Matting Agents Market Size, Low-Gloss Coating Demand, and Advanced Surface Finishing Outlook

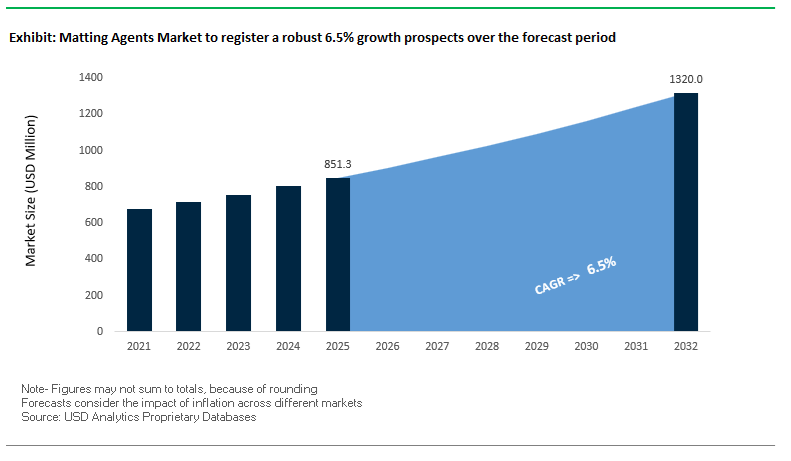

The global matting agents market was valued at $851.3 million in 2025 and is projected to reach $1,322.9 million by 2032, expanding at a CAGR of 6.5%. This growth is driven by increasing demand for matte coatings, low-gloss finishes, silica-based matting agents, wax-based additives, and specialty surface modifiers across automotive coatings, wood coatings, industrial coatings, architectural paints, and consumer electronics applications. As end-users prioritize aesthetic differentiation, anti-glare performance, and soft-touch finishes, matting agents are becoming essential components in advanced coating formulations.

A key growth driver is the rising preference for premium matte and satin finishes in sectors such as automotive interiors, furniture, and electronics, where visual appeal and tactile performance are critical. Additionally, the transition toward waterborne coatings, UV-curable systems, and low-VOC formulations is increasing the technical complexity of achieving consistent matte finishes, thereby boosting demand for high-performance matting additives. Challenges such as the “clarity vs. matte” trade-off, cure interference, and dispersion stability are driving innovation in next-generation matting technologies.

The market is also benefiting from advancements in additive chemistry, nano-silica technology, and hybrid matting systems, which enable improved scratch resistance, transparency, and mechanical durability. Growth in 3D printing, EV interiors, and high-performance plastics is further expanding application areas for matting agents. Regionally, Europe leads in high-end industrial coatings and regulatory-driven innovation, while Asia-Pacific is emerging as a high-growth region due to expanding automotive production and electronics manufacturing.

The matting agents industry is undergoing significant transformation driven by product innovation, integrated additive development, and sustainability initiatives. In January 2026, W.R. Grace & Co. introduced SYLOID® AQ 880, a next-generation silica-based matting agent designed for waterborne coatings. This innovation addresses the long-standing challenge of balancing matte finish with optical clarity, enabling deep matte surfaces without the haze typically associated with water-based systems, particularly in wood furniture coatings.

Strategic expansion and integration across the additive value chain are becoming key competitive strategies. Evonik, in February 2026, announced a global expansion of hydroxyl-terminated polybutadienes (HTPB) production, linking it directly to its strategy of creating integrated “Matte & Flow” additive packages by combining its ACEMATT® matting agents with TEGO® flow additives. This integrated approach enhances surface uniformity, gloss control, and application performance, particularly in automotive interior coatings. Additionally, Evonik’s November 2025 expansion of polyamide production in China supports rising demand for matting agents in high-performance plastics and EV interior applications.

Sustainability and regulatory compliance are also shaping product development. In October 2024, PPG Industries entered a strategic partnership to develop bio-derived matting agents, aiming to replace conventional silica and wax-based additives with renewable alternatives that meet strict “Red List” chemical-free requirements in architectural coatings. This reflects a broader shift toward environmentally friendly and low-VOC additive solutions.

Technological advancements are improving compatibility and performance in complex coating systems. W.R. Grace’s June 2024 launch of SYLOID® CAT 11 addresses catalyst compatibility issues, preventing cure retardation in coil and industrial coatings where high silica loading is required for low gloss. Furthermore, Arkema’s August 2024 expansion of its N3xtDimension® portfolio introduced matting additives for UV-curable systems, enabling soft-touch matte finishes while maintaining surface hardness in 3D-printed components.

Emerging applications in advanced manufacturing and surface engineering are further expanding market opportunities. Höganäs AB’s May 2024 expansion of Amperit® powders integrates matting and wear-resistant properties for laser cladding applications, where non-reflective surfaces are required for both functional and safety purposes. Additionally, W.R. Grace’s January 2024 study on SYLOID® RAD series demonstrated consistent matting performance in LED-cured coatings, supporting the industry’s transition toward energy-efficient curing technologies.

Capacity expansion and operational scaling are also supporting market growth. Huntsman Corporation’s March 2026 expansion in Hungary enhances production of specialty additives and matting-compatible resins, strengthening supply for the European industrial coatings market.

Market Trend: Silica-Based Matting Agents Replacing Wax Systems in Industrial Wood Coatings for Thermal Stability and Surface Performance

The matting agents industry is undergoing a structural transition in industrial wood coatings, where silica-based systems are rapidly replacing traditional wax-based additives. This shift is driven by the increasing adoption of high-temperature bake processes and UV-cured coating technologies, which demand superior thermal stability and consistent gloss control. Conventional wax matting agents tend to soften, migrate, or bloom at elevated temperatures, leading to surface defects such as gloss inconsistency and ghosting in fast-cycle industrial ovens.

Silica matting agents, particularly untreated and surface-modified variants, offer significantly improved thermal resilience. These materials maintain stable gloss profiles at bake temperatures ranging from 150°C to 180°C, ensuring uniform surface appearance even under aggressive curing conditions. This capability is critical for high-throughput furniture and panel production lines where process consistency directly impacts yield and quality control.

In addition to thermal stability, silica-based matting agents enhance mechanical performance. Clear wood coatings formulated with silica additives achieve pencil hardness levels of 2H to 3H, delivering improved scratch resistance compared to softer wax-based systems. This is particularly relevant in applications requiring long-term durability under frequent handling and abrasion.

The compatibility of polymer-treated silicas with 100% solid UV-curable systems is further accelerating their adoption. These advanced materials demonstrate a 20% to 30% improvement in matting efficiency, defined as gloss reduction per unit loading, without interfering with photoinitiator kinetics or curing speed. This enables formulators to achieve low-gloss finishes while maintaining production throughput and energy efficiency. As industrial coating lines continue to optimize for speed, durability, and sustainability, silica-based matting agents are becoming the dominant solution in wood coating applications.

Market Trend: Polymeric Matting Agents Enabling Soft-Touch and Anti-Burnishing Performance in Automotive Interior Coatings

The automotive coatings segment is witnessing a parallel shift toward organic polymeric matting agents, particularly in interior applications where tactile performance and visual consistency are critical. Automotive OEMs are prioritizing “soft-touch” surfaces that deliver premium haptic feedback, driving the replacement of traditional silica-based matting agents with polymeric microbeads such as polyurethane and urea-formaldehyde derivatives.

A key performance advantage of polymeric matting agents lies in their resistance to burnishing. Unlike rigid silica particles that can fracture under mechanical stress, leading to localized gloss increase, polymeric microbeads function as micro-scale ball bearings. This reduces surface friction and maintains consistent gloss levels even under repeated abrasion. Standard Crockmeter testing demonstrates zero gloss increase after 100 cycles for polymeric systems, compared to a 5 to 10 gloss unit increase observed in silica-matted surfaces.

Haptic engineering is another critical differentiator. Polymeric matting agents enable coatings to achieve a controlled coefficient of friction in the range of 0.2 to 0.4, delivering a velvet-like or rubberized feel that aligns with premium automotive interior design trends, particularly in electric vehicles. This tactile enhancement is increasingly viewed as a key component of brand differentiation and user experience.

Optical clarity in dark-colored coatings further strengthens the case for polymeric systems. These agents provide near-total transparency in deep-black and dark-gray formulations, avoiding the haze or graying effect often associated with high-loading silica systems at low gloss levels. This ensures consistent color depth and aesthetic quality in interior components such as dashboards and door panels. As automotive interiors evolve toward higher sensory and visual standards, polymeric matting agents are becoming a preferred material solution.

Market Opportunity: CARB 2027 SCM Driving Demand for Low-Viscosity, High-Performance Matting Agents in Low-VOC Coatings

The tightening of VOC regulations under the California Air Resources Board’s 2027 Suggested Control Measure is creating significant opportunities for advanced matting agent technologies. As formulators transition toward high-solids and waterborne coating systems to meet VOC limits below 100 g/L, the role of matting agents is becoming increasingly critical in maintaining performance without compromising processability.

One of the primary challenges in high-solids formulations is viscosity control. Conventional matting agents often increase formulation viscosity, limiting loading capacity and affecting application properties. New-generation silica matting agents are engineered to exhibit low thickening behavior, allowing for a 15% to 20% increase in loading without significant increases in Krebs Unit viscosity. This enables formulators to achieve desired gloss levels while maintaining sprayability and film formation characteristics in compliant low-VOC systems.

Waterborne coatings, which now account for more than 40% of the premium architectural segment, present additional formulation challenges related to stability and dispersion. There is growing demand for surface-treated matting agents that prevent issues such as seeding and hard settling in aqueous systems. Advanced treatments, including polymer and wax surface modifications, improve compatibility with waterborne resins and enhance long-term storage stability. These capabilities position innovative matting agents as essential components in next-generation low-VOC coating formulations, supporting both regulatory compliance and performance optimization.

Market Opportunity: China GB/T 35609-2025 Standard Driving Demand for High-Purity, Low-Dust Matting Agent Technologies

China’s implementation of the GB/T 35609-2025 “Green Product Assessment” standard is creating a strong opportunity landscape for matting agent manufacturers focused on environmental safety and product purity. The regulation emphasizes reduced occupational hazards and stricter control over chemical composition, reshaping material selection criteria across the coatings value chain.

A key requirement under the new standard is the reduction of airborne particulate matter during manufacturing processes. This is driving increased adoption of wet-cake and masterbatch forms of matting agents, which can reduce respirable dust levels by up to 95% compared to traditional dry powder handling. These formats improve workplace safety and align with regulatory expectations for cleaner production environments, particularly in large-scale coating manufacturing facilities.

The standard also imposes stringent limits on heavy metal content, including lead, cadmium, mercury, and hexavalent chromium. This is favoring high-purity synthetic precipitated silicas, which offer controlled composition and minimal contamination, over naturally derived alternatives such as diatomaceous earth. As manufacturers seek to achieve “Green Product” certification, demand for certified, high-purity matting agents is expected to increase significantly.

This regulatory shift is reinforcing China’s role as a key growth market for advanced additive technologies, with implications for global supply chains and product development strategies. Suppliers capable of delivering low-dust, high-purity, and environmentally compliant matting agents are well positioned to capture emerging opportunities in the evolving coatings landscape.

Matting Agents Market Share and Segmentation Insights

Synthetic Matting Agents Capture 78% Share Driven by High Durability and Cross-Platform Formulation Flexibility

The matting agents market by product category is overwhelmingly led by synthetic matting agents, accounting for 78% of the global market share in 2025, driven by their superior performance in modern coating systems. These agents—primarily silica-based, polyurea, and wax-based matting additives—deliver consistent gloss reduction, enhanced scratch resistance, and superior burnish resistance, making them indispensable in industrial coatings, automotive finishes, and high-performance wood coatings. A critical growth driver is their broad compatibility across waterborne, solvent-borne, UV-curable, and powder coatings, enabling formulators to standardize performance across multiple applications. In contrast, natural alternatives like diatomaceous earth are limited in formulation flexibility. As demand rises for low-VOC coatings, durable matte finishes, and high-performance coating additives, synthetic matting agents continue to dominate the global coatings additives market.

Standard Matte Segment Holds 52% Share as Preferred Finish for Furniture, Interiors, and Anti-Glare Applications

In the matting agents market by surface finish, standard matte finishes dominate with a 52% market share in 2025, reflecting strong demand across architectural coatings, furniture coatings, and industrial surface finishes. Typically ranging between 10–30 gloss units at a 60° angle, standard matte coatings offer an optimal balance between aesthetic softness, surface smoothness, and cleanability, making them ideal for cabinetry, interior walls, and decorative wood applications. Additionally, standard matte finishes are widely preferred for their anti-fingerprint and anti-glare properties, particularly in consumer electronics, automotive interiors, and kitchen surfaces, where reduced light reflection enhances user experience. Compared to deep matte finishes, standard matte requires lower additive loading, reducing formulation costs while still meeting performance expectations. This balance of cost-efficiency, durability, and visual appeal cements its leadership in the global matting agents market.

Competitive Landscape in the Matting Agents Market

Evonik leads silica-based matting innovation with precision surface morphology control

Evonik Industries remains the global leader in silica-based matting agents, particularly through its ACEMATT® portfolio, which dominates the inorganic segment. The company introduced new precipitated silica grades (OK 390, HK 390, HK 520) designed for high-transparency matte finishes, addressing demand in premium coatings. With a projected 2026 adjusted EBITDA between €1.7 billion and €2.0 billion, Evonik continues to benefit from strong demand in advanced surface technologies. Its innovations in particle size engineering enable “deep matte” effects while preserving tactile warmth in wood and leather coatings. Additionally, Evonik is integrating Industry 4.0 tools into formulation processes, allowing customers to optimize rheology and dispersion performance through real-time digital data insights.

BYK drives sustainable and tactile matting solutions with bio-based wax technologies

BYK-Chemie, part of the ALTANA Group, is a leading innovator in wax-based matting agents, focusing on tactile performance and sustainability. In 2026, the company implemented price adjustments of up to 30% to sustain its high R&D investment of 8–10%, supporting next-generation PFAS-free additives. Its CERAFLOUR product line now includes bio-based grades (1003 and 1004) containing up to 95% renewable raw materials, delivering both matting efficiency and scratch resistance. BYK is recognized for its expertise in creating “soft-touch” surfaces, providing silky or velvety finishes for automotive and consumer electronics applications. Through its BYK-Gardner division, the company offers digital validation of gloss levels, ensuring precise matting performance within defined gloss-unit ranges.

W. R. Grace strengthens high-performance silica solutions for industrial and coil coatings

W. R. Grace & Co. is a major player in amorphous silica-based matting agents, emphasizing high purity and controlled particle size for industrial coatings. Its SYLOID® AQ and RAD series are specifically engineered for UV-curable and waterborne systems, offering high pore volume and enhanced smoothness. The company recently launched SYLOID® MX 110, targeting coil coatings requiring superior burnish resistance and chemical durability for exterior metal applications. Grace’s silica solutions also provide moisture-scavenging capabilities, improving shelf life in two-component coating systems. With continuous advancements in surface modification, the company has improved wetting performance in solvent-borne systems by over 30%, reinforcing its leadership in high-performance industrial coatings.

Lubrizol advances hybrid matting technologies for efficient and dust-free formulations

Lubrizol Corporation is a key innovator in hybrid matting technologies, combining silica and wax functionalities to simplify coating formulations. Its Lanco™ LiquiMatt 5730 liquid matting agent eliminates the need for powder-based additives in wood coatings, reducing dust generation and improving processing efficiency in high-speed manufacturing environments. The company is expanding its presence in Asia-Pacific, targeting rising demand for matte finishes in premium furniture and flooring applications. Lubrizol’s strategic focus on soft-touch coatings for automotive interiors aligns with growing demand for low-gloss, high-durability surfaces. By integrating its Lanco™ and Aptalon™ portfolios, the company provides synergistic solutions for water-based dispersions, enhancing formulation efficiency and performance.

Arkema drives bio-based and UV-curable matting solutions for sustainable coatings

Arkema is a leader in sustainable matting agent technologies, leveraging its expertise in specialty resins and ecodesign principles. At the American Coatings Show 2026, the company introduced additives with up to 93% bio-based content, targeting architectural and wood coatings with reduced carbon footprints. Arkema is also advancing UV/EB radiation-curable matting additives, which eliminate solvent emissions and represent a key growth segment in zero-VOC coatings. Its solutions are increasingly used in data center coatings, providing anti-glare and heat-shielding properties for energy-efficient infrastructure. With strong positioning in mobility and construction sectors, Arkema continues to deliver high-durability coatings with enhanced UV stability and long-term performance.

Germany stands as the global innovation hub in the matting agents market, driven by advanced specialty additives, silica-based matting technologies, and sustainability-led coating solutions. Companies such as BYK are leading the shift toward bio-based additives, with the expansion of CERAFLOUR grades (1003 and 1004) in 2026 offering high transparency, soft-touch finishes, and renewable raw material integration. This aligns with the growing demand for eco-friendly matting agents in automotive and industrial coatings.

Technological innovation is further reinforced by Deuteron GmbH, which has prioritized PTFE-free polymethylurea technologies as high-performance alternatives to PFAS-based additives, ensuring compliance with tightening EU chemical regulations. Meanwhile, Evonik Industries continues to expand its ACEMATT® silica production for waterborne and UV-curable coatings, supporting low-VOC formulations and improved surface performance. AI-driven formulation is also gaining traction, with Münzing Chemie utilizing machine learning tools to optimize particle size distribution, reducing development cycles by approximately 25%. Key applications include ultra-matte automotive interiors and high-durability wood coatings for premium furniture.

China Matting Agents Market: Regulatory Compliance, Scale Dominance, and Waterborne Transition

China dominates the global matting agents market size and consumption, supported by its large coatings industry and evolving regulatory framework. The implementation of the 2026 Regulations on Industrial and Supply Chain Security by the State Council has strengthened oversight of critical raw materials such as high-purity silica and wax-based matting agents, ensuring domestic supply chain resilience.

Environmental policies such as the updated “Blue Sky” initiative are accelerating the transition toward waterborne coatings, requiring large-scale requalification of matting agents for compatibility with aqueous systems. Industrial expansion remains strong, with BASF Coatings (Guangdong) Co. Ltd. increasing automotive refinish capacity to 30,000 tons annually, integrating advanced matting technologies to support the EV boom. China’s consumption exceeds 135,000 metric tons annually, making it the largest single-country market, particularly in architectural coatings and consumer electronics finishing applications. Key applications include high-volume industrial coatings and passive depollution infrastructure, reinforcing China’s scale-driven market leadership.

United States Matting Agents Market: Clean Chemistry, Functional Coatings, and Optical Precision

The United States matting agents market is defined by a strong emphasis on regulatory compliance, high-performance coatings, and functional additive innovation. Under evolving regulations from the Environmental Protection Agency, the phase-out of fluorinated additives is accelerating adoption of wax-based matting agents and micronized silica technologies that deliver slip resistance and durability without persistent environmental impact.

Innovation remains a key differentiator, with industry-academic collaborations developing organic matting agents (OMA) featuring self-healing properties, enabling coatings to repair micro-scratches while maintaining consistent matte finishes. Lubrizol Corporation has expanded its LiquiMatt product portfolio to address growing demand for liquid-dispersion matting agents, simplifying manufacturing for SMEs. Additionally, U.S. R&D is advancing optical-grade matting technologies, where controlled silica morphology enables precise light diffusion for applications in LED displays and AR/VR devices. Key applications include aerospace anti-glare coatings and premium architectural finishes with eggshell textures.

India Matting Agents Market: Infrastructure Boom and Sustainable Textile Integration

India’s matting agents market growth is closely tied to infrastructure expansion and government-backed initiatives promoting technical textiles and sustainable coatings. The Union Budget 2026–27 introduced the Integrated Programme for the Textile Sector, supporting Mega Textile Parks that require matte-finish, eco-friendly coating additives for synthetic fabrics under the Tex-Eco initiative.

Infrastructure development under PM Gati Shakti is driving demand for industrial metal coatings with anti-glare and wear-resistant properties, particularly in railway stations, airports, and logistics hubs. To support industry transition, both domestic and multinational players are establishing testing and certification centers to help MSMEs adopt waterborne and powder coating matting technologies. Innovation is also emerging in bio-based matting agents derived from natural fibers such as jute and rice husk ash, aligning with the Atmanirbhar Bharat vision. Key applications include protective coatings for coastal infrastructure and matte finishes in consumer appliances.

Japan Matting Agents Market: Functional Aesthetics and Electronics-Grade Additives

Japan’s matting agents market is distinguished by its focus on ultra-high-purity materials and functional coatings for electronics and automotive applications. Companies such as Nitto Denko and Shin-Etsu Chemical are advancing “functionalized” matting agents that go beyond aesthetics, incorporating thermal management and antistatic properties for high-performance electronic displays.

Technological advancements include the development of ultra-hydrophobic matting layers, which enhance fingerprint resistance and improve visibility on touchscreen interfaces in high-traffic environments. Japan is also investing heavily in nano-structured $TiO_{2}$ matting agents, valued for their non-toxic profile and UV stability in outdoor applications. These innovations are particularly relevant for smart city digital signage and automotive satin-finish coatings, where both durability and visual performance are critical. Key applications include anti-glare display films and premium automotive surface finishes, reinforcing Japan’s leadership in high-value, niche matting technologies.

Matting Agents Market Report Scope

Matting Agents Market

Parameter

Details

Market Size (2025)

$851.3 Million

Market Size (2032)

$1322.9 Million

Market Growth Rate

6.5%

Segments

By Material (Inorganic Matting Agents, Organic Matting Agents, Hybrid Matting Agents), By Product Category (Synthetic Matting Agents, Natural), By Formulation Technology (Water-borne, Solvent-borne, Powder Coatings, Radiation-Cured, High-Solids), By Application (Coatings, Printing Inks, Plastics and Textiles, Paper and Cardboard Coatings), By End-Use Industry (Building and Construction, Automotive and Transportation, Consumer Electronics, Furniture and Flooring, Packaging and Labels, Textile and Apparel, Aerospace and Defense), By Surface Finish (Deep Matte, Standard Matte, Satin), By Functional Property (Scratch and Abrasion Resistance, Clarity, Burnish Resistance, Soft-Touch, Chemical Resistance)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

Evonik Industries AG, BYK-Chemie GmbH, PPG Industries, Inc., W. R. Grace and Co., The Lubrizol Corporation, Arkema S.A., BASF SE, Imerys S.A., J.M. Huber Corporation, Eastman Chemical Company, PQ Corporation, Dovell, Lamberti S.p.A., Deuteron GmbH, Thomas Swan and Co. Ltd.

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Matting Agents Market Segmentation

By Material

Inorganic Matting Agents

Organic Matting Agents

Hybrid Matting Agents

By Product Category

Synthetic Matting Agents

Natural

By Formulation Technology

Water-borne

Solvent-borne

Powder Coatings

Radiation-Cured

High-Solids

By Application

Coatings

Architectural Coatings

Industrial Coatings

Automotive and Transportation Coatings

Wood and Furniture Coatings

Leather Coatings

Printing Inks

Packaging Inks

Publication Inks

Plastics and Textiles

Paper and Cardboard Coatings

By End-Use Industry

Building and Construction

Automotive and Transportation

Consumer Electronics

Furniture and Flooring

Packaging and Labels

Textile and Apparel

Aerospace and Defense

By Surface Finish

Deep Matte

Standard Matte

Satin

By Functional Property

Scratch and Abrasion Resistance

Clarity

Burnish Resistance

Soft-Touch

Chemical Resistance

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Matting Agents Industry

Evonik Industries AG

BYK-Chemie GmbH

PPG Industries, Inc.

W. R. Grace & Co.

The Lubrizol Corporation

Arkema S.A.

BASF SE

Imerys S.A.

J.M. Huber Corporation

Eastman Chemical Company

PQ Corporation

Dovell

Lamberti S.p.A.

Deuteron GmbH

Thomas Swan & Co. Ltd.

*- List not Exhaustive

Table of Contents: Matting Agents Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Matting Agents Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Matting Agents Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the Matting Agents Market

3.1. Trend: Silica-Based Matting Agents Replacing Wax Systems in Industrial Wood Coatings

3.2. Trend: Polymeric Matting Agents Enabling Soft-Touch Automotive Interior Finishes

3.3. Opportunity: CARB 2027 SCM Driving Demand for Low-Viscosity Matting Agents in Low-VOC Coatings

3.4. Opportunity: China GB/T 35609-2025 Standard Accelerating High-Purity, Low-Dust Matting Technologies

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Product Innovation

4.3. Sustainability and ESG Strategies

4.4. Capacity Expansion and Geographic Expansion

5. Market Share and Segmentation Insights: Matting Agents Market

5.1. By Material

5.1.1. Inorganic Matting Agents

5.1.2. Organic Matting Agents

5.1.3. Hybrid Matting Agents

5.2. By Product Category

5.2.1. Synthetic Matting Agents

5.2.2. Natural

5.3. By Formulation Technology

5.3.1. Water-borne

5.3.2. Solvent-borne

5.3.3. Powder Coatings

5.3.4. Radiation-Cured

5.3.5. High-Solids

5.4. By Application

5.4.1. Coatings

5.4.2. Architectural Coatings

5.4.3. Industrial Coatings

5.4.4. Automotive and Transportation Coatings

5.4.5. Wood and Furniture Coatings

5.4.6. Leather Coatings

5.4.7. Printing Inks

5.4.8. Packaging Inks

5.4.9. Publication Inks

5.4.10. Plastics and Textiles

5.4.11. Paper and Cardboard Coatings

5.5. By End-Use Industry

5.5.1. Building and Construction

5.5.2. Automotive and Transportation

5.5.3. Consumer Electronics

5.5.4. Furniture and Flooring

5.5.5. Packaging and Labels

5.5.6. Textile and Apparel

5.5.7. Aerospace and Defense

5.6. By Surface Finish

5.6.1. Deep Matte

5.6.2. Standard Matte

5.6.3. Satin

5.7. By Functional Property

5.7.1. Scratch and Abrasion Resistance

5.7.2. Clarity

5.7.3. Burnish Resistance

5.7.4. Soft-Touch

5.7.5. Chemical Resistance

6. Country Analysis and Outlook of Matting Agents Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Saudi Arabia

6.19. UAE

6.20. Middle East and Africa

7. Matting Agents Market Size Outlook by Region (2025–2034)

7.1. North America Matting Agents Market Size Outlook to 2034

7.1.1. By Material

7.1.2. By Product Category

7.1.3. By Formulation Technology

7.1.4. By Application

7.1.5. By End-Use Industry

7.1.6. By Surface Finish

7.1.7. By Functional Property

7.2. Europe Matting Agents Market Size Outlook to 2034

7.2.1. By Material

7.2.2. By Product Category

7.2.3. By Formulation Technology

7.2.4. By Application

7.2.5. By End-Use Industry

7.2.6. By Surface Finish

7.2.7. By Functional Property

7.3. Asia Pacific Matting Agents Market Size Outlook to 2034

7.3.1. By Material

7.3.2. By Product Category

7.3.3. By Formulation Technology

7.3.4. By Application

7.3.5. By End-Use Industry

7.3.6. By Surface Finish

7.3.7. By Functional Property

7.4. South and Central America Matting Agents Market Size Outlook to 2034

7.4.1. By Material

7.4.2. By Product Category

7.4.3. By Formulation Technology

7.4.4. By Application

7.4.5. By End-Use Industry

7.4.6. By Surface Finish

7.4.7. By Functional Property

7.5. Middle East and Africa Matting Agents Market Size Outlook to 2034

7.5.1. By Material

7.5.2. By Product Category

7.5.3. By Formulation Technology

7.5.4. By Application

7.5.5. By End-Use Industry

7.5.6. By Surface Finish

7.5.7. By Functional Property

8. Company Profiles: Leading Players in the Matting Agents Market

8.1. Evonik Industries AG

8.2. BYK-Chemie GmbH

8.3. PPG Industries, Inc.

8.4. W. R. Grace and Co.

8.5. The Lubrizol Corporation

8.6. Arkema S.A.

8.7. BASF SE

8.8. Imerys S.A.

8.9. J.M. Huber Corporation

8.10. Eastman Chemical Company

8.11. PQ Corporation

8.12. Dovell

8.13. Lamberti S.p.A.

8.14. Deuteron GmbH

8.15. Thomas Swan and Co. Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Matting Agents Market Segmentation

By Material

Inorganic Matting Agents

Organic Matting Agents

Hybrid Matting Agents

By Product Category

Synthetic Matting Agents

Natural

By Formulation Technology

Water-borne

Solvent-borne

Powder Coatings

Radiation-Cured

High-Solids

By Application

Coatings

Architectural Coatings

Industrial Coatings

Automotive and Transportation Coatings

Wood and Furniture Coatings

Leather Coatings

Printing Inks

Packaging Inks

Publication Inks

Plastics and Textiles

Paper and Cardboard Coatings

By End-Use Industry

Building and Construction

Automotive and Transportation

Consumer Electronics

Furniture and Flooring

Packaging and Labels

Textile and Apparel

Aerospace and Defense

By Surface Finish

Deep Matte

Standard Matte

Satin

By Functional Property

Scratch and Abrasion Resistance

Clarity

Burnish Resistance

Soft-Touch

Chemical Resistance

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global matting agents market was valued at $851.3 million in 2025 and is projected to reach $1,322.9 million by 2032, growing at a CAGR of 6.5%. Market expansion is being driven by increasing demand for matte coatings, low-gloss finishes, silica-based matting agents, and specialty surface modifiers across automotive coatings, furniture coatings, industrial finishes, consumer electronics, and architectural paints.

Silica-based matting agents are gaining strong adoption because they provide superior thermal stability, gloss consistency, and scratch resistance under high-temperature bake and UV-curing conditions. Unlike wax additives, silica systems maintain stable matte performance at curing temperatures of 150°C to 180°C while improving hardness and durability in furniture and wood coatings. Their compatibility with UV-curable and waterborne systems is also accelerating usage in advanced industrial coating lines.

Automotive OEMs are increasingly adopting polymeric matting agents to create premium soft-touch interiors with improved anti-burnishing performance and enhanced tactile feel. Polyurethane and urea-formaldehyde microbeads deliver consistent low-gloss finishes without the haze often associated with silica systems, especially in dark-colored EV interiors. These technologies also improve abrasion resistance and maintain gloss uniformity under repeated mechanical stress, supporting next-generation automotive cabin design trends.

Europe remains the leading innovation hub due to strict VOC regulations, sustainability initiatives, and advanced specialty coating development, while Asia-Pacific is emerging as the fastest-growing region because of expanding automotive production, electronics manufacturing, and industrial coatings demand in China and India. Major opportunities are also developing in UV-curable coatings, EV interiors, anti-glare electronics, high-performance plastics, and premium furniture coatings.

Major companies operating in the matting agents industry include Evonik Industries AG, BYK-Chemie GmbH, PPG Industries, Inc., W. R. Grace & Co., The Lubrizol Corporation, Arkema S.A., BASF SE, and Imerys S.A.. These companies are investing heavily in nano-silica technologies, bio-based additives, UV-curable matting systems, soft-touch coatings, and sustainable low-VOC surface finishing solutions to strengthen their global market positions.