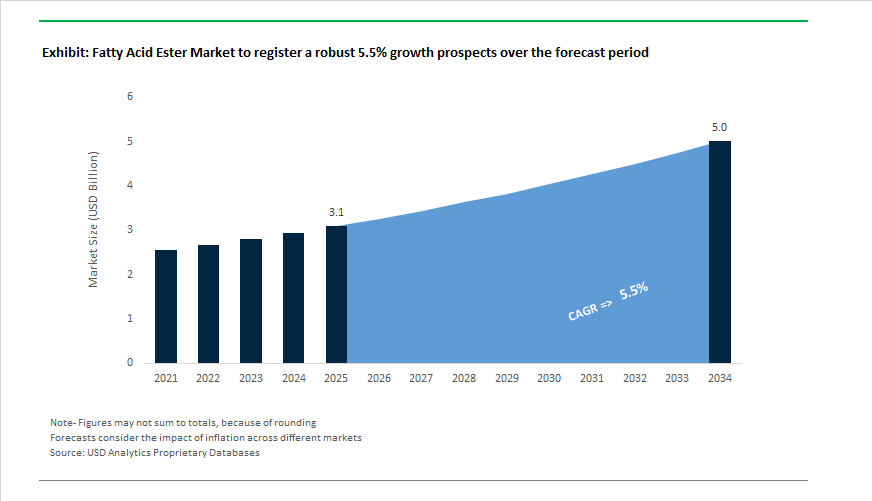

Fatty Acid Ester Market Valued at $3.1 Billion in 2025 Set to Reach $5 Billion by 2034 at 5.5% CAGR Driven by Bio-Based Lubricants, EV Fluids and High-Purity Specialty Esters

The Fatty Acid Ester Market is projected to increase from $3.1 billion in 2025 to $5 billion by 2034, advancing at a CAGR of 5.5%. Growth momentum is anchored in expanding demand for bio-based lubricants, phosphate ester emulsifiers, polyol esters, medium-chain triglycerides, and high-purity pharmaceutical-grade esters. Regulatory pressure on carbon intensity, sustainability compliance in consumer goods supply chains, and performance requirements in electric vehicle fluids are reshaping procurement strategies across lubricants, coatings, cosmetics, and biopharma segments. Market expansion is further supported by upstream feedstock integration in palm-based oleochemicals, capacity additions in isostearic and dimer acids, and diversification into biodegradable ester derivatives for industrial and agricultural use.

In early 2024, Oleon commissioned a new reactor at its Ertvelde, Belgium site, doubling production capacity for isostearic and dimer acids, critical intermediates for high-stability fatty acid esters used in premium cosmetics and high-performance lubricants. During 2024, Stepan Company completed the full integration of Ecogreen Oleochemicals’ fatty acid ester business, strengthening its footprint in medium-chain triglycerides and polyol ester segments serving food, nutrition, and pharmaceutical applications. In October 2024, Emery Oleochemicals expanded its USDA BioPreferred 100% bio-based portfolio by adding four pelargonic acid derivatives, reinforcing its biodegradable lubricant and herbicide ester platform. The same month, Oleon finalized the integration and renaming of A.Azevedo Óleos to Oleon Brasil SA, establishing its first major South American manufacturing base in Itupeva, São Paulo, positioned as a strategic hub for plant-based esters targeting Latin American lubricants and personal care markets.

Strategic developments intensified in 2025 across leadership, supply chain control, and sustainability compliance. In June 2025, Wilmar International signed an agreement to acquire PZ Cussons plc’s 50% stake in the PZ Wilmar joint venture for $70 million, consolidating its palm-based value chain in Africa and securing feedstock control for fatty acid ester production lines. In June 2025, Emery Oleochemicals achieved ISO 50001 certification and earned the EcoVadis Silver Medal, ranking within the top 15% globally and aligning with its 2026 strategy to supply carbon-transparent esters to multinational consumer brands. In July 2025, BASF started expanded production at its Nanjing, China site for polyetheramines and ester precursors, strengthening upstream intermediates supporting specialized fatty acid ester lines for Asian home and personal care markets through 2026. In July 2025, Emery appointed Min Chong as Group CEO, accelerating its pivot toward high-performance natural-based specialty chemicals and expanding DEHYLUB® ester base stocks and EMEROX® specialty acids for EV and industrial fluids.

Product innovation and compliance positioning gained further traction toward late 2025 and 2026. In October 2025, Wilmar maintained its top global ranking in the Global Child Protection Benchmark, reinforcing ethical sourcing compliance critical for ester exports to Europe and North America. In December 2025, Croda International entered a strategic supply partnership with Amino GmbH to expand its pharmaceutical-grade ester capabilities, leveraging its high-purity Super Refined™ platform and preparing for the launch of the BioXPro™ range in January 2026 to address evolving biopharma formulation requirements. In 2025, Croda Beauty launched Natrineo™ CR8, a PEG-free phosphate ester emulsifier responding to clean-label cosmetic formulation trends and enabling advanced W/O/W emulsions. In May 2026, Emery announced it will showcase next-generation ester-based technologies for electric vehicle fluids and sustainable industrial coatings at the American Coatings Show 2026, highlighting the sector’s transition toward thermally stable, oxidation-resistant, bio-based ester chemistries tailored for EV drivetrain lubrication and advanced coatings applications.

Trends and Opportunities in the Fatty Acid Ester Market

Commercialization of Isosorbide-Based Diesters as Non-Toxic Plasticizers

- The global phase-out of phthalate plasticizers has moved decisively from regulatory intent to full-scale commercial substitution, positioning isosorbide-based fatty acid esters as a leading solution. These diesters, synthesized from renewable sorbitol, are gaining traction across medical devices, toys, flooring, and flexible PVC applications where toxicological safety and regulatory compliance are non-negotiable.

- By late 2025, Roquette had optimized world-scale isosorbide production using its patented sorbitol dehydration process. The ability to consistently deliver isosorbide at purities above 99.5% has enabled downstream synthesis of isosorbide dioleate and isosorbide monostearate suitable for sensitive applications governed by EU REACH and U.S. EPA standards. These materials are now being specified in medical-grade PVC formulations and children’s products, where legacy plasticizers such as DINP and DEHP face structural exclusion.

- From a performance standpoint, 2024 technical benchmarking confirmed that isosorbide-based diesters can deliver approximately 15% higher plasticizing efficiency than conventional DINP in selected flexible PVC systems. This efficiency advantage allows compounders to reduce total additive loading while maintaining low-temperature flexibility, transparency, and mechanical durability, improving both material economics and lifecycle performance.

- Strategically, BASF accelerated its Biomass Balance portfolio expansion during 2025, introducing renewable-attributed ester plasticizers targeted at green building materials. These offerings are increasingly specified in resilient flooring, wall coverings, and interior construction products where embodied carbon reporting and material health disclosures are now standard procurement criteria.

High-Purity Synthetic MCTs for Pharmaceuticals and Lipid Nanoparticle Delivery

- Medium-chain triglycerides have transitioned from nutritional supplements into mission-critical pharmaceutical excipients, creating a premium demand segment within the fatty acid ester market. Synthetic MCTs based on caprylic (C8) and capric (C10) esters are now essential components in drug solubilization, parenteral nutrition, and lipid nanoparticle delivery systems.

- In January 2025, IOI Oleo GmbH reaffirmed its leadership in pharmaceutical-grade MCTs through EU-GMP and U.S. FDA-certified production in Germany. Its WITARIX® and MIGLYOL® product lines are widely used as solubilizers for poorly water-soluble active pharmaceutical ingredients, directly enhancing oral and injectable drug bioavailability.

- Unlike food-grade triglycerides, pharmaceutical MCTs are engineered for ultra-low moisture content, narrow molecular weight distribution, and exceptional oxidative stability. These attributes are critical for parenteral nutrition and mRNA-based vaccine formulations, where lipid degradation can compromise therapeutic efficacy and shelf stability. The increasing use of lipid nanoparticles as delivery vehicles has elevated synthetic fatty acid esters from formulation aids to enabling technologies in advanced therapeutics.

- Beyond excipients, 2025 also saw the commercialization of ketone ester-based therapies targeting metabolic and neurological disorders. These high-purity fatty acid esters are designed for controlled release and patient tolerability, reinforcing the long-term structural demand for precision-engineered ester chemistries in regulated healthcare markets.

Low-VOC, Biodegradable Solvents for Industrial and Institutional Cleaning

- Industrial and institutional cleaning is emerging as a high-volume opportunity for fatty acid methyl esters as regulators and facility operators move aggressively away from petroleum-derived solvents. Under pressure from the U.S. EPA TSCA framework and the EU Water Framework Directive, manufacturers are prioritizing solvents that combine high solvency with rapid biodegradability and low worker exposure risk.

- In May 2025, Cargill launched a new portfolio of fatty acid esters derived from soybean and coconut oil for low-VOC cleaning and coating applications. These esters deliver strong grease and ink removal performance while avoiding the respiratory and aquatic toxicity concerns associated with glycol ethers and chlorinated solvents. Their ability to achieve over 90% biodegradation within 28 days significantly reduces wastewater treatment costs for industrial users.

- Policy-driven scale effects are reinforcing this opportunity. Indonesia’s expansion of mandatory bio-content requirements to B40 in January 2025 is increasing global methyl ester production volumes, improving supply chain resilience and lowering unit costs. This biodiesel-linked capacity expansion is indirectly strengthening the economics of ester-based solvents for I&I cleaning, coatings maintenance, and surface preparation applications worldwide.

Performance Additives for Lithium-Ion Battery Electrolytes and Energy Storage

- Fatty acid esters are gaining strategic importance in lithium-ion battery and energy storage systems as manufacturers pursue higher energy density, improved safety, and longer cycle life. Specialized esters are increasingly used as co-solvents and functional additives to stabilize electrolyte chemistry under high-voltage and high-temperature conditions.

- Research published in June 2025 demonstrated that esters such as methyl trifluoroacetate can significantly enhance the stability of the solid-electrolyte interphase at operating voltages up to 5.5 V. By suppressing electrolyte decomposition, these additives improve capacity retention in nickel-rich cathode systems, including NCM811, which are widely adopted in next-generation electric vehicles.

- Thermal safety is a parallel driver. Chemical suppliers are developing flame-retardant ester blends that improve electrolyte wettability while reducing the risk of thermal runaway. These formulations are particularly relevant as battery pack architectures become denser and fast-charging protocols impose greater thermal stress on cell chemistry.

- Market pull remains strong. Global EV sales reached approximately 17 million units in 2024, while grid-scale energy storage capacity exceeded 7.5 GW, according to U.S. Department of Energy documentation. This dual expansion across mobility and stationary storage is creating sustained, high-value demand for fatty acid ester additives that can meet stringent performance, safety, and longevity requirements.

Fatty Acid Ester Market Share and Segmentation Insights

Fatty Acid Methyl Esters Lead Volume Growth Supported by Biofuel Mandates and Oleochemical Demand

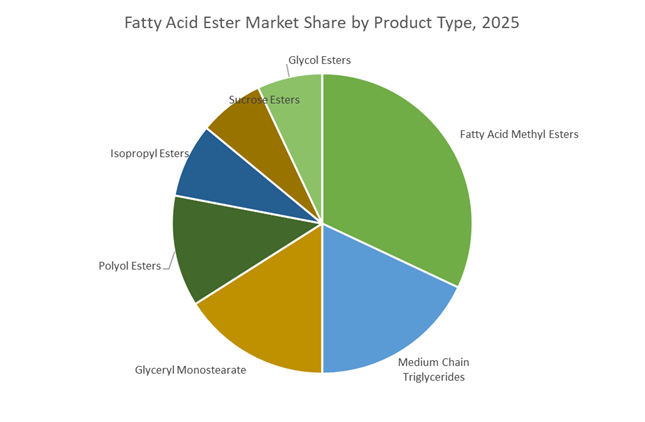

Fatty Acid Methyl Esters (FAME) account for 32% of total fatty acid ester market share in 2025, driven primarily by large-scale biodiesel production and expanding renewable fuel mandates worldwide. Beyond energy, FAME also serves as a key oleochemical intermediate and industrial solvent, reinforcing its dominant volume position. Medium chain triglycerides represent a significant premium segment, valued in nutraceuticals, medical nutrition, pharmaceuticals, and personal care for rapid metabolism and emollient properties. Glyceryl monostearate maintains strong demand as a multifunctional emulsifier across food processing and cosmetics. Polyol esters are gaining momentum in high-performance refrigeration and aviation lubricants, supported by HFC phase-down regulations and demand for biodegradable fluids. Isopropyl esters remain steady in skincare formulations, while sucrose esters and glycol esters occupy smaller but growing niches aligned with clean-label food emulsifiers and specialty HLB-controlled personal care systems.

Surfactants and Detergents Anchor Consumption as Personal Care and Polymers Accelerate

Surfactants and detergents represent 28% of global fatty acid ester consumption in 2025, reflecting widespread use in laundry, dishwashing, and industrial cleaning products where biodegradability and mildness outperform petrochemical alternatives. Personal care and cosmetics form a major secondary segment, leveraging fatty acid esters as emollients, emulsifiers, and sensory modifiers in skincare, haircare, and color cosmetics amid rising demand for plant-derived ingredients. Food processing remains significant, utilizing esters to improve texture, stability, and shelf life in bakery, dairy, and confectionery applications. Lubricants and greases rely on ester chemistry for biodegradable hydraulic fluids and metalworking oils in environmentally sensitive environments. Pharmaceuticals maintain steady uptake through excipient and drug delivery roles, while polymers and plastics represent a fast-growing segment, adopting fatty acid esters as bio-based plasticizers and processing aids in PVC, bioplastics, and compound formulations.

Competitive Landscape of the Fatty Acid Ester Market

The global Fatty Acid Ester market is defined by vertically integrated oleochemical majors and specialty innovators competing across bio-based lubricants, personal care esters, EV thermal fluids, and clean-label food applications, with circular chemistry, traceable feedstocks, and high-purity production emerging as decisive differentiators.

BASF SE leads specialty fatty acid esters with circular chemistry and EV-grade innovation

BASF SE remains a dominant force in high-performance fatty acid esters, leveraging its Verbund integration and deep R&D pipeline. In 2026, BASF is aggressively marketing Verdessence™ and Cetiol® as waxy plant polymer solutions positioned as 1:1 replacements for synthetic microplastics in cosmetics. Early 2026 also saw the launch of next-generation long-chain specialty esters engineered for high thermal stability in EV battery cooling fluids. Through its mass-balance circular chemistry platform, customers can track renewable feedstock content such as palm or coconut oil at batch level. BASF further expanded its Monheim site in late 2025 to boost high-purity ester output for Europe’s premium personal care market.

Wilmar International Limited dominates volume supply via palm integration and biodiesel-grade FAME

Wilmar International Limited leverages unmatched palm oil integration to command a cost advantage across fatty acid methyl esters and food-grade derivatives. In 2026, Wilmar stands as a primary supplier of FAME supporting Indonesia’s B40 biodiesel mandate, highlighting its strength in renewable fuels. The company controls the full value chain from plantations and crushing mills to esterification, ensuring traceability and supply security. Its Glyceryl Monostearate portfolio holds the largest volume share in food applications, particularly for texture enhancement in plant-based meat alternatives. To capture Southeast Asia manufacturing growth, Wilmar announced a multi-million-dollar investment in a new Vietnam oleochemical complex in early 2026.

Cargill, Incorporated scales bio-industrial esters for lubricants, coatings, and clean-label foods

Cargill, Incorporated combines global agricultural feedstock access with advanced ester chemistry for bio-industrial performance. Its Agri-Pure™ and Oxi-Cure® ranges serve hydraulic fluids and low-VOC paints and coatings, while Agri-Pure® 315, launched during 2025 to 2026, delivers ultra-low pour points below −20°C for environmentally sensitive metalworking. Strategically, Cargill positions its fatty acid esters as drop-in replacements for petroleum-based fluids in North American industrial lubricants. The company also maintains leadership in food-grade esters, supplying essential emulsifiers and stabilizers for clean-label dairy and bakery products, reinforcing its dual strength across industrial and food and beverage ester markets.

KLK OLEO expands palm-based high-purity esters with RSPO and EUDR compliance

KLK OLEO, part of Kuala Lumpur Kepong Berhad, is a global specialist in palm-derived fatty acid esters for beauty, pharma, and specialty applications. In late 2025, KLK OLEO commissioned a 200 ktpa expansion in Zhangjiagang, China, strengthening its position in East Asia’s fast-growing personal care sector. Early 2026 saw the rollout of AI-powered quality control systems across global plants to ensure pharmaceutical-grade consistency. Its PALMERE ester portfolio is widely used as emollients and thickeners in luxury skincare. With strong RSPO alignment and readiness for EU Deforestation Regulation compliance, KLK OLEO remains a preferred supplier for sustainability-driven multinationals.

Croda International Plc targets pharma and nutraceutical growth with ultra-pure specialty esters

Croda International Plc positions itself as the sustainability architect of the fatty acid ester market, focusing on high-margin life sciences and beauty applications. Its Super Refined™ excipients include industry-leading Isopropyl Palmitate and Isopropyl Myristate grades for injectable drug formulations. In 2026, Croda launched a blockchain-enabled traceability platform, allowing pharmaceutical clients to verify ester origin and sustainability in real time. The company also differentiates through enzymatic synthesis, delivering higher-purity esters with superior sensory profiles versus traditional catalysis. Strategically, Croda is expanding into nutraceutical delivery systems, where its MCT oils act as carriers for lipid-based therapeutics and functional supplements.

China: Self-Sufficiency Drive and AI-Led Process Intensification

China’s fatty acid ester landscape is being reshaped by a policy-driven push toward chemical self-reliance and higher value-added output. In September 2025, the Ministry of Industry and Information Technology and six allied departments released a joint Work Plan targeting more than 5% annual growth in chemical added value through 2026. A central pillar of this roadmap is the acceleration of high-end fine chemicals, explicitly including advanced surfactants, specialty fatty acid esters, and bio-based polymers, with an ambitious target of achieving 90% domestic self-sufficiency. This policy signal has materially shifted capital allocation away from commodity oleochemicals toward precision esterification platforms capable of serving food processing, personal care, and performance materials.

On the industrial front, Wilmar International inaugurated a world-scale fatty acid ester manufacturing plant in China in July 2025, strengthening local supply for specialty fats and cosmetic-grade esters. Parallel to capacity expansion, Beijing’s AI + Petrochemical initiative is moving from pilot to deployment. Producers in Zhejiang and Jiangsu are integrating AI-driven process controls in 2026 to optimize esterification yields and reduce VOC emissions by an estimated 15%. Demand pull is also emerging from adjacent sectors. China’s lithium-ion battery chemical exports reached USD 69.1 billion in late 2025, stimulating localized production of high-purity polyol esters used in battery electrolytes and EV thermal management fluids. Collectively, these factors position China as both a volume and specification leader in fatty acid esters.

India: Bioenergy Incentives and Lubricant-Led Ester Upgrading

India’s fatty acid ester market is increasingly anchored in synthetic lubricants, bioenergy integration, and policy-supported capacity creation. In May 2024, Kluber Lubrication, part of the Freudenberg Group, announced a €15.6 million expansion of its Mysore manufacturing site. Reaching full operational scale during 2025–2026, the facility focuses on high-performance synthetic lubricants that rely on fatty acid esters as core base stocks for thermal stability and oxidation resistance. This expansion reflects a broader shift among Indian manufacturers toward ester-based formulations for industrial, automotive, and wind energy applications.

Policy support is reinforcing this transition. The Ministry of New and Renewable Energy extended Phase-I of the National Bioenergy Programme through March 2026, providing Central Financial Assistance for biomass-based chemical projects, including bio-derived esters. At the same time, the government’s advancement of the 20% ethanol blending target has generated large volumes of bio-derivative streams, catalyzing investment in Fatty Acid Methyl Ester refineries supported by capital subsidies of up to 30% for advanced waste-to-energy technologies. Multinational participation is also rising. Shell commissioned its first grease manufacturing plant in India in 2024, with commercial ramp-up in 2025. The facility produces Shell Gadus greases that rely heavily on complex ester technology, reinforcing India’s role as a regional hub for ester-based lubricant systems.

United States: High-Performance Ester Innovation for EVs and Life Sciences

In the United States, fatty acid ester development is being pulled by stringent performance requirements in lubricants, biopharma delivery systems, and electric mobility. In March 2025, BASF announced a major investment across its North American network to expand aminic antioxidant capacity. Scheduled for completion in 2026, this project supports the stability and oxidation resistance of long-life ester-based lubricating oils used in demanding industrial and automotive environments.

The life sciences sector is emerging as another growth vector. Croda International opened an advanced lipids manufacturing facility in Lamar, Pennsylvania, in March 2025. The site applies precision esterification to produce high-purity lipid delivery systems for biopharmaceutical formulations, underscoring the expanding role of fatty acid esters beyond traditional oleochemical uses. Innovation momentum was further highlighted at the 2025 Annual Meeting of the Society of Tribologists and Lubrication Engineers, where Emery Oleochemicals presented next-generation DEHYLUB® ester base stocks designed for EV fluids. These products target improved friction control and wear protection, with commercialization aligned to the 2026 automotive model year.

Germany: Pharmaceutical-Grade Esters and Low-Carbon Dispersions

Germany’s fatty acid ester market is evolving along two high-value axes: pharmaceutical excipients and low-carbon coating systems. In December 2025, Croda International entered a strategic supply partnership with Amino GmbH to strengthen its pharma-grade portfolio. This collaboration underpins the January 2026 launch of the BioXPro™ range, which uses ultra-high-purity fatty acid esters as stabilizing excipients for biologic drugs, a segment where consistency and impurity control are critical.

Sustainability-linked innovation is also accelerating. In October 2025, BASF started up a new production line for low-VOC, low-CO2 dispersions based on a Mass Balance approach. The facility enables the manufacture of esters with a significantly reduced carbon footprint, aligning with tightening European environmental standards and growing demand from the architectural coatings sector for lower-emission formulations.

Indonesia: Biodiesel Policy Tightening Ester Feedstock Dynamics

Indonesia’s fatty acid ester market is being directly reshaped by biofuel policy. The implementation of the B40 mandate, effective January 1, 2025, requires biodiesel to contain 40% palm oil content. This regulation has materially tightened the regional supply of palm-derived Fatty Acid Methyl Esters, creating competition between fuel blending and industrial ester applications. As a result, non-fuel ester producers are being pushed to diversify feedstocks, improve refining efficiency, or move up the value chain into specialty ester grades less exposed to biodiesel demand cycles. The Indonesian case illustrates how energy policy can rapidly alter the economics and strategic priorities of the broader fatty acid ester value chain.

Strategic Snapshot: Fatty Acid Ester Market by Country (2025–2026)

Fatty Acid Ester Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Industrial Focus

|

Market Implication

|

|

China

|

Chemical self-sufficiency and AI deployment

|

Specialty esters, EV and battery additives

|

Scale plus specification leadership

|

|

India

|

Bioenergy incentives and lubricant demand

|

Synthetic lubricants, FAME integration

|

Rapid upgrading from commodity esters

|

|

United States

|

Performance and purity requirements

|

EV fluids, biopharma lipid systems

|

Innovation-led margin expansion

|

|

Germany

|

Sustainability and pharma compliance

|

Low-carbon dispersions, excipients

|

Premium regulatory-aligned growth

|

|

Indonesia

|

Biodiesel mandate B40

|

Feedstock reallocation and efficiency

|

Structural pressure on industrial ester supply

|

Fatty Acid Ester Market Report Scope

Fatty Acid Ester Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$5 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Medium Chain Triglycerides, Glyceryl Monostearate, Isopropyl Esters, Polyol Esters, Sucrose Esters, Glycol Esters, Fatty Acid Methyl Esters), By Feedstock (Vegetable Oils, Animal Fats, Tall Oil and Distilled Fatty Acids), By Grade (Food Grade, Pharmaceutical Grade, Industrial Grade), By Application (Personal Care and Cosmetics, Food Processing, Lubricants and Greases, Pharmaceuticals, Surfactants and Detergents, Polymers and Plastics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Wilmar International Limited, Croda International Plc, Emery Oleochemicals LLC, KLK Oleo, Cargill, Incorporated, Evonik Industries AG, Stepan Company, Oleon NV, Indorama Ventures Public Company Limited, Gattefossé, Fine Organic Industries Limited, Godrej Industries Limited, Vantage Specialty Chemicals, Archer Daniels Midland Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fatty Acid Ester Market Segmentation

By Product Type

- Medium Chain Triglycerides

- Glyceryl Monostearate

- Isopropyl Esters

- Polyol Esters

- Sucrose Esters

- Glycol Esters

- Fatty Acid Methyl Esters

By Feedstock

- Vegetable Oils

- Animal Fats

- Tall Oil and Distilled Fatty Acids

By Grade

- Food Grade

- Pharmaceutical Grade

- Industrial Grade

By Application

- Personal Care and Cosmetics

- Food Processing

- Lubricants and Greases

- Pharmaceuticals

- Surfactants and Detergents

- Polymers and Plastics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fatty Acid Ester Industry

- BASF SE

- Wilmar International Limited

- Croda International Plc

- Emery Oleochemicals LLC

- KLK Oleo

- Cargill, Incorporated

- Evonik Industries AG

- Stepan Company

- Oleon NV

- Indorama Ventures Public Company Limited

- Gattefossé

- Fine Organic Industries Limited

- Godrej Industries Limited

- Vantage Specialty Chemicals

- Archer Daniels Midland Company

*- List not Exhaustive