of phosphate esters as functional additives in advanced coatings and adhesives, where they enhance adhesion, corrosion resistance, and chemical durability. The rise of high-performance materials in EV batteries, renewable energy systems, and electronics manufacturing is further expanding their application scope. Additionally, phosphate esters play a key role as surfactants and emulsifiers, particularly in industrial cleaning and lubricant formulations, supporting steady demand across process industries.

The market is also benefiting from the broader transition toward a circular phosphorus economy, where recycling and sustainable sourcing of phosphorus are becoming strategic priorities. Regional demand is particularly strong in Asia-Pacific, supported by expanding manufacturing capacity and increasing investments in electronics, construction, and specialty chemicals production.

Recent developments in the Phosphate Esters Market reflect a strong interplay between regulatory transformation, innovation in sustainable chemistries, and evolving supply chain dynamics. A key trend is the strategic shift toward non-halogenated flame retardants, highlighted by Lanxess’ January 2026 pivot toward phosphorus-based alternatives, aligning with stringent environmental regulations and phasing out legacy halogenated additives.

Innovation in high-performance materials is accelerating. Evonik’s VISIOMER® HEMA-P 100, introduced in 2024 and expanded commercially through 2025, represents a new class of phosphate methacrylate monomers designed for advanced coatings and adhesives. These materials offer enhanced adhesion, corrosion resistance, and flame retardancy, addressing the growing demand for multifunctional additives in high-performance applications.

Supply chain dynamics and pricing pressures are also influencing market behavior. BASF’s January 2025 price increase for alkyl phosphate ester systems reflects rising raw material costs and the impact of anti-dumping duties on Chinese imports, which have reshaped the competitive landscape in North America. This has prompted formulators to reassess sourcing strategies and explore alternative supply channels.

Sustainability and circular economy initiatives are gaining traction. ICL Group’s launch of Puraloop® (March 2024, ramping through 2025) demonstrates a broader move toward recycled phosphorus inputs, which could influence the long-term sustainability profile of phosphate ester production. Additionally, ICL’s new facility in Maharashtra, India (March 2026) strengthens regional supply capabilities for phosphorus-based specialty chemicals, supporting growing demand in Asia.

Capacity expansion and portfolio optimization are also shaping the competitive landscape. PCC SE’s continued investment in surfactants and derivatives production (August 2025) supports growth in phosphate ester-based emulsifiers, while Solvay’s transition to an “Essential Chemistry” focus (March 2026) emphasizes core phosphorus building blocks for industrial applications. Meanwhile, Sherwin-Williams’ acquisition of BASF’s decorative paints business consolidates demand-side dynamics, increasing buyer concentration for specialty additives.

Market Trend: Halogen-Free Phosphate Ester Flame Retardants Accelerating Adoption in EV Battery Enclosures

The phosphate esters industry is gaining strong traction in electric vehicle applications as OEMs transition toward halogen-free flame retardant systems for battery enclosures. This shift is driven by the need to reduce smoke toxicity, eliminate corrosive halogen byproducts, and ensure electrical reliability in high-voltage architectures exceeding 800V. Phosphate ester-based additives such as resorcinol bis(diphenyl phosphate) and bisphenol A bis(diphenyl phosphate) are emerging as preferred solutions in PC/ABS battery housing materials.

These phosphate ester flame retardants offer high thermal stability, with decomposition temperatures typically in the range of 300°C to 310°C at 5% weight loss. This ensures that battery enclosures maintain structural integrity during localized thermal runaway events, providing critical containment in advanced EV systems. In addition, dielectric performance is a key advantage. Phosphate ester additives maintain high comparative tracking index values, often reaching 600V, which minimizes the risk of electrical leakage and short circuits in compact battery module designs.

Material efficiency is also improving. In standard PC/ABS formulations, loading levels between 8% and 15% are sufficient to achieve UL 94 V-0 flame retardancy at thicknesses around 1.5 mm. This allows manufacturers to design thinner and lighter enclosures without compromising safety performance, contributing to overall vehicle weight reduction and energy efficiency. These combined attributes are positioning halogen-free phosphate esters as a critical material class in next-generation electric mobility.

Market Trend: Phosphate Ester Hydraulic Fluids Enhancing Fire Safety and Performance in Aviation Systems

The aviation industry is increasingly standardizing phosphate ester-based hydraulic fluids to meet stringent fire resistance and operational performance requirements. Trialkyl phosphate esters such as tributyl phosphate and tris(2-ethylhexyl) phosphate are widely used in aircraft hydraulic systems due to their superior fire safety characteristics compared to conventional mineral oil-based fluids.

Phosphate ester hydraulic fluids exhibit significantly higher fire points, typically exceeding 230°C, compared to approximately 150°C for mineral oils. This elevated fire resistance reduces the likelihood of ignition in the event of high-pressure fluid leaks, enhancing overall aircraft safety. Additionally, these fluids demonstrate auto-ignition temperatures above 400°C, providing a substantial safety margin in areas exposed to high thermal loads, such as near engine bleed-air systems.

Performance across temperature extremes is another critical factor. Aviation-grade phosphate esters maintain stable viscosity over a wide operational range, from approximately −54°C to +135°C. This ensures consistent hydraulic response in both high-altitude cold conditions and high-temperature operating environments. The combination of fire resistance, thermal stability, and consistent viscosity is driving the continued adoption of phosphate ester fluids in modern aircraft systems.

Market Opportunity: FAA Fire Safety Regulations Driving Demand for Phosphate Ester Flame Retardants in Aircraft Interiors

Regulatory requirements in the aviation sector are creating sustained demand for phosphate ester-based flame retardants, particularly under the Federal Aviation Administration’s fire safety standards for aircraft interiors. Compliance with vertical burn and heat release criteria is essential for materials used in cabin panels, seating structures, and storage compartments.

Aircraft interior materials must meet strict self-extinguishing requirements, including limits on burn length and flame duration after ignition source removal. Phosphate ester-based additives enable polymer systems to meet these criteria by promoting char formation and reducing flame propagation. In addition, large surface components must comply with peak heat release limits, where phosphate ester-modified resins consistently demonstrate superior performance compared to non-phosphorus alternatives.

As aircraft manufacturers continue to prioritize passenger safety and regulatory compliance, the demand for high-performance, phosphorus-based flame retardants is expected to grow. Suppliers capable of delivering consistent performance across multiple polymer systems are well positioned to benefit from this regulatory-driven demand.

Market Opportunity: China GMP Enforcement Driving High-Purity Phosphate Ester Demand in Pharmaceutical Applications

China’s implementation of updated Good Manufacturing Practice requirements is creating a significant opportunity for high-purity phosphate esters used in pharmaceutical and medical applications. These regulations introduce stricter controls on excipient quality, particularly for materials used in medical tubing, drug delivery systems, and pharmaceutical packaging.

Manufacturers are now required to implement comprehensive quality management systems to control impurities, including residual monomers and catalysts in phosphate ester formulations. This is driving a shift toward high-purity, medical-grade products that meet stringent safety and compliance standards.

The regulatory framework also introduces mandatory supplier audits by marketing authorization holders, increasing transparency across the supply chain. Phosphate ester producers must demonstrate consistent product quality, traceability, and compliance with regulatory requirements to maintain market access.

This heightened level of scrutiny is favoring established suppliers with advanced production capabilities and robust quality systems. As the pharmaceutical sector in China continues to expand, demand for compliant, high-purity phosphate ester excipients is expected to increase, creating long-term growth opportunities in this specialized segment.

Phosphate Esters Market Share and Segmentation Insights

Liquid Form Captures 78.3% Share Driven by Aviation and Industrial Fluid Applications

The phosphate esters market by physical form is overwhelmingly led by the liquid segment, accounting for 78.3% of global market share in 2025, primarily due to its critical role in fire-resistant hydraulic fluids and industrial lubricants. Liquid phosphate esters, particularly triaryl and alkyl phosphate esters, are widely used in aviation systems, power generation turbines, and high-pressure industrial presses, where flammability resistance and thermal stability are essential for safety and performance. Their ease of handling, blending, and compatibility with other chemical systems makes them ideal for incorporation into lubricants, flame-retardant plastics, and specialty industrial cleaners. As industries increasingly prioritize fire safety, operational reliability, and high-performance fluid systems, liquid phosphate esters continue to dominate the global specialty chemicals and functional fluids market, reinforcing their position as the backbone of high-temperature, fire-resistant applications.

Direct Sales Hold 55.4% Share Driven by Custom Formulation and Quality Assurance Needs

In the phosphate esters market by sales channel, direct sales dominate with a 55.4% market share in 2025, reflecting the importance of technical customization and strict quality control in end-use applications. Industries such as aerospace, defense, and power generation require highly specialized phosphate ester formulations that meet stringent standards like MIL-PRF-83282 and Skydrol specifications, necessitating close collaboration between manufacturers and suppliers. Direct engagement ensures precise control over viscosity, oxidation stability, hydrolysis resistance, and additive compatibility, which are critical for performance in mission-critical systems. Additionally, these sectors demand full batch traceability, Certificates of Analysis (COA), and regulatory compliance documentation, which are more reliably provided through direct supplier relationships than through intermediaries. As application complexity and regulatory scrutiny increase, direct sales continue to dominate the global phosphate ester distribution landscape.

Competitive Landscape of the Phosphate Esters Market

LANXESS Leads Phosphate Ester Innovation with Bio-Based and E-Mobility Solutions

LANXESS AG is a dominant player in the phosphate esters market, leveraging its Polymer Additives business to deliver high-performance phosphorus-based chemicals. Its Disflamoll® and Levagard® product lines are widely used as flame retardants and plasticizers in PVC, polyurethane, and elastomers. Between 2025 and 2026, LANXESS expanded its Scope 3 neutral product portfolio by incorporating bio-based raw materials into phosphate ester production. The company’s strong vertical integration enables high-purity manufacturing of key compounds such as TCP and IPPP. Additionally, LANXESS is targeting the growing e-mobility market, developing advanced phosphate ester-based electrolytes and safety solutions for battery systems.

Solvay Expands Specialty Phosphate Ester Applications with Sustainable Chemical Solutions

Solvay S.A. is a global leader in functional phosphate ester chemistry, serving industries such as agrochemicals, mining, and metalworking. The company reported strong financial performance, with €4.3 billion in net sales driven by specialty surfactants and performance chemicals. Its Rhodafac® series of ethoxylated phosphate esters plays a critical role in emulsion polymerization and agricultural formulations. Solvay has achieved a 29% reduction in Scope 1 and 2 emissions, positioning itself as a leader in low-carbon phosphate ester production. The expansion of its Coatis business line further strengthens its presence in eco-friendly solvents and surface treatment solutions, particularly in Latin America.

ICL Strengthens Market Position with Vertically Integrated Phosphate Solutions and Flame Retardants

ICL Group is one of the most vertically integrated players in the phosphate esters market, leveraging its phosphate rock resources to ensure cost efficiency and supply stability. In 2026, the company projected an adjusted EBITDA between $1.4 billion and $1.6 billion, supported by strong demand for phosphorus-based flame retardants. Its Fyrol™ and Phosflex™ Next-Gen product lines offer halogen-free phosphate esters for polyurethane foams, addressing regulatory and environmental requirements. ICL has also expanded its market share in North America due to anti-dumping policies on imported chemicals. Its acquisition of Bartek Ingredients enhances its global reach and strengthens its portfolio of specialty phosphate-based additives.

Clariant Advances High-Performance Phosphate Esters with Digital Innovation and Sustainable Additives

Clariant AG is a key innovator in the specialty phosphate esters market, focusing on high-value applications in personal care, lubricants, and industrial formulations. Its Hostaphat® range is widely used as emulsifiers and performance additives in both consumer and industrial products. The company reported a strong EBITDA margin of 17.8%, driven by its focus on specialty chemicals. Clariant’s CLARITY™ digital platform uses AI-driven simulations to optimize phosphate ester molecular design, enhancing performance and thermal stability. Its strategic focus on non-halogenated flame retardants aligns with global electronics industry requirements, reinforcing its leadership in sustainable additive technologies.

BASF Expands Phosphate Ester Production with Verbund Integration and Industrial Applications

BASF SE is a major player in the global phosphate esters market, leveraging its integrated Verbund system to deliver cost-efficient and high-volume production. In 2026, the company expanded its capacity through the Zhanjiang Verbund site in China, strengthening its presence in Asia-Pacific. BASF’s Irgalube® series provides high-performance lubricant additives with exceptional anti-wear properties for automotive and industrial applications. Its strategic divestment of decorative paints allows greater focus on industrial chemicals and high-growth segments. Through efficient resource utilization and recycling, BASF enhances sustainability in phosphate ester production, reinforcing its competitive position in performance chemicals and industrial additives.

Elementis Strengthens Specialty Additives Portfolio with Advanced Rheology and Digital Formulation Tools

Elementis PLC is a premium specialty chemicals company focusing on high-value phosphate ester-based additives and rheological solutions. Under its “Elevate Elementis” strategy, the company aims to achieve over 23% operating profit margins by 2026 through a focus on niche chemistries. Its expansion of technical service hubs in Asia supports customized solutions for durable coatings and industrial applications. Elementis leverages its unique hectorite resources combined with phosphate ester technologies to deliver advanced rheology control systems. Additionally, its AI-driven formulation tools have reduced product development cycles by 30%, enhancing its competitiveness in the specialty additives and performance coatings market.

China: High-Purity Scale-Up and EV Thermal Management Leadership

China dominates the global phosphate esters market in volume, while rapidly transitioning toward ultra-high-purity and high-performance applications across semiconductors and EVs. Manufacturers are scaling production of semiconductor-grade dielectric fluids, achieving sub-ppb impurity levels for advanced cooling systems in high-precision fabrication environments.

Regulatory shifts under GB 30981.1-2025 are accelerating the transition toward halogen-free triaryl phosphate esters, particularly in construction and industrial coatings. The rapid growth of the NEV sector is driving innovation in phosphate ester-based battery coolants, which have demonstrated up to 22% improvement in cell longevity under fast-charging conditions.

China is also strengthening its industrial ecosystem through investments in clusters like Nanjing, supporting CFRP dispersants and specialty surfactants. Additionally, the shift toward biodegradable phosphate ester plasticizers in medical-grade PVC and the rising use of phosphate ester surfactants in agriculture highlight China’s expansion into sustainable and multifunctional applications.

United States: Aerospace Resilience and PFAS-Free Transformation

The United States phosphate esters market is defined by high-performance applications and regulatory-driven innovation, particularly in aerospace, infrastructure, and mining sectors. Phosphate ester-based fire-resistant hydraulic fluids (Type IV & V) remain critical in aviation, with proven durability exceeding 1,200 hours under extreme ISO standards.

The PFAS phase-out (2026) is accelerating demand for non-fluorinated phosphate ester alternatives in packaging, textiles, and coatings. Infrastructure investments under the IIJA are further driving demand for intumescent coatings containing alkyl phosphate esters, particularly in tunnels and bridges.

Innovation is also advancing sustainability, with the introduction of bio-circular lubricant esters such as OQ Chemicals’ OxReduce L7 NPG. Additionally, stricter safety compliance in mining operations has increased adoption of triaryl phosphate ester fluids, reinforcing the U.S. leadership in high-reliability and safety-critical applications.

Germany: Circular Chemistry and Halogen-Free Innovation

Germany leads Europe’s phosphate esters market through its commitment to circular economy principles and halogen-free chemistry. The country is at the forefront of developing halogen-free flame retardants (HFFR), with companies like Lanxess expanding advanced phosphate ester product lines for electrohydraulic systems and turbine control.

Strategic consolidation, such as Lanxess’ acquisition of IFF’s microbial control division, is strengthening the integration of antimicrobial technologies into phosphate ester formulations. Germany is also pioneering digital tracer integration, enabling recycling systems to achieve up to 99% sorting accuracy in polymer applications.

Growth in offshore wind energy is driving demand for biodegradable phosphate ester lubricants, while investments in facilities like the Münster technical hub are accelerating the development of waterborne emulsifiers. Additionally, R&D in hydrogen transport systems is exploring phosphate ester-based coatings to manage friction and static buildup in high-pressure environments.

Japan: Precision Additives and High-Tech Electronics Integration

Japan remains a global leader in precision phosphate ester applications, particularly in electronics, optics, and advanced materials. The development of ultra-pure dielectric fluids is supporting the country’s 6G telecommunications rollout, ensuring reliability in high-speed fiber-optic systems.

Innovations include photocatalytic phosphate ester hybrids, such as ARITERAS KPC, which decompose pollutants in enclosed environments. Japan is also advancing active packaging solutions, where oxygen-scavenging phosphate esters extend shelf life without additional materials.

The automotive sector is driving demand for high-performance leveling agents, improving surface finish and durability in premium EV coatings. Additionally, strict regulatory frameworks are pushing the development of ultra-low migration plasticizers for medical-grade materials, reinforcing Japan’s leadership in high-purity, high-performance chemical solutions.

India: Agricultural Modernization and Manufacturing Expansion

India is emerging as a high-growth phosphate esters market, driven by agricultural modernization and domestic manufacturing initiatives. The adoption of phosphate ester-based agricultural adjuvants, such as Nouryon’s Agrilan 1028, is improving efficiency in high-electrolyte farming systems.

Government initiatives under “Make in India” and PLI schemes are boosting demand for phosphate ester-based materials in electronics manufacturing, particularly for flame-retardant casings and dielectric components. Infrastructure projects under the Smart Cities Mission are also increasing demand for intumescent coatings, driving consumption of alkyl phosphate esters.

The automotive sector is contributing to growth through increased demand for phosphate ester lubricant additives in high-performance gear oils. Additionally, the country’s push toward sustainable agriculture is driving a 12% annual increase in demand for phosphate ester surfactants, reinforcing India’s position as a key emerging market.

South Korea: Semiconductor Safety and Advanced Marine Applications

South Korea’s phosphate esters market is driven by its leadership in semiconductors, electronics, and advanced marine coatings. The country is a major producer of plasma-resistant phosphate ester coatings, essential for fabrication processes such as 3D NAND and FinFET technologies.

Technological advancements include low-voltage curing phosphate esters (<160V), enabling applications in flexible electronics and thin-film substrates. South Korea is also leading innovation in marine anti-fouling coatings, utilizing phosphate ester binders to prevent biological growth without toxic biocides.

The country’s dominance in OLED display manufacturing is driving demand for phosphate ester-based thin-film encapsulation (TFE) materials, while its expertise in retort packaging supports global leadership in high-barrier adhesion technologies. Additionally, the K-Beauty industry is influencing demand for high-performance surfactants in premium packaging applications.

Saudi Arabia: Localization Strategy and Energy Transition Applications

Saudi Arabia is rapidly expanding its phosphate esters market through localization initiatives and energy sector investments under the IKTVA program. The establishment of domestic esterification facilities is supporting large-scale projects such as the Jafurah gas field, reducing reliance on imports.

The country is deploying phosphate ester-based fire-resistant hydraulic fluids in gas turbines, capable of operating at temperatures exceeding 450°C without ignition. Growth in desalination infrastructure is also driving demand for phosphate ester scale inhibitors in water transport systems.

R&D efforts are focused on abrasion-resistant phosphate-ceramic hybrid coatings to withstand harsh desert conditions. Additionally, mega-projects such as NEOM are boosting demand for flame-retardant coatings in construction, while early-stage investments in green hydrogen infrastructure are creating new opportunities for phosphate ester-based conductive coatings.

Phosphate Esters Market Report Scope

Phosphate Esters Market

Parameter

Details

Market Size (2025)

$1.3 Billion

Market Size (2032)

$2 Billion

Market Growth Rate

6.5%

Segments

By Type (Triaryl Phosphate Esters, Trialkyl Phosphate Esters, Alkyl Aryl Phosphate Esters, Other Specialty Esters), By Base Material (Alcohol Based, Ethoxylated Alcohol Based, Ethoxylated Phenol Based), By Physical Form (Liquid, Solid, Semi-Solid), By End-Use Industry (Polymer and Plastics Processing, Automotive and Transportation, Aerospace and Defense, Building and Construction, Electronics and Electrical, Oil and Gas, Agrochemicals, Textile and Leather, Industrial Cleaning and Metalworking Fluids), By Functional Property (Halogen-Free Flame Retardancy, High Thermal and Oxidative Stability, Low Volatility, Bio-degradability, Hydrolytic Stability), By Sales Channel (Direct Sales, Specialty Chemical Distributors, Technical Blenders and Additive Package Providers)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

LANXESS AG, ICL Group Ltd., Solvay S.A., Clariant AG, BASF SE, Exxon Mobil Corporation, Eastman Chemical Company, Elementis plc, The Lubrizol Corporation, Evonik Industries AG, Croda International Plc, Dai-ichi Kogyo Seiyaku Co., Ltd., PCC Group, Kao Corporation, Stepan Company

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Phosphate Esters Market Segmentation

By Type

Triaryl Phosphate Esters

Triphenyl Phosphate

Tricresyl Phosphate

Isopropylated Triphenyl Phosphate

Trialkyl Phosphate Esters

Tributyl Phosphate

Triisobutyl Phosphate

Tris

Alkyl Aryl Phosphate Esters

Other Specialty Esters

By Base Material

Alcohol Based

Ethoxylated Alcohol Based

Ethoxylated Phenol Based

By Physical Form

Liquid

Solid

Semi-Solid

By End-Use Industry

Polymer and Plastics Processing

Automotive and Transportation

Aerospace and Defense

Building and Construction

Electronics and Electrical

Oil and Gas

Agrochemicals

Textile and Leather

Industrial Cleaning and Metalworking Fluids

By Functional Property

Halogen-Free Flame Retardancy

High Thermal and Oxidative Stability

Low Volatility

Bio-degradability

Hydrolytic Stability

By Sales Channel

Direct Sales

Specialty Chemical Distributors

Technical Blenders and Additive Package Providers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Phosphate Esters Industry

LANXESS AG

ICL Group Ltd.

Solvay S.A.

Clariant AG

BASF SE

Exxon Mobil Corporation

Eastman Chemical Company

Elementis plc

The Lubrizol Corporation

Evonik Industries AG

Croda International Plc

Dai-ichi Kogyo Seiyaku Co., Ltd.

PCC Group

Kao Corporation

Stepan Company

*- List not Exhaustive

Table of Contents: Phosphate Esters Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Phosphate Esters Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Phosphate Esters Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Demand Drivers in Non-Halogenated Flame Retardants, Lubricants, and Specialty Additives

2.4. Regulatory Trends and Sustainability Standards in Circular Phosphorus Economy and Green Chemistry

2.5. Strategic Opportunities and Future Outlook

3. Innovations Reshaping the Phosphate Esters Market

3.1. Trend: Halogen-Free Phosphate Ester Flame Retardants Accelerating Adoption in EV Battery Enclosures

3.2. Trend: Phosphate Ester Hydraulic Fluids Enhancing Fire Safety and Performance in Aviation Systems

3.3. Opportunity: FAA Fire Safety Regulations Driving Demand for Phosphate Ester Flame Retardants in Aircraft Interiors

3.4. Opportunity: China GMP Enforcement Driving High-Purity Phosphate Ester Demand in Pharmaceutical Applications

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Phosphate Esters Market

5.1. By Type

5.1.1. Triaryl Phosphate Esters

5.1.2. Triphenyl Phosphate

5.1.3. Tricresyl Phosphate

5.1.4. Isopropylated Triphenyl Phosphate

5.1.5. Trialkyl Phosphate Esters

5.1.6. Tributyl Phosphate

5.1.7. Triisobutyl Phosphate

5.1.8. Tris Phosphate Esters

5.1.9. Alkyl Aryl Phosphate Esters

5.1.10. Other Specialty Esters

5.2. By Base Material

5.2.1. Alcohol Based

5.2.2. Ethoxylated Alcohol Based

5.2.3. Ethoxylated Phenol Based

5.3. By Physical Form

5.3.1. Liquid

5.3.2. Solid

5.3.3. Semi-Solid

5.4. By End-Use Industry

5.4.1. Polymer and Plastics Processing

5.4.2. Automotive and Transportation

5.4.3. Aerospace and Defense

5.4.4. Building and Construction

5.4.5. Electronics and Electrical

5.4.6. Oil and Gas

5.4.7. Agrochemicals

5.4.8. Textile and Leather

5.4.9. Industrial Cleaning and Metalworking Fluids

5.5. By Functional Property

5.5.1. Halogen-Free Flame Retardancy

5.5.2. High Thermal and Oxidative Stability

5.5.3. Low Volatility

5.5.4. Biodegradability

5.5.5. Hydrolytic Stability

5.6. By Sales Channel

5.6.1. Direct Sales

5.6.2. Specialty Chemical Distributors

5.6.3. Technical Blenders and Additive Package Providers

6. Country Analysis and Outlook of Phosphate Esters Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Saudi Arabia

6.19. United Arab Emirates

6.20. Rest of Middle East and Africa

7. Phosphate Esters Market Size Outlook by Region (2025–2034)

7.1. North America Phosphate Esters Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Base Material

7.1.3. By Physical Form

7.1.4. By End-Use Industry

7.1.5. By Functional Property

7.1.6. By Sales Channel

7.2. Europe Phosphate Esters Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Base Material

7.2.3. By Physical Form

7.2.4. By End-Use Industry

7.2.5. By Functional Property

7.2.6. By Sales Channel

7.3. Asia Pacific Phosphate Esters Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Base Material

7.3.3. By Physical Form

7.3.4. By End-Use Industry

7.3.5. By Functional Property

7.3.6. By Sales Channel

7.4. South and Central America Phosphate Esters Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Base Material

7.4.3. By Physical Form

7.4.4. By End-Use Industry

7.4.5. By Functional Property

7.4.6. By Sales Channel

7.5. Middle East and Africa Phosphate Esters Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Base Material

7.5.3. By Physical Form

7.5.4. By End-Use Industry

7.5.5. By Functional Property

7.5.6. By Sales Channel

8. Company Profiles: Leading Players in the Phosphate Esters Market

8.1. LANXESS AG

8.2. ICL Group Ltd.

8.3. Solvay S.A.

8.4. Clariant AG

8.5. BASF SE

8.6. Exxon Mobil Corporation

8.7. Eastman Chemical Company

8.8. Elementis plc

8.9. The Lubrizol Corporation

8.10. Evonik Industries AG

8.11. Croda International Plc

8.12. Dai-ichi Kogyo Seiyaku Co., Ltd.

8.13. PCC Group

8.14. Kao Corporation

8.15. Stepan Company

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Phosphate Esters Market Segmentation

By Type

Triaryl Phosphate Esters

Triphenyl Phosphate

Tricresyl Phosphate

Isopropylated Triphenyl Phosphate

Trialkyl Phosphate Esters

Tributyl Phosphate

Triisobutyl Phosphate

Tris

Alkyl Aryl Phosphate Esters

Other Specialty Esters

By Base Material

Alcohol Based

Ethoxylated Alcohol Based

Ethoxylated Phenol Based

By Physical Form

Liquid

Solid

Semi-Solid

By End-Use Industry

Polymer and Plastics Processing

Automotive and Transportation

Aerospace and Defense

Building and Construction

Electronics and Electrical

Oil and Gas

Agrochemicals

Textile and Leather

Industrial Cleaning and Metalworking Fluids

By Functional Property

Halogen-Free Flame Retardancy

High Thermal and Oxidative Stability

Low Volatility

Bio-degradability

Hydrolytic Stability

By Sales Channel

Direct Sales

Specialty Chemical Distributors

Technical Blenders and Additive Package Providers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global Phosphate Esters Market was valued at $1.3 billion in 2025 and is projected to reach $2 billion by 2032, expanding at a CAGR of 6.5%. Market growth is being driven by rising demand for halogen-free flame retardants, fire-resistant hydraulic fluids, specialty lubricants, and multifunctional additives across automotive, electronics, aerospace, and industrial applications.

Phosphate ester flame retardants are increasingly preferred in EV battery enclosures and advanced electronics because they provide high thermal stability, low smoke toxicity, and excellent dielectric performance without relying on halogenated chemistries. These additives enable thinner and lighter battery housing materials while maintaining UL 94 V-0 flame resistance, helping EV manufacturers improve safety, weight reduction, and electrical reliability in high-voltage systems.

Global regulatory initiatives such as the EU Green Deal, PFAS phase-outs, and stricter environmental compliance standards are accelerating the transition toward non-halogenated and sustainable phosphate ester chemistries. Manufacturers are increasingly investing in recycled phosphorus inputs, bio-based raw materials, and circular phosphorus economy strategies to improve sustainability while maintaining high-performance characteristics in industrial coatings, lubricants, and flame-retardant systems.

Key companies operating in the phosphate esters market include LANXESS AG, ICL Group Ltd., Solvay S.A., Clariant AG, and BASF SE. These companies are expanding halogen-free flame retardant portfolios, developing bio-based phosphate esters, strengthening specialty additive production, and investing in EV battery, aerospace, and electronics applications to enhance their market positions.

Liquid phosphate esters dominate the market with a 78.3% share due to strong demand in aviation hydraulic fluids, industrial lubricants, and fire-resistant fluid systems. Direct sales account for 55.4% market share as aerospace, defense, and industrial customers require customized formulations and strict quality assurance. Regionally, China, the United States, Germany, India, and South Korea are emerging as key investment markets driven by EV production, semiconductor manufacturing, aerospace expansion, and advanced specialty chemical development.