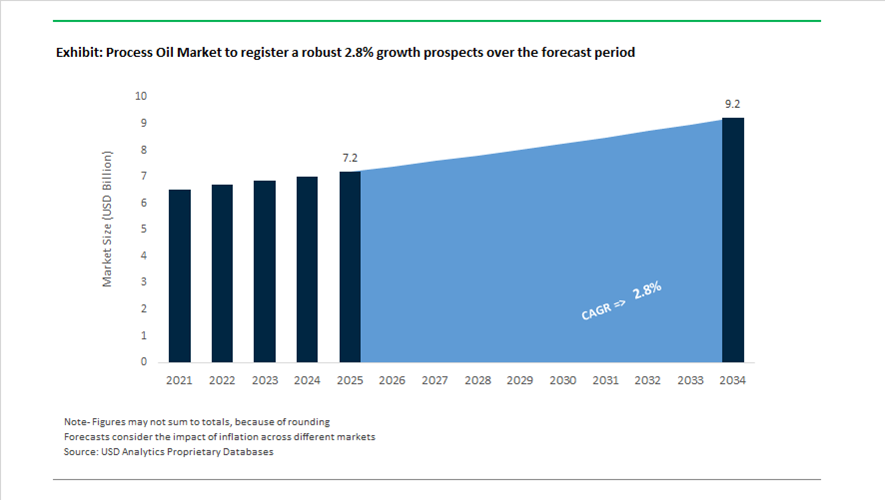

Process Oil Market Valued at $7.2 Billion in 2025, Projected to Reach $9.2 Billion by 2034 at 2.8% CAGR

The global process oil market is valued at $7.2 billion in 2025 and is forecast to reach $9.2 billion by 2034, expanding at a CAGR of 2.8%. Growth remains moderate but structurally resilient, driven by steady demand for naphthenic process oils, paraffinic oils, transformer oils, rubber process oils, white oils, and specialty industrial fluids across tire manufacturing, power transmission, automotive lubricants, and renewable energy infrastructure. Sustainability mandates, circular base oil integration, and electrification of transport are reshaping product portfolios toward re-refined base oils (RRBO), bio-based transformer fluids, and low-aromatic specialty oils.

Circular economy investments gained traction in 2024. In June 2024, TotalEnergies introduced its Quartz EV3R and Rubia EV3R lubricant ranges formulated with high-quality recycled base oils, targeting automotive sustainability standards. In July 2024, TotalEnergies acquired Finnish re-refining specialist Tecoil, strengthening its capability to produce RRBOs and integrate circular feedstocks into specialty process oils. During the same month, Petronas, Enilive, and Euglena reached a final investment decision for a Johor, Malaysia biorefinery scheduled for 2026 startup. The facility will produce bionaphtha and sustainable fluids, expanding bio-derived inputs into downstream process oil and transformer oil portfolios.

Strategic expansion accelerated in 2025. In July 2025, Shell Lubricants finalized its acquisition of Raj Petro Specialities from Brenntag Group, reinforcing Shell’s presence in India’s specialty process oil and transformer oil segments. In August 2025, Shell India upgraded its premium motor oil range to comply with the 2025 API SQ standard, reflecting continuous evolution in additive chemistry and base oil refinement. In October 2025, Nynas received EcoVadis Platinum status, ranking among the top 1% of sustainable companies globally and reinforcing its positioning in low-carbon naphthenic oil production. In November 2025, Nynas recorded the first commercial use of its bio-based transformer fluid, NYTRO® BIO 300X, within Croatia’s power grid, demonstrating practical deployment of renewable process oil alternatives. In December 2025, Ergon was recognized by Pirelli with its 2025 Quality Award for supplying high-performance rubber process oils critical to advanced tire manufacturing.

Portfolio diversification and geographic expansion intensified into 2026. In January 2026, HF Sinclair completed the acquisition of Industrial Oils Unlimited, expanding its regional manufacturing footprint and specialty process oil capabilities in North America. In the same month, Ergon formalized a distribution agreement with Japan Sun Oil to supply HyVolt and OmniVolt naphthenic transformer oils across Japan, targeting Asia-Pacific power transmission markets. Also in January 2026, Nynas delivered nearly 700 metric tonnes of NYTRO® Lyra X transformer oil for Poland’s largest offshore wind project, underscoring the role of high-performance naphthenic oils in renewable grid expansion.

The process oil market is increasingly defined by re-refined base oil integration, bio-based transformer fluids, naphthenic oils for offshore wind projects, rubber process oils for high-performance tires, sustainable lubricant upgrades meeting API SQ standards, and Asia-Pacific distribution alliances. While overall growth remains moderate, sustainability-driven reformulation, renewable energy infrastructure build-out, and supply chain localization continue to shape competitive positioning across global specialty oil producers.

Strategic Trends and High-Impact Opportunities in the Process Oil Market

Mandatory Transition to Non-Carcinogenic and Low-PAH Extender Oils

The process oil market has reached a regulatory inflection point, with compliance now acting as the primary demand driver rather than cost optimization. As of April 2025, the tightening of EU REACH Annex XVII under Regulation (EU) 2025/660 has effectively closed global primary supply chains to traditional Distillate Aromatic Extract (DAE) oils. These rules impose strict toxicological thresholds, requiring Benzo[a]pyrene (BaP) content below 1 mg/kg and a combined limit of 10 mg/kg across eight regulated PAHs. As a result, process oil producers are compelled to deliver extender oils that meet both regulatory and OEM audit requirements across Europe, North America, and increasingly Asia.

To maintain market access, refiners have accelerated investments in mild extraction, severe hydrotreatment, and hydrogenation technologies. Treated Distillate Aromatic Extract (TDAE) and Mild Extracted Solvate (MES) oils have become the new industry baseline, with consistent IP 346 DMSO extract values below 3%, ensuring non-carcinogenic classification. Leading suppliers have reconfigured refinery cut selection and solvent systems to deliver tighter batch-to-batch consistency, which is critical for automated tire mixing lines operating at industrial scale.

The shift is further reinforced by downstream branding and labeling dynamics. In 2025, enforcement of updated testing protocols such as ISO 21461 at EU borders significantly increased scrutiny on imported rubber goods. This has driven a surge in demand for naphthenic process oils, which offer inherently low PAH profiles alongside superior low-temperature flexibility. For winter and all-season tire formulations, these oils are increasingly preferred not only for compliance, but also for performance differentiation under “green tire” sustainability labeling frameworks.

Strategic Supply Chain Realignment Across the Indo-Pacific Tire Corridor

As global tire manufacturing capacity consolidates in India and Southeast Asia, the process oil market is undergoing a geographic and contractual reset. India, in particular, is transitioning from an import-dependent extender oil market toward localized, long-term supply models aligned with domestic automotive and infrastructure growth. According to the September 2025 ATMA–PwC outlook, the Indian tire industry is positioned for up to 12-fold revenue growth by 2047, creating sustained upstream demand for compliant, high-purity process oils.

This expansion is already reshaping investment behavior. Large-scale commitments in tire reinforcement, cord, and compounding capacity are triggering parallel demand for locally produced TDAE, MES, and naphthenic oils within Special Economic Zones to reduce logistics risk and foreign exchange exposure. Process oil suppliers are increasingly entering multi-year offtake agreements tied to quality metrics such as viscosity stability, volatility loss, and compatibility with high-speed Banbury and intermix systems.

Quality and reliability are now explicit differentiators. In late 2025, supplier recognition programs by global tire OEMs underscored a clear shift away from transactional sourcing toward strategic partnerships. Awards tied to rheological consistency and process predictability reflect the reality that modern tire gigafactories cannot tolerate formulation drift, reinforcing the premium placed on process oil suppliers that can guarantee uniformity at scale.

Commercialization of Bio-Based and Pyrolysis-Derived Circular Process Oils

The most attractive growth opportunity in the process oil market lies in bio-circular and recycled feedstock integration. Tire manufacturers have moved decisively beyond pilot trials, embedding bio-based and pyrolysis-derived oils into commercial production through mass-balance certification frameworks. These materials are no longer niche sustainability add-ons but core inputs aligned with Scope 3 emissions reduction targets.

By September 2025, leading tire producers reported that nearly 30% of their material inputs were derived from sustainable sources, including bio-based process oils and resins. Used cooking oil, vegetable oil derivatives, and waste-based hydrocarbons are being refined into extender oils that meet both performance and compliance requirements, with stated targets rising toward 40% sustainable content by 2030. This transition is supported by the maturation of tire pyrolysis oil (TPO) infrastructure. Large-scale projects commissioned in 2024–2025 have demonstrated that refined TPO can deliver a carbon footprint reduction of approximately 30% versus virgin mineral oils, while maintaining compatibility with existing rubber formulations.

From a market perspective, this is creating a premium tier within process oils, where sustainability credentials, traceability, and life-cycle carbon data directly influence supplier selection. As regulatory pressure converges with OEM decarbonization strategies, bio-circular oils are positioned to command structurally higher margins than conventional extender oils.

Specialty Fluids for High-Performance Adhesives and Polymer Modification

Beyond tire compounding, a structurally attractive opportunity is emerging in specialty process oils for non-black rubber, adhesives, sealants, and advanced polymer modification. These applications impose far stricter requirements on color stability, odor, UV resistance, and volatility than traditional tire formulations, effectively excluding aromatic oils from consideration.

In EPDM and thermoplastic elastomer systems, high-viscosity-index, hydrogenated process oils are becoming essential to control oil migration, long-term elasticity, and surface appearance. Automotive weatherstripping, roofing membranes, and cable insulation increasingly rely on these specialty oils to meet extended durability and emissions standards. R&D milestones highlighted in 2025 confirm that process oil selection is now a primary determinant of long-term performance rather than a secondary formulation variable.

A similar shift is evident in adhesives and sealants, particularly for electronics, medical devices, and construction. High-mix, low-volume manufacturing environments demand zero-odor, high-clarity oils that do not yellow, bleed, or degrade tack over time. Hydrogenated and ultra-low aromatic grades are therefore gaining share as premium formulation aids, offering a defensible growth avenue for refiners capable of delivering consistent, application-specific products.

Process Oil Market Share and Segmentation Insights

Naphthenic Process Oils Lead Rubber Compounding and Industrial Processing Applications

Naphthenic oils accounted for 38.60% of the Process Oil Market by type in 2025, reflecting their strong compatibility with elastomers and superior solvency characteristics required in rubber compounding processes. Their cycloalkane molecular structure provides excellent low temperature performance, processing efficiency, and plasticizing properties for tire and industrial rubber manufacturing. Naphthenic process oils are widely used in rubber processing, polymer compounding, and specialty industrial formulations due to their balanced viscosity and solvency profile. In 2025, regulatory restrictions on highly aromatic oils have accelerated the transition toward safer alternatives, with naphthenic oils and treated distillate aromatic extracts increasingly replacing traditional DAE oils while maintaining performance requirements in tire manufacturing and rubber processing industries.

Tire and Rubber Industry Drives Global Demand for Process Oils in Elastomer Compounding

Tire and rubber applications represented 48.60% of the Process Oil Market by application in 2025, reflecting the extensive use of process oils as plasticizers, extenders, and processing aids in rubber compounding formulations. Passenger vehicle tires, commercial truck tires, and industrial rubber products require process oils to improve polymer flexibility, mixing efficiency, and compound processing characteristics. The global scale of tire production and replacement tire demand continues to support high consumption of rubber process oils. In 2025, global regulatory requirements limiting polycyclic aromatic hydrocarbons in tire oils have influenced formulation strategies, encouraging tire manufacturers to adopt low PAH process oils such as TDAE, MES, and naphthenic oils that meet environmental regulations while preserving tire durability and performance.

Process Oil Market Competitive Landscape

The global process oil market in 2026 is shifting toward low-PCA naphthenic oils, Group II/III base stocks, and bio-circular process oils to meet ESPR compliance and Scope 3 targets. Key players are leveraging integrated refining, mass balance carbon tracking, and specialty formulations for tire and polymer applications.

Nynas Expands Sustainable Naphthenic Portfolio with EVO Line and Strong NSP Growth

Nynas continues to strengthen its specialty chemicals positioning through its Naphthenic Specialty Products (NSP) segment and NYNAS® EVO sustainable product line. The company reported strong Q4 2025 earnings with a 4% year-over-year increase in NSP volumes, driven by demand in non-European emerging markets. In October 2025, Nynas achieved EcoVadis Platinum status, ranking in the top 1% globally for sustainability performance. Its entry into the United Nations Global Compact in 2025 reinforces its commitment to responsible supply chains and ESG compliance. The NYNAS® EVO line is positioned as a drop-in solution enabling rubber and lubricant manufacturers to reduce carbon footprint without reformulation. In June 2025, Nynas issued a $380 million senior secured bond to strengthen liquidity and support its electrification-focused long-term strategy.

Shell Strengthens Global Leadership Through Acquisition and Portfolio Optimization in Process Oils

Shell maintains its position as the world’s leading lubricants supplier for the 19th consecutive year, integrating circular process oils into its global portfolio. In July 2025, Shell completed the acquisition of Raj Petro Specialities, expanding its presence in the Indian process oil and transformer oil market. The company launched upgraded lubricant and process additive solutions in August 2025 to meet the API SQ Standard, reinforcing compliance leadership. In March 2026, Shell announced the divestiture of Jiffy Lube International to streamline operations and focus on high-value chemical and energy segments. Its 2025 Annual Report highlights the “Powering Progress” strategy, emphasizing integration of technical capabilities into value-generating business lines. This strategic alignment strengthens Shell’s role in specialty process fluids and sustainable oil solutions.

ExxonMobil Advances Group II/III Base Oil Strategy Through Major Refining Reconfiguration

ExxonMobil is executing a large-scale transformation of its refining portfolio to prioritize high-value Group II/III base stocks and specialty process oils. The Baytown multi-billion dollar project announced in September 2025 will shift production away from fuels toward premium base oils, with startup planned for 2028. The company reported $7.4 billion in Energy Products earnings in 2025, reflecting a $3.4 billion increase driven by refinery throughput and cost efficiencies. Its Singapore Resid Upgrade project enhances conversion of low-value fuels into high-value distillates and process oils. ExxonMobil remains the only supplier offering the full Group I–V base stock range, strengthening its competitive positioning. Its methane reduction targets and broader 2030 GHG roadmap align with sustainability-driven process oil demand.

HF Sinclair Expands Specialty Process Oil Capabilities Through Strategic Acquisition and Integration

HF Sinclair is strengthening its Lubricants & Specialties segment through targeted acquisitions and integrated marketing strategies. The acquisition of Industrial Oils Unlimited in January 2026 expands its regional manufacturing capabilities in industrial lubricants and process fluids. The company reported stable 2025 financial performance, highlighting resilience in its Specialties segment and consistent cash dividend distribution. Its branded marketing joint venture launched in early 2026 aims to deepen integration between refining operations and end-user industrial markets. HF Sinclair is prioritizing service reliability as it integrates acquired assets into its portfolio. This strategy positions the company as a comprehensive supplier of customized process oil formulations in North America.

PetroChina Accelerates Refining-to-Chemicals Transition with Large-Scale Petrochemical Hubs

PetroChina is advancing its refining-to-chemicals strategy by replacing legacy refineries with integrated petrochemical hubs focused on specialty oils and ethylene production. The $9.56 billion Dalian project approved in January 2026 includes a 200,000 bpd refinery and a 1.4 million ton ethylene unit. The company reported strong operating performance in 2025, supported by innovation and reduced reliance on diesel markets. The Guangdong Petrochemical Complex became fully operational in 2025–2026, boosting supply of high-purity process oils in South China. PetroChina’s upstream drilling expansion in the Jabung Working Area ensures feedstock security for downstream operations. This vertically integrated model strengthens its leadership in Asia’s specialty oil market.

Ergon Strengthens Naphthenic Oil Leadership Through Supply Chain Agility and Strategic Partnerships

Ergon maintains its global leadership in naphthenic specialty oils through agile supply chain management and targeted regional partnerships. In January 2026, the company partnered with Japan Sun Oil to expand distribution of transformer and process oils in North Asia. Its 2025 Doing Right Report highlights progress in sustainability and environmental impact reduction across operations. Ergon demonstrated strong market responsiveness by issuing a supply chain advisory in March 2026 to address Middle East disruptions. The company also announced a significant naphthenic oil price increase in North America due to tightening crude supply and rising refining costs. This combination of pricing leadership and operational agility reinforces Ergon’s position in high-specification process oil markets.

United States: Product Solutions Strategy and Regulatory-Driven Purification

The United States process oil industry is being reshaped by strategic refinery integration, emissions regulation, and grid-focused innovation. In December 2025, ExxonMobil finalized its 2030 strategic roadmap, positioning high-value process oils as a core Product Solutions priority. By leveraging upstream Permian Basin feedstocks into domestic refining systems, ExxonMobil is strengthening the supply of ultra-pure paraffinic process oils required for medical-grade plastics and sensitive polymer processing. Regulatory pressure is reinforcing this transition. Revised Clean Air Act guidelines for 2025–2026 are pushing U.S. rubber manufacturers to adopt low-volatility process oils to curb VOC emissions during vulcanization, particularly across Midwest automotive clusters.

Infrastructure and performance standards are adding further momentum. In August 2025, Ergon expanded its Vicksburg Pilot Plant, a dedicated R&D hub for next-generation naphthenic dielectric and insulating oils aligned with U.S. grid modernization efforts. Sustainability benchmarks are tightening across the sector, with Ergon achieving a 25% intensity-based emissions reduction by mid-2025, underscoring the shift toward green specialty oils. On the downstream side, U.S. formulators were among the earliest adopters of the 2025 API SQ Standard in early 2026, utilizing high-viscosity-index process oils to improve fuel economy and engine durability in turbocharged gasoline direct injection platforms.

India: Refining Expansion, Petrochemical Deepening, and Bio-Blended Transition

India’s process oil market is expanding rapidly through refinery scale-up, petrochemical integration, and sustainability-led blending initiatives. In September 2025, Indian Oil Corporation announced plans to increase national refining capacity by 25%, backed by a ₹1.66 lakh crore investment program. This expansion is designed to secure domestic supply of process oils for rubber, footwear, and textile manufacturing. A parallel objective is petrochemical deepening. IOC is targeting a rise in its Petrochemical Intensity Index from 6.11% to 15% by 2030, with flagship 2025 projects such as the Paradip Petrochemical Complex focused on downstream process oil derivatives.

Quality and sustainability are converging. In August 2025, Shell India launched its upgraded Shell Helix Ultra range engineered with PurePlus gas-to-liquid technology to meet the 2025 API SQ Standard, signaling a shift toward ultra-pure GTL-based process oils in India. At the policy level, the SATAT initiative is accelerating bio-blending adoption. By late 2025, Indian refineries achieved an 18% bio-blend milestone through co-processing of non-edible oils, expanding the availability of sustainable process oils for industrial applications without compromising performance.

China: Specialty Output Growth and AI-Enabled Refining

China’s process oil industry is pivoting toward specialty products, digital refining, and low-carbon allocation. In its 2024–2025 annual review, PetroChina reported a 6.6% increase in specialty products and jet fuel output, even as gasoline yields declined. This shift reflects rising domestic demand for high-grade process oils used in EV batteries, advanced tires, and polymer elastomers. Policy support is reinforcing this trend. Under China’s New Materials Acceleration Program, output exceeded 2 million tons by early 2025, with a focus on polyolefin elastomers that require highly compatible naphthenic process oils.

Operational efficiency is improving through digitalization. Major Chinese refineries implemented AI-driven optimization tools during 2025, delivering 5–7% efficiency gains in the distillation of aromatic process oils with tighter quality control. Capital allocation is also evolving. PetroChina earmarked 8% of its 2025 capital expenditure for low-carbon initiatives, including the development of bio-based process oils from non-fossil feedstocks. China’s market trajectory therefore combines scale, digital efficiency, and early-stage decarbonization.

Sweden and European Union: Sustainability Leadership and Regulatory Standardization

The European process oil market, led by Sweden, is defined by sustainability leadership and regulatory harmonization. In October 2025, Nynas achieved the EcoVadis Platinum rating, placing its operations within the top one% globally for environmental and ESG performance. Product innovation is aligned with this positioning. Nynas expanded its EVO line in 2025, offering drop-in process oil alternatives that immediately reduce carbon footprint without requiring tire manufacturers to reformulate compounds.

Regulatory clarity is shaping product baselines. With EU REACH Annex XVII updates effective in 2026, European producers have fully phased out high-PCA aromatic extracts, standardizing treated distillate aromatic extract as the default rubber extension oil. Infrastructure decarbonization is reinforcing credibility. In May 2025, the Nynäshamn site completed its Clean Shore Power upgrade, enabling zero-emission vessel loading for process oil shipments. The EU market is thus anchored in compliance-led innovation and low-carbon logistics.

Brazil: Offshore Feedstocks and Premium Tire Supply Chains

Brazil’s process oil industry is underpinned by offshore feedstock strength and premium tire manufacturing demand. Petrobras continues to deploy large-scale floating production storage and offloading units in the Mero and Búzios fields, ensuring steady access to naphthenic-rich crude. This feedstock profile supports the production of heavy process oils essential for South American asphalt, rubber, and industrial applications.

Quality recognition underscores Brazil’s positioning in high-end segments. In December 2025, Ergon received the Pirelli Quality Award, highlighting the critical role of high-grade process oils in Brazil’s premium tire manufacturing ecosystem. Brazil’s market dynamics therefore reflect a combination of resource advantage and downstream quality-driven demand.

Comparative Overview of Country-Level Dynamics in the Process Oil Industry

Process Oil Market County Level Snapshot

|

Country / Region

|

Strategic Focus Areas

|

Implications for Process Oils

|

|

United States

|

Low-emission standards, grid fluids, API SQ

|

Growth in ultra-pure paraffinic and naphthenic oils

|

|

India

|

Refining scale-up, GTL adoption, bio-blending

|

Expanding domestic supply with sustainability tilt

|

|

China

|

Specialty materials, AI refining, low-carbon capex

|

Rising demand for high-compatibility process oils

|

|

Sweden / EU

|

REACH compliance, drop-in low-carbon oils

|

Standardized, sustainable process oil baselines

|

|

Brazil

|

Offshore crude integration, tire quality focus

|

Stable demand for heavy and premium-grade oils

|

Process Oil Market Report Scope

Process Oil Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.2 Billion

|

|

Market Size (2034)

|

$9.2 Billion

|

|

Market Growth Rate

|

2.8%

|

|

Segments

|

By Type (Naphthenic Oils, Paraffinic Oils, Aromatic Oils, White Oils, Bio-Based & GTL Oils), By Application (Tire & Rubber, Polymer & Plastics, Personal Care & Pharmaceuticals, Textiles, Electrical & Energy, Adhesives & Sealants), By Production Technology (Conventional Refining, Hydrocracking & Hydrotreating, Gas-to-Liquid Technology, Bio-Based Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Exxon Mobil Corporation, Shell plc, Nynas AB, Ergon Inc., PetroChina Company Limited, Indian Oil Corporation Limited, TotalEnergies SE, Petroliam Nasional Berhad, Idemitsu Kosan Co. Ltd., HollyFrontier Specialty Products, Repsol SA, Sinopec Group, H&R Group, Chevron Corporation, Apar Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Process Oil Market Segmentation

By Type

- Naphthenic Oils

- Paraffinic Oils

- Aromatic Oils

- White Oils

- Bio-Based & GTL Oils

By Application

- Tire & Rubber

- Polymer & Plastics

- Personal Care & Pharmaceuticals

- Textiles

- Electrical & Energy

- Adhesives & Sealants

By Production Technology

- Conventional Refining

- Hydrocracking & Hydrotreating

- Gas-to-Liquid Technology

- Bio-Based Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Process Oil Industry

- Exxon Mobil Corporation

- Shell plc

- Nynas AB

- Ergon Inc.

- PetroChina Company Limited

- Indian Oil Corporation Limited

- TotalEnergies SE

- Petroliam Nasional Berhad

- Idemitsu Kosan Co. Ltd.

- HollyFrontier Specialty Products

- Repsol SA

- Sinopec Group

- H&R Group

- Chevron Corporation

- Apar Industries Limited

*- List not Exhaustive