Automotive Shielding Market Size and Growth Driven by EV Electrification and Thermal Management Needs

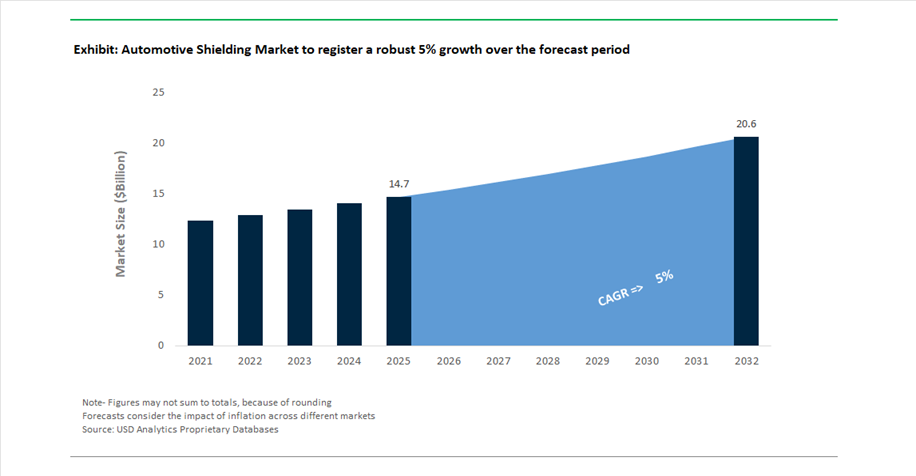

The Automotive Shielding Market is projected to grow from USD 14.7 billion in 2025 to USD 20.7 billion by 2032, registering a CAGR of 5%. This market plays a critical role in ensuring vehicle safety, electronic reliability, and thermal stability, particularly as modern vehicles become increasingly dependent on complex electronic systems and electrified powertrains.

Automotive shielding solutions are designed to address two primary challenges: electromagnetic interference (EMI) protection and thermal management. With the rapid proliferation of ADAS, infotainment systems, battery management systems, and high-voltage EV architectures, the density of electronic components within vehicles has increased significantly. This creates a heightened risk of signal interference, overheating, and component failure, making shielding materials essential for maintaining system integrity and operational reliability.

In electric vehicles, shielding is especially critical for battery packs, power electronics, and high-voltage cables, where effective thermal insulation and fire resistance are required to prevent thermal runaway and ensure passenger safety. Materials such as lightweight composites, advanced polymers, and metal-based shielding systems are being engineered to deliver high performance with reduced weight, supporting overall vehicle efficiency and range optimization.

The market is also influenced by growing regulatory focus on vehicle safety, electromagnetic compatibility (EMC), and sustainability, pushing manufacturers toward recyclable, low-emission, and high-durability shielding solutions. Competitive dynamics are shaped by innovation in material science, integration of multi-functional shielding systems, and strategic investments in EV-focused technologies, positioning automotive shielding as a foundational component of next-generation mobility platforms

Lightweight Shielding Innovation, EV Battery Protection, and Strategic Expansion Transforming Market Dynamics

The automotive shielding market is undergoing rapid transformation driven by lightweight material innovation, electrification trends, and strategic global expansion. A major development occurred in May 2025, when Autoneum introduced a lightweight composite battery shielding plate, utilizing long-fiber thermoplastic (LFT) technology. This innovation provides impact protection, fire resistance, and corrosion shielding, while significantly reducing weight compared to traditional metal solutions, directly contributing to improved EV driving range.

Product innovation is increasingly focused on thermal and fire protection for EV systems. In March 2026, Autoneum expanded its portfolio with E-Fiber Flame Shields, designed specifically for battery electric vehicles (BEVs). These recyclable polyester-based solutions deliver enhanced thermal insulation and fire resistance, aligning with the industry’s shift toward circular economy principles. Similarly, Schlegel Electronic Materials’ silicone-free thermal shielding solutions (March 2025) address critical challenges such as outgassing and interference in ADAS and optical systems, ensuring long-term reliability of sensitive electronics.

Strategic investments and acquisitions are reinforcing market capabilities. Parker Hannifin’s acquisition of Filtration Group Corporation (November 2025) strengthens its position in EMI shielding and thermal management materials, particularly through its Chomerics division. Meanwhile, Autoneum’s dual acquisitions in China (March 2026) expand its footprint in the world’s largest EV market, supported by the establishment of a Shanghai R&D center focused on cost-efficient shielding solutions for local OEMs.

Sustainability and advanced material development are key innovation drivers. Henkel’s expansion of its Teroson MS 9381 HPT line (April 2026) introduces solvent-free, silicone-free, and PVC-free formulations, providing UV-resistant shielding and bonding solutions for vehicle structures. Additionally, Henkel’s Shanghai Innovation Center (February 2026) is accelerating the development of next-generation EMI shielding and thermal interface materials, targeting the rapidly growing Chinese EV ecosystem.

Corporate restructuring and operational focus are also shaping the competitive landscape. ElringKlinger’s divestment of its UK subsidiary (November 2025) reflects a strategic pivot toward high-margin component businesses, including thermal and acoustic shielding systems. The company’s subsequent ramp-up in e-mobility orders (March 2026) highlights strong demand for shielding components in EV production.

Technological integration across vehicle systems is further driving innovation. Tenneco’s advanced passive valve technology (March 2026) incorporates shielding mechanisms to protect sensitive components from debris, corrosion, and environmental exposure, demonstrating the increasing convergence of mechanical systems and protective shielding technologies.

Hybrid Shielding Solutions Enhancing ADAS Sensor Performance and Weight Efficiency

The rapid evolution of Advanced Driver Assistance Systems is creating demand for next-generation shielding solutions that balance electromagnetic performance with lightweight design. Traditional die-cast aluminum enclosures are increasingly being replaced by hybrid shielding systems that combine conductive polymer over-molding with strategically placed metallic inserts.

These hybrid solutions offer significant weight advantages, reducing enclosure mass by 30% to 50% compared to conventional aluminum housings. This contributes directly to improved vehicle energy efficiency and extended driving range in electric vehicles. At the same time, advanced conductive polymers incorporating carbon nanotubes or graphene fillers provide tailored dielectric properties that reduce radar backscatter, improving sensor resolution by approximately 12%.

Manufacturing efficiency is another key benefit. Over-molding processes consolidate multiple assembly steps into a single operation, reducing production complexity and lowering total manufacturing costs by up to 20%. Additionally, modern hybrid materials are achieving thermal conductivities in the range of 3.0 to 5.0 W/m·K, enabling dual functionality as both electromagnetic shields and heat dissipation components for high-performance sensor processors.

Ultra-Thin Conductive Foams Enabling Reliable Shielding in Digital Cockpit Displays

The expansion of digital cockpit architectures, including large-format and curved displays, is driving demand for advanced shielding materials capable of maintaining electrical continuity in complex geometries. Formable conductive foams are emerging as a key solution, providing both electromagnetic shielding and grounding functionality in thin, flexible formats.

These next-generation materials are engineered for high resilience, with compression recovery rates exceeding 95%, ensuring consistent contact resistance even under continuous vibration conditions typical of automotive environments. Electrical performance is equally critical, with advanced conductive foams achieving contact resistance levels below 0.05 ohms, enabling effective grounding for high-frequency display systems operating at refresh rates above 120 Hz.

Design flexibility is a major advantage. Form-in-place and die-cut foam gaskets can be applied to intricate, curved surfaces with thicknesses as low as 0.2 mm, supporting the integration of next-generation OLED displays in modern vehicle interiors. Durability testing further validates their performance, with these materials maintaining shielding effectiveness above 70 dB after 5,000 hours of exposure to high humidity conditions (85% relative humidity at 85°C).

Heat Shielding Dominates Automotive Shielding Market with 62% Share Driven by High-Temperature Powertrain Protection

Shielding Type Analysis: Advanced Thermal Management Solutions Lead with Hybrid and ICE Demand

Heat shielding commands a dominant 62.0% share of the automotive shielding market in 2025, driven by the critical need to manage extreme exhaust system temperatures ranging from 800°C to 1,000°C in internal combustion engine (ICE) and hybrid vehicles. Key applications include turbocharger heat shields, exhaust manifold protection, catalytic converter shields, and underbody thermal barriers, all essential for safeguarding nearby components such as wiring harnesses, fuel systems, and battery packs. The rise of hybrid vehicles (HEVs and PHEVs) has further amplified demand, creating complex thermal conflict zones where hot exhaust systems coexist with temperature-sensitive lithium-ion batteries, requiring multi-layer shielding solutions. Additionally, advancements in lightweight composite heat shields, including aluminized polyamide, glass fiber composites, and ceramic-coated stainless steel, are driving innovation by combining thermal insulation with aerodynamic efficiency. These factors solidify heat shielding as the backbone of the automotive thermal management market.

Passenger Cars Lead Automotive Shielding Market with 72% Share Driven by High Production Volume and Component Density

Vehicle Type Analysis: EV Transition and Electronics Integration Boost Shielding Demand

Passenger cars dominate the automotive shielding market with a 72.0% share in 2025, supported by global production volumes of approximately 70 million units annually and increasing component density in modern vehicle architectures. Tight engine bay packaging and proximity between heat sources and sensitive electronics necessitate extensive use of both thermal and electromagnetic shielding solutions. The ongoing shift toward electric vehicles (EVs) introduces new requirements, including battery pack fire protection shields, high-voltage cable insulation, and EMI shielding for power electronics, ensuring compliance with safety standards such as UN GTR No. 20 and China GB 38031-2020. Additionally, premium vehicles are incorporating advanced materials like ceramic fiber barriers, gold foil reflective shielding, and titanium exhaust wraps, enhancing performance and durability. Combined with increasing adoption of ADAS, connectivity systems, and high-voltage architectures, passenger cars remain the primary driver of growth in the global automotive shielding market.

Automotive Shielding Market Competitive Landscape Driven by EV Thermal Management, EMI Shielding, and Lightweight Materials

The automotive shielding market is evolving with rising demand for EV thermal shielding, electromagnetic interference (EMI) shielding, and lightweight acoustic insulation. Key players are focusing on multifunctional shielding systems, liquid-applied coatings, and high-frequency EMI solutions to support ADAS, autonomous driving, and electrified powertrains.

Autoneum leads automotive shielding with lightweight acoustic-thermal integration for EV platforms

Autoneum holds a strong position in automotive shielding with an 8.0% global market share, driven by its expertise in acoustic and thermal management solutions. The company is advancing multifunctional heat shields that combine sound absorption and thermal insulation, addressing the noise sensitivity of electric vehicles. Its Hybrid-Acoustics and Ultra-Silent product lines utilize fiber-based materials that reduce weight by 20% compared to conventional metallic shields. Autoneum’s solutions are deployed across 75% of leading European EV platforms, supported by a just-in-time manufacturing model. The company achieved 40% recycled fiber content in 2025, aligning with circular economy requirements. Product development focuses on lightweight, sustainable, and high-performance shielding materials.

Henkel expands automotive shielding with liquid-applied EMI protection and dual-cure technologies

Henkel is a leader in liquid-applied automotive shielding, particularly for high-density PCB protection in ADAS and infotainment systems. The launch of Loctite Stycast UV 7998 in 2026 introduced a solvent-free conformal coating with UL 94 V-0 rating, reducing sprayed volume by four times while enhancing EMI and moisture protection. Its dual-cure UV/moisture technology ensures complete coverage in complex electronic assemblies, eliminating shadowing issues. The company expanded its innovation footprint with a new Shanghai center to support 800V SiC power electronics development. Strategic partnerships with Tier-1 suppliers enable integration of EMI shielding into battery management systems. Product innovation focuses on advanced electronics protection and sustainable coating technologies.

Dana strengthens EV shielding leadership with multi-layer thermal protection and drivetrain integration

Dana Incorporated is a key player in automotive shielding, particularly in battery thermal management for electric vehicles. Its multi-layer steel heat shields offer 99% radiant heat reflection, protecting lithium-ion batteries from thermal stress. The company is dedicating 45% of its R&D pipeline to electrified drivetrain shielding, including high-voltage cable protection and electromagnetic containment. Dana supplies modular underbody shielding systems that enhance vehicle aerodynamics and improve range by 2–3%. Strong financial performance, with $10.6 billion in 2025 sales, supports continued investment in EV technologies. Product development focuses on thermal efficiency, safety, and integrated shielding systems.

3M advances automotive shielding with AI-driven EMI solutions and radar-transparent materials

3M is a leading innovator in automotive shielding materials, combining advanced adhesives with EMI shielding technologies. At CES 2026, the company introduced AI-powered simulation tools to optimize shielding performance for connected and autonomous vehicles. Its conductive tapes and absorbers are widely used in ADAS and display systems, supporting frequencies from 24GHz to 77GHz. Self-bonding materials reduce the need for mechanical fasteners, lowering vehicle weight and assembly complexity. The company also launched lightweight EMI gaskets designed for high-vibration EV environments. Product innovation focuses on high-frequency shielding, adhesive integration, and digital simulation capabilities.

Laird Performance Materials drives high-frequency shielding innovation with MXene-based solutions

Laird Performance Materials, part of DuPont, specializes in high-frequency EMI shielding for next-generation automotive electronics. The company introduced bio-based EMI enclosures in 2026, combining sustainability with high-performance polymer science. Its MXene-based shielding materials deliver conductivity of 35,000 S/cm and block over 80 dB of interference at 18 GHz, supporting advanced autonomous systems. Laird dominates the telematics control unit segment with precision shielding components that ensure stable 5G connectivity. Expansion of rapid prototyping services enables EV startups to accelerate product development cycles. Product development focuses on high-frequency performance, sustainability, and rapid customization.

China Automotive Shielding Market: EV Safety Regulations and AI-Driven EMI Shielding Driving Scale Leadership

China’s automotive shielding market is undergoing rapid transformation, driven by stringent EV safety regulations and the rise of AI-powered mobility systems. The implementation of 2026 EV Battery Safety Regulations mandates that battery packs withstand up to 2 hours without fire or explosion during thermal runaway, significantly increasing demand for high-performance fire-retardant heat shields. This regulatory push is reshaping shielding design standards across the EV ecosystem.

Technological innovation is equally impactful. The surge in AI-driven autonomous “world model” processors is driving demand for high-frequency EMI shielding solutions to protect sensitive electronics. China is also leading in product innovation, with the commercialization of flexible silver-nanowire transparent EMI shields for HUDs and smart windshields. Additionally, the adoption of radar-transparent shielding materials is enabling seamless integration of ADAS systems while minimizing signal interference. Large-scale manufacturing expansion in regions like the Greater Bay Area is further reinforcing China’s position as a global leader in automotive shielding technologies.

United States Automotive Shielding Market: Circular Shielding Economy and High-Voltage Electronics Driving Innovation

The United States automotive shielding market is evolving through sustainability initiatives and advancements in high-voltage power electronics. The shift toward a “circular shielding economy” is accelerating the adoption of PFAS-free EMI shielding materials, particularly foams and gaskets, in response to state-level environmental regulations.

Innovation is focused on performance and manufacturability. The development of 3D-printed EMI shields for zonal control units (ZCUs) is enabling complex geometries required for next-generation software-defined vehicles. Additionally, federal investments in silicon carbide (SiC) semiconductor manufacturing are driving demand for high-temperature dielectric shielding materials. Lightweighting strategies, supported by stricter CAFE standards, are promoting the use of ultra-thin aluminum heat shields to reduce vehicle weight and improve efficiency. Strategic expansions by major material suppliers are also strengthening the supply chain for advanced thermal and EMI shielding solutions.

Germany remains a global leader in automotive shielding technologies, particularly in high-frequency applications and precision engineering. The expansion of ultra-fast charging infrastructure (400kW+) is driving demand for EMI-shielded cable assemblies, ensuring safe and efficient power transfer in EV ecosystems.

Technological advancements are redefining product capabilities. The commercialization of intelligent heat shields embedded with thin-film sensors allows real-time monitoring of exhaust temperatures, improving diagnostics and performance. Additionally, Germany is standardizing multi-layer heat shield systems for hybrid vehicles and advancing metamaterial-based shielding for V2X communication systems. Sustainability is also a key focus, with the adoption of recycled carbon-fiber EMI shields to meet EU circular economy targets. These innovations position Germany at the forefront of high-performance automotive shielding solutions.

India Automotive Shielding Market: Localization Push and Cost-Effective Hybrid Shielding Driving Growth

India’s automotive shielding market is transitioning from cost-driven manufacturing to high-tech production under the “Make in India” initiative. The PLI scheme for advanced automotive technology is encouraging local production of dielectric shielding solutions for battery management systems (BMS), strengthening domestic capabilities.

The market is characterized by rapid infrastructure and manufacturing expansion. New production facilities, such as advanced heat shield manufacturing lines, are supporting both ICE and EV applications. Innovations such as aluminum-ceramic hybrid shields are addressing the high-vibration conditions of electric three-wheelers, while high-reflectivity coatings for heat shields are improving thermal management in tropical climates. Additionally, the expansion of testing infrastructure for EMI/EMC validation is enhancing product quality and compliance, positioning India as a key emerging market in automotive shielding.

South Korea Automotive Shielding Market: Dielectric Barrier Innovation and Lightweight EMI Solutions Leading EV Development

South Korea is a global leader in automotive shielding technologies, particularly in EV-specific dielectric and EMI shielding solutions. The establishment of dedicated shielding and insulation R&D centers by Hyundai and Kia is accelerating the development of high-voltage protection systems for next-generation EV platforms.

Innovation is focused on performance, weight reduction, and safety. The commercialization of graphene-doped EMI shielding paints is reducing component weight by up to 40% compared to traditional metal housings, while maintaining high shielding effectiveness. Additionally, the integration of dielectric powder coatings in EV motor housings is preventing parasitic currents and improving system reliability. Strategic partnerships between battery manufacturers are advancing thermal barrier materials for cell-to-pack designs, while new safety standards require shielding systems to maintain integrity under extreme conditions. These developments position South Korea as a leader in advanced EV shielding technologies.

Japan Automotive Shielding Market: Nanoscale Precision and Sensor-Integrated Shielding Driving Advanced Applications

Japan’s automotive shielding market is defined by its leadership in precision engineering and integration with advanced sensor systems. The development of hydrophilic self-cleaning EMI shields is improving visibility and reliability for automotive camera modules, particularly in adverse weather conditions.

Innovation is also focused on multifunctional materials. Japan is advancing signal-transparent shielding materials that allow seamless operation of LiDAR and radar systems, while maintaining aesthetic quality. Additionally, the development of stress-relief conformal coatings that act as secondary EMI shields is enhancing durability in miniaturized electronic systems. Regulatory mandates for recyclability are further driving innovation in sustainable shielding materials. These advancements position Japan as a global leader in high-performance, sensor-integrated automotive shielding technologies.

Automotive Shielding Market Report Scope

Automotive Shielding Market

Parameter

Automotive Shielding Market

Market Size (2025)

$14.7 Billion

Market Size (2032)

$20.7 Billion

Market Growth Rate

5%

Segments

By Shielding (Heat Shielding, Electromagnetic Interference (EMI) Shielding), By Material Chemistry (Metallic Shielding, Composite Shielding), By Application Area (Thermal Applications, EMI and EMC Applications), By Propulsion Technology (Internal Combustion Engine (ICE), Battery Electric Vehicle (BEV), Hybrid Electric Vehicle, Fuel Cell Electric Vehicle (FCEV)), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV)), By Sales Channel (OEM, Aftermarket)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Automotive Shielding Market Segmentation

By Shielding

Heat Shielding

Electromagnetic Interference (EMI) Shielding

By Material Chemistry

Metallic Shielding

Composite Shielding

By Application Area

Thermal Applications

Exhaust Systems and Turbochargers

Engine Compartment (Under-bonnet)

Under-chassis and Fuel Tank Protection

Battery Thermal Management Systems (BTMS)

EMI and EMC Applications

ADAS and Safety Systems (Radar, LiDAR, Camera modules)

EV Powertrain (Inverters, Electric Motors, On-board Chargers)

High-Voltage Cabling and Connectors

Infotainment, Connectivity (V2X), and Telematics

By Propulsion Technology

Internal Combustion Engine (ICE)

Battery Electric Vehicle (BEV)

Hybrid Electric Vehicle

Fuel Cell Electric Vehicle (FCEV)

By Vehicle Type

Passenger Cars

Light Commercial Vehicles (LCV)

Heavy Commercial Vehicles (HCV)

By Sales Channel

OEM

Aftermarket

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Automotive Shielding Market

Tenneco Inc.

Dana Incorporated

ElringKlinger AG

Autoneum Holding AG

Laird Performance Materials

Parker Hannifin Corporation

3M Company

Henkel AG & Co. KGaA

Morgan Advanced Materials plc

Schaffner Holding AG

Kitagawa Industries Co., Ltd.

Marian, Inc.

Tech-Etch, Inc.

Lydall, Inc.

TE Connectivity

*- List not Exhaustive

Table of Contents: Automotive Shielding Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Automotive Shielding Market Landscape & Outlook (2025–2032)

2.1. Introduction to Automotive Shielding Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Market Drivers: EV Electrification, ADAS Expansion, and Electronic Component Density

2.4. Regulatory Landscape: EMC Compliance, Safety Standards, and Sustainability Requirements

2.5. Technology Evolution: Lightweight Materials, Multi-Functional Shielding, and Thermal Management Systems

3. Innovations Reshaping the Automotive Shielding Market

3.1. Trend: Lightweight Composite and Hybrid Shielding Solutions for EV Efficiency

3.2. Trend: Advanced EMI Shielding for High-Frequency ADAS and Connectivity Systems

3.3. Opportunity: Thermal and Fire Protection Solutions for EV Battery Systems

3.4. Opportunity: Ultra-Thin Conductive Materials for Digital Cockpit and Display Applications

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Automotive Shielding Market

The automotive shielding market is estimated at USD 14.7 billion in 2025 and is projected to reach USD 20.7 billion by 2032, registering a CAGR of 5%. Growth is driven by increasing electronic complexity in vehicles and the rapid expansion of electric vehicle (EV) platforms requiring advanced shielding solutions.

Automotive shielding ensures protection against electromagnetic interference (EMI) and manages thermal loads in high-density electronic environments. It is essential for maintaining signal integrity in ADAS systems, preventing overheating in power electronics, and ensuring safety in high-voltage EV architectures.

EVs significantly increase the demand for both thermal and EMI shielding. Battery packs, inverters, and high-voltage cables require fire-resistant and thermally stable materials to prevent thermal runaway. Additionally, shielding solutions must be lightweight to support vehicle range and efficiency optimization.

Key trends include hybrid shielding systems combining conductive polymers and metals, ultra-thin conductive foams for digital displays, and recyclable composite heat shields. Innovations such as graphene-enhanced materials and radar-transparent shielding are also improving ADAS performance and reducing vehicle weight.

Leading players include Autoneum Holding AG, Dana Incorporated, 3M Company, Henkel AG & Co. KGaA, and Parker Hannifin Corporation, focusing on lightweight materials, EV shielding, and high-frequency EMI solutions.