Market Overview: Syensqo Spin-Off, Electronic-Grade Demand Surge, and Agrochemical Expansion Define Catechol Market Growth

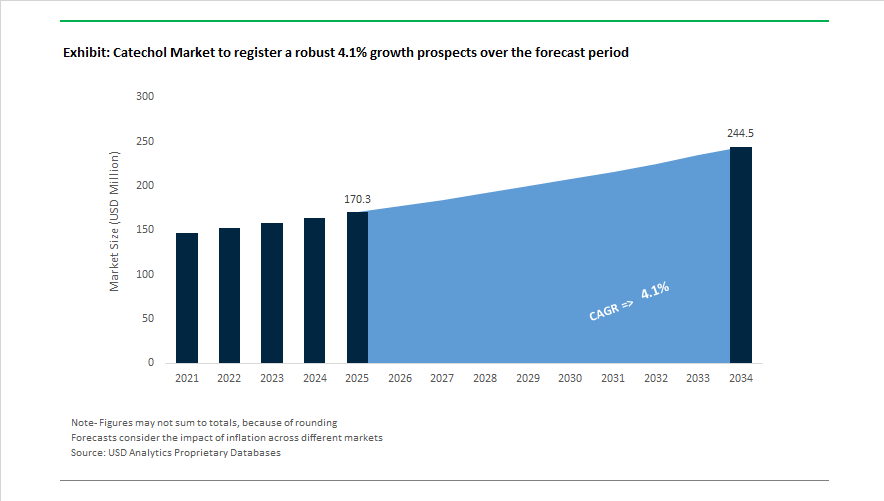

The Catechol Market is projected to increase from USD 170.3 Million in 2025 to USD 244.5 Million by 2034, advancing at a CAGR of 4.1% as demand rises for high-purity diphenols, antioxidant intermediates, and specialty aromatic chemicals across electronics, agrochemicals, flavors, and personal care. A major structural shift occurred in 2024 when Solvay completed its corporate separation, creating Syensqo, which now manages diphenols such as catechol under its Industrial Intermediates portfolio. This reorganization sharpened focus on high-growth applications including semiconductor materials and fragrance intermediates. In June 2024, Camlin Fine Sciences acquired Vitafor Invest NV in Belgium, expanding downstream exposure to animal nutrition where catechol-based antioxidants play a stabilization role.

Technology upgrades and sustainability initiatives accelerated through 2025. BASF introduced more sustainable catalytic oxidation routes for hydroquinone and catechol production in 2025, lowering environmental intensity in diphenol synthesis. UBE Industries completed debottlenecking projects in Asia during 2025 to secure supply for agrochemical intermediates such as carbamate pesticides. That same year, Huntsman expanded catechol production aimed at crop protection chemical demand, reflecting agricultural yield pressures in Asia. In August 2025, Camlin Fine Sciences reported revenue growth in Q1 FY26 driven by its integrated catechol to vanillin model, following the ramp-up of its adorr vanillin line during 2024 to 2025. In September 2025, Solvay announced the phase-out of TFA and derivatives by early 2026 as part of portfolio restructuring, signaling broader rationalization in complex organic intermediate production.

Circularity and high-purity applications increasingly shape market positioning. Syensqo reported record 2025 demand for electronic-grade catechol and hydroquinone used in photoresist materials for AI and 5G semiconductor fabrication. In October 2025, Axens moved toward full ownership of Eurecat, whose valorization technologies are being applied to complex diphenolic waste treatment, reinforcing circular chemical processing. January 2026 saw Evonik establish SYNEQT GmbH to streamline chemical park logistics in Germany, supporting specialty intermediates supply chains. During 2025, specialty firms including Merck piloted bio-based catechol derived from biomass fermentation, targeting clean beauty formulations.

Trends and Opportunities Reshaping the Global Catechol Market

Supply Disruption and Cost Inflation Triggered by Phenol Capacity Rationalization in Europe

The global catechol market is undergoing a structural reset linked to disruptions in upstream phenol supply. Because catechol is predominantly produced via hydroxylation of phenol, refinery shutdowns directly translate into constrained catechol output and elevated raw material costs. A defining moment occurred in July 2025, when INEOS Phenol confirmed the permanent shutdown of its Gladbeck, Germany facility, removing 650,000 metric tons of annual phenol capacity from Europe. This was not a temporary curtailment but a full exit that reconfigured the feedstock landscape and altered the cost baseline across the catechol value chain.

Since Q3 2025, European phenol pricing has maintained a consistent premium over Asia, peaking at USD 1,030/MT (FD Hamburg). This is not solely a demand-supply dynamic; it reflects structural energy inflation, carbon taxation, and geopolitical logistics rerouting. As freight around the Suez and Red Sea remains volatile, downstream catechol consumers in fragrances, antioxidants, and dye intermediates are migrating long-term procurement to China and India. For many FMCG brands and personal care formulators, the procurement challenge now rests on balancing ESG-compliant sourcing with cost stability, driving new hybrid sourcing models that blend Asia-Pacific bulk supply with regional polishing and purification in EU and U.S. facilities.

Acceleration of Precision Microbial Fermentation to Reduce Fossil Dependency

The catechol industry is now actively pursuing bio-based routes that reduce Scope 1–3 emissions and eliminate reliance on fragile petrochemical supply. While early-stage biocatalysis experiments once lacked yield efficiency, recent breakthroughs suggest commercial viability is approaching.

A pivotal example surfaced in August 2024 through a peer-reviewed Fermentation publication demonstrating that Bacillus subtilis, when applied in solid-state fermentation over barley bran, enabled significant increases in free catechol and gallic acid concentrations. What makes this breakthrough strategically meaningful is not the academic yield uplift, but the validation of a viable waste-to-catechol platform utilizing food and agricultural residues, reducing dependency on cumene–phenol processing.

Momentum accelerated further at the Tech Tour Bio-based Industries 2025 event in Germany, where several biotechnology startups revealed AI-powered Design–Build–Test–Learn (DBTL) systems that autonomously evolve microbial pathways. Their vision is 100% bio-certified catechol for cosmetic and pharma buyers by 2026, directly aligning with sustainability procurement frameworks like L’Oréal’s LCA mandates and Merck’s supplier risk scoring. For catechol producers, this signals an inflection point: value will increasingly shift from volume-based commodity sales toward IP-led fermentation, ESG compliance, and certification-driven pricing power.

High-Performance Catechol-Based Antioxidants for Engineering Polymers and UV Stability

Catechol is transitioning from a commodity chemical into a high-value structural ingredient for long-life polymer systems. The automotive, construction, and solar infrastructure industries are demanding additive packages capable of resisting UV degradation, thermal stress, and weather exposure over multi-decade asset lifetimes.

This demand materialized at scale in October 2025 when SONGWON announced investment expansion in Saudi Arabia to extend One Pack Systems (OPS) capacity for catechol-phosphite and hydroxybenzoate UV stabilizers. These high-performance blends are particularly essential in TPO membranes used in roofing, where UV-driven polymer erosion causes premature cracking. Likewise, Syensqo (formerly Solvay) disclosed that over 90% of its additive portfolio is now engineered for extreme durability—its CYASORB CYXTRA V series relies on catechol chemistry to deliver a balance of thermal stability and processing efficiency for lightweight EV interior components, where weight reduction is linked to battery-range economics.

This shift represents a margin expansion opportunity: proportionally, polymer stabilizers derived from catechol command significantly higher per-kilogram pricing than commodity catechol sold into dye or rubber applications.

Pharmaceutical-Grade Catechol as a Foundational Intermediate for Oncology and CNS Therapies

In pharmaceuticals, catechol serves as an indispensable chiral intermediate for complex heterocyclic synthesis. Demand is escalating due to oncology and CNS drug pipelines scaling in parallel with biotech investments.

In November 2025, the FDA issued Fast Track Designation for multiple agents including EGFR/HER3 ADC AVZO-1418 and DPTX3186. These compounds depend on catechol-derived intermediates to construct precise molecular architectures that deliver targeted tumor-site action. Similar requirements are emerging in neurology compounds designed to address dopamine-related disorders.

After a series of large 2025 acquisitions by Novartis and Merck & Co., procurement divisions are prioritizing supply resilience. This strategic shift is pushing manufacturers toward regional production hubs in North America and India to avoid regulatory compliance risks, transport delays, and purity inconsistencies. The pharmaceutical intermediates market trajectory indicates that catechol producers equipped to deliver GMP-compliant, ≥99.5% purity, and lot-traceability documentation will have the strongest negotiating leverage.

Catechol Market Share and Segmentation Insights

Market Share by Type: Industrial Grade Leads Volume as Electronic Grade Accelerates

Industrial grade catechol holds 58% of market share in 2025, reflecting its large-scale use in agrochemicals, polymer stabilizers, and rubber antioxidants, where typical purities of 98–99.5% balance performance with cost efficiency. Demand tracks agricultural chemical cycles and polymer production, with China remaining the dominant producer-consumer hub. Pharmaceutical grade ranks second, supplying 99.5% + purity catechol for API synthesis in bronchodilators, antihypertensives, anti-Parkinson’s therapies, and catecholamine pathways, supported by aging populations, chronic disease prevalence, and generic drug manufacturing. Electronic grade is the smallest but fastest-growing segment, driven by ultra-high-purity (99.9% +) requirements for electronic polymers, photoresists, and copper CMP corrosion inhibition. Advanced semiconductor node transitions, capacity expansions, and tighter contamination thresholds are accelerating adoption, shifting market value toward high-margin purification, traceability, and impurity control.

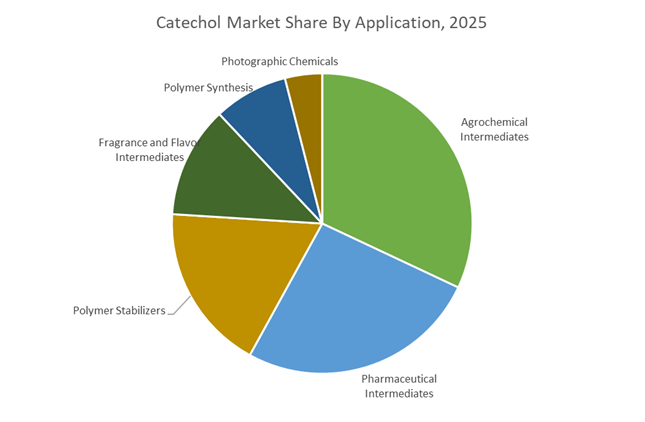

Market Share by Application: Crop Protection Dominates While Pharma and Polymers Add Stability

Agrochemical intermediates account for 32% of catechol demand in 2025, anchored by carbamate insecticides, phenoxy herbicides, and plant growth regulators, with seasonal volumes tied to crop cycles and commodity pricing, and generic production concentrated in India and China. Pharmaceutical intermediates follow, leveraging catechol derivatives in bronchodilators, methyldopa-class antihypertensives, and anti-Parkinson’s drugs, where high-purity inputs command premiums. Polymer stabilizers form a significant segment, using catechol as an antioxidant and polymerization inhibitor across polyolefins, polyamides, adhesives, and epoxy systems to extend service life in automotive and industrial components. Fragrance and flavor intermediates are a growing specialty outlet via guaiacol, vanillin, and piperonal pathways, while polymer synthesis remains niche for high-performance resins. Photographic chemicals continue structural decline, limited to residual specialty printing and medical X-ray applications.

Competitive Landscape of the Catechol Market

The global catechol market in 2026 is characterized by rapid capacity expansion, semiconductor-grade purity requirements, and rising demand from advanced electronics, pharmaceuticals, polymers, agrochemicals, and aroma ingredients. Competition centers on high-purity diphenols, vertically integrated phenol-to-catechol value chains, ISCC PLUS mass-balance certification, and downstream derivative integration. Leading manufacturers are differentiating through AI-driven process optimization, low-impurity synthesis routes, circular chemistry platforms, and local-for-local manufacturing footprints. Growth is further supported by strong uptake in 2nm semiconductor fabrication, clean-label flavors, polymerization inhibitors, and specialty pharma intermediates, positioning catechol as a strategic building block across multiple high-growth end-use industries.

Net-zero specialty catechol for green electronics from Syensqo

Syensqo enters 2026 as a pure-play specialty science leader following its demerger, focusing on mass-balance certified catechol aligned with ISCC PLUS standards. The company is a dominant supplier of catechol-derived intermediates for advanced semiconductors and high-performance polymers, supporting next-generation 2nm chip manufacturing. Its SyGPT and syensqo.ai platforms accelerate R&D cycles, enabling rapid customization of catechol derivatives for automotive and aerospace adhesives. With major manufacturing hubs in France and China, Syensqo maintains a resilient local-for-local supply chain, buffering customers from global trade volatility while advancing its net-zero specialty chemicals strategy for green electronics and sustainable pharmaceuticals.

Vertically integrated diphenol leadership by Camlin Fine Sciences

Camlin Fine Sciences (CFS) stands out in 2026 as the global integration champion in catechol and diphenols. Its Dahej facility in India has reached steady-state at doubled capacity of around 20,000 MT, reinforcing CFS as a price leader. The company has adopted a “zero-sale” approach, channeling internal catechol into high-value downstream products such as Vanillin (Vanesse), Ethyl Vanillin (Evanil), and Guaiacol. Following its French acquisition, CFS is consolidating European operations to optimize tariff exposure. Its proprietary green synthesis routes support the booming clean-label food, fragrance, and antioxidant markets, delivering strong traceability and sustainability credentials.

Semiconductor-grade ultra-pure catechol from UBE Corporation

UBE remains the 2026 benchmark for high-purity catechol, supplying critical materials to the global semiconductor and display industries. Its flaky powder catechol achieves sub-ppb metal impurity levels, making it essential for photoresist strippers and ultra-miniaturized circuitry. UBE’s proprietary CO and methanol-based production process delivers superior purity and cost efficiency versus traditional phenol hydroxylation. Strategically focused on 5G infrastructure, EV displays, and advanced electronics, UBE is commissioning a major manufacturing base in the United States during fiscal 2026, strengthening North American supply security and reducing dependence on Asian imports for mission-critical electronic materials.

Large-scale industrial catechol production by Jiangsu Sanjili Chemical Co., Ltd.

Jiangsu Sanjili leads China’s large-scale industrial catechol segment, leveraging deep integration within chemical parks and massive throughput capacity. In 2026, the company serves as a primary feedstock supplier to domestic agrochemical and dye manufacturers, producing molten and flake catechol for crop protection intermediates such as carbofuran phenol. Environmental upgrades completed in 2025 introduced advanced VOC recovery systems to meet China’s “Blue Sky” mandates. Looking ahead, Sanjili is diversifying downstream into tert-butyl catechol (TBC), supporting the fast-growing synthetic rubber and plastics industries across Asia-Pacific.

Aroma and vitamin integration driven by Brother Enterprises Holding Co., Ltd.

Brother Enterprises positions itself in 2026 as a vitamin and aroma chemicals specialist, using catechol as a core intermediate for vanillin and nutritional derivatives. After capacity debottlenecking in 2025, the company expanded strongly into South America and Africa, supplying catechol-based antioxidants for meat and poultry preservation. Its integrated “feed-to-flavor” model supports high utilization across Vitamin B3, flavor ingredients, and aromatic chemicals. Brother is also piloting a bio-fermentation hybrid route for biomass-derived catechol, targeting premium natural fragrance and organic ingredient markets, reinforcing its presence in sustainable aroma chemistry.

Knowledge-driven pharma intermediates from Aarti Industries Limited

Aarti Industries is advancing a knowledge-driven catechol strategy in 2026, prioritizing complex pharmaceutical intermediates over bulk volumes. New process blocks at its Jhagadia Zone IV platform support multi-step catechol derivatives for cardiovascular and Parkinson’s therapies. Despite tariff pressures, Aarti maintains a calibrated US market approach while improving capacity utilization for polymer additives. Its fully indigenous R&D and engineering capabilities enable rapid debottlenecking and process optimization without external licenses. By focusing on custom synthesis and benzene-based value chains, Aarti continues to deepen partnerships with global pharma innovators seeking high-purity, application-specific catechol intermediates.

India: Commercial Catechol Production Launch, PLI-Backed Fine Chemical Clusters, and Agrochemical Demand Surge

India’s catechol industry entered a structural transformation phase on December 18, 2025, when Clean Science and Technology Limited, through its subsidiary Clean Fino-Chem Limited, commenced commercial production of Catechol and Hydroquinone. This milestone significantly reduces India’s dependence on imported organic intermediates from China and Europe, strengthening domestic supply security for phenolic derivatives. The facility integrates advanced catalytic oxidation technologies, positioning India as an emerging producer of high-purity catechol for downstream fine chemicals and pharmaceutical synthesis.

The newly commissioned catechol output is primarily allocated for captive integration into Guaiacol and Veratrole manufacturing, critical intermediates for fragrance compounds and active pharmaceutical ingredients (APIs). In October 2025, the Directorate General of Foreign Trade revised import policy conditions, tightening permit requirements to encourage domestic production of specialized intermediates. Agrochemical exports expanded at a 14% CAGR, reaching $5.4 billion by 2025, intensifying demand for catechol in carbamate-based insecticides and fungicides. The Institute of Pesticide Formulation Technology announced successful field trials of Benzoyl Sulphonamide suspension concentrates utilizing catechol derivatives for enhanced crop protection performance. Under the Production Linked Incentive (PLI) scheme, Fine Chemical Clusters are being developed to deploy improved catalytic oxidation methods, targeting a 12% increase in catechol yield efficiency across domestic facilities.

China: Molten Catechol Capacity Expansion, Semiconductor Integration, and Green Chemistry Consolidation

China continues to dominate technical-grade molten catechol production, with early 2026 capacity peaks driven by expansion in Lianyungang Sanjili Chemical and Shanghai Amino-Chem industrial zones. These large-scale chemical parks consolidate production under stricter environmental compliance frameworks while achieving cost-efficient phenol hydroxylation throughput.

The Key State Laboratory of Fine Chemicals achieved a catalytic breakthrough in 2025 using enzymatic pathways that reduced phenol hydroxylation energy intensity by 18% and minimized undesirable isomer co-production. Chinese manufacturers have pivoted toward electronic-grade catechol derivatives for photoresist formulations supporting 7nm and 5nm semiconductor fabrication. Digitalization initiatives across major facilities incorporate IoT sensors and AI-driven oxidation controls, achieving a 9% reduction in chemical waste during distillation. Research published in early 2026 by the Affiliated Stomatological Hospital of Chongqing Medical University highlighted DOPA-derived catechol bioadhesives for precision medical applications. Meanwhile, the Ministry of Ecology and Environment implemented 2025 Green Chemistry guidelines, accelerating consolidation of smaller high-pollution units into environmentally compliant chemical parks.

United States: GMP Pharmaceutical-Grade Catechol, TSCA HAP Designation, and Bio-Adhesive Innovation

The United States catechol market is increasingly oriented toward pharmaceutical-grade production, regulatory compliance, and advanced biomaterials research. In late 2025, Chemwerth launched GMP-certified pharmaceutical-grade catechol tailored for synthesis of advanced neurological APIs. Regulatory oversight intensified following the U.S. Environmental Protection Agency designation of catechol as a Hazardous Air Pollutant (HAP) under updated TSCA provisions in late 2024, requiring manufacturers such as Eastman Chemical Company to install enhanced vapor recovery systems.

U.S. academic research in 2025–2026 has advanced catechol-PVA hydrogels inspired by mussel adhesion mechanisms, enabling wet-tissue bonding for cardiac and pulmonary surgeries. Specialty chemical firms reported a 6.5% increase in R&D investment for ethyl vanillin synthesis, reliant on high-purity catechol intermediates. The U.S. Department of Commerce has supported domestic development of secondary distillation units to secure 4-tert-butylcatechol supply, reinforcing polymerization inhibitor availability after global supply disruptions in 2024.

Japan: Electronic-Grade Purity Leadership and Lignin-Derived Catechol Innovation

Japan maintains global leadership in electronic-grade catechol production, particularly for photoresist applications in advanced semiconductor manufacturing. UBE Corporation expanded its C1 chemical portfolio in 2025, integrating proprietary catechol processing into high-performance urethanes and specialty esters. Metallic impurity thresholds are strictly controlled below 10 ppb, ensuring compatibility with high-resolution lithography.

UBE Group is constructing a large-scale Louisiana facility scheduled for H2 2026, transferring Japanese catechol-processing expertise into the North American supply chain. The Ministry of Economy, Trade and Industry has provided grants to accelerate lignin-derived catechol development using forest biomass, supporting renewable phenolic intermediates and reducing reliance on petroleum-based phenol feedstocks. This combination of ultra-high purity production and bio-based innovation secures Japan’s premium positioning in specialty catechol markets.

Canada: Pulp-Derived Catechol Streams and Tightened Cosmetic and Environmental Oversight

Canada’s catechol landscape is shaped by pulp and paper integration and precautionary regulatory controls. The Environment and Climate Change Canada reported in 2025 that catechol extraction from black liquor remains primarily an internal energy recovery process within pulp mills rather than a commercialized chemical stream.

Regulatory controls are stringent. Under the 2025 revision of the Health Canada Cosmetic Ingredient Hotlist, catechol remains prohibited in leave-on cosmetic formulations, redirecting personal care manufacturers toward alternatives such as BHT. Additionally, Canada introduced a Future Use Notification requirement in 2025, mandating federal risk assessment for any new industrial catechol application exceeding 10 metric tons annually. These policies position Canada as a tightly regulated but technically capable participant in niche catechol applications, with strong environmental monitoring frameworks.

Catechol Market Report Scope

Catechol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$170.3 Million

|

|

Market Size (2034)

|

$244.5 Million

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Type (Industrial Grade, Pharmaceutical Grade, Electronic Grade), By Form (Solid, Liquid), By Production Method (Phenol Hydroxylation, Cumene Process, Bio Based Production), By Application (Agrochemical Intermediates, Fragrance and Flavor Intermediates, Pharmaceutical Intermediates, Polymer Stabilizers, Polymer Synthesis, Photographic Chemicals), By End User (Agriculture, Pharmaceuticals and Healthcare, Food and Beverages, Cosmetics and Personal Care, Electronics and Electrical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Syensqo, UBE Corporation, Camlin Fine Sciences, Jiangsu Sanjili Chemical, Lianyungang Sanjili Chemical Industry, Hubei Yuancheng Saichuang Technology, Brother Enterprises, Mitsui Chemicals, Merck, Tokyo Chemical Industry, Alfa Aesar, Huntsman Corporation, Zhejiang Zhongxin Fluoride Materials, Versalis, Sisco Research Laboratories

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Catechol Market Segmentation

By Grade

- Industrial Grade

- Pharmaceutical Grade

- Electronic Grade

By Form

By Production Method

- Phenol Hydroxylation

- Cumene Process

- Bio Based Production

By Application

- Agrochemical Intermediates

- Fragrance and Flavor Intermediates

- Pharmaceutical Intermediates

- Polymer Stabilizers

- Polymer Synthesis

- Photographic Chemicals

By End User

- Agriculture

- Pharmaceuticals and Healthcare

- Food and Beverages

- Cosmetics and Personal Care

- Electronics and Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Catechol Industry

- Syensqo

- UBE Corporation

- Camlin Fine Sciences

- Jiangsu Sanjili Chemical

- Lianyungang Sanjili Chemical Industry

- Hubei Yuancheng Saichuang Technology

- Brother Enterprises

- Mitsui Chemicals

- Merck

- Tokyo Chemical Industry

- Alfa Aesar

- Huntsman Corporation

- Zhejiang Zhongxin Fluoride Materials

- Versalis

- Sisco Research Laboratories

*- List not Exhaustive