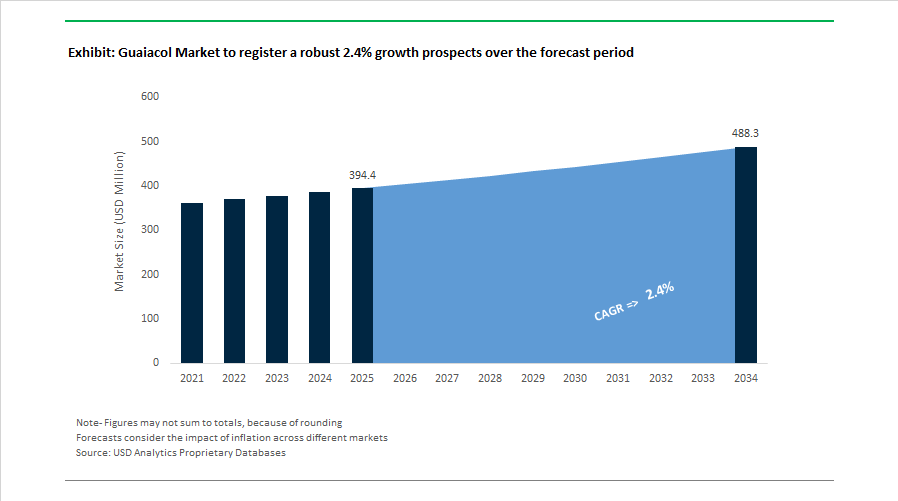

Guaiacol Market to Reach $488.2 Million by 2034 at 2.4% CAGR Amid Bio-Vanillin Shift, Pharma-Grade Demand, and Indian Capacity Expansion

The Guaiacol Market is projected to grow from $394.4 Million in 2025 to $488.2 Million by 2034, registering a CAGR of 2.4%. Growth remains moderate compared to other specialty aromatics due to structural shifts toward lignin-derived bio-vanillin; however, sustained demand from pharmaceuticals, agrochemical intermediates, veterinary formulations, and flavor synthesis continues to underpin volume stability. Market dynamics are increasingly influenced by purity regulations, captive catechol integration strategies, and the repositioning of aroma performance businesses toward higher-value specialty segments.

In mid-2024, India enforced mandatory Bureau of Indian Standards certifications for phenol and its derivatives, directly impacting guaiacol producers by tightening raw material quality and traceability requirements. In late 2024, veterinary industry reports indicated an 18% increase in the use of guaiacol-based compounds for respiratory health treatments in poultry and swine farming across Asia-Pacific. During 2024–2025, pharmaceutical suppliers reported heightened demand for 99.5%+ pharma-grade guaiacol driven by expanded global production of guaifenesin expectorants. In February 2025, Syensqo announced its intention to divest its Aroma Performance business unit, a major global producer of guaiacol-derived vanillin, as part of a broader portfolio shift toward advanced specialty materials. In September 2025, Borregaard ASA opened a new sales office and application laboratory in Mumbai to strengthen its bio-based aromatic intermediates presence in Asia. In December 2025, Clean Science and Technology Limited commenced commercial catechol production through its subsidiary Clean Fino-Chem, enabling captive downstream manufacturing of guaiacol and veratrole under India’s domestic manufacturing initiatives.

Structural realignment accelerated into 2026. In January 2026, Syensqo completed the divestiture of its Oil & Gas business to SNF Group, reallocating capital toward performance and care applications where aroma intermediates remain strategically relevant. The same month, Borregaard received the Household & Commercial Products Association Carbon Footprint Innovation Award for its lignin-based aromatics platform, underscoring the growing market preference for bio-vanillin over petroleum-derived guaiacol routes. In February 2026, financial analysts upgraded Clean Science and Technology following successful ramp-up of its new project blocks, highlighting its catalytic manufacturing efficiency and competitive positioning against traditional Chinese and European suppliers.

Throughout 2025, agrochemical manufacturers expanded the use of guaiacol derivatives in next-generation plant growth regulators and targeted pesticide intermediates designed to align with European Green Deal sustainability targets. Simultaneously, flavor houses intensified investment in lignin-to-vanillin conversion technologies, gradually moderating growth in guaiacol-based vanillin while maintaining its cost-advantaged position for bulk flavor applications.

The Guaiacol Market landscape reflects a balance between mature aroma chemical demand and emerging sustainability pressures. Competitive differentiation increasingly centers on high-purity pharma-grade production, captive catechol integration, compliance with BIS and international phenol standards, cost efficiency versus bio-based alternatives, and diversification into agrochemical and veterinary respiratory health applications across Asia-Pacific and Europe.

Guaiacol Market Trends and Strategic Growth Opportunities

Vertical Integration and Regional Re-Shoring of Guaiacol for Vanillin Supply Security

The guaiacol market is undergoing a structural reconfiguration as flavor and fragrance manufacturers prioritize supply chain resilience amid escalating trade barriers and geopolitical uncertainty. Guaiacol remains a critical precursor for synthetic and nature-identical vanillin, making it strategically important for multinational F&F companies seeking insulation from tariff volatility. This has driven a wave of localized vertical integration, with producers restarting previously mothballed guaiacol-to-vanillin assets to serve protected regional markets.

A pivotal development occurred in September 2025, when Syensqo announced the restart of its synthetic vanillin unit in Saint-Fons, France. The facility, idled in May 2024, is scheduled to return to operation by late 2025 following the European Commission’s imposition of anti-dumping duties of up to 131% on Chinese vanillin imports, coupled with additional U.S. duties exceeding 230%. This regulatory environment has made local production economically compelling despite higher operating costs.

Syensqo’s broader strategy highlights a tri-regional production footprint spanning Baton Rouge in the United States, Saint-Fons in France, and Zhenjiang in China. This configuration allows guaiacol-derived vanillin to be produced within each major trade bloc, reducing tariff exposure while lowering logistics-related emissions. Parallel to synthetic capacity restarts, industry disclosures from 2024 and 2025 show increased investment in biotechnology routes for natural vanillin. In this context, high-purity guaiacol serves as a benchmark molecule for quality control and sensory equivalence, reinforcing its role as a foundational intermediate even as bio-based pathways scale.

Structural Decline in Legacy Agrochemical Demand

While food and fragrance applications are strengthening, traditional agrochemical demand for guaiacol is contracting due to regulatory phase-outs of older pesticide chemistries. Historically, guaiacol was used as an intermediate in certain synthetic pyrethroid and organophosphate formulations. However, global regulatory tightening is accelerating the removal of these products from key agricultural markets.

In India, an updated pesticide ban list released in August 2025 confirmed restrictions on dozens of active ingredients, with enforcement aligned to earlier notifications effective from March 2024. Similar policy signals from the European Chemicals Agency emphasize a transition toward bio-pesticides and integrated pest management frameworks. These shifts are structurally reducing bulk, industrial-grade guaiacol consumption in crop protection.

For producers, this contraction is prompting a portfolio pivot. Market data indicate that pharmaceutical-grade guaiacol now represents roughly 30% of global consumption, driven primarily by demand for expectorants such as guaifenesin and other respiratory therapeutics. As agrochemical volumes decline, margins are increasingly defended through tighter specifications, higher purity grades, and regulated end-use applications in pharmaceuticals and personal care.

Lignin-Derived Guaiacol as a Platform for Bio-Based Polymers

One of the most compelling growth opportunities for the guaiacol market lies in the valorization of lignin, the second most abundant biopolymer globally. Advances in lignin depolymerization are enabling the production of bio-aromatic intermediates, including guaiacol, at industrial scale. This creates a pathway to renewable monomers that can directly displace petroleum-derived aromatics in polymer synthesis.

Research published in 2024 demonstrated the synthesis of multiple bio-based monomers from 4-vinyl guaiacol, positioning these materials as low-carbon substitutes for styrene in radical polymerization. Subsequent studies in 2025 confirmed that guaiacol-derived polybenzoxazine resins can achieve anticorrosion efficiencies approaching 99.99%, opening high-value applications in automotive and aerospace coatings where durability and sustainability are equally critical.

Industrial waste-to-value initiatives are reinforcing this trajectory. Hydrothermal liquefaction processes are being optimized to extract phenolic monomers from pulp and paper black liquor, enabling chemical producers to source guaiacol from renewable biomass rather than benzene-based feedstocks. This alignment with ESG objectives is making lignin-based guaiacol an increasingly attractive option for resin, coating, and composite manufacturers pursuing net-zero material strategies.

REACH-Compliant Rubber Process Oils and Advanced Adhesives

Stringent European REACH regulations governing polycyclic aromatic hydrocarbons in tires have created a significant opening for guaiacol-based solutions in rubber processing. Under Annex XVII, extender oils must meet extremely low thresholds for carcinogenic PAHs, effectively eliminating traditional aromatic oils from tire formulations. This regulatory shift is driving demand for treated distillate aromatic extracts and bio-based alternatives that deliver comparable performance without toxicity concerns.

Guaiacol’s phenolic structure provides inherent antioxidant functionality, making it a promising candidate for non-carcinogenic rubber process aids. Recent materials research has highlighted guaiacol-derived additives as effective stabilizers against thermo-oxidative degradation in rubber compounds and rubber-modified asphalt. These properties align with the tire industry’s sustainability benchmarks set for the mid-2020s.

Beyond tires, guaiacol’s dual functional groups enable its use in high-performance adhesive systems. In flexible electronics and advanced composites, where thermal stability and environmental certification are increasingly decisive purchasing criteria, guaiacol-based intermediates offer a combination of performance and green credentials. This positions the guaiacol market at the intersection of regulatory compliance, renewable chemistry, and advanced materials innovation, supporting diversified growth beyond its traditional flavor and pharmaceutical anchors.

Guaiacol Market Share and Segmentation Insights

Flavor and Fragrance Grade Guaiacol Leads the Market Through Synthetic Vanillin Production

Flavor and Fragrance Grade accounted for 48.60% of the Guaiacol Market share in 2025, establishing it as the most widely utilized grade in global guaiacol consumption. This dominance is closely linked to guaiacol’s critical role as a primary precursor in the synthesis of synthetic vanillin, one of the most widely used flavor compounds in the global food and fragrance industry. Guaiacol-derived vanillin offers significant advantages including consistent quality, scalable production, and cost efficiency compared to natural vanilla extract, making it a preferred raw material for large-scale flavor manufacturing. Flavor and fragrance grade guaiacol must meet strict purity and stability standards to ensure reliable performance in flavor synthesis and fragrance formulation processes. In 2025, the segment is increasingly influenced by the shift toward sustainable flavor ingredient production. Manufacturers are developing guaiacol using bio-based feedstocks derived from lignin streams or fermentation-based aromatic compounds, allowing flavor houses to produce renewably sourced vanillin with natural-identical positioning. Certified renewable guaiacol enables food and beverage companies to support clean label initiatives and sustainability commitments, creating premium pricing opportunities within the global guaiacol market.

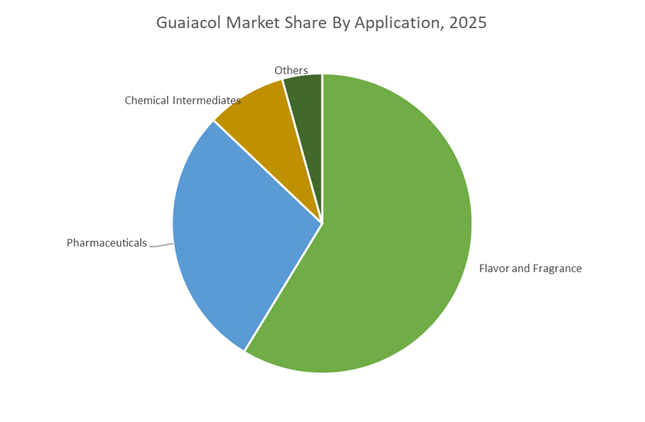

Flavor and Fragrance Applications Drive the Largest Demand for Guaiacol

Flavor and Fragrance represented 58.70% of the Guaiacol Market share in 2025, making it the largest application segment for guaiacol-based chemical intermediates. The compound serves as a foundational raw material in the production of synthetic vanillin and ethyl vanillin, which are extensively used in food flavoring, confectionery products, baked goods, dairy desserts, beverages, perfumes, and cosmetic fragrances. In addition to vanillin synthesis, guaiacol is also used in the production of other aromatic compounds such as guaiacyl acetate and eugenol derivatives, which are incorporated into flavor formulations and fragrance compositions. The scale of global food processing and consumer product manufacturing ensures steady demand for guaiacol-based flavor ingredients. In 2025, the guaiacol market continues to benefit from consistent growth in global vanillin consumption, which is expanding at an estimated 4–5% annual growth rate driven by rising demand for flavored foods and beverages. Increasing emphasis on clean label formulations and natural flavor positioning has further strengthened demand for high-quality guaiacol-based vanillin, particularly as manufacturers shift away from lignin-derived vanillin toward higher purity guaiacol synthesis routes.

Competitive Landscape in Guaiacol Market

Solvay (Syensqo) Anchors the Global Catechol-to-Vanillin Value Chain

Solvay, now operating its guaiacol and vanillin portfolio under Syensqo, maintains annual guaiacol production capacity exceeding 6,000 metric tons, reinforcing its status as the world’s largest integrated vanillin producer. Its fully integrated model spans catechol synthesis through downstream aroma chemicals, ensuring cost control and supply security. In early 2026, the company emphasized its Sustainable Growth roadmap, reporting a 29% reduction in Scope 1 and 2 emissions compared to 2021 levels, directly addressing the energy intensity of guaiacol synthesis. Syensqo prioritizes circular and renewable feedstock innovation as part of its post-corporate-split strategy. The company’s pharmaceutical-grade guaiacol remains critical for global cough and cold formulations and regulated medical supply chains.

Jiaxing Zhonghua Strengthens Captive Integration for Vanillin Dominance

Jiaxing Zhonghua Chemical Co., Ltd. operates as the largest volume producer in Asia and a major captive consumer of guaiacol for its Eternal Pearl vanillin brand. Recognized as the Chinese vanillin production base and ranked among the top 500 Chinese chemical enterprises in 2026, the company supplies guaiacol at purity levels of at least 99.5% by gas chromatography. Most of its guaiacol output is internally consumed for ortho-vanillin and ethyl vanillin production, shielding operations from feedstock price volatility. In early 2026, Zhonghua reinforced anti-counterfeiting and quality tracking measures to protect export markets. Expansion of downstream aroma chemical capacity further consolidates its vertically integrated supply chain position.

Borregaard Leads the Bio-Based Alternative to Petrochemical Guaiacol

Borregaard represents the primary structural alternative to petrochemical guaiacol by producing lignin-derived vanillin through its advanced biorefinery platform. As of 2026, it remains the only large-scale supplier of fully bio-based vanillin that bypasses the petroleum-to-guaiacol pathway. Under its Green Shift strategy, Borregaard continues strengthening traceability and carbon footprint transparency across its supply chain. Integration of its Supplier Development Action program requires logistics and raw material partners to document emissions reduction initiatives. The company secured EcoVadis Gold and Platinum recognition in 2025 and 2026, reinforcing its ESG positioning. Although focused on lignin-based vanillin, Borregaard’s model exerts competitive pressure on synthetic guaiacol producers in sustainability-sensitive markets.

Anhui Jinhe Advances High-Efficiency Guaiacol Synthesis

Anhui Jinhe Industrial Co., Ltd. is emerging as a significant fine chemical supplier with growing emphasis on guaiacol and aroma intermediates. Under its ACE 2.0 growth framework, the company is optimizing synthesis efficiency to reduce wastewater intensity and improve process yields. It markets high-stability industrial-grade guaiacol for agrochemical and dye intermediates while increasing focus on ultra-pure pharmaceutical-grade variants. In early 2026, Jinhe benefited from China+1 procurement strategies adopted by European buyers seeking diversified sourcing. By prioritizing high-margin specialty grades over bulk commodity output, the company navigated China’s 2025 and 2026 capacity rationalization environment effectively.

Layn Natural Ingredients Bridges Botanical and Chemical Innovation

Layn Natural Ingredients operates at the intersection of botanical extraction and specialty chemical intermediates. In February 2026, the company launched a nicotinamide adenine dinucleotide ingredient utilizing enzymatic catalysis, a technology platform that also supports improved extraction of natural guaiacol derivatives. Layn is positioning guaiacol-derived compounds within mitochondrial health and cellular performance segments of the nutraceutical market. Its sustainability credentials include Gold-level SAI Farm Sustainability recognition for monk fruit sourcing, with similar standards applied to botanical precursors. At Natural Products Expo West 2026, Layn showcased clean-label guaiacol-based flavors targeted at functional beverages, reinforcing its strategy of integrating natural extraction expertise with high-purity aroma chemistry.

India: Backward Integration and Policy-Led Pharma Alignment

India has emerged as one of the most structurally advantaged production bases for guaiacol, supported by capital investment, regulatory tightening, and downstream pharmaceutical integration. In 2025–2026, Clean Science and Technology Limited earmarked an additional INR 3 billion in capital expenditure to expand high-value specialty chemical lines, including guaiacol. The company’s backward-integrated manufacturing model is reinforcing cost leadership at a time when global catechol and anisole price volatility is reshaping sourcing strategies. Parallel to this, the government’s BioE3 policy framework has formally classified bio-based chemical building blocks as a priority area, prompting Indian producers to explore lignin-derived feedstocks to structurally reduce import exposure and align with decarbonization objectives.

Regulatory and market-side pull is equally strong. Following the implementation of Revised Schedule M in 2025, Indian manufacturers have upgraded guaiacol distillation and purification units to meet stricter pharma-grade export specifications, particularly for cough syrups, expectorants, and respiratory formulations. Camlin Fine Sciences has expanded vertical integration by using domestically produced guaiacol as a key precursor for vanillin, stabilizing margins amid petrochemical price swings. In parallel, the rapidly expanding Indian CDMO ecosystem is driving localized guaiacol synthesis for complex pharmaceutical intermediates and APIs, reinforced by Production Linked Incentive oversight from the Department of Pharmaceuticals targeting bulk drug self-reliance.

China: Scale Protection, AI Process Control, and Export Realignment

China continues to operate as a high-volume, efficiency-driven hub for guaiacol and its derivatives, with policy measures focused on stabilizing margins rather than aggressive capacity additions. Under the 2025 industrial stabilization directive issued by the Ministry of Industry and Information Technology, high-efficiency guaiacol producers are being shielded from the effects of regional overcapacity, particularly in Shandong and Jiangsu. State-owned enterprises, which control roughly 52% of the chemical raw materials sector, retain preferential access to financing for large-scale guaiacol synthesis projects, reinforcing China’s cost-competitive positioning.

Trade dynamics, however, are reshaping downstream integration. The definitive anti-dumping duty imposed by the European Commission on Chinese vanillin imports in June 2025 has forced guaiacol producers to redirect supply toward domestic food-grade applications and alternative export destinations across Southeast Asia. At the operational level, leading facilities in the Ningbo region have deployed AI-driven catalytic monitoring to optimize catechol methylation, achieving an estimated 12% reduction in energy intensity. This combination of policy insulation and digital manufacturing is enabling Chinese producers to defend profitability despite shifting export pathways.

United States: Regulatory Validation and Feedstock Risk Management

In the United States, guaiacol demand is increasingly shaped by regulatory validation and supply-chain resilience rather than capacity growth. The 2025 FDA Guidance Agenda introduced new recommendations on replacing inactive ingredients and color additives in drug products, directly influencing how guaiacol-derived stabilizers and flavoring components are qualified in pharmaceutical formulations. These changes are pushing manufacturers to document impurity profiles and origin transparency more rigorously, particularly for oral and pediatric medicines.

Further regulatory tightening is expected following the January 2026 draft guidance from the American Association of Blood Banks, which emphasizes non-DEHP materials and non-animal-origin inputs. This has accelerated validation of synthetic guaiacol routes for medical-grade applications. On the supply side, U.S. producers are leveraging more stable domestic catechol availability following Gulf Coast infrastructure upgrades in 2025, reducing exposure to geopolitical disruptions in Middle Eastern petrochemical feedstocks.

Norway: Lignin-Based Specialization and EU Taxonomy Alignment

Norway occupies a distinct premium niche in the global guaiacol industry through biorefinery-based production. Borregaard reported in its Q3 2025 investor update a strategic shift toward full specialization, expanding debottlenecking capacity at its Sarpsborg biorefinery to increase output of lignin-derived guaiacol and vanillin. This wood-based route offers inherent differentiation versus petrochemical synthesis, particularly for food and fragrance customers seeking traceable, renewable intermediates.

Borregaard’s 2025–2026 strategy is tightly aligned with EU Taxonomy criteria and Science Based Targets, positioning its guaiacol as a low-carbon alternative for European buyers. The ramp-up of EuroVanillin Supreme, launched in late 2024 and scaled through 2025, has further increased internal demand for natural guaiacol intermediates, reinforcing Norway’s role as a sustainability benchmark rather than a volume supplier.

France: Cost Optimization and Energy Transition in Specialty Production

France remains a critical European processing center for guaiacol derivatives, driven by operational efficiency and decarbonization initiatives. In 2025, Solvay reported a €40 million EBITDA gain in Q3 alone through optimized CO₂ emission rights management, part of a broader structural cost-reduction program exceeding €190 million since 2024. These efficiency gains directly support competitiveness in guaiacol and vanillin production within its Coatis and Special Chem units.

At the same time, Solvay has confirmed tangible progress on biomass-based energy projects, including the commissioning of a biomass boiler to decarbonize energy-intensive distillation steps required for high-purity guaiacol derivatives. This transition is strengthening France’s positioning as a compliant supplier to EU customers facing tightening Scope 3 and lifecycle emissions scrutiny.

Country-Level Strategic Snapshot: Guaiacol Industry

Guaiacol Market County Level Snapshot

|

Country

|

Core Strategic Theme

|

Structural Industry Impact

|

|

India

|

Backward integration and pharma compliance

|

Cost leadership and CDMO-driven demand

|

|

China

|

Scale protection and AI manufacturing

|

Margin defense amid export realignment

|

|

United States

|

Regulatory validation and feedstock security

|

Stable medical and pharma-grade demand

|

|

Norway

|

Lignin-based biorefinery specialization

|

Premium low-carbon guaiacol positioning

|

|

France

|

Cost optimization and biomass energy

|

EU-compliant, efficiency-led production

|

Guaiacol Market Report Scope

Guaiacol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$394.4 Million

|

|

Market Size (2034)

|

$488.2 Million

|

|

Market Growth Rate

|

2.4%

|

|

Segments

|

By Grade (Pharmaceutical Grade, Industrial Grade, Flavor and Fragrance Grade), By Source (Synthetic, Natural, Biotechnological), By Application (Flavor and Fragrance, Pharmaceuticals, Chemical Intermediates, Other Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Syensqo, Borregaard ASA, Clean Science and Technology Limited, Anhui Bayi Chemical Industry, Camlin Fine Sciences Ltd., Zhonghua Chemical, Liaoning Shixing Pharmaceutical & Chemical, Merck KGaA, Vandana Chemicals, Hubei Ju Sheng Technology, Cayman Chemical, Derek Clarke, Helly Chem, Tianyuan Chemical, Zheng Agrolooks

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Guaiacol Market Segmentation

By Grade

- Pharmaceutical Grade

- Industrial Grade

- Flavor and Fragrance Grade

By Source

- Synthetic

- Natural

- Biotechnological

By Application

- Flavor and Fragrance

- Pharmaceuticals

- Chemical Intermediates

- Other Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Guaiacol Market

- Syensqo

- Borregaard ASA

- Clean Science and Technology Limited

- Anhui Bayi Chemical Industry

- Camlin Fine Sciences Ltd.

- Zhonghua Chemical

- Liaoning Shixing Pharmaceutical & Chemical

- Merck KGaA

- Vandana Chemicals

- Hubei Ju Sheng Technology

- Cayman Chemical

- Derek Clarke

- Helly Chem

- Tianyuan Chemical

- Zheng Agrolooks

*- List not Exhaustive