Esters Market to Reach $175.2 Billion by 2034 at 6.9% CAGR as Bio-Based Lubricants, Data Center Cooling Fluids, and Specialty Emollients Accelerate Demand

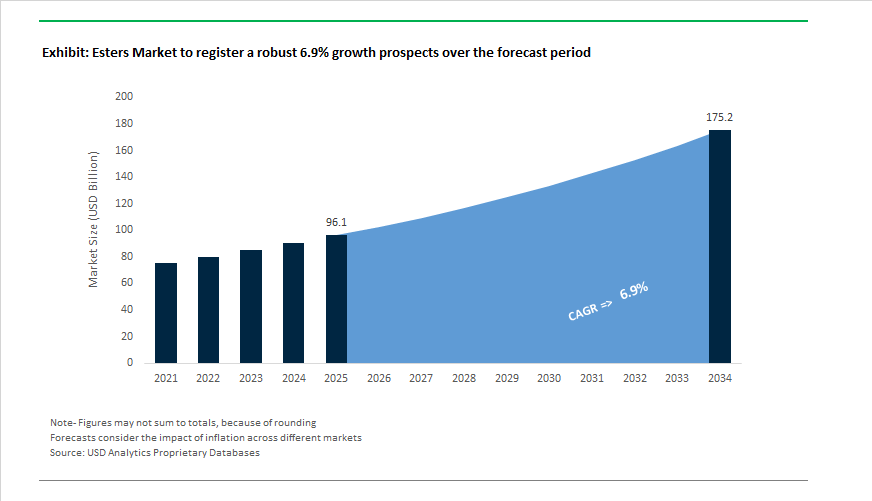

The Esters Market is projected to expand from $96.1 billion in 2025 to $175.2 billion by 2034, registering a CAGR of 6.9%, driven by structural demand in high-performance lubricants, dielectric cooling fluids, food emulsifiers, and bio-based personal care ingredients. A pivotal development occurred in January 2025, when Perstorp, a subsidiary of PETRONAS Chemicals Group, established a synthetic ester hub in Amsterdam. The facility focuses on advanced specialty fluids, including dielectric esters engineered for immersion cooling in hyperscale data centers and EV battery systems. Complementing this, Perstorp launched Synmerse™ DC in late 2024, a biodegradable synthetic cooling fluid formulated to handle extreme thermal loads generated by AI-driven semiconductor architectures. These innovations highlight a structural pivot in ester demand—from traditional plasticizers and lubricants toward thermally stable, low-carbon, high-dielectric fluids that support digital infrastructure expansion.

Capacity expansions in North America and Asia are reshaping supply dynamics. Oleon announced the addition of a state-of-the-art esterification and blending unit at its Conroe, Texas site, expected to be fully operational in early 2026. This investment localizes sustainable ester production for lubricants and industrial fluids, reducing transatlantic supply dependencies. In Japan, Mitsubishi Chemical Group commissioned a new sugar ester production line in March 2024, adding 2,000 tons per year to address escalating demand for food-grade emulsifiers, with a second line scheduled for 2026. Meanwhile, Clariant introduced next-generation Hostagliss™ synthetic esters in mid-2025, targeting water-based metalworking fluids that require self-emulsifying, polyether ester chemistries to replace mineral oil systems under tightening environmental regulations. These investments collectively reinforce a shift toward localized, high-purity, and application-specific ester production aligned with regulatory and sustainability imperatives.

The personal care and advanced materials segments are also expanding ester penetration. Croda International launched Crodamol GTS in April 2024, a 100% bio-based emollient ester positioned as a silicone alternative in inclusive hair care formulations. Its rapid adoption across 2025 underscores the migration from petrochemical-derived conditioning agents to biodegradable, renewable esters. In Asia, Croda’s $16 million expansion of its Singapore pastille ester facility increased regional supply capacity for cosmetic and specialty alkoxylate applications. Arkema is further strengthening its specialty ester value chain through the startup of its Rilsan® Clear unit in Singapore and its 1233zd fluorospecialty plant in the United States in late 2025, supporting electronics, healthcare, and low-GWP refrigeration markets. Concurrently, BASF and Evonik Industries are reallocating capital toward high-margin specialty ester portfolios as part of broader restructuring initiatives, emphasizing bio-based feedstocks and high-purity intermediates.

Trends and Opportunities in the Esters Market

Rapid Commercialization of Next-Generation Synthetic Lubricant Base Stocks

- Electrification of mobility platforms is fundamentally changing lubricant formulation priorities, accelerating the adoption of synthetic esters as Group V base stocks for EV drivetrains, e-axles, and battery thermal management. Unlike conventional PAOs, synthetic esters deliver a rare combination of dielectric behavior, polarity, and thermal conductivity, making them suitable for direct oil contact with electric motor windings and battery modules.

- Technical assessments published in February 2024 by the Society of Tribologists and Lubrication Engineers (STLE) confirmed that high-performance polyol esters can reduce friction coefficients by up to 32% compared to PAO 100-based formulations. This reduction directly translates into improved motor efficiency, lower heat generation, and extended driving range in compact 800V EV architectures. Responding to this demand, BASF announced plans to nearly double synthetic ester base oil capacity at its Jinshan site in China, positioning the facility as a strategic hub for e-driveline fluids in Asia-Pacific.

- Automotive OEMs such as Tesla, Hyundai, and BYD are increasingly shifting toward oil-cooled motors to manage higher power densities. In response, lubricant suppliers are engineering ultra-low-viscosity esters such as Cargill’s Priolube EF series, offering viscosities as low as 6.1 cSt at 40°C. These formulations minimize churning losses while maintaining strong polarity for heat transfer, positioning synthetic esters as indispensable materials in next-generation EV thermal systems.

Bio-Based Feedstock Diversification Beyond Palm and Coconut Oils

- Sustainability mandates and supply-chain risk are accelerating diversification away from palm and coconut oils toward second-generation, non-food biomass feedstocks. This transition is being driven by the EU Deforestation Regulation and growing scrutiny of land-use impacts embedded in tropical oil sourcing.

- In June 2024, the joint venture between Elevance Renewable Sciences and Wilmar launched a world-scale biochemical refinery in Asia based on olefin metathesis technology. The facility prioritizes tall oil, a pulp-and-paper byproduct, and waste animal fats to produce multifunctional esters with lower carbon intensity and reduced exposure to agricultural commodity volatility. These esters are increasingly specified in lubricants, surfactants, and cosmetic formulations seeking renewable content without compromising performance.

- Regulatory certainty is further supporting this trend. On September 17, 2025, the European Commission approved rapeseed oil as a low-risk active substance under Regulation (EU) 2025/1879 until 2040. This long-term authorization provides manufacturers with a stable regulatory runway to commercialize biodegradable ester-based botanical agrochemicals. By December 2025, industry reports confirmed that second-generation bio-esters such as levulinate-ketal esters were successfully replacing cyclic silicones like D5 in cosmetics, delivering comparable sensory profiles while achieving 100% renewable carbon content.

Formulation of Safe and Effective Solvents for Lithium-Ion Battery Manufacturing

- The global buildout of lithium-ion battery gigafactories is creating a premium opportunity for ester solvents as replacements for N-methyl-2-pyrrolidone, a reproductive toxicant facing tightening restrictions under REACH and TSCA. Battery manufacturers are actively seeking solvents that combine solvency power, fast evaporation, and improved worker safety.

- By November 2025, ultra-high-purity methyl acetate had emerged as a leading NMP substitute in electrode slurry mixing. Its rapid evaporation enables faster drying of coated electrodes, reducing energy consumption in calendering and drying ovens while improving throughput. From a performance standpoint, ester-based electrolyte systems are also gaining traction. Research published in Electrochimica Acta demonstrated that ethyl acetate–based electrolyte blends significantly enhance low-temperature performance. At −14°C, ester-blended lithium-ion cells retained approximately 40% of discharge energy at 4C rates, whereas conventional carbonate electrolytes delivered negligible capacity.

- This technical advantage is translating into commercial momentum. The market for high-purity ester solvents such as methyl acetate is projected to approach USD 295 million by 2032, driven largely by battery manufacturing, advanced electrode processing, and next-generation electrolyte development. For ester producers, this represents a high-margin entry point into the energy storage value chain.

Development of Biodegradable Esters for Low-Toxicity Agrochemicals

- Agricultural regulation is emerging as a powerful demand catalyst for biodegradable ester carriers, particularly in Europe and North America. Under the EU Farm to Fork Strategy and California Department of Pesticide Regulation initiatives, formulators are being forced to replace persistent aromatic solvents with ester-based systems that degrade rapidly after application.

- From May 12, 2025, the EU reduced Maximum Residue Limits for several active substances to the limit of determination at 0.01 mg/kg. This regulatory shift compels agrochemical companies to use biodegradable esters as co-solvents and penetrants that ensure effective delivery while minimizing residual contamination. In October 2025, biodegradable ester-based coatings and microencapsulation systems were identified as the fastest-growing segment within crop protection, as they enable controlled release and reduce total active ingredient loading per hectare.

- Precision agriculture is amplifying this opportunity. AI-driven spraying systems increasingly rely on ester-based adjuvants engineered to optimize droplet adhesion and reduce drift. These properties directly support the EU target of reducing chemical pesticide use and risk by 50% by 2030. As a result, esters are transitioning from auxiliary solvents to core enablers of sustainable, regulation-compliant crop protection strategies.

Esters Market Share and Segmentation Insights

Polyester Resin Esters Anchor Composite, Packaging, and Industrial Materials Demand

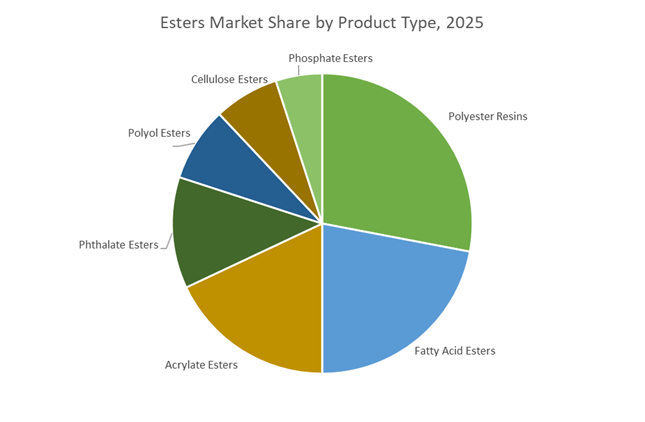

Polyester resins account for 28% of total esters market share in 2025, driven by widespread use in fiber-reinforced composites, synthetic fibers, and packaging materials across construction, marine, and automotive sectors. Their strong mechanical properties, processing flexibility, and cost efficiency position them as foundational materials for structural panels, automotive components, and consumer packaging. Fatty acid esters form a significant secondary segment, supported by rising adoption in personal care, food formulations, and biodegradable lubricants as manufacturers pivot toward bio-based ingredients. Acrylate esters remain critical monomers for acrylic polymers used in coatings and adhesives, delivering durable film formation and weather resistance. Phthalate esters retain a steady presence in flexible PVC despite regulatory pressure, while polyol esters are gaining momentum in high-performance refrigeration and aviation lubricants. Cellulose esters and phosphate esters serve specialty niches, supporting applications requiring optical clarity, flame retardancy, and extreme-condition lubricity.

Paints and Coatings Drive the Largest Share of Ester Consumption Worldwide

Paints and coatings represent 32% of global ester demand in 2025, making this the leading application segment. Polyester resins, acrylate esters, and cellulose esters are extensively used in architectural, industrial, and automotive coatings to enhance durability, gloss, adhesion, and corrosion resistance. Lubricants and greases follow as a major segment, incorporating fatty acid esters, polyol esters, and phosphate esters for biodegradability, thermal stability, and extreme-pressure performance in automotive and industrial systems. Personal care and cosmetics maintain strong uptake of fatty acid esters as emollients and texture modifiers, while chemical processing relies on esters as solvents and intermediates for specialty chemicals and polymers. Food and beverage applications remain steady through regulated emulsifiers and stabilizers. Pharmaceuticals represent a fast-growing segment, leveraging ester chemistry in drug delivery systems, coatings, and controlled-release formulations.

Competitive Landscape of the Esters Market

The global esters market is shaped by vertically integrated chemical majors and precision specialty players competing across bio-based esters, synthetic ester base oils, sugar esters, cosmetic esters, and high-performance lubricant esters, with sustainability, circular chemistry, and APAC capacity expansion defining leadership in 2026.

BASF drives circular chemistry leadership across synthetic and bio-based ester value chains

BASF SE dominates the global esters market through its Verbund integration, controlling the value chain from feedstocks to high-purity specialty esters. BASF reported preliminary 2025 sales of ~€59.7 billion and is targeting €6.7 to €7.2 billion EBITDA in 2026 as chemical demand rebounds. The company nearly doubled synthetic ester base oil capacity at Jinshan, China, to serve Asia’s high-performance lubricant market, while launching bio-based acrylic esters for coatings and long-chain fatty esters for automotive engine oils. Backward integration into ammonia and ethylene oxide delivers major cost advantages in polyol and phosphate esters. BASF’s sustainability strategy targets net-zero CO2 by 2050, reinforcing its leadership in circular ester chemistry.

Cargill leads plant-based esters for clean-label food and bio-industrial applications

Cargill Incorporated is the global powerhouse in plant-derived esters, leveraging unmatched access to vegetable oil feedstocks. In January 2026, Cargill invested over RMB 45 million to expand its Beijing facility, strengthening ester-based functional systems for APAC food and beverage markets. The company won the 2026 BIG Innovation Award for sustainable ingredient technology and specializes in MCT oils and sucrose esters used in clean-label infant nutrition and premium confectionery. Its 2026 AI-driven optimization platform enhances real-time feed and ingredient efficiency, especially in aquafeed and animal nutrition. With farm-to-formulation integration and full traceability, Cargill anchors global demand for bio-based fatty acid esters.

Croda accelerates high-margin specialty esters for personal care and biopharma delivery

Croda International Plc operates as the industry’s precision specialist, supplying low-inclusion cosmetic esters and life-science ingredients. Following its February 2026 results, Croda introduced a three-year framework focused on high-margin specialty growth. It expanded its SenStories™ selector in late 2025 to guide formulators toward optimal skin-feel ester systems and commissioned its Singapore Pastillator 4 facility (15 kt capacity) to meet APAC demand for premium personal care esters. A strategic partnership with Amino GmbH integrates tailored esters into biopharma drug delivery. Known for “Smart Science,” Croda is consistently ranked among the UK’s most admired chemical companies for sustainable innovation.

Mitsubishi Chemical scales sugar esters for food emulsification and ultra-pure specialties

Mitsubishi Chemical Group is the world leader in sugar esters, supplying critical emulsifiers to global food manufacturers. The company expanded capacity by 2,000 tons in 2024 and added a further 1,100 tons per year at its Kyushu plant by March 2026. Its Ryoto™ Sugar Ester series is the benchmark for canned beverages, low-fat bakery, and confectionery stabilization. Mitsubishi is also pivoting toward ultra-high-purity esters for pharmaceutical and semiconductor applications. With Asia-Pacific holding the largest esters market share, valued above $4.06 billion in 2025/2026, Mitsubishi’s regional scale underpins its leadership in food safety and advanced ester purification.

ExxonMobil powers synthetic ester growth for EV thermal fluids and aerospace lubricants

Exxon Mobil Corporation leads high-performance synthetic esters for aerospace, energy, and industrial lubrication. Backed by a $400+ billion asset base, ExxonMobil controls the full chain from hydrocarbons to high-purity alcohols used in esterification. In 2025/2026, it expanded its Singapore petrochemical complex to boost specialty ester output for electric vehicle thermal management fluids. Its Esterex™ synthetic esters are prized for thermal stability and low volatility in jet engines and hydraulic systems. The company’s lower-emission product strategy focuses on friction-reducing lubricants that enhance fuel efficiency across heavy-duty transport and advanced manufacturing.

Japan: Bio-Based Innovation and High-Purity Ester Leadership

Japan’s esters market is being reshaped by a convergence of food-grade capacity expansion, bio-based materials innovation, and semiconductor-driven purity requirements. In March 2024, Mitsubishi Chemical Group completed a 2,000-ton capacity expansion of sugar ester emulsifiers at its Kyushu Plant, followed by a second 1,100-ton expansion scheduled to be operational by March 2026. This phased investment reflects sustained global demand for food-grade surfactants that deliver stable emulsification while aligning with clean-label and allergen-free formulation trends across Asia, Europe, and North America.

Beyond food applications, Japan is positioning esters at the center of advanced materials and sustainability transitions. In late 2025, Mitsubishi Chemical adopted its DURABIO™ bio-based polycarbonate ester for interior components in Honda’s N-ONE e: electric vehicle, signaling broader automotive acceptance of renewable ester polymers. Regulatory pressure on fluorinated chemistries has also accelerated PFAS-free coating development. In December 2025, Mitsubishi Chemical introduced a paper coating technology using SoarnoL™ EVOH resin as an oil-resistant alternative for food packaging, aligned with 2026 restrictions on fluorinated substances. On the electronics front, Sumitomo Chemical and peers are deploying Agentic AI systems in 2026 to optimize ultra-high-purity ester synthesis for 2nm photoresist materials. Parallel to this, a late-2025 joint venture between Asahi Kasei, Mitsui Chemicals, and Mitsubishi Chemical is advancing chemical recycling of methyl methacrylate esters, embedding circularity into Japan’s acrylic ester value chain by Q3 2026.

United States: Biofuel Policy Realignment and Specialty Ester Upgrading

The U.S. esters market is being decisively influenced by federal biofuel policy reforms and decarbonization-linked capital deployment. Effective January 1, 2025, the Inflation Reduction Act’s Clean Fuel Production Credit (45Z) replaced the traditional blender’s credit, reshaping ester demand economics. Under the 2026 framework, soybean-based biodiesel composed of fatty acid methyl esters qualifies for an estimated $0.64 per gallon incentive, provided North American feedstocks are used. This has reinforced domestic esterification capacity investment and strengthened supply chain localization.

Regulatory momentum is also accelerating aviation and marine bio-ester adoption. In June 2025, the Environmental Protection Agency proposed a record 5.61 billion gallon biomass-based diesel blending target for 2026. This signal has driven multi-million-dollar expansion plans by vertically integrated producers such as Chevron Renewable Energy Group, particularly in esterification and transesterification units. At the specialty end, Eastman Chemical Company announced global price increases on esters and oxo-derivatives effective January 2026 to offset rising operational costs and fund low-carbon infrastructure upgrades. Meanwhile, Perstorp launched saturated synthetic polyol esters in June 2025, engineered for high-temperature aerospace and EV thermal management systems. This illustrates a clear bifurcation in the U.S. market between volume-driven bio-esters and high-margin specialty ester chemistries.

India: Policy-Driven Scale-Up and Domestic Ester Localization

India’s esters market is expanding on the back of aggressive biofuel mandates, emissions regulation, and industrial policy support. For the 2025–26 supply year, the Government of India removed quantitative restrictions on ethanol production, targeting a 20% ethanol-gasoline blending ratio by end-2026. This policy shift is driving strong demand for fermentation-derived esters across fuel, solvent, and intermediate applications, particularly as sugar mills and grain processors diversify revenue streams.

Environmental compliance is adding further momentum. In October 2025, the Ministry of Environment, Forest and Climate Change finalized emission intensity targets under the Carbon Credit Trading Scheme, mandating up to 11% greenhouse gas intensity reductions for petrochemical producers during the 2025–26 cycle. Ester manufacturers are responding by investing in energy-efficient esterification processes and bio-based feedstocks. Industrial capacity is also being reinforced through the Production Linked Incentive scheme. In March 2025, Rs. 28,602 crores were approved for 12 new specialty chemical projects, with a strong emphasis on pharmaceutical and agrochemical ester intermediates. Parallel investments by Balrampur Chini Mills and Shree Renuka Sugars in late 2025 expanded distillation capacity, positioning India as a competitive ester producer aligned with both fuel security and export-oriented specialty chemicals.

China: Portfolio Rebalancing Toward Specialty Esters

China’s esters market is undergoing a structural transition from volume-driven commodity production to higher-value specialty formulations. BASF is nearing full capacity doubling of its synthetic ester base oil production at the Jinshan site in Shanghai, with full throughput expected by mid-2026. These synthetic esters are targeted at high-performance lubricants used in automotive, wind energy, and industrial machinery across Asia.

At the same time, the €10 billion Zhanjiang Verbund project is moving into downstream activation. BASF began phased startups of acrylate ester and specialty additive units in late 2025, strengthening local supply for China’s automotive and coatings industries through 2026. This industrial repositioning aligns with broader national trends. According to Deloitte’s 2026 Chemical Industry Outlook, China is actively rationalizing overcapacity in basic ester categories and reallocating capital toward specialty polyol esters to mitigate margin compression. As a result, ester production in China is becoming more application-specific, integrated, and technologically differentiated.

Singapore: Regional Hub for High-Purity Specialty Esters

Singapore continues to strengthen its role as an Asia-Pacific hub for high-purity and specialty esters serving personal care and pharmaceutical markets. In late 2024, Croda International inaugurated its $16 million Pastillator 4 facility at Jurong Island’s Seraya site. Throughout 2025 and 2026, this unit is ramping toward its full 15-kiloton capacity, focused on precision-engineered ester products with tight particle size and purity control.

The strategic significance of this investment lies in its proximity to fast-growing ASEAN consumer markets and regulated pharmaceutical supply chains. By concentrating ester finishing and formulation in Singapore, Croda and similar players are reducing lead times, ensuring regulatory consistency, and supporting premium positioning in cosmetics, dermatology, and drug delivery systems. This reinforces Singapore’s function as a regional value-addition and innovation node rather than a bulk production center.

Strategic Snapshot: Esters Market by Country

Esters Market County Level Snapshot

|

Country

|

Primary Growth Lever

|

Key Ester Applications

|

Strategic Orientation

|

|

Japan

|

Bio-based materials, electronics purity

|

Food emulsifiers, EV plastics, photoresists

|

High-purity and circular esters

|

|

United States

|

Biofuel incentives, specialty materials

|

Biodiesel, aerospace lubricants

|

Policy-driven volume plus premium niches

|

|

India

|

Ethanol blending, PLI incentives

|

Fuel esters, pharma intermediates

|

Import substitution and scale-up

|

|

China

|

Portfolio rebalancing, Verbund integration

|

Synthetic lubricants, acrylates

|

Shift from commodity to specialty

|

|

Singapore

|

Regional hub investments

|

Personal care, pharma esters

|

High-value finishing and formulation

|

Esters Market Report Scope

Esters Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$96.1 Billion

|

|

Market Size (2034)

|

$175.2 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Product Type (Fatty Acid Esters, Polyol Esters, Phthalate Esters, Acrylate Esters, Phosphate Esters, Cellulose Esters, Polyester Resins), By Source (Bio-Based, Synthetic), By Application (Lubricants and Greases, Personal Care and Cosmetics, Food and Beverages, Chemical Processing, Pharmaceuticals, Paints and Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Eastman Chemical Company, Croda International Plc, Evonik Industries AG, Cargill, Incorporated, Mitsubishi Chemical Group Corporation, Arkema S.A., Oleon N.V., Stepan Company, KLK Oleo, Wilmar International Limited, Innospec Inc., Fine Organics Industries Limited, Perstorp Group, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Esters Market Segmentation

By Product Type

- Fatty Acid Esters

- Polyol Esters

- Phthalate Esters

- Acrylate Esters

- Phosphate Esters

- Cellulose Esters

- Polyester Resins

By Source

By Application

- Lubricants and Greases

- Personal Care and Cosmetics

- Food and Beverages

- Chemical Processing

- Pharmaceuticals

- Paints and Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Esters Industry

- BASF SE

- Eastman Chemical Company

- Croda International Plc

- Evonik Industries AG

- Cargill, Incorporated

- Mitsubishi Chemical Group Corporation

- Arkema S.A.

- Oleon N.V.

- Stepan Company

- KLK Oleo

- Wilmar International Limited

- Innospec Inc.

- Fine Organics Industries Limited

- Perstorp Group

- Huntsman Corporation

*- List not Exhaustive