Energy-Cured Printing, Circular Packaging, and Regulatory Compliance Driving Moderate Growth

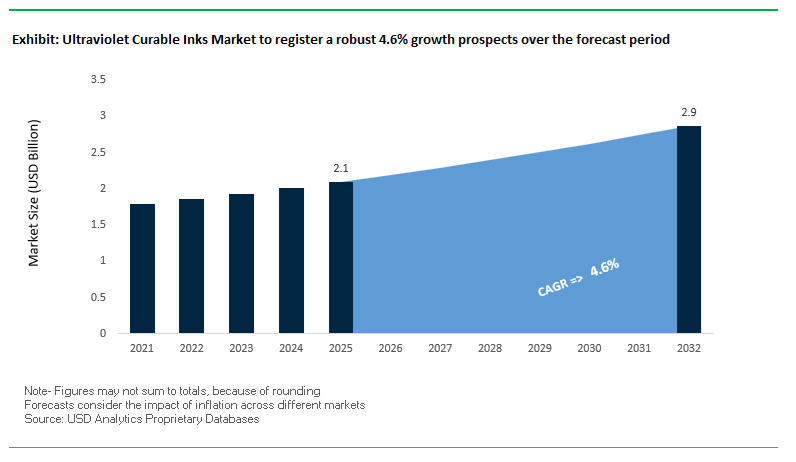

The global Ultraviolet Curable Inks Market is expanding steadily, supported by increasing demand for high-performance, fast-curing, and environmentally efficient printing solutions across packaging, labeling, commercial printing, and industrial applications. The market was valued at $2.1 billion in 2025 and is projected to reach $2.9 billion by 2032, growing at a CAGR of 4.6% during 2025–2032. Growth is driven by the shift toward energy-curable technologies, which offer instant curing, reduced energy consumption, and minimal emissions compared to traditional solvent-based inks.

A key structural driver is the rising adoption of UV and LED-UV curing systems, particularly in flexible packaging and label printing. These inks enable high-speed production, superior adhesion, and enhanced print quality across diverse substrates, including plastics, films, and metals. The increasing demand for short-run, customized, and digitally printed packaging is further accelerating adoption, as UV-curable inks are highly compatible with digital and hybrid printing systems.

Regulatory compliance is a major factor shaping the market. Stricter global standards for food-contact safety, migration limits, and recyclability are pushing manufacturers to develop low-migration, BPA-free, and VOC-free formulations. Additionally, the growing emphasis on circular economy principles is driving innovation in inks that can be easily removed during recycling or are compatible with existing recycling streams.

Another important trend is the integration of advanced additives and hybrid chemistries, which enhance pigment stability, curing efficiency, and surface performance. The convergence of aqueous and UV technologies is also enabling the development of inks that combine low environmental impact with high-performance characteristics, expanding their application scope.

The ultraviolet curable inks market is being transformed by regulatory-driven innovation, sustainability breakthroughs, and advanced material development, reflecting the evolving requirements of modern packaging and printing industries. In February 2026, Siegwerk achieved a landmark milestone with the first RecyClass Technology Approval for its SICURA UV/LED ink series. This certification confirms compatibility with European colored polyethylene (PE) recycling streams, addressing a long-standing challenge in integrating UV inks into circular packaging systems.

Regulatory compliance is accelerating product innovation. Toyo Ink Europe’s February 2026 rollout of GIO-compliant UV ink portfolios ensures adherence to strict German Printing Ink Ordinance (GIO) standards, particularly for low-migration food-contact packaging. Similarly, Flint Group’s Flexocure LEAP (August 2025) introduces a novel resin system designed to minimize photoinitiator migration, a critical safety concern in food packaging applications.

Sustainability-focused solutions are gaining traction. Sun Chemical’s SunCure EcoPlast (July 2025) enables UV inks to be washed off during recycling, allowing plastic substrates to be reused in compliance with Association of Plastic Recyclers (APR) guidelines. This innovation directly supports the transition toward recyclable plastic packaging systems.

Material and additive innovation is also enhancing performance. hubergroup’s ELARA additive brand (February 2026) introduces specialized dispersing and wetting agents that improve pigment stability and surface finish in UV-curable systems. Meanwhile, Flint Group’s EkoCure® XS expansion (January 2026) provides inks capable of maintaining structural integrity during heat-shrink labeling processes, addressing the growing demand for complex packaging formats.

Hybrid ink technologies are redefining environmental performance. The February 2025 commercialization of AQUAFUZE™ technology by Fujifilm and Mutoh combines aqueous and UV-LED chemistries, delivering low-VOC, odorless prints with strong adhesion across diverse substrates. This innovation demonstrates the convergence of performance and sustainability in next-generation ink systems.

Digital printing applications are also expanding. INX International’s INXJet MDLM (July 2025) offers a BPA-NI and No-VOC UV inkjet solution for beverage can decoration, aligning with stringent safety standards from major global brands and industry bodies.

Upstream supply chain consolidation is strengthening market stability. Sudarshan Chemical’s October 2024 acquisition of the Heubach Group enhances access to high-quality pigments, while Toyo Ink India’s capacity expansion (2024–2026) supports the growing demand for UV ink components in the Asia-Pacific packaging market.

Market Trend: REACH Annex XIV Inclusion of Photoinitiators Accelerates Transition to Low-Migration UV Ink Systems

The ultraviolet curable inks industry is undergoing a critical reformulation phase following the European Chemicals Agency’s recommendation to include key photoinitiators, including Photoinitiator 379, in the REACH Annex XIV Authorisation List. This follows the earlier reclassification and effective ban of TPO in September 2025, which has already disrupted conventional UV ink chemistries. Under the 2026 regulatory trajectory, substances placed on Annex XIV will require explicit authorization beyond their sunset dates, particularly for applications involving food-contact packaging. This is forcing ink manufacturers to transition toward polymeric or high-molecular-weight photoinitiator systems that minimize migration levels below 10 parts per billion. The shift is technically challenging, as alternative chemistries such as TPO-L and BAPO require higher UV energy input, typically 15% to 20% more intensity, to achieve equivalent curing performance in high-speed flexographic printing. This is driving simultaneous upgrades in curing equipment and formulation design to maintain throughput efficiency. As regulatory scrutiny intensifies, low-migration UV inks are becoming a baseline requirement in packaging applications, reshaping product development strategies across the industry.

Market Trend: China GB 46997-2025 and GB/T 41653-2025 Establish Unified Framework for Heavy Metals and Migration Control

China’s implementation of GB 46997-2025 and GB/T 41653-2025 is consolidating regulatory requirements for UV-curable inks, particularly in food packaging and consumer goods applications. These standards introduce strict limits on heavy metals, capping soluble lead at 90 mg/kg and mercury at 60 mg/kg, thereby eliminating the use of traditional mineral-based pigments with higher impurity levels. In parallel, the updated framework expands the permitted raw material list to 346 substances while imposing stringent migration limits for primary aromatic amines, aligning with European Union food-contact regulations. This dual approach of expanding material options while tightening safety thresholds is driving the adoption of high-purity synthetic pigments and advanced resin systems. The regulatory changes are also influencing global supply chains, as manufacturers targeting the Chinese market must ensure compliance with both heavy metal and migration standards. As China continues to strengthen its environmental and consumer safety policies, these regulations are setting new benchmarks for UV ink formulation and compliance in the global market.

Market Opportunity: LED-UV Curable Inks Enable High-Speed, Energy-Efficient Digital Printing at Industrial Scale

The convergence of LED-UV curing technology with high-speed digital printing platforms is creating a significant growth opportunity in the UV inks market. Modern LED-UV systems operating at wavelengths such as 395 nm are enabling ultra-fast curing, with surface drying times of less than one second. This allows single-pass inkjet presses to achieve production speeds exceeding 200 meters per minute at high resolutions, making digital printing competitive with traditional offset methods. In addition to speed, LED-UV curing offers substantial energy efficiency benefits, reducing power consumption by 50% to 70% compared to conventional mercury vapor lamps. This is particularly relevant in the context of ESG reporting and sustainability targets for large-scale printing operations. Advances in photoinitiator chemistry have also enabled the development of broadband systems that maintain effective cure-through depth even at high intensities typical of modern LED units. As printing technologies continue to evolve toward higher throughput and lower environmental impact, LED-UV inks are emerging as a key enabler of next-generation industrial printing solutions.

Market Opportunity: UV-Curable Inks Expand into Functional 3D Printing with Engineering-Grade Performance

The application of UV-curable inks in vat photopolymerization is expanding rapidly beyond prototyping into the production of functional components. Advances in resin chemistry are enabling mechanical properties that closely resemble those of engineering thermoplastics, with tensile strengths exceeding 50 MPa and elongation at break above 30%. These characteristics allow 3D-printed parts to be used in demanding applications such as automotive components and consumer electronics. Precision is another critical advantage, with optimized light absorption properties enabling XY resolutions of 50 microns or less and layer thicknesses as low as 25 microns. This level of accuracy is essential for specialized applications such as microfluidics and dental devices. Additionally, high-temperature UV-curable resins are achieving heat deflection temperatures above 150°C, enabling the production of tooling components such as injection mold inserts that can withstand repeated thermal cycling. As additive manufacturing transitions toward end-use production, UV-curable inks and resins are becoming a cornerstone technology for high-performance, customizable manufacturing solutions.

Ultraviolet Curable Inks Market Share and Segmentation Insights

UV Digital (Inkjet) Leads with 45.4% Share Driven by Personalization and On-Demand Printing

The UV digital (inkjet) segment dominates the ultraviolet curable inks market with a 45.4% market share in 2025, fueled by rapid growth in short-run printing, mass customization, and variable data printing applications. Within the UV inks and digital printing market, UV inkjet technology enables on-demand production for labels, flexible packaging, signage, and direct-to-object printing, eliminating the need for plates or tooling. This significantly reduces setup time and costs, making it ideal for e-commerce packaging, promotional printing, and industrial decoration. A major technological advantage is instant LED-UV curing, where inks cure immediately between print heads, allowing printing on heat-sensitive substrates such as films, foils, plastics, and specialty materials. This not only enhances production speed but also reduces energy consumption compared to traditional mercury UV systems. As industries increasingly adopt sustainable, high-speed, and flexible printing solutions, UV digital inkjet remains the leading segment in the global UV curable inks market.

Direct Sales Channel Dominates with 47.8% Share Through OEM Ink Ecosystems and Customization

The direct sales segment leads the UV curable inks market by sales channel with a 47.8% market share in 2025, driven by strong integration between printing equipment manufacturers and ink suppliers. In the industrial printing inks and digital press ecosystem, major OEMs such as HP, EFI, Durst, Mimaki, and Canon supply proprietary UV ink formulations directly to printer users, ensuring optimal curing performance, adhesion, and color gamut compatibility. This closed-loop system enhances print quality, reduces operational issues, and supports high-speed production environments. Additionally, large-scale packaging and label converters increasingly rely on direct supplier relationships for custom ink formulations tailored to specific substrates, including BOPP, PET, PE, and metallized films. This level of collaboration enables precise performance tuning for diverse applications, reinforcing the importance of direct sales in the UV inks supply chain. The combination of technical support, customization, and system compatibility continues to drive the dominance of this channel in the global UV curable inks market.

Competitive Landscape Analysis of the Ultraviolet Curable Inks Market

DIC Corporation Leads Low-Migration UV Ink Systems with Sustainable Innovation

DIC Corporation (Sun Chemical) maintains a dominant position in the UV curable inks market, leveraging combined annual sales exceeding USD 7.0 billion. In 2026, the company is investing heavily in its Newport, Delaware facility to scale production of quinacridone pigments, essential for high-performance UV inkjet and offset inks. Its newly launched SunCure® Advance ECO series features 25–30% bio-renewable content and supports high-speed presses exceeding 20,000 impressions per hour. Through a strategic partnership with Emerald, DIC is integrating Physical AI technologies to optimize color consistency and viscosity control. Its low-migration ink systems, fully compliant with Nestlé guidelines and Swiss Ordinance standards, reinforce its leadership in food and pharmaceutical packaging inks.

Flint Group Expands Packaging-Focused UV Ink Solutions with Energy Efficiency

Flint Group is strengthening its position in the UV curable inks market with its strategic pivot toward packaging solutions, unveiled under its new “Flint Group Packaging Solutions” identity in 2026. The company introduced the Flexocure® LEAP range, which stabilizes photoinitiators to eliminate migration risks in food-contact materials. Its transition to LED-UV formulations has significantly improved energy efficiency, reducing consumption by up to 50% compared to traditional mercury systems. Through its Xeikon brand, Flint offers a fully integrated equipment-and-ink ecosystem, enabling converters to streamline digital and analog UV printing processes. This positions Flint as a leader in sustainable packaging inks and high-efficiency UV curing technologies.

Toyo Ink SC Holdings (Artience Group) is actively expanding its footprint in the UV curable inks market, particularly across the high-growth Asia-Pacific region. In 2026, the company implemented a 10% price revision to offset rising logistics and energy costs while funding R&D for next-generation solvent-free UV inks. Its Liojet™ series is engineered for high-speed industrial printing, featuring ultra-low viscosity and high pigment loading compatible with advanced Piezo Drop-on-Demand print heads. Toyo Ink’s dual-cure systems allow seamless switching between conventional UV and LED-UV curing, reducing downtime for commercial printers. With localized production in India and Thailand, the company is well-positioned to capitalize on e-commerce packaging demand.

Fujifilm Drives Wide-Format and Functional UV Ink Applications with Advanced Chemistry

Fujifilm Holdings Corporation is a key innovator in the UV curable inks market, particularly in the wide-format inkjet printing segment. Its Uvijet Digital UV range utilizes Micro-V dispersion technology to deliver high pigment loading and superior durability for outdoor signage. In 2026, Fujifilm introduced transparent UV-curable inks designed for electronics manufacturing, offering high abrasion resistance on glass and metal substrates. The company is expanding production capacity for its Acuity and OnsetM press inks to meet the 6.4% CAGR growth in specialty substrate printing. Leveraging its semiconductor materials expertise, Fujifilm ensures precise dot reproduction and strong adhesion, strengthening its leadership in industrial UV ink applications.

Siegwerk Advances Regulatory-Compliant and Circular UV Ink Solutions for Packaging

Siegwerk Druckfarben AG & Co. KGaA is a leading player in the UV curable inks market, focusing on regulatory-compliant and circular packaging solutions. In 2026, the company achieved full readiness for the German Printing Ink Ordinance (GIO), offering a GIO-ready portfolio including the SICURA Nutriflex series. Its SICURA Nutriflex LEDTec inks are dual-cure, low-migration formulations designed for sensitive food packaging applications, ensuring consistent color performance under both LED and conventional UV curing systems. Siegwerk is also collaborating with global brands to enhance de-inkability and recyclability in paper and board packaging. Its advanced migration modeling tools provide converters with predictive insights, reinforcing its leadership in safe and sustainable UV ink technologies.

China’s Leadership in Optical Fiber UV Inks and Smart Textile Digital Printing Expansion

China continues to dominate the ultraviolet curable inks market, leveraging its large-scale manufacturing ecosystem and strong integration across telecommunications and textile industries. The country’s optical fiber production capacity has surged beyond 350 million fiber-km, creating massive demand for optical fiber UV inks used for identification, insulation, and long-term durability in high-speed data transmission networks. This expansion aligns with China’s aggressive push toward digital infrastructure and 5G deployment.

Technological advancements include the deployment of nano-carbon black-based UV ink formulations, enhancing weather resistance and electrical protection in industrial cables and pipelines. The expansion of the Guangzhou Digital Printing Hub is accelerating the adoption of UV inkjet textile printing, which is rapidly replacing conventional dyeing methods due to its efficiency and sustainability. Government initiatives such as the Green Printing Action Plan are further driving the shift toward LED-curable UV inks, reducing VOC emissions and improving environmental compliance. Key applications include multi-layer UV inks for flexible electronics and touchscreen overlays, offering anti-fingerprint and scratch-resistant properties. Regulatory enforcement of low-migration standards is also boosting demand for food-safe UV inks in flexible packaging.

United States Driving High-Purity UV Inks for Aerospace, Electronics, and Smart Labeling

The United States is advancing the UV curable inks market through innovation in high-purity formulations and specialty industrial applications. The market is witnessing a strong shift toward transparent UV inks and functional coatings, particularly for aerospace maintenance and electronics manufacturing.

Recent product innovations include thixotropic gel-based UV inks and strippers, enabling precision repairs in aerospace MRO without damaging underlying composite materials. Technological advancements in high-speed pigment inkjet printing are transforming the publishing industry by enabling print-on-demand models, significantly reducing inventory waste. Strategic investments by major players are expanding production of UV-based intelligent labeling solutions, particularly for pharmaceutical cold-chain logistics.

Regulatory enforcement under the Clean Air Act is accelerating the adoption of 100% solids UV-curing systems, replacing traditional solvent-based inks across multiple industries. Key applications include the use of UV-LED inks as conformal coatings on PCBs, enhancing durability in defense and EV electronics. Additionally, the transition to LED curing systems is improving energy efficiency, reducing operational costs in large-scale printing operations.

Germany’s Circular Economy Leadership and De-Inkable UV Ink Technologies

Germany is at the forefront of sustainable UV ink technologies, focusing on circular economy integration and compliance with stringent environmental regulations. Innovations in de-inkable UV inks are enabling improved recyclability of paper and packaging materials, aligning with Europe’s sustainability goals.

Regulatory frameworks such as the EU Ecodesign standards are promoting transparency through digital product passports, ensuring traceability and environmental compliance. Technological advancements include the development of water-vapor-resistant UV coatings, supporting applications in hydrogen-based energy systems.

Significant investments in renewable energy-powered production facilities are enhancing the manufacturing of eco-friendly UV resins. Germany also dominates in low-migration UV inks for pharmaceutical and laboratory applications, where purity and safety are critical. Expansion of UV ink systems for recyclable packaging solutions is further strengthening Germany’s position as a leader in sustainable and high-performance UV curable inks.

India’s Growth Driven by Telecom Expansion and Domestic Manufacturing Initiatives

India is emerging as a high-growth region in the UV curable inks market, supported by rapid telecom expansion and strong government initiatives under the “Make-in-India” framework. The BharatNet project is significantly increasing demand for UV inks used in fiber optic networks, particularly those designed to withstand tropical climate conditions.

Government incentives under the PLI Scheme 2.0 are encouraging domestic production of UV printing equipment, reducing dependence on imports. Technological advancements include the development of quick-cure UV-LED inks for railway applications, enabling faster maintenance and reduced downtime for modern train systems.

Industrial expansion is also driving growth, with significant investments in UV-curable coatings for furniture and manufacturing sectors. Regulatory updates such as the Quality Control Order are ensuring adherence to performance standards, boosting the adoption of high-quality inks. Key applications include anti-counterfeiting UV security inks for pharmaceutical packaging, ensuring authenticity and cold-chain compliance, which is critical in India’s growing healthcare sector.

Japan’s Nano-Precision UV Ink Technologies for Electronics and Medical Applications

Japan continues to lead in nano-engineered UV curable inks, focusing on precision, performance, and advanced applications in electronics and healthcare. Innovations such as ultra-thin nanostructured UV coatings are enhancing optical clarity in wearable devices, ensuring high sensitivity and performance.

Technological advancements include the use of AI-driven predictive modeling to optimize ink properties, improving production efficiency and reducing waste. Strategic investments by major corporations are expanding the development of UV-curable anti-fogging coatings, particularly for medical devices and endoscopy applications.

Product innovation also extends to photocatalytic self-cleaning UV inks, which contribute to environmental sustainability by breaking down pollutants on surfaces. Regulatory updates are ensuring durability and resistance to harsh environmental conditions, reinforcing Japan’s leadership in high-performance coatings. Additionally, specialized clean-room facilities are supporting the production of anti-static UV inks for semiconductor manufacturing, highlighting Japan’s role in advanced electronics coatings.

South Korea’s Innovation in 6G-Enabled UV Inks and Smart Wearable Applications

South Korea is rapidly advancing in the UV curable inks market, leveraging its leadership in semiconductors and next-generation electronics. Technological breakthroughs include the commercialization of conductive UV inks integrated with carbon nanotubes, enabling advanced functionalities in 6G-enabled devices and wearable sensors.

Product innovation is focused on EMI shielding UV inks, protecting sensitive electronics in robotics and communication systems. Significant investments are supporting the development of radar-absorbent coatings for defense applications, particularly in advanced fighter jet systems.

Key applications include the integration of UV-curable smart-heating inks in automotive interiors, enhancing user experience in EVs. Regulatory updates promoting eco-friendly formulations are accelerating the shift toward UV-LED silicone-based inks, reducing solvent usage and improving sustainability. Infrastructure developments such as advanced materials clusters are further strengthening South Korea’s position as a global hub for next-generation UV ink technologies and smart coating solutions.

Ultraviolet Curable Inks Market Report Scope

Ultraviolet Curable Inks Market

Parameter

Details

Market Size (2025)

$2.1 Billion

Market Size (2032)

$2.9 Billion

Market Growth Rate

4.6%

Segments

By Printing Process (UV Flexographic Inks, UV Digital, UV Offset, UV Screen Printing Inks, UV Gravure Inks, UV Letterpress Inks), By Curing Type (UV-LED Curing, Mercury Vapor, Hybrid Systems), By Resin Chemistry (Free Radical Curable, Cationic Curable, Hybrid Systems), By Ink Form and Composition (Liquid Inks, Paste Inks, Low-Migration Inks, Specialty and Functional Inks), By Substrate (Plastics and Polymers, Paper and Paperboard, Metal, Glass and Ceramics, Wood and Textiles), By End-User Industry (Packaging, Commercial Printing and Publication, Outdoor Advertising and Signage, Electronics and Semiconductors, Automotive, Medical and Healthcare, Consumer Goods), By Sales Channel (Direct Sales, Specialized Chemical and Ink Distributors, Value-Added Resellers)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

Sun Chemical, DIC Corporation, Flint Group, Siegwerk Druckfarben AG and Co. KGaA, Toyo Ink SC Holdings Co., Ltd., Fujifilm Holdings Corporation, INX International Ink Co., Hubergroup Holding SE, TandK TOKA Corporation, Zeller+Gmelin GmbH and Co. KG, Marabu GmbH and Co. KG, Nazdar Ink Technologies, Wikoff Color Corporation, Mimaki Engineering Co., Ltd., Roland DG Corporation, 8.16. Kao Collins Inc.

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Ultraviolet Curable Inks Market Segmentation

By Printing Process

UV Flexographic Inks

UV Digital

UV Offset

UV Screen Printing Inks

UV Gravure Inks

UV Letterpress Inks

By Curing Type

UV-LED Curing

Mercury Vapor

Hybrid Systems

By Resin Chemistry

Free Radical Curable

Cationic Curable

Hybrid Systems

By Ink Form and Composition

Liquid Inks

Paste Inks

Low-Migration Inks

Specialty and Functional Inks

By Substrate

Plastics and Polymers

Paper and Paperboard

Metal

Glass and Ceramics

Wood and Textiles

By End-User Industry

Packaging

Commercial Printing and Publication

Outdoor Advertising and Signage

Electronics and Semiconductors

Automotive

Medical and Healthcare

Consumer Goods

By Sales Channel

Direct Sales

Specialized Chemical and Ink Distributors

Value-Added Resellers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Ultraviolet Curable Inks Industry

Sun Chemical

DIC Corporation

Flint Group

Siegwerk Druckfarben AG & Co. KGaA

Toyo Ink SC Holdings Co., Ltd.

Fujifilm Holdings Corporation

INX International Ink Co.

Hubergroup Holding SE

T&K TOKA Corporation

Zeller+Gmelin GmbH & Co. KG

Marabu GmbH & Co. KG

Nazdar Ink Technologies

Wikoff Color Corporation

Mimaki Engineering Co., Ltd.

Roland DG Corporation

Kao Collins Inc.

*- List not Exhaustive

Table of Contents: Ultraviolet Curable Inks Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Ultraviolet Curable Inks Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Ultraviolet Curable Inks Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Demand Drivers in Energy-Cured Printing, Circular Packaging, and Regulatory Compliance

2.4. Sustainability Trends and Innovation in Low-Migration and Recyclable Ink Systems

2.5. Strategic Opportunities and Future Outlook

3. Innovations Reshaping the Ultraviolet Curable Inks Market

3.1. Trend: REACH Annex XIV Inclusion of Photoinitiators Accelerates Transition to Low-Migration UV Ink Systems

3.2. Trend: China GB 46997-2025 and GB/T 41653-2025 Establish Unified Framework for Heavy Metals and Migration Control

3.3. Opportunity: LED-UV Curable Inks Enable High-Speed, Energy-Efficient Digital Printing at Industrial Scale

3.4. Opportunity: UV-Curable Inks Expand into Functional 3D Printing with Engineering-Grade Performance

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Formulation Innovation

4.3. Sustainability and Circular Economy Strategies

4.4. Capacity Expansion and Regional Market Development

5. Market Share and Segmentation Insights: Ultraviolet Curable Inks Market

5.1. By Printing Process

5.1.1. UV Flexographic Inks

5.1.2. UV Digital

5.1.3. UV Offset

5.1.4. UV Screen Printing Inks

5.1.5. UV Gravure Inks

5.1.6. UV Letterpress Inks

5.2. By Curing Type

5.2.1. UV-LED Curing

5.2.2. Mercury Vapor

5.2.3. Hybrid Systems

5.3. By Resin Chemistry

5.3.1. Free Radical Curable

5.3.2. Cationic Curable

5.3.3. Hybrid Systems

5.4. By Ink Form and Composition

5.4.1. Liquid Inks

5.4.2. Paste Inks

5.4.3. Low-Migration Inks

5.4.4. Specialty and Functional Inks

5.5. By Substrate

5.5.1. Plastics and Polymers

5.5.2. Paper and Paperboard

5.5.3. Metal

5.5.4. Glass and Ceramics

5.5.5. Wood and Textiles

5.6. By End-User Industry

5.6.1. Packaging

5.6.2. Commercial Printing and Publication

5.6.3. Outdoor Advertising and Signage

5.6.4. Electronics and Semiconductors

5.6.5. Automotive

5.6.6. Medical and Healthcare

5.6.7. Consumer Goods

5.7. By Sales Channel

5.7.1. Direct Sales

5.7.2. Specialized Chemical and Ink Distributors

5.7.3. Value-Added Resellers

6. Country Analysis and Outlook of Ultraviolet Curable Inks Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Ultraviolet Curable Inks Market Size Outlook by Region (2025–2034)

7.1. North America Ultraviolet Curable Inks Market Size Outlook to 2034

7.1.1. By Printing Process

7.1.2. By Curing Type

7.1.3. By Resin Chemistry

7.1.4. By Ink Form and Composition

7.1.5. By Substrate

7.1.6. By End-User Industry

7.1.7. By Sales Channel

7.2. Europe Ultraviolet Curable Inks Market Size Outlook to 2034

7.2.1. By Printing Process

7.2.2. By Curing Type

7.2.3. By Resin Chemistry

7.2.4. By Ink Form and Composition

7.2.5. By Substrate

7.2.6. By End-User Industry

7.2.7. By Sales Channel

7.3. Asia Pacific Ultraviolet Curable Inks Market Size Outlook to 2034

7.3.1. By Printing Process

7.3.2. By Curing Type

7.3.3. By Resin Chemistry

7.3.4. By Ink Form and Composition

7.3.5. By Substrate

7.3.6. By End-User Industry

7.3.7. By Sales Channel

7.4. South America Ultraviolet Curable Inks Market Size Outlook to 2034

7.4.1. By Printing Process

7.4.2. By Curing Type

7.4.3. By Resin Chemistry

7.4.4. By Ink Form and Composition

7.4.5. By Substrate

7.4.6. By End-User Industry

7.4.7. By Sales Channel

7.5. Middle East and Africa Ultraviolet Curable Inks Market Size Outlook to 2034

7.5.1. By Printing Process

7.5.2. By Curing Type

7.5.3. By Resin Chemistry

7.5.4. By Ink Form and Composition

7.5.5. By Substrate

7.5.6. By End-User Industry

7.5.7. By Sales Channel

8. Company Profiles: Leading Players in the Ultraviolet Curable Inks Market

8.1. Sun Chemical

8.2. DIC Corporation

8.3. Flint Group

8.4. Siegwerk Druckfarben AG and Co. KGaA

8.5. Toyo Ink SC Holdings Co., Ltd.

8.6. Fujifilm Holdings Corporation

8.7. INX International Ink Co.

8.8. Hubergroup Holding SE

8.9. TandK TOKA Corporation

8.10. Zeller+Gmelin GmbH and Co. KG

8.11. Marabu GmbH and Co. KG

8.12. Nazdar Ink Technologies

8.13. Wikoff Color Corporation

8.14. Mimaki Engineering Co., Ltd.

8.15. Roland DG Corporation

8.16. Kao Collins Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Ultraviolet Curable Inks Market Segmentation

By Printing Process

UV Flexographic Inks

UV Digital

UV Offset

UV Screen Printing Inks

UV Gravure Inks

UV Letterpress Inks

By Curing Type

UV-LED Curing

Mercury Vapor

Hybrid Systems

By Resin Chemistry

Free Radical Curable

Cationic Curable

Hybrid Systems

By Ink Form and Composition

Liquid Inks

Paste Inks

Low-Migration Inks

Specialty and Functional Inks

By Substrate

Plastics and Polymers

Paper and Paperboard

Metal

Glass and Ceramics

Wood and Textiles

By End-User Industry

Packaging

Commercial Printing and Publication

Outdoor Advertising and Signage

Electronics and Semiconductors

Automotive

Medical and Healthcare

Consumer Goods

By Sales Channel

Direct Sales

Specialized Chemical and Ink Distributors

Value-Added Resellers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global Ultraviolet Curable Inks Market was valued at $2.1 billion in 2025 and is projected to reach $2.9 billion by 2032, growing at a CAGR of 4.6% during the forecast period. Rising demand for energy-efficient printing technologies, sustainable packaging, and high-speed digital printing systems is supporting long-term market growth globally.

UV-LED curing systems are gaining popularity because they provide instant curing, lower energy consumption, minimal heat generation, and reduced VOC emissions compared to traditional mercury vapor systems. These technologies also support high-speed production, superior substrate compatibility, and improved sustainability in flexible packaging, label printing, and digital printing applications.

Regulations such as EU REACH, German Printing Ink Ordinance (GIO), and China GB 46997-2025 are accelerating the development of low-migration, BPA-free, VOC-free, and heavy-metal-free UV ink formulations. Manufacturers are increasingly adopting polymeric photoinitiators and recyclable ink chemistries to comply with strict food-contact and environmental safety standards.

The market is witnessing rapid innovation in hybrid aqueous-UV technologies, recyclable UV inks, LED-UV digital printing systems, and UV-curable functional materials for 3D printing. Advanced formulations now offer faster curing, improved pigment stability, superior adhesion, enhanced recyclability, and engineering-grade performance for industrial and packaging applications.

Major companies operating in the market include Sun Chemical, DIC Corporation, Flint Group, Siegwerk Druckfarben AG & Co. KGaA, Toyo Ink SC Holdings Co., Ltd., and Fujifilm Holdings Corporation. These companies are investing in low-migration formulations, LED-UV technologies, recyclable packaging inks, and high-speed digital printing innovations.