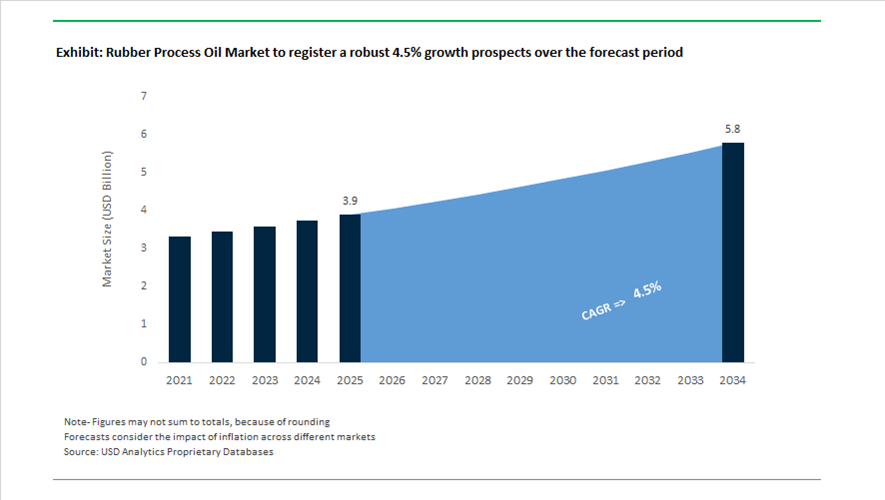

Rubber Process Oil Market Valued at $3.9 Billion in 2025, Projected to Reach $5.8 Billion by 2034 at 4.5% CAGR

The global rubber process oil (RPO) market is valued at $3.9 billion in 2025 and is projected to reach $5.8 billion by 2034, registering a CAGR of 4.5%. Growth is supported by rising demand for naphthenic process oils, paraffinic rubber oils, treated distillate aromatic extracts (TDAE), low-polycyclic aromatic (PCA) oils, bio-based rubber process oils, and high-purity extender oils used in tire manufacturing, industrial rubber goods, conveyor belts, hoses, and footwear compounds. Increasing tire production, EV adoption, and stricter EU REACH regulations limiting high-PCA aromatic oils are accelerating the transition toward sustainable and performance-enhanced formulations.

Sustainability-driven innovation defined early 2024. In February 2024, Nynas launched its first renewable-feedstock rubber process oil, marking a transition toward bio-attributed alternatives designed to deliver comparable solvency and compatibility with elastomers such as SBR and BR while reducing lifecycle carbon intensity. During the same month, Panama Petrochem introduced an eco-certified bio-based RPO derived from castor oil derivatives, targeting export markets in Europe and North America with a reported biodegradability index of 87%. In March 2024, TotalEnergies released a specialized multi-grade RPO with anti-aging additives engineered to extend the service life of industrial rubber equipment by approximately 21%. Capacity expansion also accelerated in early 2024 when Apar Industries increased specialty oil output at its Gujarat facility by 80,000 tons to address record demand from automotive OEMs in India and Southeast Asia.

Integration and scale expansion intensified in 2025. In March 2025, Ergon announced a $400 million expansion at its Vicksburg refinery, enhancing production capabilities for naphthenic and paraffinic specialty process oils. In late 2025, Sinopec reported increased large-scale RPO production volumes supported by its vertically integrated refining infrastructure, meeting rising domestic demand for high-purity rubber precursors in China’s tire sector. Throughout 2025, Aramco strengthened vertical integration across base oil and specialty distribution channels, reinforcing supply reliability for high-durability tire and industrial rubber applications.

Distribution expansion and circular economy initiatives extended into 2026. In January 2026, Ergon formalized a distribution agreement with Japan Sun Oil to market specialty process oils across Japan, strengthening Asia-Pacific penetration. In the same month, Farrel Pomini acquired a majority stake in WF Recycle-Tech to advance pyrolysis technology that converts end-of-life tires into recovered carbon black and oil, promoting a circular rubber process oil ecosystem.

The rubber process oil market is increasingly characterized by bio-based extender oils, low-PCA compliant formulations, naphthenic and paraffinic specialty oil expansion, vertically integrated refining operations, anti-aging additive technology, pyrolysis-derived recycled oil recovery, and distribution consolidation across Asia-Pacific and North America. As tire manufacturers pursue lower rolling resistance, extended durability, and regulatory compliance, advanced RPO formulations remain critical to elastomer performance optimization and sustainable rubber compounding.

Key Trends and Growth Opportunities in the Rubber Process Oil Market

Mandatory Phase-Out of DAE and the REACH Compliance Cliff-Edge

Regulation has become the single most powerful force restructuring the rubber process oil market, with EU REACH Annex XVII acting as a global inflection point rather than a regional constraint. The effective elimination of Distillate Aromatic Extracts due to their high polycyclic aromatic content has accelerated a structural transition toward Treated Distillate Aromatic Extracts and Mild Extracted Solvates. What was once a gradual substitution cycle has turned into a compliance-driven demand shock across tire and automotive rubber value chains.

By October 2024, the EU had tightened restrictions on hazardous substances embedded in rubber articles entering the European Economic Area, directly impacting tires, hoses, belts, and molded automotive components. As manufacturers prepared for the 2025 REACH update, major European tire plants reported that more than 25% of total process oil consumption had shifted exclusively to TDAE and MES grades by late 2025. This was driven not only by regulatory enforcement risk but also by the commercial imperative to eliminate legacy DAE inventories that could render finished products non-compliant at customs checkpoints.

Importantly, this regulatory reset has now become a global manufacturing baseline. Vietnam’s introduction of Extended Producer Responsibility rules in April 2024 mirrored EU chemical safety expectations, forcing exporters to reformulate for compliance. With nearly 90% of Vietnamese tire output destined for international markets, low-PAH oils have become the default specification. As a result, REACH-aligned rubber process oils are no longer a European premium category but a global standard input for export-oriented rubber manufacturing.

Strategic Supply Consolidation Across the Asian Tire Belt

While Europe and North America focus on regulatory transition, the center of volume growth in the rubber process oil market continues to shift toward Asia, particularly India, Vietnam, Thailand, and China. These markets are witnessing rapid consolidation as refiners and specialty oil blenders compete to secure long-term supply agreements for MES and naphthenic oils to support large-scale tire capacity expansions.

By 2024–2025, the Asia-Pacific region accounted for nearly 47% of global rubber process oil consumption, underpinned by sustained automotive production growth. China’s vehicle output crossed 30 million units in late 2023, creating persistent downstream demand for compliant aromatic and naphthenic oils. This has driven strategic offtake agreements in which refiners prioritize domestic tire majors to shield them from feedstock price volatility and supply disruptions.

Southeast Asia has emerged as a critical battleground for future capacity. In December 2025, regional specialty oil suppliers announced expansion projects in Vietnam to support a tire sector producing roughly 30 million units annually, with capacity projected to reach 52 million units by 2033. These investments are increasingly bundled with technical services, including blending optimization and high-speed filling support, reflecting a shift from commodity oil supply toward solution-oriented partnerships aligned with international export standards.

Bio-Based and Circular Rubber Process Oils for Sustainable Tire Compounds

Sustainability commitments from global tire manufacturers are creating a structurally attractive niche for bio-based and circular rubber process oils. Leading brands have publicly committed to raising renewable and recycled material content to 40% or more by 2030, forcing procurement teams to look beyond compliance-grade fossil oils toward low-carbon alternatives derived from vegetable oils, pine tall oil, and tire pyrolysis streams.

By September 2025, major tire producers had increased renewable and recycled material usage to approximately 28–29%, supported by synthetic rubber derived from used cooking oil and circular resins. This transition directly benefits suppliers capable of delivering ISCC PLUS-certified bio-oils that can replace paraffinic and aromatic process oils without compromising wet grip, abrasion resistance, or rolling efficiency. Unlike early bio-oil trials, current formulations are engineered to integrate seamlessly into existing tire compound recipes, reducing reformulation risk.

Capital allocation patterns reflect this shift. Industry data from mid-2025 shows that around 5% of all new rubber process oil blending investments are now targeting renewable feedstocks. Energy majors and specialty chemical producers have moved beyond pilot-scale validation toward commercial bio-RPO production, positioning themselves to serve the emerging green tire segment where lower carbon-intensity scores increasingly influence OEM sourcing decisions.

High-Performance Naphthenic Oils for Non-Tire Engineering Applications

Although tires dominate total volume, non-tire rubber goods represent a stable and margin-resilient opportunity for specialty rubber process oil suppliers. Applications such as automotive seals, industrial hoses, belts, and EPDM-based components place a premium on solvency, low volatility, and compound stability rather than sheer price competitiveness. In this segment, naphthenic oils have emerged as the preferred choice.

By late 2025, non-tire rubber applications accounted for approximately 1.1 million tons of annual global rubber process oil consumption. Naphthenic oils offer superior filler dispersion and polymer compatibility in complex elastomer systems such as EPDM and nitrile rubber, making them indispensable for industrial and infrastructure-related rubber products. In fast-growing markets like Vietnam, the industrial rubber segment alone is valued at roughly 188 million dollars, underlining the scale of opportunity.

Electrification trends are further amplifying demand. Electric vehicles impose higher torque and weight loads, driving an estimated 12–15% annual increase in rubber process oil intake across emerging markets. EV-specific tire and sealing systems require higher oil loading, often around 8% more than conventional formulations, to manage heat build-up and elasticity. This creates a premium opportunity for ultra-low volatility naphthenic oils engineered for thermal stability, positioning specialty suppliers to capture value beyond the highly competitive tire mass-market.

Rubber Process Oil Market Share and Segmentation Insights

Naphthenic Oils Lead Rubber Process Oil Market Due to Superior Compatibility in Rubber Compounding

Naphthenic oils accounted for 42.80% of the rubber process oil market in 2025, making them the most widely used processing oil in rubber manufacturing. Their cycloalkane molecular structure provides excellent solvency, compatibility with rubber polymers, and strong low-temperature flexibility, making them ideal for tire compounding and industrial rubber product manufacturing. These oils improve rubber plasticity, filler dispersion, and processing efficiency, enabling consistent performance during mixing and extrusion processes. A key 2025 industry transition is the increasing replacement of highly aromatic distillate extract oils due to environmental restrictions on polycyclic aromatic hydrocarbons (PAHs). Naphthenic oils, along with treated distillate aromatic extracts (TDAE), have gained market share as safer alternatives that maintain processing performance while complying with global environmental regulations.

Tire Manufacturing Drives Global Demand for Rubber Process Oils

Tire manufacturing represents the largest application segment in the rubber process oil market, accounting for 48.60% of total consumption in 2025 due to the massive scale of global tire production. Process oils function as extenders, plasticizers, and processing aids in tire tread compounds, sidewalls, and inner liners, improving compound flexibility and manufacturability. With the global tire industry producing more than two billion tires annually, rubber process oils remain essential to maintaining efficient large-scale tire manufacturing operations. A major 2025 industry milestone is the near completion of the low-PAH tire oil transition, where manufacturers have shifted from traditional aromatic oils toward TDAE, MES, and naphthenic oils that meet stringent environmental standards while preserving tire durability, wet traction performance, and rolling resistance characteristics.

Rubber Process Oil Market Competitive Landscape

The 2026 rubber process oil market is shaped by low-PCA formulations, TDAE and naphthenic oils, and refinery-integrated production. Growth is driven by EV tire requirements, regulatory compliance under REACH and TSCA, and rising demand for high-performance, eco-friendly extender oils.

Nynas strengthens naphthenic rubber oil leadership with sustainability excellence and advanced tire wear research

Nynas AB is reinforcing its leadership in naphthenic rubber process oils through strong financial performance and sustainability differentiation. Q4 2025 earnings growth was driven by its Naphthenic Specialty Products segment, supported by a $380 million bond issuance for infrastructure upgrades. EcoVadis Platinum recognition places the company in the top 1% globally for ESG performance. Collaboration with KTH focuses on reducing tire wear particle emissions, influencing next-generation low-PCA oil formulations. Operational upgrades at its Nynäshamn facility improve energy efficiency through shore power integration. Focus on high-purity naphthenic oils supports premium tire and industrial rubber applications.

ExxonMobil advances high-purity paraffinic and naphthenic RPOs with integrated refining and EV tire focus

ExxonMobil Corporation is leveraging its global refining scale and hydroprocessing expertise to deliver high-stability rubber process oils. Its portfolio emphasizes low-volatility paraffinic oils that prevent migration and blooming in rubber compounds. 2026 strategy targets compliance with PAH regulations while optimizing formulations for SBR and PBR used in EV tires. Integration with Group I and II base oil production ensures cost-efficient supply across major markets. Participation in tire pyrolysis initiatives supports circular recovery of process oils. Focus on durability and consistency aligns with high-performance automotive and industrial rubber requirements.

HF Sinclair expands specialty rubber oil footprint through acquisitions and branded distribution strategy

HF Sinclair Corporation is strengthening its position in the rubber process oil market through strategic acquisitions and refining integration. Acquisition of Industrial Oils Unlimited expands blending and distribution capabilities in the U.S. Midwest. Strong 2025 financial performance is supported by its diversified refining network and specialty lubricants segment. Product portfolio includes high-saturation paraffinic oils with strong UV stability for wire, cable, and footwear applications. A 2026 joint venture focuses on expanding branded lubricant sales directly to manufacturers. Emphasis on specialty oils enhances margins in a competitive refining environment.

PetroChina drives large-scale RPO production with integrated refining and green tire application focus

PetroChina Company Limited dominates the Asian rubber process oil market through large-scale integrated refining operations. Approval of a $9.56 billion refinery complex in Dalian will significantly increase output of high-purity process oils and petrochemical intermediates. Strong cash flow of RMB 227 billion supports transition toward high-value chemical production. Integrated complexes supply a major share of regional demand for rubber additives. Focus on naphthenic oils supports solution-polymerized rubber used in low-PAH EV tire treads. Strategic alignment with China’s green tire standards strengthens its global export competitiveness.

ENEOS accelerates bio-based rubber oil innovation with circular feedstocks and AI-driven R&D integration

ENEOS Corporation is advancing sustainable rubber process oils through bio-based feedstocks and digital R&D transformation. Integration of bio-naphtha enables development of renewable-origin plasticizers for high-performance rubber applications. Dual leadership structure enhances collaboration between research and commercialization teams. Participation in CES 2026 highlights its focus on EV fluids and advanced lubricants. Chemical recycling facility developed with Mitsubishi Chemical supports circular feedstock generation for process oils. Pursuit of ISCC PLUS certification strengthens its position in sustainable materials markets.

Chevron sets benchmark for high-purity paraffinic RPOs with hydroprocessing technology and global base oil integration

Chevron Corporation is leading the rubber process oil market with advanced hydroprocessing and high-purity paraffinic formulations. ParaLux® oils offer low aromatic content, superior color stability, and UV resistance for EPDM and specialty rubber applications. Capital allocation of up to $19 billion in 2026 includes investments in low-carbon and downstream specialty businesses. Extensive Group II and III base oil production ensures consistent global supply for industrial applications. Focus on cost optimization enhances competitiveness in volatile crude markets. Expansion into biofuels and renewable energy supports long-term sustainability in process oil production.

United States: Regulatory Transparency and EV-Driven Reformulation

The United States rubber process oil industry is undergoing a structural transition driven by regulatory disclosure, electrification of mobility, and low-emission formulation requirements. Under the 2024–2025 Toxic Substances Control Act Chemical Data Reporting rule, more than 20 domestic producers are now required to disclose precise rubber process oil volumes and compositional data. This has materially increased market transparency and accelerated the shift toward low-VOC rubber process oils, particularly paraffinic grades that comply with tightening occupational and environmental standards. Parallel to this regulatory pressure, the U.S. Department of Energy reported a 60% year-on-year increase in electric vehicle sales by late 2024, fundamentally altering tire performance specifications. EV platforms impose higher torque and weight loads, directly increasing demand for high-purity paraffinic rubber process oils that improve heat resistance, aging stability, and rolling efficiency in advanced tire compounds.

Sustainability-linked refining is reinforcing this transition. In 2025, multiple U.S. refiners leveraged USDA bio-refining incentives to scale bio-based paraffinic process oil production, with the objective of substituting 10–12% of petroleum-derived rubber process oils by 2030. At the corporate level, HF Sinclair highlighted in its Q2 2025 disclosures that its Lubricants & Specialties segment remains strategically central, emphasizing higher-margin specialty rubber process oils even amid refinery turnaround cycles. Technological decarbonization is also progressing, as methane pyrolysis integration following the 2025 investment cycle is enabling refiners to reduce the carbon intensity of process oil manufacturing by nearly 30%. Concurrently, 2025 PFAS-free material guidelines have pushed U.S. producers to develop rubber process oils that act as compliant carrier fluids for non-fluorinated additives used in medical tubing, seals, and automotive gasket applications.

India: Export-Oriented Scale-Up and Green Tire Alignment

India’s rubber process oil landscape is increasingly export-driven, supported by capacity expansion, automotive growth, and infrastructure-led consumption. In October 2025, APAR Industries announced the operation of more than 65 advanced manufacturing facilities globally, with both domestic plants and its Sharjah unit focused on high-purity rubber process oils for automotive and transmission and distribution applications. India has now emerged as a top-10 global lubricants producer, with APAR reporting that exports contributed 32.8% of FY2025 revenue, underpinned by strong demand from the GCC and North American markets for transformer oils and rubber process oils.

Domestic demand fundamentals remain robust. As India’s automotive sector prepares for accelerated growth in 2026, local producers such as Panama Petrochem are scaling TDAE and residual aromatic extract production to meet green tire specifications mandated by OEMs and global tire brands. Infrastructure spending is reinforcing this trajectory. The ₹2,056 crore sanctioned for regional projects in late 2024 has directly increased consumption of rubber-intensive products including conveyor belts, hoses, vibration dampers, and industrial flooring, all of which rely on rubber process oils for flexibility, abrasion resistance, and processability. This combination of export pull and domestic infrastructure demand is positioning India as a structurally important rubber process oil supplier rather than a purely price-driven market.

China: Low-PAH Compliance and Smart Refining Integration

China continues to dominate global rubber manufacturing, with rubber process oil demand closely tied to synthetic rubber output and export compliance requirements. At the September 2025 RubberTech China exhibition, H&R Group’s Ningbo operations showcased new environmental-grade rubber process oils with low polycyclic aromatic hydrocarbon content, specifically formulated to satisfy stringent European tire export regulations. These developments reflect a broader industry shift away from traditional high-PAH aromatic oils toward compliant naphthenic and treated aromatic alternatives.

Supply-side dynamics are reinforcing this shift. PetroChina reported a 10.1% year-on-year increase in synthetic rubber production in Q3 2025, necessitating proportional growth in high-solvency rubber process oil supply to support compounding and extrusion efficiency. At the refinery level, large-scale facilities in the Zhejiang cluster have implemented AI-driven dosing and blending systems by early 2026, reducing raw material waste by an estimated 15% while improving batch consistency. This integration of smart manufacturing is strengthening China’s ability to deliver specification-driven rubber process oils at scale, particularly for export-oriented tire and industrial rubber applications.

Sweden and European Union: Sustainability Benchmarks and Scope 3 Transparency

The European rubber process oil market is increasingly defined by sustainability certification, lifecycle transparency, and bio-based innovation. In October 2025, Nynas AB achieved the EcoVadis Platinum rating, placing it within the top 1% of organizations globally for environmental and social performance. This distinction has become a critical qualification criterion for suppliers serving European tire manufacturers, particularly those marketing low-carbon or green tire portfolios.

Technological innovation is reinforcing this positioning. In November 2025, Nynas successfully delivered its NYTRO® BIO 300X fluids, initially developed for transformer applications but increasingly adapted for rubber processing use cases where bio-based content and low toxicity are prioritized. At the same time, European producers have introduced carbon footprint calculators across their rubber process oil portfolios, enabling tire manufacturers to precisely quantify Scope 3 emissions and comply with tightening EU disclosure requirements. This transparency is reshaping procurement decisions, favoring suppliers capable of delivering both performance consistency and verified emissions data.

Spain: Circular Oils and Refining Decarbonization

Spain plays a growing role in the European rubber process oil ecosystem through circular economy integration and refining decarbonization. Repsol has committed to a 55% reduction in Scope 1 and Scope 2 emissions by 2025 compared with 2016 levels, embedding renewable base oils and circular feedstocks into its Master Line of process lubricants. This strategy aligns closely with the needs of industrial rubber manufacturers seeking low-carbon rubber process oils without compromising solvency or compatibility.

In 2025, Repsol began incorporating treated used oils into the production of high-quality rubber process oils, effectively closing the material loop for Mediterranean rubber processors. This circular oil integration is reducing dependency on virgin feedstocks while maintaining compliance with European chemical and performance standards, positioning Spain as a key hub for circular rubber process oil supply in Southern Europe.

Rubber Process Oil Industry: Country-Level Strategic Summary

Rubber Process Oil Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Structural Impact on Rubber Process Oil Market

|

|

United States

|

TSCA transparency, EV tire demand, bio-refining

|

Shift toward low-VOC, paraffinic and PFAS-free specialty RPOs

|

|

India

|

Export-led scale-up, green tire alignment

|

Emergence as a high-growth global supplier of TDAE and RAE oils

|

|

China

|

Low-PAH compliance, smart refining

|

Specification-driven RPO production for export-oriented rubber

|

|

Sweden / EU

|

Sustainability certification, Scope 3 disclosure

|

Preference for bio-based, traceable rubber process oils

|

|

Spain

|

Circular oil integration, decarbonization

|

Closed-loop RPO supply for European industrial rubber users

|

Rubber Process Oil Market Report Scope

Rubber Process Oil Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$5.8 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Type (Aromatic Oils, Paraffinic Oils, Naphthenic Oils, Bio-Based & Renewable Oils), By Application (Tire Manufacturing, Industrial Rubber Goods, Automotive Components, Polymer Extension, Adhesives & Sealants, Footwear & Consumer Goods), By Viscosity Grade (Low Viscosity, Medium Viscosity, High Viscosity)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nynas AB, H R Group, Sinopec Group, PetroChina Company Limited, Exxon Mobil Corporation, Shell plc, Apar Industries Ltd., Repsol SA, TotalEnergies SE, HF Sinclair Corporation, Chevron Corporation, ORGKHIM, Panama Petrochem Ltd., Eni SpA, Cross Oil Refining & Marketing Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rubber Process Oil Market Segmentation

By Type

- Aromatic Oils

- Paraffinic Oils

- Naphthenic Oils

- Bio-Based & Renewable Oils

By Application

- Tire Manufacturing

- Industrial Rubber Goods

- Automotive Components

- Polymer Extension

- Adhesives & Sealants

- Footwear & Consumer Goods

By Viscosity Grade

- Low Viscosity

- Medium Viscosity

- High Viscosity

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Rubber Process Oil Industry

- Nynas AB

- H R Group

- Sinopec Group

- PetroChina Company Limited

- Exxon Mobil Corporation

- Shell plc

- Apar Industries Ltd.

- Repsol SA

- TotalEnergies SE

- HF Sinclair Corporation

- Chevron Corporation

- ORGKHIM

- Panama Petrochem Ltd.

- Eni SpA

- Cross Oil Refining & Marketing Inc.

*- List not Exhaustive