Physical Vapor Deposition (PVD) on Plastics Market Size, Lightweight Metallization Demand, and Functional Surface Engineering

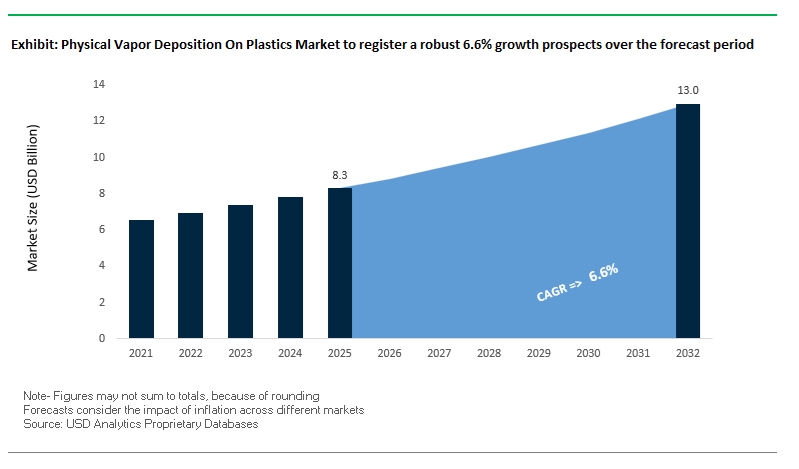

The global Physical Vapor Deposition (PVD) on Plastics Market was valued at $8.3 billion in 2025 and is projected to grow at a CAGR of 6.6% through 2032, reaching $13 billion by 2032. This growth is driven by the increasing demand for lightweight, corrosion-resistant, and aesthetically advanced plastic components across automotive, consumer electronics, packaging, and emerging energy applications.

PVD on plastics enables the deposition of thin metallic or ceramic layers onto polymer substrates, delivering properties such as enhanced conductivity, barrier protection, decorative finishes, and improved wear resistance without significantly increasing weight. This makes it a critical technology in industries transitioning toward lightweight materials and multifunctional components, particularly in electric vehicles, aerospace, and portable electronics.

A major growth driver is the replacement of traditional electroplating processes, which involve hazardous chemicals, with vacuum-based PVD technologies that offer superior environmental compliance and process control. In automotive interiors and consumer products, PVD coatings are increasingly used to achieve premium chrome-like finishes, “dead-front” display surfaces, and scratch-resistant decorative elements, aligning with evolving design and sustainability expectations.

Additionally, the integration of PVD coatings into functional applications such as electromagnetic shielding, thermal management, and corrosion resistance is expanding their role beyond aesthetics. This is particularly relevant in AI-driven electronics, hydrogen energy systems, and advanced composite materials, where plastic substrates require enhanced performance characteristics to meet demanding operational conditions.

Recent developments in the PVD on plastics market highlight a strong convergence of process innovation, application diversification, and regional expansion. In September 2025, Kolzer’s merger into Kolzer International marked a significant step toward scaling “PVD 2.0” technologies, designed for high-throughput coating of plastic components in automotive and cosmetics applications. The expansion into new operational hubs reflects growing global demand for efficient, large-scale PVD processing capabilities.

Innovation in manufacturing integration is also reshaping the market. Kurz’s expansion of IMD Varioform® technology (2025) enables the direct integration of PVD metallization within injection molding processes, allowing manufacturers to produce functional and decorative surfaces in a single step. This approach is particularly impactful in automotive interiors, where “dead-front” displays and touch-sensitive surfaces are becoming standard design elements.

The market is also expanding into energy transition applications. Impact Coatings’ growth in coating services (February 2026) is being driven by demand for PVD-metallized plastic components in hydrogen fuel cells and electrolyzers, where coatings provide critical electrical conductivity and corrosion resistance. This highlights the increasing role of PVD in enabling next-generation clean energy technologies.

Advanced manufacturing systems are supporting broader adoption. Singulus Technologies’ TIMARIS system order (December 2025) underscores demand for modular vacuum coating platforms capable of processing complex plastic substrates for electronics and sensor applications. Meanwhile, Applied Materials’ insights (February 2026) indicate that AI-driven semiconductor packaging is increasing the need for PVD coatings on advanced polymer substrates, particularly for thermal and electromagnetic management.

Supporting technologies and tooling innovations are also critical to ecosystem development. CemeCon’s collaboration with Hufschmied (January 2026) focuses on PVD-coated tools for machining carbon fiber reinforced plastics (CFRP), addressing challenges in manufacturing high-performance composite materials used in aerospace and automotive sectors.

Regional expansion remains a key strategic priority. Kolzer’s planned expansion into Asia targets consumer electronics and luxury packaging hubs, while Impact Coatings’ investment in service centers reflects growing adoption across Europe, North America, and China.

Market Trend: Automotive Shift to PVD Chromium and CrN Coatings for Sustainable, High-Durability Plastic Components

The physical vapor deposition on plastics industry is experiencing a structural transition as automotive OEMs replace hexavalent chromium electroplating with PVD chromium and chromium nitride coatings for interior and exterior trim. This shift is driven by the convergence of environmental compliance, worker safety, and the need for durable premium finishes on lightweight polymer substrates such as ABS and PC blends.

PVD chromium coatings deliver comparable baseline hardness to electroplated chrome at approximately 1,000 HV, ensuring that aesthetic and tactile expectations are maintained. However, when combined with chromium nitride base layers, hardness values exceed 2,200 HV, representing a 120% improvement in scratch resistance. This enhanced hardness is critical for high-contact automotive components such as door handles, center consoles, and dashboard trims that are subject to repeated abrasion.

Wear resistance is also significantly improved. Testing on PVD-coated plastic substrates indicates a 30% increase in wear performance compared to traditional chromium-plated systems. This directly extends the cosmetic lifespan of interior components, reducing warranty claims and improving perceived vehicle quality over time.

From an environmental perspective, the transition to PVD represents a major process innovation. Unlike electroplating, which involves multiple wet chemical stages and hazardous waste streams, PVD is a dry, vacuum-based deposition process that eliminates volatile organic compound emissions and hexavalent chromium exposure. This simplifies compliance with global environmental and occupational safety regulations while supporting automotive manufacturers’ broader sustainability targets.

Market Trend: DLC and TiN PVD Coatings Enabling Premium Durability and Aesthetics in Consumer Electronics

The consumer electronics sector is rapidly adopting diamond-like carbon and titanium nitride PVD coatings for plastic and composite housings in devices such as smartphones, wearables, and accessories. These coatings enable manufacturers to achieve a metallic appearance and tactile feel while maintaining the lightweight and cost advantages of polymer substrates.

Diamond-like carbon coatings offer exceptional hardness, reaching up to 3,000 HV, along with an ultra-low coefficient of friction. This combination prevents surface degradation such as polishing, buffing, or gloss variation that typically occurs with uncoated or painted plastic housings during daily use. The result is a consistent, high-quality surface finish that retains its appearance over extended product lifecycles.

Titanium nitride coatings contribute both functional and aesthetic benefits. These coatings maintain thermal stability up to approximately 1,100°C, providing protection against heat exposure during manufacturing processes and high-performance device operation, including rapid charging cycles. In addition, TiN and zirconium nitride coatings enable the creation of premium metallic color finishes such as champagne and rose gold.

Color stability is a key differentiator. PVD-generated metallic finishes demonstrate approximately 50% higher resistance to fading and discoloration compared to organic lacquer-based coatings. This ensures long-term visual consistency, which is critical in high-end consumer electronics where design and durability are tightly integrated.

Market Opportunity: EPA Chromium Plating Regulations Driving Accelerated Adoption of PVD on Plastics

Regulatory developments in the United States are creating a strong substitution opportunity for PVD coatings on plastic substrates. Updates to the National Emission Standards for Hazardous Air Pollutants under 40 CFR Part 63 are increasing compliance complexity for chromium electroplating operations, particularly for decorative applications on plastics.

Current requirements mandate strict control of bath surface tension and emissions, often requiring advanced fume suppression systems and continuous monitoring. These regulatory burdens are increasing operational costs and capital investment requirements for plating facilities, particularly for small and mid-sized operators.

PVD technology offers a clear alternative as a zero-discharge process that eliminates the need for chemical baths, wastewater treatment, and emissions control systems. Manufacturers transitioning to PVD can reduce federal reporting and compliance obligations by approximately 60% to 70%, streamlining operations while maintaining high-performance finishes.

This regulatory-driven shift is accelerating the adoption of PVD coatings in automotive, electronics, and consumer goods sectors, where manufacturers are seeking both compliance and long-term cost efficiency.

Market Opportunity: China Green Product Standards Driving Demand for Low-Emission PVD Finishes on Plastic Substrates

China’s implementation of GB/T 39789-2026 is creating significant growth opportunities for PVD coatings on plastics by introducing stringent environmental and safety requirements for surface finishes. The standard imposes strict limits on hazardous substances, including hexavalent chromium and phthalates, which are commonly associated with traditional coating and plating processes.

PVD coatings provide a functional advantage by forming dense, inert barrier layers that prevent the migration of heavy metals from the substrate. These coatings enable manufacturers to meet the required thresholds for harmful substance content, including limits on total heavy metals below 90 mg/kg for export-grade products.

In addition to chemical safety, the standard introduces strict requirements for formaldehyde and VOC emissions. Products seeking Green Product certification must demonstrate zero-formaldehyde emissions, effectively eliminating the use of conventional paint systems that rely on primers and clearcoats. PVD technology, as a dry and solvent-free process, aligns directly with these requirements.

Given China’s role as a global manufacturing hub for consumer electronics, automotive components, and household goods, the enforcement of these standards is driving a large-scale transition toward advanced PVD finishing technologies. Suppliers offering compliant, high-performance coating solutions are positioned to benefit from increased demand across multiple high-volume production sectors.

PVD on Plastics Market Share and Segmentation Insights

Topcoat Segment Captures 45.8% Share Driven by Surface Protection and Aesthetic Control

The physical vapor deposition (PVD) on plastics market by component layer is dominated by the topcoat segment, accounting for 45.8% of global market share in 2025, due to its critical role in enhancing both durability and visual performance. In PVD-coated plastic components, thin metallic layers such as chrome, aluminum, or brass-tone finishes require protection from abrasion, oxidation, and fingerprinting, which is provided by UV-cured acrylic or polyurethane topcoats. These topcoats also enable precise control over gloss levels and surface texture, ensuring premium finish quality. Additionally, they allow color customization and effect tuning, enabling finishes like black chrome, rose gold, and smoked nickel without altering the underlying PVD material. This flexibility is highly valued in automotive interiors, consumer electronics, and cosmetic packaging, driving strong demand for advanced decorative PVD coatings on plastics.

Outsourced Services Hold 55.3% Share Driven by Technical Complexity and Production Flexibility

In the PVD on plastics market by sales channel, outsourced coating services lead with a 55.3% market share in 2025, reflecting the high level of technical complexity and process specialization required. Coating plastic substrates such as ABS, PC/ABS, and nylon presents unique challenges, including outgassing, thermal sensitivity, and the need for low-temperature deposition (<80°C) to prevent deformation. Contract coating providers have developed proprietary racking systems, surface preparation methods, and controlled vacuum processes to address these challenges effectively. Additionally, outsourced services offer volume flexibility, enabling manufacturers in automotive, consumer electronics, and cosmetic packaging industries to scale production for seasonal demand and product launches without investing in expensive in-house PVD systems. As demand for high-quality decorative and functional coatings on plastics continues to grow, outsourced services remain the preferred model in the global PVD plastics coatings market.

Competitive Landscape of the Physical Vapor Deposition (PVD) on Plastics Market

Oerlikon Balzers Leads Decorative and Functional Plastic Coatings with ePD™ Technology

Oerlikon Balzers is the global leader in the PVD on plastics market, particularly for automotive and consumer electronics applications. Its proprietary ePD™ (embedded PVD for Design parts) technology enables chrome-like finishes on plastic components that are radar-transparent, making them ideal for ADAS systems. The company’s INVENTA PVD system, introduced in 2025, incorporates Advanced Arc Technology to reduce energy consumption by 20% while operating below 120°C—critical for heat-sensitive polymers. Oerlikon’s strong vertical integration, combining equipment manufacturing with coating-as-a-service, allows rapid prototyping and scalable production of complex 3D plastic components with zero VOC emissions.

Ionbond Expands Decorative PVD Coatings with Sustainable and PFAS-Free Technologies

IHI Ionbond AG is a key innovator in the decorative PVD coatings market for plastics, offering premium metallic finishes through its Decobond™ series. Its coatings deliver high wear resistance and a premium tactile experience, targeting luxury appliances and aerospace interiors. In 2026, Ionbond published research on low-temperature PVD processes for recycled plastics, supporting circular economy goals. The company is also focusing on replacing PFAS and chrome-based coatings with non-toxic alternatives, aligning with global environmental regulations. Its collaborations with additive manufacturing firms enable efficient coating of 3D-printed plastic components, enhancing production efficiency and durability.

Kolzer Leads Industrial-Scale Plastic Metallization with High-Vacuum Sputtering Systems

Kolzer Srl is a leading provider of PVD equipment for plastic metallization, particularly in Europe. Its DGK series represents one of the most advanced horizontal vacuum systems, enabling one-step coating processes for automotive lighting and large plastic components with full recyclability. Kolzer’s hybrid sputtering and PECVD systems allow simultaneous deposition of metallic and protective layers, eliminating the need for additional coating steps. The company specializes in coating complex 3D geometries with high precision, making it a preferred partner for industries requiring uniform thin-film deposition on intricate plastic parts.

Impact Coatings Drives Functional Plastic Coatings with EMI Shielding and Integrated Production Systems

Impact Coatings AB is a specialized leader in functional PVD coatings for plastics, particularly in EMI/RFI shielding applications for electronics. Its solutions provide superior electrical conductivity compared to traditional conductive paints, making them essential for 5G-enabled devices and smart electronics. The company’s INLINECOATER™ system integrates PVD coating directly into injection molding processes, enabling a seamless “mold-to-finish” workflow. Strong demand from China’s electronics market has driven growth in its coating services segment. Impact Coatings is also expanding into hydrogen-related applications, strengthening its position in advanced functional coating technologies.

Veeco Advances Thin-Film Coatings for Flexible Electronics and Display Applications

Veeco Instruments, Inc. plays a critical role in the PVD on plastics market, particularly in flexible electronics and display technologies. Its high-throughput sputtering systems enable deposition of ultra-thin Indium Tin Oxide (ITO) coatings on plastic substrates used in foldable smartphones and touchscreens. The company is focusing on low-damage deposition processes to protect sensitive organic layers in OLED production. With increasing demand from AI-driven hardware and next-generation displays, Veeco is strengthening its position in high-precision thin-film deposition for flexible substrates.

Singulus Expands High-Volume PVD Production for Medical and Semiconductor Plastic Applications

Singulus Technologies AG is a key player in high-volume PVD coating systems for plastics, offering advanced cluster tool platforms such as TIMARIS and ROTARIS. These systems enable deposition of ultra-thin films on plastic wafers and sensors, supporting applications in medical diagnostics and semiconductor manufacturing. Singulus is also expanding into photovoltaic applications, applying PVD coatings to lightweight plastic solar modules to enhance efficiency. Its expertise in automated production lines positions the company as a leader in precision coating technologies for high-volume industrial applications.

China PVD on Plastics Market: High-Purity Coatings for 5G, NEVs, and Advanced Polymer Metallization

China continues to dominate the PVD on plastics market, evolving rapidly toward ultra-high purity (UHP) coatings on engineering polymers to support high-growth sectors such as 5G/6G telecommunications and New Energy Vehicles (NEVs). Regulatory enforcement under GB 30981.1-2025 has accelerated the shift to water-borne UV PVD primers, significantly reducing VOC emissions across major chemical clusters in Guangdong and Zhejiang.

Technological advancements are centered on magnetron sputtering on advanced substrates like PEEK and polyimide, enabling ultra-clean metallization for semiconductor components such as FOUP systems. The integration of PVD-metallized plastic antenna arrays is improving signal transmission efficiency, outperforming traditional LDS technologies. Automotive innovation is also a key driver, with increasing adoption of backlit PVD-coated plastics in smart cabin interiors. Large-scale investments, including the Meishan Industrial Base expansion, and innovations such as multi-component alloy sputtering targets for single-step TiAlN deposition, further strengthen China’s leadership in high-volume, high-performance PVD plastic coatings.

Germany PVD on Plastics Market: Circular Economy Leadership and Chrome-Free Automotive Solutions

Germany is leading the global transition toward sustainable PVD coatings on plastics, particularly within the automotive and medical sectors. The phase-out of traditional chrome plating under EU REACH Annex XIV has accelerated the adoption of PVD-coated PC/ABS materials for exterior automotive trim, delivering enhanced durability and environmental compliance.

German innovation is also focused on digital traceability and recyclability, with plasma-assisted markers embedded within PVD layers to enable automated sorting of metallized plastics with high accuracy. The establishment of a HiPIMS-focused center in Münster is advancing coating density and performance, rivaling traditional electroplating methods. Additionally, the development of low-temperature deposition processes allows coating of heat-sensitive polymers without deformation. The introduction of Blue Angel eco-label criteria for metallized plastics further reinforces Germany’s leadership in environmentally responsible PVD coating technologies.

United States PVD on Plastics Market: Aerospace Lightweighting and Medical Device Innovation

The U.S. PVD on plastics market is witnessing strong growth across aerospace, healthcare, and electronics, driven by innovation and regulatory transformation. Aerospace manufacturers are increasingly adopting PVD-coated CFRP components, achieving significant weight reduction while maintaining performance in non-structural applications.

In the semiconductor ecosystem, CHIPS Act-driven investments are fueling demand for PVD-coated fluoropolymer components used in ultra-pure water systems. The medical device industry is rapidly adopting Titanium-PVD coatings on plastic components to meet biocompatibility and sterilization standards. The expansion of domestic manufacturing capabilities, including roll-to-roll PVD systems for flexible electronics, is supporting nearshoring efforts. Additionally, regulatory pressures such as the EPA NESHAP mandate are accelerating the replacement of traditional chrome plating with vacuum metallization technologies. Innovations in UV-LED curing systems are also reducing energy consumption, enhancing production efficiency in U.S. PVD lines.

Japan PVD on Plastics Market: Precision Sputtering for Optical and 6G Applications

Japan remains a global leader in precision PVD coatings on plastics, particularly for advanced optics, telecommunications, and high-performance packaging. The country is pioneering ultra-thin PVD layers on plastic surfaces for 6G infrastructure, enabling building facades to function as passive signal reflectors in smart urban environments.

Breakthroughs such as photocatalytic PVD hybrid coatings are enabling self-sanitizing plastic surfaces in public transit systems. Japanese manufacturers are also advancing active packaging technologies, utilizing PVD-coated PET films with oxygen-scavenging properties to extend product shelf life. The adoption of DMD-modulated sputtering is enabling highly detailed textures on consumer electronics, while the surge in AR/VR device production is driving demand for anti-reflective PVD coatings on plastic lenses with near-perfect light transmission. Updated standards such as JIS R 1703:2024 are setting global benchmarks for adhesion and performance on recycled plastic substrates.

India PVD on Plastics Market: Manufacturing Growth and PLI-Driven Localization

India is emerging as a high-growth market in the PVD on plastics industry, supported by the Make in India initiative, PLI schemes, and expanding automotive and electronics manufacturing sectors. The automotive industry is increasingly adopting PVD-coated plastic components for exterior trim, replacing traditional painted finishes to enhance durability and aesthetics.

Government support through the PLI scheme for specialty chemicals is encouraging local production of PVD targets and coatings, reducing dependency on imports. Smart infrastructure projects are driving demand for PVD-coated plastic hardware designed to withstand harsh environmental conditions. The rapid growth of consumer electronics manufacturing has led to the installation of multiple high-volume PVD systems in hubs such as Noida and Chennai. Additionally, innovations in agritech, including PVD-metallized plastic sensors for soil monitoring, are creating new application areas, further strengthening India’s position in the global PVD coatings market.

South Korea PVD on Plastics Market: Semiconductor Precision and OLED Encapsulation

South Korea’s PVD on plastics market is closely aligned with its leadership in semiconductors, OLED displays, and advanced packaging technologies. The development of plasma-resistant PVD coatings for plastics is critical for 3D NAND and FinFET fabrication processes, particularly within the Gyeonggi-do semiconductor cluster.

The country leads in Thin-Film Encapsulation (TFE) technologies, using PVD-based inorganic layers to protect flexible OLED displays from moisture ingress. South Korea is also innovating in marine applications with PVD-infused anti-fouling plastic panels, offering environmentally friendly alternatives to traditional coatings. Advances in low-voltage curing processes are enabling PVD coatings on highly heat-sensitive plastic substrates, while high-barrier PVD coatings are widely used in food packaging to block UV light and oxygen. Additionally, the K-beauty sector is driving demand for PVD-metallized recycled plastic packaging, combining premium aesthetics with sustainability.

Brazil PVD on Plastics Market: Healthcare Expansion and Bio-Based Innovation

Brazil is emerging as a growing market in the PVD on plastics sector, driven by rising healthcare investments and a focus on sustainable material integration. Increased healthcare spending is supporting the adoption of PVD-coated plastic medical devices and disposables, improving durability and hygiene standards.

The country’s leadership in bio-ethanol production is enabling the integration of bio-based solvents into pre-treatment processes for PVD coatings, supporting environmentally friendly manufacturing. Industrial expansion, including PPG’s Sumaré plant, is boosting demand for PVD-coated plastic components in agricultural machinery. Given Brazil’s high solar exposure, R&D is focused on improving UV resistance and coating durability using advanced stabilizers. Additionally, the growth of retail distribution networks is accelerating the adoption of premium PVD-finished home hardware, while efforts to localize PVD target production are strengthening supply chain resilience.

Physical Vapor Deposition On Plastics Market Report Scope

Physical Vapor Deposition On Plastics Market

Parameter

Details

Market Size (2025)

$8.3 Billion

Market Size (2032)

$13 Billion

Market Growth Rate

6.6%

Segments

By Deposition Technology (Sputter Deposition, Thermal Evaporation, Cathodic Arc Deposition, High-Power Impulse Magnetron Sputtering, Plasma-Enhanced PVD), By Plastic Substrate Type (ABS, PC, PC, PMMA, PP, PET, PA, TPU, PEEK and High-Performance Polymers), By Coating Material (Metals, Ceramics and Oxides, Carbon-based, Precious Metals), By End-Use Industry (Automotive, Consumer Electronics, Packaging, Home Appliances, Medical Devices, Aerospace), By Component Layer (Basecoat, PVD Layer, Topcoat), By Sales Channel (In-house PVD Equipment, Outsourced Coating Services, PVD Equipment and Target Material Sales)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Physical Vapor Deposition On Plastics Market Segmentation

By Deposition Technology

Sputter Deposition

Thermal Evaporation

Cathodic Arc Deposition

High-Power Impulse Magnetron Sputtering

Plasma-Enhanced PVD

By Plastic Substrate Type

ABS

PC

PC

PMMA

PP

PET

PA

TPU

PEEK and High-Performance Polymers

By Coating Material

Metals

Ceramics and Oxides

Carbon-based

Precious Metals

By End-Use Industry

Automotive

Consumer Electronics

Packaging

Home Appliances

Medical Devices

Aerospace

By Component Layer

Basecoat

PVD Layer

Topcoat

By Sales Channel

In-house PVD Equipment

Outsourced Coating Services

PVD Equipment and Target Material Sales

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Physical Vapor Deposition On Plastics Industry

Oerlikon Balzers

Vergason Technology, Inc.

Hauzer Techno Coating B.V.

Applied Materials, Inc.

Bühler Group

IHI Ionbond AG

Impact Coatings AB

Vapor Technologies, Inc.

Singulus Technologies AG

Kolzer Srl

Denton Vacuum, LLC

Mustang Vacuum Systems Inc.

Aalberts Surface Technologies

Semicore Equipment, Inc.

Angstrom Engineering Inc.

*- List not Exhaustive

Table of Contents: Physical Vapor Deposition On Plastics Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Physical Vapor Deposition On Plastics Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Physical Vapor Deposition On Plastics Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Dynamics and Growth Drivers

2.4. Regulatory and Sustainability Landscape

2.5. Strategic Developments and Future Outlook

3. Innovations Reshaping the Physical Vapor Deposition On Plastics Market

3.1. Trend: Automotive Shift to PVD Chromium and CrN Coatings for Sustainable Plastic Components

3.2. Trend: DLC and TiN PVD Coatings Enabling Premium Consumer Electronics Finishes

3.3. Opportunity: EPA Chromium Plating Regulations Accelerating PVD Adoption on Plastics

3.4. Opportunity: China Green Product Standards Driving Low-Emission PVD Finishes

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Physical Vapor Deposition On Plastics Market

5.1. By Deposition Technology

5.1.1. Sputter Deposition

5.1.2. Thermal Evaporation

5.1.3. Cathodic Arc Deposition

5.1.4. High-Power Impulse Magnetron Sputtering

5.1.5. Plasma-Enhanced PVD

5.2. By Plastic Substrate Type

5.2.1. ABS

5.2.2. PC

5.2.3. PMMA

5.2.4. PP

5.2.5. PET

5.2.6. PA

5.2.7. TPU

5.2.8. PEEK and High-Performance Polymers

5.3. By Coating Material

5.3.1. Metals

5.3.2. Ceramics and Oxides

5.3.3. Carbon-based

5.3.4. Precious Metals

5.4. By End-Use Industry

5.4.1. Automotive

5.4.2. Consumer Electronics

5.4.3. Packaging

5.4.4. Home Appliances

5.4.5. Medical Devices

5.4.6. Aerospace

5.5. By Component Layer

5.5.1. Basecoat

5.5.2. PVD Layer

5.5.3. Topcoat

5.6. By Sales Channel

5.6.1. In-house PVD Equipment

5.6.2. Outsourced Coating Services

5.6.3. PVD Equipment and Target Material Sales

6. Country Analysis and Outlook of Physical Vapor Deposition On Plastics Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Physical Vapor Deposition On Plastics Market Size Outlook by Region (2025–2034)

7.1. North America Physical Vapor Deposition On Plastics Market Size Outlook to 2034

7.1.1. By Deposition Technology

7.1.2. By Plastic Substrate Type

7.1.3. By Coating Material

7.1.4. By End-Use Industry

7.1.5. By Component Layer

7.1.6. By Sales Channel

7.2. Europe Physical Vapor Deposition On Plastics Market Size Outlook to 2034

7.2.1. By Deposition Technology

7.2.2. By Plastic Substrate Type

7.2.3. By Coating Material

7.2.4. By End-Use Industry

7.2.5. By Component Layer

7.2.6. By Sales Channel

7.3. Asia Pacific Physical Vapor Deposition On Plastics Market Size Outlook to 2034

7.3.1. By Deposition Technology

7.3.2. By Plastic Substrate Type

7.3.3. By Coating Material

7.3.4. By End-Use Industry

7.3.5. By Component Layer

7.3.6. By Sales Channel

7.4. South America Physical Vapor Deposition On Plastics Market Size Outlook to 2034

7.4.1. By Deposition Technology

7.4.2. By Plastic Substrate Type

7.4.3. By Coating Material

7.4.4. By End-Use Industry

7.4.5. By Component Layer

7.4.6. By Sales Channel

7.5. Middle East and Africa Physical Vapor Deposition On Plastics Market Size Outlook to 2034

7.5.1. By Deposition Technology

7.5.2. By Plastic Substrate Type

7.5.3. By Coating Material

7.5.4. By End-Use Industry

7.5.5. By Component Layer

7.5.6. By Sales Channel

8. Company Profiles: Leading Players in the Physical Vapor Deposition On Plastics Market

8.1. Oerlikon Balzers

8.2. Vergason Technology, Inc.

8.3. Hauzer Techno Coating B.V.

8.4. Applied Materials, Inc.

8.5. Bühler Group

8.6. IHI Ionbond AG

8.7. Impact Coatings AB

8.8. Vapor Technologies, Inc.

8.9. Singulus Technologies AG

8.10. Kolzer Srl

8.11. Denton Vacuum, LLC

8.12. Mustang Vacuum Systems Inc.

8.13. Aalberts Surface Technologies

8.14. Semicore Equipment, Inc.

8.15. Angstrom Engineering Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Physical Vapor Deposition On Plastics Market Segmentation

By Deposition Technology

Sputter Deposition

Thermal Evaporation

Cathodic Arc Deposition

High-Power Impulse Magnetron Sputtering

Plasma-Enhanced PVD

By Plastic Substrate Type

ABS

PC

PC

PMMA

PP

PET

PA

TPU

PEEK and High-Performance Polymers

By Coating Material

Metals

Ceramics and Oxides

Carbon-based

Precious Metals

By End-Use Industry

Automotive

Consumer Electronics

Packaging

Home Appliances

Medical Devices

Aerospace

By Component Layer

Basecoat

PVD Layer

Topcoat

By Sales Channel

In-house PVD Equipment

Outsourced Coating Services

PVD Equipment and Target Material Sales

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global Physical Vapor Deposition on Plastics Market was valued at $8.3 billion in 2025 and is projected to reach $13 billion by 2032, expanding at a CAGR of 6.6%. Market growth is being driven by increasing demand for lightweight, corrosion-resistant, and aesthetically advanced plastic components across automotive, electronics, packaging, aerospace, and energy applications.

Automotive OEMs and consumer electronics brands are increasingly adopting PVD chromium, CrN, DLC, and TiN coatings on plastics to replace traditional electroplating and painted finishes. These coatings provide superior scratch resistance, premium metallic aesthetics, enhanced wear protection, electromagnetic shielding, and long-term color stability while supporting lightweighting and environmental compliance objectives.

Stringent environmental regulations targeting hexavalent chromium plating, VOC emissions, and hazardous substances are accelerating the adoption of vacuum-based PVD technologies on plastic substrates. Standards such as U.S. EPA NESHAP updates and China’s GB/T 39789-2026 are encouraging manufacturers to transition toward solvent-free, zero-discharge PVD processes that simplify compliance and reduce environmental impact.

Major companies operating in the PVD on plastics market include Oerlikon Balzers, IHI Ionbond AG, Kolzer Srl, Impact Coatings AB, and Singulus Technologies AG. These companies are investing in radar-transparent coatings, decorative metallization, EMI shielding solutions, low-temperature deposition systems, and high-throughput vacuum coating platforms to strengthen their positions in automotive, electronics, and advanced manufacturing applications.

The topcoat segment dominates the market with a 45.8% share due to its critical role in surface protection, gloss control, fingerprint resistance, and aesthetic customization in decorative plastic components. Outsourced coating services account for 55.3% market share because of the technical complexity associated with coating heat-sensitive polymer substrates. Regionally, China, Germany, the United States, Japan, India, South Korea, and Brazil are emerging as major investment markets driven by automotive lightweighting, consumer electronics growth, semiconductor expansion, and sustainable manufacturing initiatives.