Market Overview: Battery Electrolyte Market Value Expansion and Gigafactory-Driven Demand Acceleration

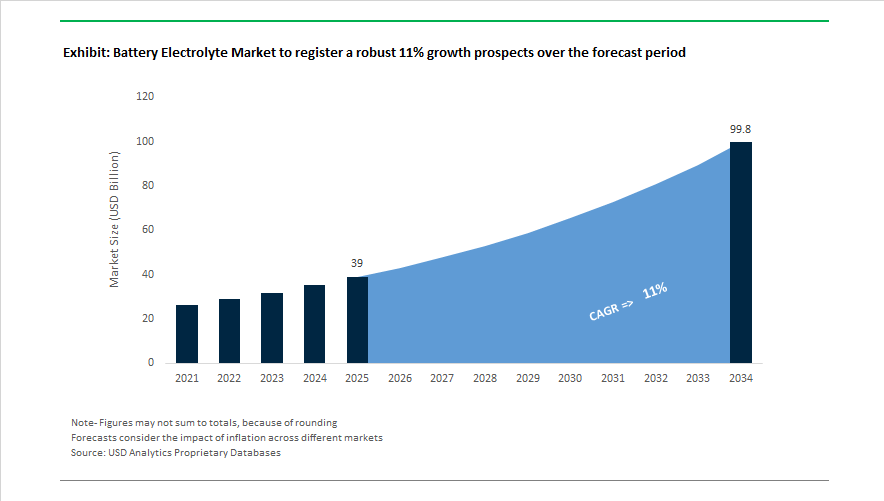

The battery electrolyte market is scaling in direct alignment with global lithium-ion battery manufacturing capacity additions and the parallel emergence of solid-state and sodium-ion chemistries. Market value is projected to increase from USD 39 billion in 2025 to USD 99.8 billion by 2034, representing a CAGR of 11% . Electrolytes have evolved from a commoditized chemical input into a performance-critical material influencing cycle life, thermal stability, fast charging capability, and safety compliance in EV batteries and stationary energy storage systems. Supply chain localization and production scale are central industry themes. In February 2025, UBE Corporation began construction of a large-scale dimethyl carbonate and ethyl methyl carbonate solvent facility in Louisiana, establishing the first significant U.S. domestic source of these electrolyte solvents, with operations expected by 2027. Capacity reinforcement continued across 2024 and 2025 as BASF expanded lithium hexafluorophosphate production in Germany by 50% through a €100 million investment to support European cell manufacturing. In late 2025, Soulbrain MI activated its Kokomo, Indiana site to supply high-purity electrolytes to the Stellantis and Samsung SDI joint venture battery plant, strengthening Tier 1 integration into U.S. gigafactory ecosystems.

Strategic contracts and aggressive international expansion define competitive momentum in 2025 and early 2026. In December 2025, Enchem secured a five-year agreement with CATL covering 350,000 tonnes of electrolyte supply between 2026 and 2030, the largest single-customer contract in its history. In January 2026, Enchem unveiled a roadmap targeting 1 million tonnes of global electrolyte production by 2030, supported by ongoing negotiations in North America and Europe. Capacity localization in the United States intensified in December 2025 when Orbia completed a Madison, Wisconsin expansion tripling electrolyte output through installation of advanced mixing systems, reducing reliance on Asian imports. Shenzhen Capchem advanced its global footprint in October 2025, confirming its Ohio plant timeline for 2027 while its Polish facility reached 40,000 tonnes annual output to serve European OEMs. In parallel, Capchem evaluated a $350 million solvent and electrolyte complex in Louisiana in late 2025, which would become the largest electrolyte facility in the U.S. if realized.

Technology diversification is reshaping electrolyte chemistry innovation. In October 2024, Idemitsu Kosan and Toyota initiated scale-up of sulfide-based solid electrolytes, supporting limited-run solid-state battery vehicles expected around 2027. Sodium-ion electrolyte commercialization advanced in 2025 as manufacturers in China and Europe deployed non-flammable sodium systems optimized for cold climates and cost-sensitive EV segments. Safety-focused formulations also gained traction. In late 2024, Volt Carbon Technologies partnered with Charge CCCV to supply non-flammable electrolytes for energy storage systems. Market concentration remains high. Tinci Materials shipped 301,000 tonnes of electrolyte in 2025 with 32% year-on-year growth, reinforcing the dominant 86.4% share held by Chinese suppliers as of Q3 2025.

Trends and Opportunities Redefining the Battery Electrolyte Market

Market Trend: Localization and "Fenceline" Electrolyte Manufacturing Near Gigafactories

The industry is undergoing a radical reshaping of electrolyte supply chains. Instead of importing pre-mixed electrolyte blends from Asia, producers are now colocating production next to EV battery gigafactories to align with tax credit incentives, mitigate logistics risks, and eliminate degradation during transport.

Green Energy Origin (GEO) is rapidly becoming a Western equities-backed electrolyte powerhouse. In December 2025, GEO acquired Mitsubishi Chemical Corporation’s electrolyte assets in the United States and the United Kingdom, including the fully operational Memphis, Tennessee facility. This acquisition enables GEO to deliver direct-to-line electrolyte replenishment within hours for the U.S. Midwest EV hub, bypassing two to three years of greenfield construction delays.

Meanwhile, Enchem’s repositioning underscores the shift toward “cluster economics.” Instead of building speculative new projects, the company abandoned its $142 million Tennessee plan in October 2025 and redirected investment into existing Georgia and Indiana hubs supplying LG Energy Solution and Samsung SDI. In Europe, GEO’s 200,000-ton Czech plant commissioned in 2024, combined with its newly acquired Billingham UK facility, sets a localized delivery time of four to six hours for most OEM partners—minimizing electrolyte “aging” and maintaining formulation purity prior to cell filling.

For industry strategists, this shift suggests that electrolyte qualification in 2026-2028 will increasingly be awarded to suppliers capable of just-in-time delivery within regional battery corridors.

Market Trend: LiFSI Incorporation as the New Benchmark for High-Voltage Systems

A structural technology transition is underway as LiPF6, long considered the “default” lithium-ion conducting salt, is being replaced by Lithium Bis(fluorosulfonyl)imide (LiFSI) to meet voltage, cycle-life, and ultra-fast-charging requirements.

Technical data validated in late 2025 shows that electrolytes with 20-30% LiFSI deliver 40% higher oxidative stability at voltages above 4.5V and increase cycle life by 30-50% at 60°C in nickel-rich systems such as NMC811. This stabilization at elevated temperature is becoming critical as pack-level power densities and charging currents rise. LiFSI-based blends also demonstrate approximately 50% lower lithium dendrite formation at 4C to 6C charging rates, a prerequisite for 10-minute rapid-charge EV targets.

Unlike LiPF6, which hydrolyzes readily to produce hydrofluoric acid, LiFSI is thermally stable up to 200°C and far more resistant to moisture intrusion. This allows cell manufacturers to reduce environmental humidity control overhead while maintaining electrolyte integrity—lowering both energy operating costs and equipment complexity in cell-filling lines.

Market Opportunity: Non-Flammable Electrolytes for Aviation Batteries and eVTOL Propulsion

Aviation electrification is elevating electrolyte safety requirements to a new regulatory tier. For eVTOLs and aerospace applications, electrolytes must comply with UL 9540A (5th Edition, March 2025), which now includes more rigorous cell-level and system-level flame propagation testing.

Localized High-Concentration Electrolytes (LHCE) and dual-salt systems blending LiPF6 + LiTFSI or LiPF6 + LiFSI are demonstrating potential for “non-flammable vent gas” behavior—an emerging procurement requirement for aviation and residential energy storage OEMs.

High-flash-point fluorinated solvent blends are being qualified for eVTOL batteries, increasing flash points from ~25°C (typical carbonate electrolytes) to above 100°C. This ensures that a single cell failure does not cascade into pack-level thermal runaway, a core prerequisite for FAA and DO-160 flight certification.

For specialty chemical suppliers, this segment offers one of the market’s highest margin pools due to low-volume high-performance needs, controlled approval cycles, and long-term aerospace contracts.

Market Opportunity: Electrolyte Formulations for 20-Year Grid Storage and Long-Duration ESS

Utility-scale battery storage has completely different operating economics than EV systems. The priority is not volumetric capacity but cycle life and cost per megawatt-hour over a 20-year period. Electrolyte innovation is therefore targeting LFP and emerging aqueous zinc-ion chemistries.

A zinc-ion breakthrough published in June 2025 by the University of Technology Sydney and the University of Manchester demonstrated that a tailored superlattice cathode paired with a specialized electrolyte surpassed 5,000 cycles—representing a 50% increase versus 2024 benchmarks. This opens a credible pathway to low-cost, non-flammable alternatives to lithium-ion for grid-connected storage.

LFP degradation management is another commercial design frontier. Field performance data from large-format LFP systems installed in 2025 suggests usable capacity declines by 2-3% annually. Advanced electrolyte additives engineered to continuously repair the SEI layer are now being evaluated to push LFP past 10,000 cycles, enabling Long-Duration Energy Storage (LDES) deployments aligned with renewable grid stability and peak-shifting requirements.

Battery Electrolyte Market Share and Segmentation Insights

Market Share by Chemistry: Lithium-Ion Electrolytes Anchor Volume While Sodium-Ion Emerges as a Cost Disruptor

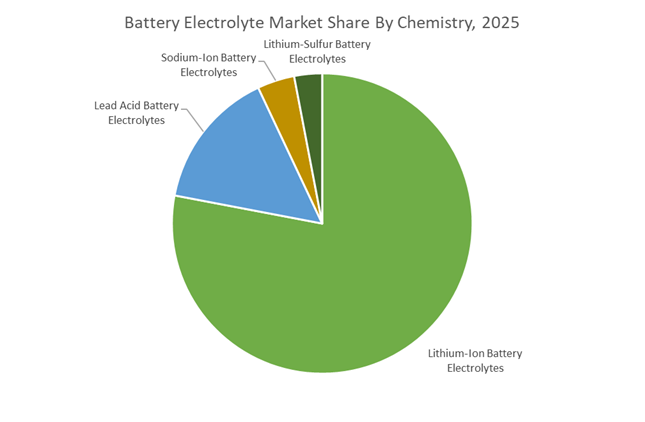

Lithium-ion battery electrolytes dominate the Battery Electrolyte Market with a commanding 78% share in 2025, reflecting their central role in electric vehicles, consumer electronics, and grid-scale storage. Growth is increasingly tied to high-nickel cathodes and silicon anodes, accelerating demand for advanced formulations such as LiPF6 in mixed carbonate solvents, supported by performance additives that enhance voltage stability and SEI layer optimization. Lead-acid battery electrolytes remain relevant in SLI automotive, backup power, and low-cost motive applications, but the segment faces structural decline due to EV penetration and tightening environmental regulations. Sodium-ion battery electrolytes are gaining commercial traction as a geopolitically secure, low-cost alternative, with China leading deployments in stationary storage and low-speed EVs. Lithium-sulfur electrolytes remain largely in R&D, targeting ultra-high energy density, with early adoption concentrated in aerospace despite challenges around polysulfide shuttling and anode corrosion.

Market Share by Application: Electric Vehicles Drive Electrolyte Performance Upgrades at Scale

Electric vehicles represent the largest application segment, capturing 58% of battery electrolyte demand in 2025, positioning EV electrification as the primary growth engine for advanced electrolyte technologies. OEMs and cell manufacturers are prioritizing formulations that enable fast charging, high-voltage operation, and enhanced safety, including non-flammable systems and pathways toward solid-state electrolytes. Consumer electronics continues as a mature but stable market, where electrolyte design focuses on maximizing energy density and cycle life within compact device architectures. Energy Storage Systems are emerging as a high-growth segment, driven by renewable integration and long-duration storage needs, pushing adoption of electrolytes capable of supporting extended cycle life beyond 8,000 cycles while lowering cost per kWh, with sodium-ion gaining momentum here. Industrial and motive power applications, including forklifts and AGVs, are steadily transitioning from lead-acid to lithium-ion, requiring electrolytes optimized for high discharge rates and rugged operating environments.

Competitive Landscape Analysis of the Battery Electrolyte Market

The battery electrolyte market is undergoing rapid structural transformation as suppliers race to support high-voltage EV platforms, solid-state battery development, and ultra-fast charging architectures. Competition is centered on high-purity carbonate solvents, advanced lithium salts, functional additives, and interface-engineered electrolyte systems that improve cycle life, suppress side reactions, and enhance safety. Leading players are shifting toward vertically integrated production models, strategic licensing partnerships, and global capacity expansions across APAC, North America, and Europe. Sustainability initiatives such as electrolyte recycling, low-moisture processing, and ESG-driven solvent manufacturing are also becoming decisive differentiators as OEMs demand compliant, high-performance electrolyte chemistries for next-generation electric mobility.

Mitsubishi Chemical Group advances high-purity electrolytes through functional additive innovation

Mitsubishi Chemical Group positions itself as a high-end technology leader in battery electrolytes, specializing in proprietary additives that suppress side reactions in automotive-grade lithium-ion cells. Its Sol-Rite formulated electrolytes enhance cycle life and high-power output across extreme temperatures for xEV platforms. In March 2026, the company is set to transfer its US and UK electrolyte assets to Green E Origin, signaling a strategic pivot toward technology licensing while retaining manufacturing strength in Japan and China. Mitsubishi’s core advantage lies in ultra-high-purity ethylene carbonate production, minimizing hydrofluoric acid formation. The company also integrates graphite-based anode materials pre-optimized for its electrolyte systems.

Shenzhen Capchem Technology accelerates global expansion with next-generation electrolyte platforms

Shenzhen Capchem Technology enters 2026 as one of the most aggressive global expanders in battery electrolytes, evolving from a Chinese leader into a full-spectrum international supplier. The company is developing major production bases in Ohio and Louisiana, while its Polish facility now anchors European OEM supply and its Malaysian plant marks Southeast Asia entry. Capchem unveiled next-generation solid-state electrolyte solutions addressing interface resistance at major battery exhibitions during 2025 and 2026. Its portfolio dominates supercapacitors and high-voltage lithium-ion batteries, extending into aerospace-grade primary lithium systems. Capchem’s GROW ESG framework emphasizes hazardous waste reduction in lithium salt and solvent production.

UBE Corporation strengthens electrolyte solvent purity through C1 chemistry integration

UBE Corporation stands out as the industry’s C1 chemistry specialist, vertically integrating solvent production critical to electrolyte performance. The company is building a large Louisiana facility scheduled for operation in fiscal 2026, positioning UBE as the sole domestic US supplier of high-purity dimethyl carbonate and ethyl methyl carbonate. Its POWERLYTE functional electrolytes deliver superior purity for overcharge protection and safety enhancement. UBE recently combined urethane systems with coating technologies to develop hybrid electrolyte-separator solutions for advanced industrial applications. Unlike competitors, UBE produces solvents directly from carbon monoxide and methanol, eliminating by-products and ensuring exceptional chemical stability.

Enchem scales electrolyte supply through landmark EV contracts and solid-state R&D

Enchem has rapidly risen to the top tier of electrolyte suppliers through long-term agreements with global battery leaders. In late 2025, it secured a five-year order from CATL valued at approximately 1 billion dollars, supplying seventy thousand tonnes of electrolyte annually from 2026 onward. Through its TDL subsidiary, Enchem verified oxide-based solid-state electrolyte materials targeting lightweight robotics and drone applications. The company is a key partner to LG, SK On, Samsung SDI, AESC, and SVOLT, supporting 800V fast-charging architectures. Its strategic focus centers on process reproducibility for composite electrolytes, accelerating solid-state commercialization.

Guangzhou Tinci Materials Technology dominates LiPF6 supply through unmatched production scale

Guangzhou Tinci Materials Technology is the global volume leader in lithium hexafluorophosphate, the core salt in most liquid electrolytes. Its vertically integrated control over LiPF6 and hydrofluoric acid enables cost leadership, particularly for large-scale lithium iron phosphate battery projects. In 2026, Tinci is expanding liquid LiPF6 output to support automated electrolyte blending lines, while targeting production capacity above 270,000 tonnes by 2028. The company is also investing in electrolyte recovery and recycling technologies to close the loop on lithium salt waste from spent EV batteries, reinforcing its role as a foundational supplier to the global electrolyte value chain.

BASF Shanshan Battery Materials integrates cathode-electrolyte synergy for next-generation batteries

BASF Shanshan Battery Materials uniquely bridges European chemical engineering with Chinese manufacturing scale. In late 2025 and early 2026, the joint venture delivered its first mass-produced cathode active materials for semi-solid-state batteries to Beijing WELION New Energy. Its 2026 strategy emphasizes interface synergy between high-nickel NCM cathodes and specialized electrolytes, using composite coating layers to suppress degradation reactions. The company offers ready-to-use electrolyte systems pre-tested with BASF cathode precursors, significantly shortening R&D cycles. Through its research institute, BASF Shanshan is advancing sodium-ion electrolytes and lithium-rich manganese chemistries to support affordable urban EV platforms.

United States Battery Electrolyte Market: Inland Capacity Build-Out and FEOC-Compliant Supply Chains

The United States battery electrolyte industry is pivoting toward inland manufacturing, localized Tier-1 supply, and compliance-driven funding structures. A central development is the execution of Phase I of Capchem USA’s USD 75 million advanced battery chemicals base in Lawrence County, Ohio. Scheduled for startup in the second quarter of 2026, the facility is designed for an annual output of 100,000 tons of electrolyte materials, signaling a decisive shift from import reliance to domestic scale for lithium-ion electrolyte production. This inland siting strategy improves logistics resilience and aligns with regional gigafactory clustering in the Midwest.

Federal policy is accelerating this localization. In August 2025, the United States Department of Energy launched a USD 500 million funding program under IIJA Section 40207, prioritizing commercial-scale battery materials processing projects that commit to avoiding Foreign Entities of Concern. This framework has become a gating criterion for capital access and long-term offtake agreements. Tier-1 localization is advancing in parallel. soulbrain MI, a subsidiary of Soulbrain Holdings, is finalizing a USD 75 million electrolyte manufacturing hub in Kokomo, Indiana, expected to be fully operational by late 2025 or early 2026 to supply nearby Stellantis and Samsung SDI gigafactories. Portfolio rationalization is also reshaping the market. In December 2025, Mitsubishi Chemical America agreed to transfer its U.S. and U.K. electrolyte manufacturing assets to Green E Origin by March 31, 2026, indicating a strategic retreat from high-volume commodity electrolytes in favor of specialized R&D in Western markets.

China Battery Electrolyte Market: Long-Term Offtake Security and Safety-Driven Electrolyte Innovation

China’s battery electrolyte industry continues to consolidate global supply through long-term offtake agreements and regulatory mandates that elevate safety performance. In December 2025, Enchem signed a five-year contract valued at approximately USD 1.03 billion to supply 350,000 metric tons of electrolytes between 2026 and 2030 to Contemporary Amperex Technology Co., Limited. This agreement underpins CATL’s global factory expansion and reinforces China’s role as the anchor market for large-scale electrolyte consumption tied to export-oriented cell production.

Regulatory tightening is reshaping formulation priorities. The Ministry of Industry and Information Technology announced revised safety standard GB38031-2025, effective July 1, 2026, which requires batteries to remain fire-free for two hours following a thermal event. Compliance with this mandate is accelerating adoption of advanced flame-retardant electrolyte additives and thermal stability enhancers across both liquid and hybrid electrolyte systems. Integrated chemical infrastructure supports rapid iteration. BASF is commissioning a new production line for controlled free radical polymerization dispersants at its Nanjing site in late 2025, enabling tighter control of electrolyte rheology, dispersion stability, and interfacial performance at industrial scale.

European Union (Germany and Poland) Battery Electrolyte Market: Traceability Mandates and Solid-State Transition

Germany and Poland sit at the center of the European Union’s regulatory and technological transition in battery electrolytes, driven by transparency requirements and early solid-state integration. Under the EU Battery Regulation, 2026 is the final preparation year for the Digital Battery Passport, which becomes mandatory in February 2027. Electrolyte manufacturers supplying the region must now provide granular disclosures on chemical composition, carbon footprint, and sourcing, embedding lifecycle accountability into procurement decisions across the value chain.

Technology pathways are also diverging from conventional liquid electrolytes. In February 2025, Mercedes-Benz, in collaboration with Factorial Energy, successfully integrated a solid-state battery into a production vehicle platform. This milestone marks a tangible shift toward sulfide and polymer-based solid electrolytes and signals future demand realignment for electrolyte suppliers. Circularity infrastructure is advancing in parallel. BASF inaugurated a prototype metal refinery in Schwarzheide, Germany in late 2024, enabling recovery of lithium and other electrolyte-associated minerals to support the EU’s recycled content requirements by 2031.

South Korea Battery Electrolyte Market: Strategic Technology Status and Sulfide Electrolyte Leadership

South Korea’s battery electrolyte industry is being propelled by national strategic designation and leadership in solid-state chemistries. In 2025, the government classified next-generation large-capacity EV electrolytes as a National Strategic Technology, unlocking tax credits and accelerated approvals for firms such as Soulbrain to develop formulations optimized for silicon-anode expansion control and fast-charging durability. This policy alignment is compressing development timelines and strengthening domestic IP positions.

Commercial leadership in solid-state electrolytes remains a differentiator. Samsung SDI maintained its lead through 2025 by advancing sulfide-based electrolyte systems that combine high ionic conductivity with sufficient deformability for thin, stable interfacial layers. These attributes are critical for scaling solid-state cells while maintaining manufacturing yields. Together, strategic designation and chemistry leadership position South Korea as a reference market for next-generation electrolyte performance and qualification.

Country-Level Strategic Snapshot: Battery Electrolyte Industry

Battery Electrolyte Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

United States

|

Inland capacity and FEOC compliance

|

Ohio electrolyte plant, IIJA funding, Indiana Tier-1 supply, portfolio divestment

|

|

China

|

Long-term offtake and safety reformulation

|

Enchem–CATL contract, GB38031-2025 safety mandate, Nanjing CFRP dispersants

|

|

EU (Germany/Poland)

|

Traceability and solid-state shift

|

Digital Battery Passport prep, production SSB integration, recycling refinery

|

|

South Korea

|

Strategic designation and sulfide leadership

|

National Strategic Technology status, silicon-anode optimization, sulfide electrolytes

|

Battery Electrolyte Market Report Scope

Battery Electrolyte Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$39 Billion

|

|

Market Size (2034)

|

$99.8 Billion

|

|

Market Growth Rate

|

11%

|

|

Segments

|

By State (Liquid Electrolytes, Solid Electrolytes, Gel Electrolytes), By Chemistry (Lithium Ion Battery Electrolytes, Lead Acid Battery Electrolytes, Sodium Ion Battery Electrolytes, Lithium Sulfur Battery Electrolytes), By Component (Lithium Salts, Solvents, Functional Additives), By Application (Electric Vehicles, Consumer Electronics, Energy Storage Systems, Industrial and Motive Power)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mitsubishi Chemical Group, Shenzhen Capchem Technology, Enchem, Tinci Materials, BASF, Soulbrain Holdings, Guotai Huarong, UBE Corporation, Mitsui Chemicals, Central Glass, Shanshan Technology, NEI Corporation, Factorial Energy, Solid Power, Gelest

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Battery Electrolyte Market Segmentation

By State

- Liquid Electrolytes

- Solid Electrolytes

- Gel Electrolytes

By Chemistry

- Lithium Ion Battery Electrolytes

- Lead Acid Battery Electrolytes

- Sodium Ion Battery Electrolytes

- Lithium Sulfur Battery Electrolytes

By Component

- Lithium Salts

- Solvents

- Functional Additives

By Application

- Electric Vehicles

- Consumer Electronics

- Energy Storage Systems

- Industrial and Motive Power

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Battery Electrolyte Industry

- Mitsubishi Chemical Group

- Shenzhen Capchem Technology

- Enchem

- Tinci Materials

- BASF

- Soulbrain Holdings

- Guotai Huarong

- UBE Corporation

- Mitsui Chemicals

- Central Glass

- Shanshan Technology

- NEI Corporation

- Factorial Energy

- Solid Power

- Gelest

*- List not Exhaustive