Market Overview: Bio-Vanillin Market Growth Anchored in Fermentation Platforms, Wood-Based Routes, and Clean-Label Flavor Demand (2025–2034)

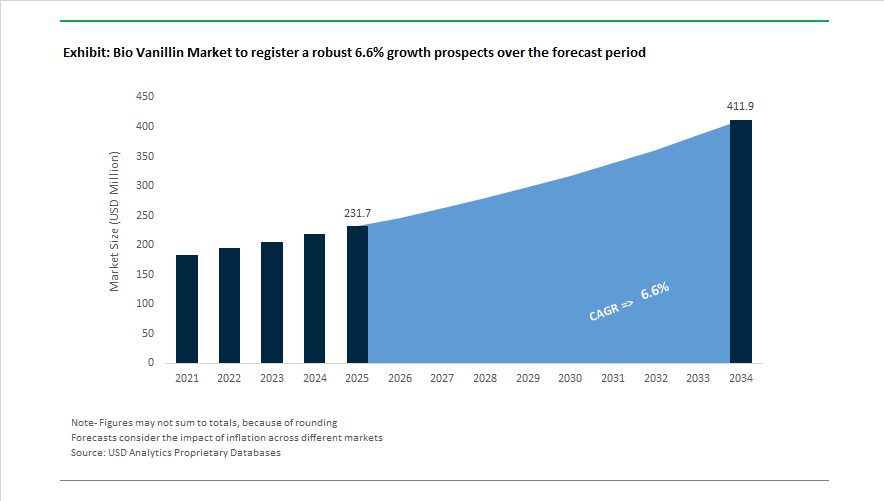

The bio vanillin market is projected to expand from USD 231.7 Million in 2025 to USD 411.9 Million by 2034, registering a CAGR of 6.6% supported by rising demand for natural flavoring agents, fermentation-derived aroma chemicals, and traceable clean-label ingredients across food, beverage, and personal care applications. Structural momentum in the bio-vanillin value chain accelerated in 2024. In June 2024, Givaudan established its House of Naturals division to consolidate expertise in fermentation-based ingredients, positioning bio-vanillin as a premium solution for high-end perfumery and food formulations requiring non-GMO traceability. In 2024, dsm-firmenich advanced integration of biotechnology platforms following its merger, optimizing microbial fermentation routes to produce vanillin from agricultural substrates such as rice bran and sugar. During the same period, Syensqo strengthened commercialization of its Rhovanil Natural portfolio across dairy and bakery applications, emphasizing tailored solubility and flavor intensity grades.

Regulatory clarity and regional demand shifts are reshaping global consumption patterns. In 2024, updated guidance from food safety authorities in Europe and the United States clarified labeling pathways for vanillin classified as natural flavor, enabling FMCG brands to accelerate adoption of bio-based variants. Givaudan’s AI-driven FlavourVision program launched in 2024 highlighted rising use of bio-vanillin in plant-based dairy alternatives to mask protein off-notes. Geographic demand realignment became evident in 2025 when Asia-Pacific emerged as the largest consumer region, accounting for over 40% of global bio-vanillin use, driven by expanding food processing hubs in China, Japan, and India. Production capacity and application innovation are scaling accordingly. In November 2025, Givaudan expanded its PlanetCaps biodegradable encapsulation platform to support controlled release of bio-vanillin in flavors and fragrances, and in Q1 2026 the company initiated production capacity expansion in Singapore to serve Asia-Pacific markets. Regional adaptation continued in 2024 with the establishment of a Givaudan innovation hub in Dubai to tailor natural flavor solutions for Middle Eastern confectionery and beverage segments.

Supplier consolidation and industrial bio-refinery maturity are defining competitive resilience. Between 2024 and 2026, biotech producer Evolva secured a multi-year supply agreement valued at approximately CHF 35 million for fermentation-derived vanillin, reinforcing stability in long-term offtake contracts. In February 2026, Borregaard reported record EBITDA driven by strong delivery volumes of wood-based bio-vanillin, demonstrating the commercial strength of lignin-derived routes. At the same time, Borregaard recorded impairment on several bio-based start-up investments, signaling a broader industry shift toward proven industrial biorefinery technologies over early-stage ventures.

Trends and Opportunities Transforming the Bio Vanillin Market

Market Trend: Fermentation-Based Biovanillin Becomes the Core Growth Engine

A pivotal transformation in the Bio Vanillin Market is the accelerating shift from petrochemical synthesis toward bioconversion-based vanillin, driven by "Natural Flavor" regulatory designations, ESG scrutiny, and brand transparency requirements. Precision fermentation and enzymatic conversion of ferulic acid sourced from rice bran and corn fiber are now the dominant technology platforms shaping supply chains.

In late 2025, Solvay expanded its Rhovanil® Natural CW range with three new SKUs — Delica, Alta, and Sublima — specifically engineered for improved flowability and dispersion in chocolate and dairy matrices. This type of product tailoring highlights a shift away from commodity flavoring toward performance-differentiated natural vanillin solutions that support consumer-visible claims. More importantly, producers like Spero Renewables are integrating isotopic fingerprinting (δ13C vs δ2H) to verify biological origin and non-GMO sourcing. This authentication technology has become a strategic differentiator, enabling compliance with EC No 1334/2008 and giving premium brands a defensible narrative around traceability and purity.

Market Trend: Premiumization and Asia-Pacific Demand Redefining Market Geography

Confectionery and dairy manufacturers are elevating flavor expectations, making bio-vanillin central to "Clean Label" and ethical sourcing platforms. Mondelēz International, for example, has embedded bio-vanillin adoption into its Vision 2030 sustainability and sourcing roadmap through its Sustainable Futures platform, channeling R&D funds toward fermentation-based aroma systems to eliminate synthetic aromatics.

Asia-Pacific currently leads market consumption, representing over 38% of global bio-vanillin shipments in 2025. The region benefits from its native rice bran supply chain, creating cost and scalability advantages not seen in Western supply chains. Retail data highlights that natural vanilla extract can cost nearly USD 700 per kg while petro-based vanillin is closer to USD 15 per kg, making bio-vanillin a cost-stabilizing middle ground with premium positioning. As Asian manufacturers increasingly export private-label chocolate, bakery, and premium dairy alternatives, the region is expected to remain the epicenter of volume growth and pricing influence.

Market Opportunity: Bio-Vanillin as a Functional Ingredient in Premium Pet Nutrition

One of the fastest-growing non-food opportunities lies within the premium pet food market, where bio-vanillin delivers both sensory and biochemical value. Its antimicrobial, anti-inflammatory, and antioxidant capabilities are being used to extend shelf life and simultaneously enhance perceived nutritional benefits.

A February 2025 Polymer Bulletin study demonstrated that vanillin-reinforced bioactive films provide a 49.44% increase in tensile strength and an 81.33% increase in antioxidant performance. In pet formulations, bio-vanillin is used to mask bitterness associated with nutrient fortification while contributing to gut health through inflammation-modulating pathways documented in 2025 clinical reviews. As pet owners globally shift toward "human-grade" and "functional" treats, bio-vanillin’s dual role as preservative and natural aromatic gives it a commercially defensible value proposition.

Market Opportunity: Sensory Engineering for Plant-Based Proteins and Dairy Alternatives

Bio-vanillin is becoming a sensory-optimization tool for plant-based dairy and meat analogs, helping brands overcome the consumer rejection associated with pea- and soy-derived off-notes. This segment represents one of the strongest long-term growth levers due to category scale. According to The Food Institute (2025), plant-based dairy alone reached USD 22.5 billion in global sales, far outpacing plant-based meat. Developers increasingly rely on bio-vanillin’s creamy aromatic profile to round flavor edges, mask metallic aftertastes, and increase product "stickiness" — a key KPI tied to repeat purchase.

Regulatory developments are acting as catalysts. In July 2025, the U.S. FDA revoked 52 legacy Standards of Identity, granting previously restricted formulations greater flexibility. This policy shift permits blended or novel dairy-alternative structures without labeling penalties, accelerating the adoption of fermentation-derived sensory enhancers. For manufacturers, this expands addressable innovation space, enabling product launches that combine plant fats, precision-fermented proteins, and bio-vanillin flavoring within a single regulatory-compliant label.

Bio Vanillin Market Share and Segmentation Insights

Market Share by Source: Lignin-Based Production Leads While Ferulic Acid and Fermentation Routes Gain Strategic Importance

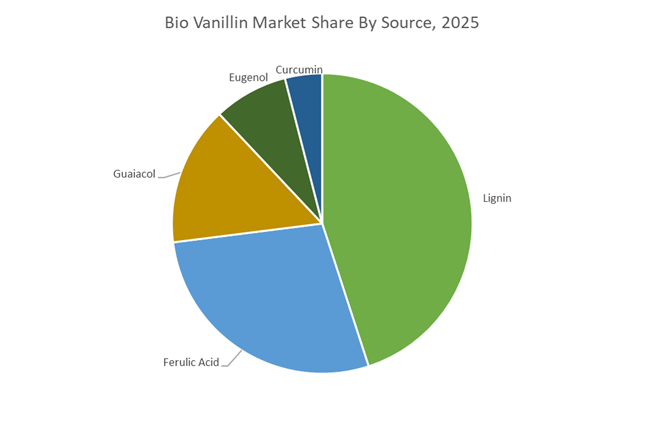

Lignin accounts for the largest share of the Bio Vanillin Market at 45% in 2025, supported by its availability as a kraft pulp by-product and its scalability via alkaline oxidation pathways. Production is concentrated in Scandinavia and North America, where integrated pulp and paper operations enable cost-efficient bio-vanillin supply. Ferulic acid represents the second-largest source, derived from rice bran, wheat bran, and corn kernels, and converted through fermentation or biocatalysis. This route is favored for clean-label and non-GMO positioning, with Japan and Europe leading adoption. Guaiacol-based bio-vanillin is expanding as synthetic biology firms scale precision fermentation, delivering chemically identical but bio-based vanillin. Eugenol from clove oil remains a premium, smaller-volume source constrained by feedstock volatility, while curcumin from turmeric is an emerging niche pathway, with India exploring waste upcycling despite current cost barriers.

Market Share by Application: Food Dominance Anchored by Natural Flavor Demand, Fragrances Drive Premium Growth

Food and beverages command 58% of global bio vanillin consumption in 2025, driven by strong uptake across ice cream, bakery, confectionery, dairy, and beverage formulations as brands transition toward natural flavors and clean-label ingredients. Premium pricing, often reaching 10 to 15 times synthetic vanillin, is increasingly accepted for authentic bio-based positioning. Fragrances and personal care form the second-largest and fastest-growing segment, leveraging bio-vanillin’s warm, creamy aroma in fine fragrances, deodorants, creams, and candles, supported by IFRA compliance and sustainability mandates. Pharmaceutical applications remain stable, using high-purity bio-vanillin as a flavoring agent in syrups and pediatric formulations, closely tied to aging populations and preventive healthcare. Agrochemicals represent a small but emerging outlet, where vanillin derivatives are being evaluated as natural insect attractants and biopesticide synergists, though commercial volumes remain limited.

Competitive Landscape Analysis of the Bio Vanillin Market

The bio vanillin market is evolving rapidly as global food, beverage, fragrance, and personal care brands accelerate their shift from petrochemical vanillin toward fermentation- and biorefinery-derived natural alternatives. Competitive differentiation is centered on feedstock sustainability, flavor fidelity, regulatory compliance under EU and US “Natural Flavor” standards, and supply chain resilience. Market leaders are investing heavily in white biotechnology, side-stream valorization, and regionalized production to reduce land use, carbon intensity, and Scope 3 emissions. In 2026, innovation is increasingly focused on enhanced dispersibility, non-caking powder formats, traceable agricultural inputs, and premium aroma profiles that replicate Bourbon vanilla complexity at industrial scale.

Syensqo dominates fermented bio vanillin with Rhovanil natural platforms

Syensqo, spun off from Solvay, operates the world’s most recognized bio-vanillin portfolio through Rhovanil Natural, setting the global benchmark for fermented vanillin. Its Rhovanil Natural CW, produced via bioconversion of rice-bran-derived ferulic acid, delivers one-to-one flavor replacement for synthetic vanillin while meeting EU and US natural labeling standards. During 2025 and 2026, Syensqo expanded with Delica, Alta, and Sublima grades, improving flowability and dispersion in challenging matrices such as dark chocolate and high-fiber bakery products. Backed by over 130 years of aroma expertise, Syensqo combines industrial-scale consistency with a global supply network. Its 2026 strategy prioritizes increasing renewable carbon content across its entire aroma portfolio.

Ennolys scales yeast-based bio vanillin through fermentation integration

Ennolys, the natural aromatic molecule division of Lesaffre, specializes in fermentation-derived bio vanillin for premium food applications. In 2025, the company commissioned two large fermenters and high-capacity freeze dryers, operating at over 95% efficiency entering 2026. Leveraging Lesaffre’s microbial strain engineering, Ennolys optimizes ferulic acid bioconversion from agricultural side-streams such as corn fiber, achieving lower production costs. Its 2026 development strategy extends beyond single molecules into total aromatic profiles, blending bio-vanillin with complementary bio-compounds to recreate smoky and woody Bourbon vanilla notes. Ennolys emphasizes European sourcing and traceability, targeting ESG-driven manufacturers seeking transparent local supply chains.

Givaudan integrates bio vanillin into premium nature-friendly fragrance systems

Givaudan positions bio vanillin as a cornerstone of its nature-friendly flavor and fragrance palette, targeting high-value consumer experiences. Under its 2030 Strategy announced in late 2025, Givaudan commits 80% of annual revenue to innovation in green chemistry and white biotechnology. In 2026, it scaled Ambrofix technology and FiveCarbon Path methodologies to minimize land use, achieving up to one hundred times lower footprint compared to vanilla bean farming. Givaudan’s bio-vanillin is embedded in fine fragrances and Taste & Wellbeing applications, enabling luxury brands to claim 90%-plus naturality. Its 110 million dollar investment in Mexico strengthens regionalized sustainable aroma production for Latin America.

Borregaard delivers lignin-based bio vanillin with industry-leading carbon metrics

Borregaard operates the world’s most advanced biorefinery, producing bio vanillin from Norwegian spruce lignin rather than agricultural feedstocks. Its EuroVanillin Supreme is the only vanillin supported by a full life cycle assessment, demonstrating approximately 90% lower carbon footprint versus guaiacol-based synthetics. As a co-product of pulp and bioethanol operations, Borregaard’s feedstock is fully insulated from rice bran and corn fiber volatility. In 2026, the company advanced its side-stream valorization model, converting residual lignin into agricultural biostimulants to achieve zero-waste manufacturing. Its high-purity crystalline and powder grades increasingly serve pharmaceutical markets, particularly as masking agents for pediatric oral formulations.

Symrise pioneers fermentative vanillin with backward-integrated aroma supply chains

Symrise remains a technology pioneer in fermentative vanillin, tracing its innovation roots to patents filed in 1995. In early 2026, Symrise launched a share buyback program while redirecting capital toward full side-stream valorization goals aimed at carbon-neutral aroma production sites. The company maintains backward integration across more than ten thousand raw materials, enabling long-term sourcing of ferulic acid and shielding customers from price volatility. Its 2026 bio-vanillin portfolio targets natural aroma applications with high-impact formulations that reduce cost-in-use for confectionery producers. A proprietary crystallization process introduced in late 2025 delivers non-caking powders, improving shelf life and automated bakery handling.

Advanced Biotech supplies FDA-compliant bio vanillin for clean-label North American brands

Advanced Biotech leads the North American natural flavor chemicals segment with ABTVanillin, a fermented ferulic acid-based product certified non-GMO, Kosher, and Halal under US FDA natural flavor regulations. In early 2026, the company expanded its catalog to over eight hundred natural aroma chemicals, with bio vanillin representing its highest-volume category. Advanced Biotech differentiates through regulatory agility, offering bilingual compliance batches suitable for both EU and US markets without reformulation. Operating as a pure-play naturals specialist, its entire business model centers on fermentation and extraction of natural molecules, making it a preferred partner for clean-label startups and premium confectionery brands.

France Bio Vanillin Market: Fermentation Scale, Regulatory Authentication, and Premium Fragrance Pull

France remains the global reference market for high-purity bio vanillin, driven by fermentation-led scale-up, strict authenticity enforcement, and premium demand from flavor and fragrance houses. During late 2024 and throughout 2025, Solvay, following its corporate separation into Syensqo and Solvay legacy assets, finalized biotechnology capacity enhancements at the Cipan manufacturing site through its partnership with Suanfarma. These investments directly support expanded output of Rhovanil® Natural, one of the most widely adopted bio-sourced vanillin grades in food, beverage, and fine fragrance formulations.

Fermentation capability is deepening across the country. In 2025, Ennolys, a subsidiary of Lesaffre, expanded its Southwest France fermentation units using proprietary yeast strains to bioconvert ferulic acid into vanillin that fully complies with EU Natural labeling requirements. Regulatory drivers are reinforcing demand. France’s Anti-Waste for a Circular Economy Law entered a decisive enforcement phase in 2025, pushing perfume and flavor manufacturers to replace synthetic aldehydes with bio-vanillin to improve sustainability scoring. Authenticity protection is also intensifying. The French National Center for Scientific Research published updated 2025 Stable Isotope Ratio Analysis protocols to detect synthetic adulteration, safeguarding the Made in France export premium. Although international in footprint, Mane reinforced France’s leadership by completing Phase II of its Pinghu expansion in December 2025, integrating biotechnologically derived aroma molecules with its Jungle Essence platform.

Norway Bio Vanillin Market: Wood-Based Circularity and Energy-Efficient Biorefining

Norway occupies a structurally differentiated position in the bio vanillin industry through lignin-based production and deep integration with pulp biorefineries. Borregaard reported in Q3 2025 that its BioSolutions segment, which produces EuroVanillin Borregaard, continued to post sustained growth as European customers accelerate de-fossilization of ingredient supply chains. Borregaard remains the world’s only producer of vanillin derived entirely from wood-based lignin, offering a distinct circular alternative to fermentation routes dependent on agricultural feedstocks.

Process efficiency improvements are strengthening competitiveness. In mid-2025, Borregaard completed an upgrade at its Sarpsborg biorefinery, implementing advanced membrane filtration that reduced the energy intensity of lignin fractionation and vanillin extraction by an estimated 18%. Trade dynamics are also favorable. According to Borregaard’s October 2025 investor briefing, ongoing anti-dumping duties on synthetic vanillin originating from China have created a more attractive competitive environment for Norwegian bio-based vanillin in North America, reinforcing export momentum beyond Europe.

China Bio Vanillin Market: Ferulic Acid Scale-Up and Vertical Integration Economics

China’s bio vanillin industry is consolidating around regulatory standardization, rice-bran feedstocks, and vertically integrated fermentation economics. In August 2025, the National Health Commission of China proposed updated safety and labeling standards for vanillin, aligning domestic Natural Equivalent classifications with Codex Alimentarius norms. This alignment is designed to ease export barriers and support Chinese producers targeting multinational food and pharmaceutical customers.

Feedstock leadership is a defining advantage. China has become the global leader in sourcing ferulic acid from rice bran, an abundant agricultural byproduct. During 2025, producers in the Zhejiang cluster expanded bioconversion capacity, targeting 99.9% purity grades suitable for pharmaceutical applications. Cost structures are being optimized through vertical integration. Firms such as Apple Flavor & Fragrance Group invested in closed-loop fermentation sites that generate microbial enzymes onsite, reducing dependence on third-party inputs and lowering unit production costs for bio vanillin.

United States Bio Vanillin Market: Clean-Label Demand, Trade Protection, and Corn-Based Pathways

The United States bio vanillin market is being driven by clean-label food demand, cosmetics regulation, and trade-led supply chain restructuring. In 2024 and 2025, Spero Renewables introduced a high-purity corn-based natural vanillin using a proprietary catalytic process. Crucially, this product qualifies for Natural labeling under FDA 21 CFR 101.22, making it highly attractive to U.S. food brands seeking simplified ingredient declarations.

Regulatory change is reinforcing adoption beyond food. Under the Modernization of Cosmetics Regulation Act enforced through 2025 and 2026, fragrance manufacturers are increasingly favoring bio-vanillin because of its lower impurity profiles and more straightforward safety substantiation. Trade policy has accelerated localization. Following United States Department of Commerce rulings in 2024 and 2025, tariffs on Chinese-origin vanillin rose to punitive levels, prompting near-shoring of bio-vanillin fermentation plants in the U.S. Midwest where corn starch feedstocks are readily available and logistics costs are lower.

India Bio Vanillin Market: Policy-Backed Pilots and Biofuel Integration

India’s bio vanillin industry is at an early but strategically important stage, shaped by national biotechnology policy and integration with biofuel infrastructure. The BioE3 Policy approved in August 2024 elevated high-performance biomanufacturing as a priority, and by 2025 this translated into pilot-scale bio-vanillin projects emerging within the Maharashtra chemical belt. These pilots are focused on fermentation routes that can eventually support food and pharmaceutical grade output for domestic consumption.

Feedstock innovation is emerging through energy sector linkages. Under updates to the National Biofuel Policy in 2025, Indian companies are evaluating recovery of vanillic acid from lignin-rich byproducts generated during second-generation ethanol production. Sites such as the Indian Oil Corporation Limited Panipat refinery are being studied as potential integration points, positioning bio vanillin as a value-added co-product within India’s expanding bio-refining ecosystem.

Country-Level Strategic Snapshot: Bio Vanillin Industry

Bio-Vanillin Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

France

|

Fermentation leadership and authenticity

|

Rhovanil® expansion, yeast-based bioconversion, AGEC enforcement, isotopic verification

|

|

Norway

|

Lignin circularity and energy efficiency

|

Wood-based vanillin scale, membrane filtration upgrades, anti-dumping tailwinds

|

|

China

|

Feedstock scale and cost optimization

|

Rice bran ferulic acid, Codex-aligned standards, closed-loop fermentation

|

|

United States

|

Clean-label demand and near-shoring

|

Corn-based natural vanillin, MoCRA compliance, tariff-driven localization

|

|

India

|

Policy-led pilots and biofuel linkage

|

BioE3-enabled pilots, lignin recovery from 2G ethanol

|

Bio-Vanillin Market Report Scope

Bio Vanillin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$231.7 Million

|

|

Market Size (2034)

|

$411.9 Million

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Source (Lignin, Ferulic Acid, Guaiacol, Eugenol, Curcumin), By Production Technology (Microbial Fermentation, Biocatalytic Conversion, Supercritical Carbon Dioxide Extraction), By Purity and Grade (Food Grade, Pharmaceutical Grade, Fragrance and Cosmetic Grade), By Application (Food and Beverages, Fragrances and Personal Care, Pharmaceuticals, Agrochemicals), By Distribution Channel (Direct Manufacturer Sales, Specialized Chemical Distributors, Custom Formulation Houses)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Syensqo, Borregaard, Mane, Givaudan, International Flavors and Fragrances, Ennolys, Symrise, Takasago International Corporation, DRT, Apple Flavor and Fragrance Group, Wuhan Youji Industries, Axxence Aromatic, Advanced Biotech, Omega Ingredients, Spero Renewables

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bio Vanillin Market Segmentation

By Source

- Lignin

- Ferulic Acid

- Guaiacol

- Eugenol

- Curcumin

By Production Technology

- Microbial Fermentation

- Biocatalytic Conversion

- Supercritical Carbon Dioxide Extraction

By Purity and Grade

- Food Grade

- Pharmaceutical Grade

- Fragrance and Cosmetic Grade

By Application

- Food and Beverages

- Fragrances and Personal Care

- Pharmaceuticals

- Agrochemicals

By Distribution Channel

- Direct Manufacturer Sales

- Specialized Chemical Distributors

- Custom Formulation Houses

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bio Vanillin Industry

- Syensqo

- Borregaard

- Mane

- Givaudan

- International Flavors and Fragrances

- Ennolys

- Symrise

- Takasago International Corporation

- DRT

- Apple Flavor and Fragrance Group

- Wuhan Youji Industries

- Axxence Aromatic

- Advanced Biotech

- Omega Ingredients

- Spero Renewables

*- List not Exhaustive