Vanillin Market Growth Accelerated by Bio-Based Production, Clean-Label Demand, and Pharmaceutical Flavor-Masking Applications (2025–2034)

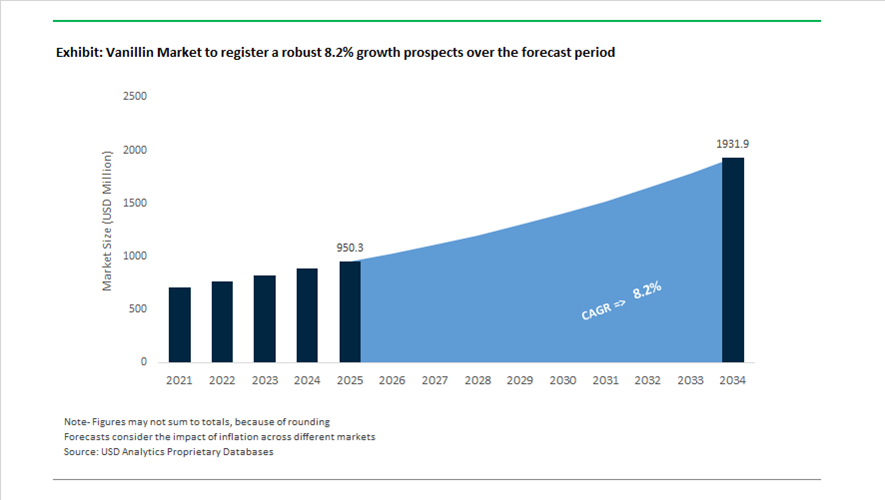

The Vanillin Market is projected to grow from USD 950.3 million in 2025 to USD 1,931.6 million by 2034, registering a robust CAGR of 8.2%, driven by escalating demand across food & beverages, pharmaceuticals, and cosmetics, alongside the accelerating shift toward clean-label and bio-based ingredients. As of early 2026, bio-vanillin production has reached approximately 1,200 tonnes annually, with fermentation-derived variants commanding premium pricing exceeding $700/kg, compared to ~$15/kg for synthetic vanillin, highlighting strong value differentiation for natural formulations. Despite this shift, petrochemical-based vanillin (guaiacol-derived) continues to dominate with ~65% of global volume, favored for cost efficiency, thermal stability, and consistency in large-scale bakery and confectionery applications. The compound also plays a critical role in pharmaceuticals, with ~49% of formulations utilizing vanillin for flavor masking, and is present in over 8,200 fragrance and cosmetic SKUs globally. Operationally, producers are optimizing output, with capacity utilization targets around 60% in early 2026, following strategic maintenance cycles in 2025. Meanwhile, sustainability benchmarks are improving, as lignin-based production processes achieve yields of 6.2%, supporting circular economy integration and reducing environmental impact through pulp and paper byproduct utilization.

The global vanillin industry is undergoing strategic transformation driven by bio-based innovation, capacity optimization, and regulatory shifts impacting trade flows and supply chains. In March 2026, Camlin Fine Sciences advanced its European expansion strategy by adjusting its tender offer timeline for Vinpai, reinforcing its position in specialty flavoring and shelf-life extension solutions across high-value markets. In February 2026, Borregaard reported record EBITDA of NOK 1,878 million for FY2025, supported by strong performance in its BioSolutions segment, particularly biovanillin demand across food and agricultural applications, signaling robust uptake of sustainable aromatic compounds. During the same month, Solvay reported a 20.7% EBITDA margin, alongside strategic restructuring initiatives, including capacity optimization in Spain and site closures in the UK and Portugal to prioritize high-margin natural vanillin products such as Rhovanil Natural.

Operational efficiency and production scaling remain central to market competitiveness. In January 2026, Camlin Fine Sciences confirmed the resolution of technical constraints at its vanillin manufacturing facility, enabling a production ramp-up aligned with rising global demand and price recovery trends in the US and European markets. Concurrently, Borregaard achieved industry recognition through the Carbon Footprint Innovation Award, highlighting advancements in low-carbon lignin-based vanillin production and reinforcing sustainability as a key differentiator. Earlier, in September 2025, Borregaard expanded its regional footprint by establishing new laboratories and sales offices in Mumbai, enhancing localized application development and technical support for South Asia’s rapidly growing food and pharmaceutical sectors.

Regulatory interventions and innovation funding are further reshaping global trade dynamics and R&D priorities. In June 2025, the U.S. Department of Commerce imposed countervailing duties on vanillin imports from China, creating favorable conditions for non-Chinese producers and altering global supply chains. Additionally, in May 2025, the European Union allocated €1.3 million in funding for Borregaard’s Biomer project, aimed at developing bio-based pest control solutions using vanillin derivatives, expanding the compound’s application scope beyond traditional flavoring. Collectively, these developments underscore a market transitioning toward bio-based production, regulatory-driven trade realignment, and high-value application diversification, positioning vanillin as a critical ingredient in next-generation sustainable and functional product formulations.

Trends and Opportunities in the Vanillin Market

Strategic Bio-Based Sourcing to Mitigate Regulatory and ESG Risks

The global vanillin market is undergoing a structural realignment as manufacturers actively de-risk their portfolios from petrochemical dependency and regulatory volatility. Synthetic guaiacol-based vanillin, long favored for cost efficiency, is increasingly exposed to ESG scrutiny, carbon disclosure requirements, and trade actions. In response, leading producers are accelerating capital allocation toward bio-based and lignin-derived vanillin platforms that offer regulatory resilience and long-term margin stability.

During 2024–2025, Syensqo significantly expanded its Rhovanil® Natural CW range, produced via bioconversion of ferulic acid extracted from rice bran. This shift is directly linked to the European Commission’s 2025 anti-dumping duties on Chinese synthetic vanillin, which materially altered the cost equation for EU-based food and flavor manufacturers. By securing EU-compliant, naturally derived vanillin at industrial scale, producers are protecting clean-label positioning while insulating supply chains from trade-related shocks.

Parallel to bioconversion, lignin valorization is emerging as a cornerstone of low-carbon vanillin supply. Borregaard reported in its Q3 2025 disclosures that demand for its wood-based vanillin continues to accelerate, supported by a documented carbon footprint reduction of approximately 90% versus oil-derived alternatives. This is particularly relevant for multinational chocolate, bakery, and confectionery brands targeting carbon-neutral product lines by 2026, where Scope 3 emissions linked to flavor ingredients are now under active review by investors and regulators.

Premiumization Through Traceability and Certified Natural Sourcing

Beyond volume substitution, the vanillin market is fragmenting into a clear two-tier structure, with a fast-growing premium segment defined by traceability, certification, and sensory differentiation. Luxury food, beverage, and fragrance brands are increasingly willing to pay a premium for vanillin that offers a verified origin story and compliance with emerging deforestation and biodiversity regulations.

In June 2025, Givaudan introduced Rainforest Alliance–certified vanilla and vanillin solutions for the European market, explicitly aligned with the EU Deforestation Regulation. This move enables downstream brands to demonstrate full supply chain transparency, a requirement that is rapidly becoming non-negotiable for premium positioning in Europe. Certified sourcing not only mitigates regulatory exposure but also supports premium pricing strategies in craft chocolate, artisanal dairy, and fine fragrance applications.

Biotechnology is reinforcing this premiumization trend through measurable sensory advantages. A late-2025 study published via the U.S. National Institutes of Health compared vanillin produced through solid-state fermentation of agri-food by-products with synthetic equivalents. Biotechnological vanillin demonstrated aroma profiles significantly closer to natural vanilla bean extract, enabling “natural” labeling claims that can command price premiums of up to three times those of conventional synthetic vanillin. This sensory differentiation is becoming a decisive competitive lever as consumers increasingly associate flavor authenticity with product quality and sustainability.

Enabling Deep Sugar Reduction and Better-for-You Reformulation

Vanillin’s role is expanding from a traditional flavor ingredient to a functional enabler of nutritional reformulation. As governments and health authorities intensify pressure to reduce added sugars, vanillin is being strategically deployed to modulate sweetness perception and mask bitterness in reduced-sugar and alternative-protein products.

Data from 2024–2025 trials under Kerry Group’s Tastesense™ Advanced platform show that vanillin-centered flavor systems can support sugar reductions of 30 to 50% without negatively impacting consumer acceptance. Vanillin enhances perceived sweetness intensity, allowing manufacturers to lower sucrose content in dairy, beverages, and bakery products while maintaining flavor balance. This functionality is increasingly critical as reformulation timelines compress under sugar taxes and front-of-pack labeling mandates.

In parallel, vanillin is playing a key role in the maturation of plant-based foods. Off-notes associated with pea, soy, and other plant proteins remain a primary barrier to repeat purchase. Natural vanillin grades developed by Syensqo, including Rhovanil® Natural Delica and Alta, are engineered for improved dispersion and stability in high-protein matrices. Their ability to suppress earthy or beany notes is reducing formulation cycles for clean-label vegan products, positioning vanillin as a strategic tool rather than a passive flavor additive.

High-Margin Pharmaceutical and Nutraceutical Therapeutics

A less visible but structurally important opportunity is emerging at the intersection of vanillin chemistry and biomedical innovation. Scientific validation of vanillin’s antioxidant, anti-inflammatory, and neuroprotective properties is opening pathways into pharmaceutical and nutraceutical applications that offer significantly higher margins than food and flavor uses.

Research published in December 2025 highlights vanillin’s utility as a multifunctional crosslinking agent in self-healing hydrogels for diabetic wound care and controlled drug delivery. These vanillin-based biomaterials leverage the compound’s inherent bioactivity to enhance therapeutic performance while maintaining biocompatibility, an attribute increasingly favored in advanced medical materials.

Additionally, pharmaceutical-grade vanillin is gaining traction as a functional excipient in nutraceutical formulations. Beyond improving the palatability of bitter APIs, vanillin contributes to oxidative stress mitigation, aligning with consumer demand for multifunctional supplements that combine sensory acceptability with measurable health benefits. As regulatory frameworks tighten around excipient transparency and quality, suppliers capable of delivering GMP-compliant vanillin with documented bioactivity are positioned to capture a defensible niche in life sciences markets.

Vanillin Market Share and Segmentation Insights

Product Type Market Share: Synthetic Vanillin Leads with Scalable Production and Cost Efficiency

Synthetic vanillin dominates the market with a 58.60% share in 2025, driven by its cost-effective production and ability to meet large-scale global demand across food, fragrance, and industrial applications. Produced primarily via guaiacol-based synthesis, it offers consistent quality and reliable supply compared to natural alternatives. Bio-vanillin, ethyl vanillin, and natural vanillin serve premium and niche segments with differentiated value propositions. A key industry trend is the dominance of guaiacol-based production routes, where integrated supply chains enable competitive pricing and stable availability, supporting widespread use in mass-market flavor and fragrance formulations.

Application Market Share: Food and Beverage Segment Leads with Global Flavor Consumption Demand

Food and beverage accounts for 68.40% of the vanillin market in 2025, reflecting its position as one of the most widely used flavoring agents in baked goods, confectionery, dairy products, beverages, and desserts. Fragrances and personal care, pharmaceuticals, animal feed, and agrochemicals represent additional application areas. A key growth trend is the increasing demand for clean label and natural ingredients, where bio-vanillin and natural extracts are gaining traction in premium food segments, while synthetic vanillin continues to dominate high-volume applications where cost efficiency and supply scalability remain critical factors.

Vanillin Market Competitive Landscape

The Vanillin market in 2026 is defined by feedstock diversification, bio-based production from lignin and ferulic acid, and vertically integrated supply chains, with anti-dumping protection and high-purity natural flavor compliance shaping competition across food, fragrance, and pharmaceutical applications.

Syensqo Expands Rhovanil® Bio-Based Vanillin for Natural Flavor Compliance and Feed Applications

Syensqo is reinforcing its leadership in the Vanillin market through its Rhovanil® technology, spanning both synthetic and bio-based high-purity vanillin production. The launch of Rhovea® Feed Vanillin targets premium animal nutrition, enhancing palatability in advanced feed formulations. Its Rhovanil® Natural CW, derived from ferulic acid bioconversion, supports natural flavor labeling under EU and FDA standards. With €1.21 billion EBITDA in 2025, the company benefits from a secure non-Chinese integrated supply chain, ensuring reliability for global food manufacturers. Its “One Planet” roadmap focuses on carbon neutrality and energy optimization across production sites. This combination of regulatory compliance and feedstock diversification strengthens Syensqo’s premium positioning.

Borregaard Leads Wood-Based Vanillin Production with Low-Carbon BioSolutions Platform

Borregaard ASA dominates the bio-based Vanillin market through lignin-derived production, offering a unique alternative to petrochemical synthesis. The company reported record EBITDA of NOK 1,878 million in 2025, driven by strong demand for biovanillin. Its products deliver up to 90% lower carbon footprint compared to guaiacol-based vanillin, making them highly attractive for sustainable cosmetics and fragrance applications. Expansion into India with a new Mumbai lab supports growth in dairy and confectionery sectors. Recognition with the HCPA Carbon Footprint Innovation Award reinforces its leadership in green aroma chemicals. This integrated wood-based value chain positions Borregaard as a benchmark in sustainable vanillin production.

Camlin Fine Sciences Strengthens Integrated Vanillin Supply with Anti-Dumping Advantage

Camlin Fine Sciences is emerging as a strong competitor in the Vanillin market by leveraging integrated catechol-based production and favorable trade policies. The company is scaling its Dahej facility toward a 4,000 MT production target by FY2027, improving capacity utilization and market share. Anti-dumping duties of up to 131% in Europe provide pricing leverage, enabling higher realization in key Western markets. The company reported 6% revenue growth to INR 572 crores in Q4 2025, supported by stable demand in aroma chemicals. Its fully integrated diphenol chain ensures cost efficiency and consistent product quality. This strategic positioning enhances its competitiveness against low-cost imports.

Jiaxing Zhonghua Chemical Dominates Global Vanillin Supply with Large-Scale Integrated Production

Jiaxing Zhonghua Chemical is the largest global producer in the Vanillin market, operating a 14,000 MT capacity facility that sets benchmark pricing for synthetic vanillin. Its ≥99.5% purity products meet global standards including FCC, USP, and BP, ensuring wide acceptance across food and pharmaceutical industries. The company’s fully integrated utilities and guaiacol-based production enhance cost efficiency and scalability. Its R&D focus on catalyst optimization reduces environmental impact while improving yield efficiency. Diversified offerings, including ethyl vanillin and ortho-vanillin, cater to high-intensity flavor applications in tobacco and beverages. This scale-driven strategy secures its dominance in bulk aroma chemical supply.

Ennolys Advances Fermentation-Based Natural Vanillin for Clean-Label Food Applications

Ennolys, a Lesaffre Group subsidiary, is strengthening its position in the Vanillin market through fermentation-based production of natural aromatic molecules. Its Ennallin® vanillin, derived from rice bran ferulic acid, achieves purity levels above 99% and complies with global natural flavor regulations. The product is increasingly adopted in clean-label dairy, plant-based beverages, and organic food formulations. Ennolys’ expertise in tailoring flavor profiles allows customization of creamy and nutty notes, reducing the need for additional additives. Its participation in CFIA Rennes 2026 highlights its focus on sustainable and traceable aroma solutions. This biotech-driven approach positions Ennolys in the high-value natural vanillin segment.

China Vanillin Market Recalibrated by Food Safety Standards and Trade Barriers

China’s vanillin market is undergoing a structural recalibration driven by tighter food safety oversight and escalating trade restrictions in Western markets. In August 2025, the National Health Commission formally notified the World Trade Organization of a draft national food safety standard dedicated to vanillin. The proposed framework specifies stringent physical and chemical benchmarks for synthetic vanillin, with the dual objective of strengthening domestic quality control and aligning export specifications with international expectations. This regulatory move is reshaping quality assurance protocols across major production clusters.

From a supply standpoint, China remains the global volume leader in synthetic vanillin, with annual production capacity exceeding 9,000 metric tons as of 2025. Manufacturing hubs in Jiangsu, Anhui, and Chongqing continue to anchor output, supported by upstream chemical integration. Players such as Anhui Guangxin Agrochemical have optimized phosgene-based chemical chains to lower the cost of guaiacol, the primary precursor in catechol-route vanillin synthesis. At the same time, producers including Jiaxing Zhonghua are diversifying into daily chemical and fragrance grades, targeting a domestic personal care sector that consumed roughly 2,000 metric tons of vanillin derivatives in 2025. However, export-oriented growth is constrained. In June 2025, the European Commission imposed definitive anti-dumping duties exceeding 130% on Chinese vanillin, while the United States levied duties above 230%. These measures are forcing Chinese exporters to pivot toward Southeast Asia and Latin America, even as Zhejiang-based facilities pilot low-carbon guaiacol synthesis programs under the 14th Five-Year Plan to cut emissions intensity by 20%.

India Vanillin Market Strengthened by Supply Chain Realignment and Pharma Demand

India’s vanillin market is emerging as a key beneficiary of global supply chain realignment away from China. In September 2025, Camlin Fine Sciences reported strong momentum in its vanillin and blends portfolio, positioning itself to capitalize on shifting sourcing strategies among multinational flavor houses. The company is preparing to supply approximately 2,700 tons of vanillin in FY 2026F, reflecting rising demand from North America and Europe seeking diversified and geopolitically resilient suppliers.

Capacity utilization and downstream diversification underpin this growth. Despite a brief maintenance shutdown in early FY26, Camlin’s vanillin facility is on a structured modernization roadmap aimed at reaching full utilization within the next 18 to 24 months. Indian manufacturers are also targeting pharmaceutical-grade vanillin, where the compound is widely used as a flavor-masking agent in pediatric formulations. Domestic pharmaceutical consumption of vanillin intermediates reached an estimated 1,200 metric tons in 2025. Beyond pharma, the high-margin blends segment encompassing antioxidants and vanillin grew by nearly 18% during the 2024–2025 cycle, driven by animal nutrition and pet food applications. Trade dynamics further favor India. Following steep U.S. tariffs on Chinese imports, Indian suppliers are positioned as the primary alternative, with industry expectations pointing toward partial tariff normalization in select Indo-U.S. corridors by 2026.

France Vanillin Market Anchored in Bio-Based Innovation and Regional Supply Security

France remains a strategic hub for high-value vanillin production, combining synthetic capacity resilience with leadership in bio-based alternatives. In September 2025, Syensqo, formerly Solvay, announced the reopening of its synthetic vanillin unit in Saint-Fons. The facility, temporarily mothballed in 2024 due to energy cost pressures, is scheduled to resume full operations by late 2025, reinforcing Europe’s ability to serve regional flavor houses amid trade barriers affecting Asian imports.

Bio-vanillin remains France’s defining strength. The country continues to lead global investment in fermentation-derived vanillin such as Rhovanil Natural, utilizing ferulic acid sourced from non-GMO rice bran. Government-backed circular economy initiatives, supported by the ADEME, are funding enzymatic and fermentation-based pathways in collaboration with biotech firms including Carbios and Evolva partners. By maintaining localized production across France, the United States, and Asia, French producers are ensuring responsiveness to European customers demanding shorter lead times, traceability, and reduced carbon footprints.

Norway Vanillin Market Defined by Lignin-Based Sustainability Leadership

Norway occupies a differentiated position in the global vanillin market through its exclusive lignin-based production route. Borregaard reported robust 2025 performance in its BioSolutions segment, underpinned by its status as the world’s only producer of vanillin derived from wood-based lignin. This unique process enables Borregaard to serve the natural-identical vanillin segment with strong sustainability credentials, allowing premium positioning among food, flavor, and specialty chemical buyers.

Operational efficiency and downstream diversification reinforce this advantage. Borregaard’s Sarpsborg biorefinery continues to convert approximately 90% of incoming wood raw material into high-value chemicals or renewable energy, reducing waste intensity and improving lifecycle metrics. In October 2025, the company highlighted sustained growth in agricultural applications, where vanillin-derived intermediates are increasingly used in specialty crop protection and feed additives. This cross-sector utilization enhances demand stability while reinforcing Norway’s reputation as a benchmark for circular bio-based chemistry.

United States Vanillin Market Shaped by Regulatory Clarity and Fermentation Partnerships

The United States vanillin market is influenced by regulatory definition, fragrance demand, and rapid progress in precision fermentation. In September 2025, the Flavor and Extract Manufacturers Association petitioned the U.S. Food and Drug Administration to retain the federal Standard of Identity for vanilla-vanillin extract. This effort aims to preserve clear labeling distinctions between bean-derived and synthetic flavorings, particularly in high-consumption categories such as ice cream and dairy desserts.

Beyond food, demand is expanding in fragrances and personal care. The U.S. daily chemical sector consumed nearly 1,500 metric tons of vanillin in 2025, driven by fine fragrances and botanical lotions emphasizing warm, natural scent profiles. At the innovation frontier, U.S.-based biotech collaborations involving International Flavors & Fragrances and Evolva secured multi-year supply agreements through 2026 for precision-fermentation vanillin. These partnerships are designed to meet growing consumer demand, particularly among younger demographics, for ethically produced and traceable flavor ingredients.

Summary of Country-Level Vanillin Market Dynamics

Vanillin Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Demand Drivers

|

Market Positioning

|

|

China

|

Regulatory tightening and cost-efficient synthesis

|

Food safety compliance, daily chemicals

|

Volume leadership with export reorientation

|

|

India

|

Supply chain diversification and pharma use

|

Flavor masking, nutrition blends

|

Preferred alternative sourcing hub

|

|

France

|

Bio-based leadership and regional resilience

|

Fermentation vanillin, EU supply security

|

High-value innovation center

|

|

Norway

|

Lignin-based circular production

|

Natural-identical vanillin, agriculture

|

Sustainability premium supplier

|

|

United States

|

Regulatory clarity and biotech fermentation

|

Fragrances, ethical ingredients

|

Innovation-driven demand market

|

Vanillin Market Report Scope

Vanillin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$950.3 Million

|

|

Market Size (2034)

|

$1931.6 Million

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Product Type (Synthetic Vanillin, Natural Vanillin, Bio-Vanillin, Ethyl Vanillin), By Form (Powder and Crystal, Liquid and Extract, Granules), By Application (Food and Beverage, Fragrances and Personal Care, Pharmaceuticals, Animal Feed, Agrochemicals and Others)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Syensqo, Borregaard ASA, Camlin Fine Sciences Limited, Jiaxing Zhonghua Chemical Co. Ltd., International Flavors and Fragrances Inc., Givaudan SA, Symrise AG, Evolva SA, Anhui Guangxin Agrochemical Co. Ltd., Liaoning Shixian Vanillin Co. Ltd., Zhengzhou Meheco, Mane SA, T. Hasegawa Co. Ltd., Kerry Group plc, Advanced Biotech

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Vanillin Market Segmentation

By Product Type

Guaiacol-based

Lignin-based

- Natural Vanillin

- Bio-Vanillin

- Ethyl Vanillin

By Form

- Powder and Crystal

- Liquid and Extract

- Granules

By Application

- Food and Beverage

- Fragrances and Personal Care

- Pharmaceuticals

- Animal Feed

- Agrochemicals and Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Vanillin Market

- Syensqo

- Borregaard ASA

- Camlin Fine Sciences Limited

- Jiaxing Zhonghua Chemical Co. Ltd.

- International Flavors and Fragrances Inc.

- Givaudan SA

- Symrise AG

- Evolva SA

- Anhui Guangxin Agrochemical Co. Ltd.

- Liaoning Shixian Vanillin Co. Ltd.

- Zhengzhou Meheco

- Mane SA

- T. Hasegawa Co. Ltd.

- Kerry Group plc

- Advanced Biotech

*- List not Exhaustive