Synthetic Lubricants Market 2025–2034: $47.3 Billion to $65.6 Billion at 3.7% CAGR Driven by EV Cooling Fluids, API SQ Upgrades, and Industrial Circular Models

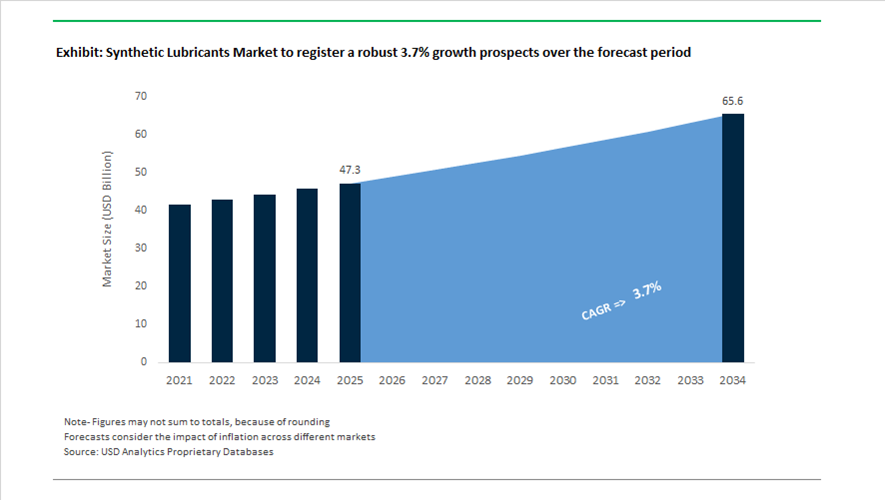

The global synthetic lubricants market is valued at $47.3 billion in 2025 and is projected to reach $65.6 billion by 2034, expanding at a CAGR of 3.7%. Growth is supported by rising demand for polyalphaolefin (PAO) oils, synthetic ester lubricants, Group III base oils, high-temperature greases, transformer fluids, EV battery immersion cooling fluids, and advanced industrial hydraulic oils. Regulatory tightening around fuel economy, lower viscosity engine oils, extended drain intervals, and electrification of mobility are driving innovation in low-viscosity synthetic engine oils and thermally stable dielectric fluids. OEM approvals tied to API SQ, ILSAC GF-7B, and JASO GLV2 standards are redefining performance benchmarks in passenger vehicles, heavy-duty fleets, renewable energy turbines, and data center cooling systems.

Portfolio expansion and strategic repositioning accelerated in 2024 and 2025. In January 2024, Shell completed the acquisition of the MIDEL and MIVOLT brands, strengthening its synthetic ester-based transformer and EV battery immersion cooling fluid portfolio. In March 2024, Shell Indonesia broke ground on a new grease plant in Bekasi to support high-performance synthetic grease demand across Southeast Asia’s industrial sector. In August 2024, Valvoline Global Operations became a certified Midas Immersion Cooling Technology Affiliate, validating its synthetic heat transfer fluids for data center immersion cooling applications. During 2024, Castrol launched its “Oil as a Service” circular model aimed at reusing and regenerating synthetic base oils for industrial clients. In late 2024, Shell upgraded its Helix Ultra range to meet the 2025 API SQ specification, utilizing gas-to-liquid PurePlus base oil technology for improved power retention and deposit control. In early 2025, SLB finalized its $7.7 billion acquisition of ChampionX, integrating specialty oilfield lubricants and production chemicals into its EOR-focused portfolio. In February 2025, Valvoline’s Restore & Protect synthetic motor oil received the 2025 Product of the Year award in the U.S. Car Care category for its engine deposit removal capability.

Capacity expansion and next-generation performance standards intensified in 2025 and 2026. Throughout 2025, ExxonMobil advanced construction of its 159,000 kiloliter-per-year lubricant manufacturing facility in India to meet rising domestic demand for premium synthetic oils across automotive and industrial segments. In Q3 2025, Castrol India reported 7% volume growth supported by rural retail expansion and increased penetration of synthetic fluids in construction and mining equipment. In January 2026, Petronas Lubricants International launched JASO GLV2-certified Syntium Supreme 0W-16 and 0W-20 formulations exceeding API SQ and ILSAC GF-7B standards, delivering up to 19% fuel savings in next-generation Japanese engines. In May 2024, TotalEnergies divested its stake in Engen Group, reallocating capital toward high-growth synthetic lubricant markets in Europe and Asia, particularly renewable energy and advanced mobility applications. These acquisitions, OEM-driven viscosity shifts, EV thermal management fluids, immersion cooling certifications, and circular base oil models are structurally shaping competitive dynamics in the synthetic lubricants market through 2034.

Strategic Trends and High-Impact Opportunities in the Synthetic Lubricants Market

OEM-Driven Shift to Ultra-Low Viscosity Fluids for EV Drivelines

The synthetic lubricants market is undergoing a structural shift as automotive OEMs redesign drivetrains around electric architectures rather than adapting legacy internal combustion platforms. Ultra-low viscosity synthetic fluids have become a mandatory specification for EV reduction gears, where rotational speeds often exceed 20,000 RPM and lubricants are required to perform dual roles as friction reducers and thermal management media. Unlike traditional gear oils, these fluids must maintain film strength under high torque while exhibiting excellent electrical compatibility with copper windings and permanent magnet motors.

OEM-specific formulation is now a critical differentiator. In April 2025, Ravenol introduced its EV-Synto product line, engineered specifically for dry and wet motor systems used by OEMs such as BMW, Tesla, Rivian, and Nio. These 70W and 75W synthetic fluids are optimized to manage high heat flux and shear stability in compact e-axles, enabling longer service intervals and reduced parasitic losses.

Thermal innovation has accelerated further as lubricants move beyond gears into direct battery cooling. In November 2025, Shell Lubricants disclosed that its EV-Plus Thermal Fluid, based on Gas-to-Liquids technology, successfully cooled an entire battery electric vehicle powertrain using a single-circuit immersion design. This architecture enables sub-10-minute fast charging from 10% to 80% by directly managing cell temperatures, translating thermal efficiency into measurable range gains per minute of charge. Such developments position synthetic lubricants as enablers of next-generation EV performance rather than passive consumables.

Strategic Adoption of Dielectric Immersion Fluids for AI Data Centers

Beyond mobility, synthetic lubricants are becoming mission-critical in digital infrastructure. The rapid expansion of artificial intelligence and high-performance computing workloads has pushed rack power densities beyond the limits of air cooling, with many hyperscale facilities now exceeding 100 kW per rack. As a result, data center operators are adopting single-phase immersion cooling, fully submerging servers in high-purity synthetic dielectric fluids to maintain thermal stability and operational reliability.

Validation and certification have emerged as key market gates. In May 2025, Shell became the first lubricant supplier to receive official immersion-cooling certification from Intel, confirming that processors operating in synthetic dielectric fluids deliver reliability equivalent to air-cooled systems. Field data demonstrated energy consumption reductions of up to 48% alongside an 80% decrease in required floor space, fundamentally reshaping the economics of hyperscale expansion.

The strategic importance of this transition is underscored by macro-energy dynamics. According to the International Energy Agency, data center electricity demand is projected to rise from 415 TWh in 2024 to 945 TWh by 2030. With cooling accounting for 30–40% of total power consumption, immersion cooling using synthetic dielectric fluids is no longer optional for operators pursuing net-zero commitments. This trend is locking in long-term demand for high-purity synthetic base fluids engineered for thermal conductivity, oxidation resistance, and ultra-low electrical conductivity.

High-Performance Synthetic Greases for Harsh EV Operating Cycles

Electric vehicles introduce a fundamentally different stress profile for auxiliary components such as wheel bearings, actuators, and steering systems. Regenerative braking and sustained high-speed motor operation generate continuous thermal cycling and stray electrical currents that accelerate grease degradation. This has created a high-growth opportunity for polyurea and lithium-complex synthetic greases formulated on PAO base stocks.

Independent research published in December 2025 confirmed that conventional mineral greases exhibit poor thermal endurance in EV motor environments, leading to premature bearing failure. In contrast, advanced PAO-based polyurea greases demonstrated superior electrical insulation and heat resistance, reducing surface pitting and scuffing by up to 70% under electrically induced loads.

Material science innovation is further expanding this opportunity. Studies referenced by the National Institutes of Health in 2025 showed that incorporating graphene and alumina nanoparticles into synthetic biolubricants reduced friction coefficients by 34% and wear rates by 30% at elevated temperatures. These performance gains support OEM strategies for sealed, fill-for-life lubrication in premium EV platforms, where reliability and low maintenance are core value propositions.

Synthetic Environmentally Acceptable Lubricants for Offshore Wind Infrastructure

The rapid build-out of offshore wind capacity is generating a structurally attractive market for synthetic environmentally acceptable lubricants. Regulatory frameworks governing oil-to-sea interfaces require lubricants that meet strict biodegradability and toxicity thresholds without sacrificing performance under high loads and corrosive marine conditions. Synthetic esters have emerged as the preferred solution, offering compliance with environmental mandates while delivering long service life.

Under the U.S. EPA’s Vessel General Permit, compliance reporting for 2024 operations was due by February 28, 2025, reinforcing strict enforcement of EAL usage across offshore assets. This regulatory environment is compelling wind farm operators associated with large projects such as SouthCoast Wind and Revolution Wind to specify synthetic ester-based EALs for hydraulic pitch systems, yaw drives, and stern tubes to mitigate regulatory and financial risk.

Operational economics further strengthen the opportunity. Modern synthetic ester EALs now achieve service intervals comparable to mineral oils, frequently exceeding 5,000 to 10,000 operating hours. For offshore wind farms, where maintenance interventions can cost more than $50,000 per turbine per day due to specialized vessel logistics, lubricant longevity directly translates into lifecycle cost savings. As offshore wind scales globally, synthetic EALs are becoming a core component of asset reliability strategies rather than a regulatory afterthought.

Synthetic Lubricants Market Share and Segmentation Insights

Group III Base Oils Lead Synthetic Lubricants Market with Cost-Performance Optimization

Group III base oils accounted for 48.60% of the synthetic lubricants market in 2025, driven by their strong balance of performance characteristics, cost efficiency, and scalability in automotive and industrial lubrication. These highly refined base oils deliver high viscosity index, oxidation stability, and low volatility, making them suitable for engine oils, hydraulic fluids, and industrial lubricants. Their cost advantage over Group IV and Group V synthetics supports widespread adoption in mass-market formulations. The 2025 market trend highlights the growing impact of gas-to-liquid (GTL) technology, where high-purity Group III+ base oils offer near-PAO performance, enabling premium lubricant formulations at competitive price points.

Automotive Sector Dominates Synthetic Lubricants Consumption with EV Fluid Innovation

Automotive accounted for 52.80% of synthetic lubricants market demand in 2025, reflecting high lubricant consumption across passenger vehicles, commercial fleets, and off-highway equipment. Synthetic lubricants are preferred for their ability to enhance fuel efficiency, extend drain intervals, and protect engines under extreme operating conditions. Increasing engine complexity and emission regulations further support synthetic lubricant adoption. The 2025 industry shift focuses on electric vehicle fluid innovation, where demand is rising for specialized transmission fluids, thermal management fluids, and greases designed for EV powertrains, battery cooling, and power electronics, creating new growth avenues within automotive lubrication.

Synthetic Lubricants Market Competitive Landscape

The synthetic lubricants market in 2026 is defined by dual-track innovation, combining decarbonized engine oils with rapid expansion into EV thermal management and data center cooling fluids. Key players are investing in re-refined base oils, biodegradable esters, and high-performance PAO formulations to meet stringent sustainability regulations.

ExxonMobil Scales Synthetic Basestock Leadership Through PAO Integration and Refinery Upgrades

ExxonMobil dominates the synthetic lubricants market through vertically integrated production of Group IV PAO and Group V ester basestocks. The company reported $28.8 billion in 2025 earnings and achieved $15.1 billion in structural cost savings, targeting $20 billion by 2030. Its $27–$29 billion 2026 capex supports advantaged projects like the Singapore Resid Upgrade, enhancing synthetic distillate output. The Energy Products segment recorded nearly 80% earnings growth driven by refinery optimization and renewable diesel integration. ExxonMobil’s Mobil 1™ portfolio is being reformulated for ultra-low viscosity engine oils aligned with next-generation turbocharged engines. Its global scale ensures leadership in high-performance synthetic lubricant supply chains.

Shell Leads Global Lubricant Volumes with EV Thermal Fluids and Data Center Cooling Innovations

Shell remains the global leader in finished lubricants, focusing on EV and AI-driven thermal management solutions. The company retained its top supplier position for the 19th consecutive year in 2025. Its EV-Plus Thermal Fluids enable single-circuit cooling systems for EV powertrains, reducing system complexity and weight. Shell’s DLC Fluid S3 is a breakthrough for data center liquid cooling, gaining certification from major semiconductor players. The acquisition of Raj Petro Specialities strengthens its footprint in India’s high-growth synthetic lubricant market. Its “Powering Progress” strategy positions Shell at the center of electrification and digital infrastructure lubrication demand.

Castrol Accelerates EV Fluid Innovation Through Formula 1 Partnerships and Strategic Restructuring

Castrol is repositioning its synthetic lubricant business through a high-value partnership-driven model and corporate restructuring. BP’s decision to sell a majority stake in Castrol, valuing it above $10 billion, enhances its operational flexibility. The partnership with Audi’s 2026 Formula 1 program drives co-engineering of advanced engine oils and EV fluids under extreme performance conditions. Castrol ON product lines, including e-coolants and e-transmission fluids, target high-voltage EV architectures. Its PATH360 strategy focuses on reducing carbon intensity and plastic usage through circular feedstocks. The company continues to leverage motorsport innovation to accelerate commercial synthetic lubricant technologies.

FUCHS Expands Smart Lubrication Systems with AI Integration and E-Mobility Fluid Development

FUCHS is strengthening its position as the largest independent lubricant manufacturer through digitalization and specialty product expansion. The company reported €3.5 billion in 2025 revenue and targets €3.7 billion in 2026 with €450 million EBIT. Its partnership with KCF Technologies integrates AI-driven monitoring for predictive maintenance and optimized lubricant usage. The acquisition of IRMCO® enhances its portfolio in oil-free synthetic lubricants for metal-forming applications. FUCHS is also advancing e-mobility solutions through collaboration with E-Lyte Innovations, focusing on battery electrolytes and e-fluids. Its “Local for Local” model ensures strong regional supply chain responsiveness.

Chevron Strengthens Synthetic Base Oil Production Through Refining Excellence and GTL Feedstock Security

Chevron is leveraging its refining and upstream integration to expand high-quality synthetic base oil production. The company reported $12.3 billion in 2025 earnings with $33.9 billion in operating cash flow. Its $18–$19 billion 2026 capex includes $1 billion dedicated to low-carbon fuels and synthetic lubricant feedstocks. Chevron’s ISODEWAXING® and ISOFINISHING® technologies produce premium Group II and Group III+ base oils for high-performance lubricants. Record refinery throughput in the U.S. supports consistent supply of synthetic basestocks. The Leviathan gas expansion ensures long-term feedstock availability for gas-to-liquid lubricant production.

United States Synthetic Lubricants Industry Anchored in Data Centers, Marine Compliance, and Carbon Pathways

The United States synthetic lubricants market is being structurally repositioned toward high-margin, low-carbon applications under the strategic realignment of ExxonMobil. Its 2030 Plan, announced in December 2025, elevates synthetic lubricants within the Product Solutions portfolio while advancing corporate GHG intensity reductions targeted for completion by late 2026. This shift is reinforced by infrastructure upgrades at Geismar, Louisiana, where Linde and ExxonMobil expanded access to high-purity polyalphaolefin precursors, improving supply security for heavy-duty engine oils and industrial synthetics.

Demand-side momentum is increasingly technology-driven. In June 2025, Shell launched Shell DLC Fluid S3 in Houston, addressing the thermal density requirements of AI-driven data centers through direct liquid cooling. Parallel regulatory pressure from Environmental Protection Agency has accelerated fleet-level adoption of environmentally acceptable lubricants, particularly 100% synthetic esters for marine and sensitive ecosystems. Additive innovation from Chevron Oronite now enables re-refined base oil integration without compromising extreme-pressure performance, while U.S. Department of Energy funding has catalyzed pilots converting captured carbon into aerospace-grade synthetic lubricants.

Germany Synthetic Lubricants Industry Defined by OEM Harmonization and PFAS-Free Innovation

Germany’s synthetic lubricants landscape is characterized by formulation harmonization and advanced manufacturing compliance. In November 2025, FUCHS introduced TITAN GT1 FLEX DE SAE 5W-30, a unified synthetic oil meeting specifications of BMW, Mercedes-Benz, Opel, and Volkswagen. This consolidation simplifies aftermarket complexity while strengthening supplier leverage with OEMs. Semiconductor manufacturing has emerged as a parallel demand vector, highlighted by FUCHS’ ECOCOOL SCS-IDM receiving ASML Grade 2 approval in August 2025 for ultra-precision processes.

Regulatory anticipation is reshaping R&D priorities. With the European Chemicals Agency expected to issue its PFAS opinion in March 2026, German producers are rapidly transitioning to PFAS-free greases and high-temperature synthetics. Process innovation is also accelerating, as German research institutes and Klüber Lubrication scaled supercritical CO2 extraction for synthetic ester production in 2025, eliminating solvent waste. Strategic energy linkages are emerging through Idemitsu Kosan’s investment in INERATEC, integrating e-fuels and synthetic waxes into Germany’s broader decarbonization ecosystem.

India Synthetic Lubricants Industry Scaling Through Defense, Offshore, and PLI Support

India’s synthetic lubricants market is expanding through application-led localization and policy-backed capacity creation. In June 2024, Castrol India, a subsidiary of BP, launched the EDGE Stay Ahead range to meet stringent API and ACEA requirements for SUVs and premium vehicles. Offshore energy operations are driving additional demand, with ONGC deploying synthetic-based drilling fluids in late 2025 for deepwater projects in the Krishna Godavari basin, where thermal stability is critical.

Institutional investment is reinforcing domestic capability. Indian Oil Corporation upgraded its Faridabad R&D center in 2025 to prioritize synthetic aviation lubricants and Group IV PAO fluids for defense applications. The Government of India’s PLI scheme for specialty chemicals continues to subsidize blending plants for fire-resistant hydraulic fluids used in mining and steel, reducing import reliance while anchoring India’s role as a regional supplier of high-performance synthetics.

Japan Synthetic Lubricants Industry Converging EV Thermal Management and AI Manufacturing

Japan’s synthetic lubricants market is aligning closely with electrification and advanced manufacturing. In May 2025, Idemitsu Kosan announced integration plans linking solid electrolytes for next-generation EV batteries with specialized synthetic thermal management fluids developed in 2025. This convergence reflects Japan’s emphasis on system-level efficiency rather than component-level optimization.

Thermal integration breakthroughs are reinforcing this approach. In November 2025, Shell demonstrated an all-in-one EV-Plus Thermal Fluid capable of cooling an entire battery electric powertrain with a single fluid, reducing weight and system complexity for OEMs. Manufacturing modernization is also evident, as ENEOS commissioned an AI-controlled blending facility in Yokohama in 2025 to produce ultra-low-viscosity synthetic transmission fluids for the 2026 hybrid vehicle cycle.

Canada Synthetic Lubricants Industry Pivoting Toward Full Synthetic Adoption

Canada’s synthetic lubricants market is undergoing a deliberate portfolio transition led by TotalEnergies. In April 2025, TotalEnergies Marketing Canada announced a shift away from mineral-based offerings, launching Quartz 7000 and Rubia Optima 1300 synthetic ranges for North American consumers. This move reflects tightening performance expectations in cold-climate operations and growing alignment with OEM fuel economy and emissions targets, positioning Canada as a stable demand base for premium synthetic technologies.

Comparative Snapshot: Synthetic Lubricants Industry by Country

Synthetic Lubricants Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Technology Focus

|

Structural Outcome

|

|

United States

|

AI data centers, marine compliance

|

PAO expansion, DLC fluids, carbon-derived synthetics

|

Margin expansion through advanced applications

|

|

Germany

|

OEM harmonization, PFAS regulation

|

Unified formulations, PFAS-free esters

|

Compliance-led innovation leadership

|

|

India

|

Defense, offshore E&P, PLI support

|

PAO localization, fire-resistant synthetics

|

Import substitution and regional supply growth

|

|

Japan

|

EV and hybrid systems

|

Single-fluid thermal management, AI blending

|

System-level efficiency leadership

|

|

Canada

|

Cold-climate performance

|

Full synthetic engine oils

|

Premiumization of consumer market

|

Synthetic Lubricants Market Report Scope

Synthetic Lubricants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$47.3 Billion

|

|

Market Size (2034)

|

$65.6 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Base Oil Group (Group III, Group IV, Group V), By Product Type (Engine Oils, Transmission and Hydraulic Fluids, Metalworking Fluids, Turbine and Compressor Oils, Thermal Management Fluids, Greases), By End-Use Industry (Automotive, Aerospace and Defense, Industrial Machinery, Energy and Power, Information Technology)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Exxon Mobil Corporation, Shell plc, BP p.l.c., Chevron Corporation, TotalEnergies SE, FUCHS SE, Idemitsu Kosan Co., Ltd., Petronas Lubricants International, Valvoline Global Operations, ENEOS Corporation, Sinopec, Indian Oil Corporation Limited, Phillips 66, Quaker Houghton, Amsoil Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Synthetic Lubricants Market Segmentation

By Base Oil Group

- Group III

- Group IV

- Group V

By Product Type

- Engine Oils

- Transmission and Hydraulic Fluids

- Metalworking Fluids

- Turbine and Compressor Oils

- Thermal Management Fluids

- Greases

By End-Use Industry

- Automotive

- Aerospace and Defense

- Industrial Machinery

- Energy and Power

- Information Technology

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Synthetic Lubricants Industry

- Exxon Mobil Corporation

- Shell plc

- BP p.l.c.

- Chevron Corporation

- TotalEnergies SE

- FUCHS SE

- Idemitsu Kosan Co., Ltd.

- Petronas Lubricants International

- Valvoline Global Operations

- ENEOS Corporation

- Sinopec

- Indian Oil Corporation Limited

- Phillips 66

- Quaker Houghton

- Amsoil Inc.

*- List not Exhaustive