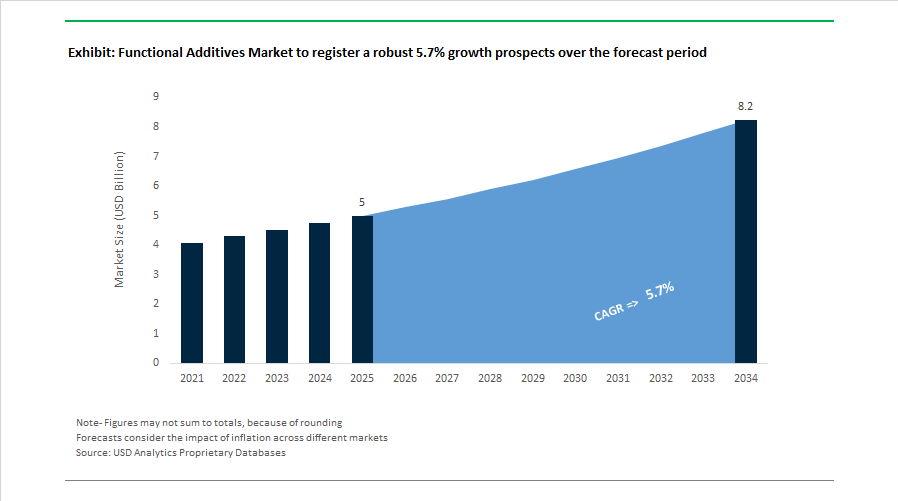

Functional Additives Market to Reach $8.2 Billion by 2034 at 5.7% CAGR Driven by Bio-Based Innovation and Performance Chemicals

The Functional Additives Market is projected to expand from $5.0 billion in 2025 to $8.2 billion by 2034, registering a CAGR of 5.7% over the forecast period. Growth is underpinned by accelerating demand for performance-enhancing additives across fuels, polymers, coatings, food ingredients, agricultural films, construction chemicals, and specialty materials. The market is evolving beyond conventional stabilizers and rheology modifiers toward bio-based additives, UV stabilizers, dispersions, enzymes, and fuel performance chemistries tailored to regulatory compliance and sustainability mandates.

In September 2025, BASF SE introduced its next-generation Keropur® gasoline performance additive series engineered to comply with the revised U.S. TOP TIER+™ detergent gasoline standard. The new Keropur AP 225-20 formulation, scheduled for commercial availability in early 2026, positions refiners and fuel marketers ahead of the 2027 compliance deadline. This launch highlights tightening fuel efficiency regulations and deposit control standards that are reshaping the fuel additives segment. In February 2026, BASF further strengthened its advanced materials portfolio through a partnership with Xfloat Ltd., integrating light stabilizer technologies into floating photovoltaic systems to extend plastic component durability beyond 30 years, signaling growing demand for UV-resistant functional additives in renewable energy infrastructure.

Sustainability and bio-based chemistry are central to competitive differentiation. In April 2025, Arkema S.A. launched bio-based acrylic thickeners under its Rheotech™, Thixol™, and Viscoatex™ brands, utilizing bio-sourced ethyl acrylate from its Carling facility in France. These additives enable high-performance rheology control in sustainable coatings and adhesives without cost penalties. During K 2025 in October 2025, Braskem S.A. unveiled a new I’m green™ bio-based EVA containing 21% vinyl acetate, offering enhanced softness and flexibility for footwear and consumer goods while maintaining renewable feedstock origins from sugarcane ethanol. In October 2025, researchers at Fraunhofer IGB presented Caramide, a fully bio-based polyamide derived from paper production by-products, targeting high-performance applications in mechanical components and medical-grade materials. These developments reflect structural migration toward renewable carbon content and circular material platforms across the functional additives ecosystem.

Portfolio consolidation and strategic acquisitions are redefining competitive scale. In October 2024, Tate & Lyle PLC completed the £1.48 billion acquisition of CP Kelco, significantly expanding its hydrocolloid and stabilizer capabilities for texture optimization in health-oriented food and beverage formulations. In April 2025, Godrej Industries Limited acquired the food additives business of Savannah Surfactants Limited, strengthening its emulsifier and specialty surfactant portfolio in functional food ingredients. In mid-2025, Methanex Corporation finalized the $2.05 billion acquisition of OCI Global’s international methanol division, securing upstream feedstock supply for a broad range of chemical additives. In February 2025, DSM-Firmenich divested its stake in the Feed Enzymes Alliance to Novonesis for $1.6 billion, reallocating capital toward human nutrition and life science-focused functional ingredients.

Regulatory shifts and regional capacity expansion continue to shape the market outlook. In July 2025, the U.S. Food and Drug Administration approved Gardenia Blue as a novel color additive for multiple food categories, reinforcing clean-label reformulation trends and accelerating the replacement of synthetic dyes with natural-origin functional additives. In February 2026, BASF expanded dispersions production at its Mangalore, India facility, targeting rising demand for performance additives in architectural coatings, construction chemicals, and paper processing across South Asia. At Plastindia 2026, BASF showcased its Tinuvin® NOR® stabilizer platform engineered for agricultural greenhouse films, enabling thinner plasticulture films with enhanced resistance to heat and agrochemical exposure.

Trends and Opportunities in the Global Functional Additives Market

Proliferation of Multi-Functional, Synergistic Additive Blends

To reduce formulation complexity, lower inventory costs, and improve processing consistency, manufacturers are increasingly adopting pre-optimized, synergistic additive systems that deliver multiple performance benefits through a single dosing step. This shift reflects a broader industry objective to minimize trial-and-error formulation while maintaining compliance with sustainability and durability requirements.

In August 2025, BASF highlighted the evolution of its VALERAS® portfolio, with a particular focus on Irgastab® multifunctional stabilizers. These systems combine oxidation resistance, thermal stabilization, and process protection, enabling higher recycled polymer content without sacrificing mechanical integrity or processing speed. For converters working with post-consumer recycled plastics, such blends directly support circularity targets while maintaining output efficiency.

Agricultural plastics represent another high-stress application accelerating demand for hardened additive packages. The introduction of Tinuvin® NOR® 211 AR in mid-2025 illustrates how synergistic heat and light stabilizers are being engineered to withstand aggressive agrochemical exposure, including sulfur- and chlorine-rich environments common in organic farming. These conditions typically degrade conventional single-function stabilizers, making multi-functional solutions essential for extending film service life.

Customization is also becoming a competitive differentiator. Clariant expanded its AddWorks™ platform in 2025 to deliver application-specific additive combinations in ready-to-use masterbatches. By reducing the average number of additives per formulation from five to one, these solutions lower total cost of ownership, simplify regulatory documentation, and improve batch-to-batch consistency for manufacturers operating at scale.

Regulatory-Driven Shift to Polymer-Immobilized and Non-Migratory Additives

Regulatory developments across Europe and Asia are accelerating a decisive shift toward polymer-immobilized and high-molecular-weight additives that eliminate migration risks. Compliance is increasingly tied not only to additive chemistry but also to its long-term behavior within polymer matrices, particularly in food contact and consumer-facing applications.

European Commission Regulation (EU) 2025/351, effective February 21, 2025, introduced stricter oversight of additive migration under Regulation (EU) No 10/2011. The update places heightened emphasis on recycled plastics, compelling the adoption of oligomeric antioxidants and high-molecular-weight stabilizers that remain physically locked within the polymer structure. This has accelerated innovation in non-migratory additive architectures designed to meet food safety requirements without compromising processing performance.

India is following a similar trajectory. In October 2025, the Ministry of Chemicals and Fertilizers issued a Second Amendment to the Polypropylene Quality Control Order, mandating compliance with updated Bureau of Indian Standards norms by April 2026. This is driving a nationwide transition toward higher-purity, standardized additives, particularly in packaging, household goods, and automotive interiors.

Reactive additive chemistries are also gaining traction. Irgastab® PUR 71, introduced during 2024–2025, exemplifies the move toward anti-scorch solutions for polyurethane systems that avoid aromatic amines. These next-generation antioxidants address rising substance classification pressures while delivering improved environmental, health, and safety profiles, particularly for automotive seating and furniture applications.

High-Temperature Functional Additives for EV Battery Packs and Power Electronics

Electrification is creating a premium, high-margin opportunity for functional additives capable of operating under extreme thermal, mechanical, and dielectric stress. As EV architectures migrate toward 800-volt systems, additive performance directly influences safety, reliability, and system lifespan.

In early 2025, Evonik Industries AG expanded its TEGO® Therm portfolio with fire-resistant coating technologies for EV battery housings. These waterborne polysiloxane hybrid systems withstand jet flame exposure approaching 1000°C for extended durations while maintaining low thermal conductivity, providing critical thermal runaway mitigation in densely packed battery modules.

Thermal interface materials are another focal point. Battery and e-axle assemblies increasingly require filler loadings above 80 weight percent to manage heat dissipation. Evonik’s ORTEGOL® DA 801 dispersant, launched in 2025, enables filler concentrations approaching 90 weight percent while reducing viscosity by more than an order of magnitude. This performance unlocks high-speed automated assembly without compromising thermal performance, directly supporting EV manufacturing scale-up.

High-voltage electrical insulation presents a parallel opportunity. Engineering plastics such as PEEK and PA12 are increasingly used for busbars and power electronics, creating demand for anti-tracking and arc-resistance additives that prevent electrical failure under high field strength. These additives are becoming essential as OEMs pursue faster charging and higher power density systems.

Active and Intelligent Packaging for Shelf-Life Extension

Functional additives are also playing a central role in the evolution of active and intelligent packaging, driven by global efforts to reduce food waste and protect temperature-sensitive pharmaceuticals. What was once a niche solution is rapidly becoming a baseline requirement across supply chains.

By 2025, demand for oxygen scavenging additives had accelerated sharply, with the segment approaching a market value of approximately 2.68 billion. Industry leaders are embedding scavenging chemistries directly into multilayer polymer structures, eliminating sachets and improving consumer safety while extending shelf life.

Biopolymer-based active packaging is gaining traction in parallel. Advances reported in November 2025 highlight the use of pullulan as a carrier for antimicrobial and antioxidant additives in fresh produce packaging. This approach aligns with clean-label expectations while serving the rapidly expanding organic food sector.

In global logistics, ethylene and carbon dioxide regulation represents a high-impact growth area. New ethylene scavenger formulations commercialized in 2025 enable controlled ripening during long-distance maritime transport, reducing port-side food waste by an estimated 15 to 20%. For packaging and additive suppliers, this positions functional additives as value-generating tools rather than cost inputs.

Functional Additives Market Share and Segmentation Insights

Polymer Stabilizers Lead Functional Additives Demand Through Protection Against Thermal and Environmental Degradation

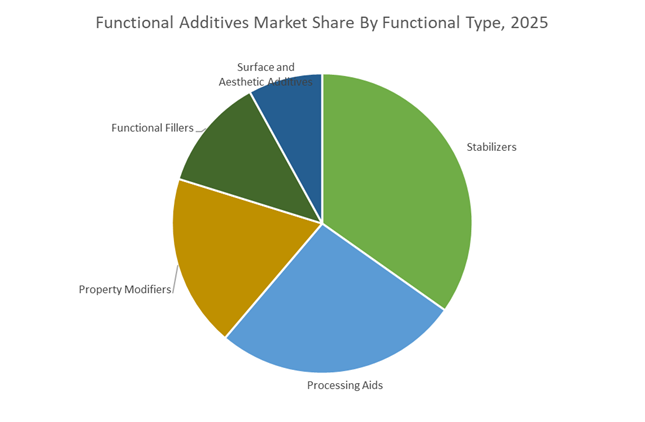

Stabilizers accounted for 34.80% of the Functional Additives Market share in 2025, making them the largest functional additive category used in polymer processing and product manufacturing. Stabilizers—including heat stabilizers, ultraviolet (UV) stabilizers, and antioxidants—play a critical role in preventing polymer degradation caused by heat, oxygen, and UV radiation during both processing and long-term product use. Without effective stabilization systems, polymers can suffer from discoloration, embrittlement, loss of mechanical properties, and premature product failure, making stabilizers essential across industries such as packaging, automotive components, construction materials, electrical cables, and consumer goods. In 2025, the stabilizer segment reflects a major industry-wide transition driven by environmental and regulatory pressure. Historically, lead-based stabilizers were widely used in PVC processing, particularly in applications such as pipes, window profiles, and cable insulation. However, global regulations restricting heavy metals have accelerated the adoption of lead-free stabilization systems based on calcium–zinc and organic stabilizer chemistries. These next-generation stabilizers are engineered for application-specific performance, delivering improved thermal stability, processing efficiency, and long-term durability while complying with strict environmental regulations. This transition has positioned stabilizers as a central component of innovation within the global functional additives market.

Packaging Industry Drives the Largest Demand for Functional Additives in Polymer Processing

Packaging represented 38.60% of the Functional Additives Market share in 2025, making it the dominant end-use industry for polymer additive technologies. Modern packaging systems rely heavily on plastic materials such as polyethylene, polypropylene, PET, and PVC, which require a range of functional additives to achieve desired performance characteristics. Stabilizers are used to protect polymers during processing and extend product shelf life, property modifiers enhance flexibility or rigidity, and surface additives improve printability, gloss, and aesthetic appearance for branded packaging applications. These additives enable packaging manufacturers to produce materials that meet the performance demands of food safety, durability, transparency, and mechanical strength. In 2025, the packaging sector is undergoing rapid transformation due to growing pressure to implement circular economy principles and sustainable packaging solutions. Functional additives are increasingly being redesigned to support recyclability and material recovery. Innovations include de-inking additives that enable easier label removal during recycling, stabilizers capable of maintaining polymer integrity through multiple reprocessing cycles, and tracer additives that allow automated sorting systems to identify specific plastic types.

Competitive Landscape in Functional Additives Market

BASF Strengthens Circular Additives and Cost Discipline Under Winning Ways

BASF SE remains the largest chemical producer globally, with its Nutrition & Care and Industrial Solutions segments driving functional additives innovation. Under its Winning Ways strategy, BASF projects 2026 EBITDA before special items between €6.2 billion and €7.0 billion, reinforcing disciplined capital allocation. In early 2025, BASF commissioned its first commercial loopamid® facility in Shanghai, enabling textile-to-textile recycling of polyamide 6 and positioning the company at the forefront of circular polymer additives. Despite ramping up the large-scale Zhanjiang Verbund site, BASF targets CO₂ emissions of 17.2 to 18.2 million metric tons in 2026. In February 2026, the company raised its annual cost savings target to €2.3 billion, enhancing competitiveness across industrial additives, performance chemicals, and sustainable polymer solutions.

Evonik Accelerates Specialty Additives Focus Through Portfolio Pruning

Evonik Industries AG is transforming into a pure-play specialty additives company by exiting its Performance Materials division, divesting approximately €350 million in sales with full financial impact expected from 2026 onward. The company continues to prioritize high-margin effects for coatings, adhesives, inks, and healthcare applications. In early 2026, Evonik launched TEGO® Dispers 695, a hyperdispersant for radiation-curing inks, and TEGO® Foamex 8051, a siloxane-based defoamer engineered for long-term stability. Expansion of a world-scale alkoxides plant in Singapore and a new aluminum specialty plant in Japan strengthens its Asian footprint. Evonik aims for more than 50% of group sales to come from Next Generation sustainable products by 2030, supported by a 2026 dividend policy targeting a 40 to 60% payout of adjusted net income.

Dow Targets EBITDA Expansion Through Operational Transformation

Dow Inc. continues to lead in materials science-driven functional additives for packaging, infrastructure, and consumer care. In January 2026, Dow introduced its Transform to Outperform initiative, targeting a $2 billion near-term operational EBITDA improvement through AI-enabled productivity and structural simplification. As part of this transformation, the company is implementing a workforce reduction of approximately 4,500 roles globally to modernize its commercial and customer support model. Dow remains a major supplier of optical materials, silicone-based additives, and high-performance surfactants that enhance durability, processability, and recyclability. The company is emphasizing circularity-enabling additives that allow plastic packaging and construction materials to meet evolving global recycling and sustainability standards.

Clariant Drives Margin Expansion Through Value-Focused Additives Strategy

Clariant AG continues to reposition itself as a focused specialty chemical supplier under its Greater Chemistry strategy. For 2026, the company projects an EBITDA margin of approximately 18%, supported by a CHF 80 million performance improvement program nearing completion. In early 2026, Clariant reported strongest growth in its Mining Solutions and Oil Services units, while its Adsorbents & Additives segment pursued value-over-volume pricing discipline. The company is targeting a 46.9% reduction in Scope 1 and Scope 2 emissions by 2030, with external agencies recognizing its innovation in sustainable additive chemistry. Confirmation of a stable CHF 0.42 per share distribution for 2026 reflects confidence in cash flow generation and disciplined capital management.

Lubrizol Expands Regional Manufacturing and Fluorine-Free Additives

Lubrizol Corporation, owned by Berkshire Hathaway, continues to expand its science-based specialty chemistry portfolio for mobility, packaging, and consumer applications. In January 2026, Lubrizol announced a multi-million-dollar upgrade of its Ohio headquarters, consolidating operations to enhance cross-functional innovation. The Shanghai Innovation Center launched PTFE-free Lanco™ Surface Modifiers in early 2026, responding to regulatory pressure on fluorinated materials in coatings and inks. Lubrizol is also broadening its Carbobond™ and Hycar® Acrylic Resins portfolio, targeting medical-grade packaging and sustainable food packaging applications. Its local-for-local manufacturing model in Asia strengthens supply reliability for regional formulators seeking compliant and high-performance functional resin technologies.

Songwon Strengthens Polymer Stabilizer Leadership and Middle East Presence

Songwon Industrial Group remains the world’s second-largest producer of polymer stabilizers and a significant supplier of specialty functional additives. For the fiscal year ending December 31, 2025, Songwon reported consolidated sales of 1,038,508 million KRW, reflecting resilient demand across PVC stabilizers and tin intermediates. In October 2025, the company announced a new One Pack Systems production facility in Saudi Arabia to serve Middle Eastern polymer markets more efficiently. Songwon earned its sixth EcoVadis Gold rating in December 2025, underscoring its sustainability leadership in chemical manufacturing. Its forward-oriented innovation strategy emphasizes environmentally compliant PVC stabilizers and next-generation polymer additives aligned with evolving global environmental safety regulations.

Germany: Mass-Balanced Chemistry and OEM-Grade Carbon Transparency

Germany is setting the benchmark for sustainable functional additives through mass-balance chemistry, digital lifecycle management, and renewable energy integration. In March 2025, Evonik Coating Additives launched TEGO Wet 270 eCO and TEGO Foamex 812 eCO, its first mass-balanced functional additives using ISCC PLUS certified bio-attributed feedstocks. These products deliver a 40 to 60% reduction in carbon footprint while maintaining performance in high-end coatings, aligning directly with German automotive and industrial OEM requirements for low-emission input materials.

Innovation visibility has also intensified ahead of K 2025 in Düsseldorf, where BASF highlighted circular plastics solutions under its VALERAS portfolio. Newly introduced Tinuvin NOR 112 light stabilizers are engineered for greenhouse films exposed to aggressive agrochemicals, supporting organic farming applications. From a systems perspective, Evonik’s rollout of automated life cycle assessment tools in September 2025 enables real-time Scope 3-ready carbon data at batch level. Coupled with the transition of German production sites for epoxy curing agents and rheology modifiers to 100% renewable electricity during 2025, Germany’s functional additives market is now defined by traceable, low-carbon, OEM-compliant supply.

China: Semiconductor-Led Demand and Scale-Up of Sustainable Additives

China’s functional additives market is advancing through policy-driven specialization and capacity expansion aligned with semiconductors, renewable energy, and low-VOC materials. In September 2025, the Ministry of Industry and Information Technology issued the Work Plan for Stabilizing Growth, targeting a 5% annual increase in chemical value-add while prioritizing high-end electronic chemicals and specialized polyolefin additives. This has redirected domestic investment toward CMP slurries and high-purity photoresist additives for 28-nanometer and below chip nodes under the AI plus petrochemicals initiative.

Multinationals are scaling alongside domestic players. In November 2025, Clariant completed an CHF 80 million expansion at Daya Bay, adding a second spray tower and increasing output of pharmaceutical excipients, ethylene oxide derivatives, and water-based coating surfactants to reduce VOC emissions. Innovation financing is also accelerating commercialization. Evonik and HosenCare launched the Jinjiang Houxin innovation fund in November 2025, targeting bio-based functional additives for Asian consumer goods. These developments position China as both a scale producer and a technology adopter in next-generation additives.

United States: Performance Standards, Biofuel Compatibility, and Circular Plastics

The United States functional additives market is being reshaped by stricter performance standards, regulatory compliance, and circular economy commitments. In September 2025, BASF introduced its next-generation Keropur gasoline performance additive series to meet the revised TOP TIER+ detergent gasoline standard. These additives address injector cleanliness in GDI engines ahead of the 2027 enforcement timeline, raising the bar for multifunctional additive performance.

Regulatory pressure is influencing formulation design. During 2025, manufacturers transitioned to ashless detergent platforms to meet the U.S. Environmental Protection Agency Lowest Additive Concentration requirements while remaining compatible with high-blend biofuels under the Renewable Fuel Standard. Feedstock sourcing is also shifting. As part of the U.S. Plastics Pact Roadmap, producers achieved a 2025 milestone of integrating an average 30% recycled or bio-based content into packaging-related functional additives. Cost structures adjusted accordingly when Dow implemented a price increase on PURAGUARD and industrial glycols in November 2025, resetting 2026 economics for coatings and personal care additives.

Japan: Regulatory Tightening and Battery-Centric Specialty Additives

Japan’s functional additives market is defined by regulatory precision and advanced materials for electronics and energy storage. In December 2025, the Ministry of Economy, Trade and Industry announced that PFHxS and related substances will be designated as Class I Specified Chemical Substances, with a full ban effective June 17, 2026. This decision is forcing rapid reformulation of surface treatment and semiconductor additives toward fluorine-free alternatives.

Food safety regulation is also shaping demand. From June 1, 2025, Japan’s Positive List system allows only 827 approved additives in food-contact plastics, tightening compliance for antioxidants, slip agents, and stabilizers. On the innovation front, BASF and Hagihara Industries completed a three-year R&D collaboration in April 2025, delivering UV-stable polyolefin yarns for artificial turf using Tinuvin grades. Energy storage applications are expanding through Evonik’s Alu5 facility in Yokkaichi, opened in late 2025, which produces aluminum oxide-based functional additives for lithium-ion battery separator coatings across the Asian EV supply chain.

India: Policy-Led Capacity Build-Up and Global Pigment Integration

India’s functional additives market is scaling rapidly through policy incentives, consolidation, and biofuel adoption. Under the 2025–26 Union Budget, the Ministry of Chemicals and Fertilizers received Rs. 1.62 lakh crore to accelerate Production Linked Incentive schemes. This support enabled first-time domestic production of specialty intermediates, generating Rs. 26,123 crore in sales and reducing import dependence for functional additives used in pharmaceuticals, coatings, and polymers.

Global integration accelerated in March 2025 when Sudarshan Chemical completed its acquisition of Germany’s Heubach Group, creating a global pigment and additive leader with 19 manufacturing sites. Fuel transition policies are adding further momentum. As India approached a 20% ethanol blend by mid-2025, demand surged for corrosion inhibitors and stability additives compatible with high-alcohol fuels. Regulatory safeguards were reinforced through enhanced Bureau of Indian Standards quality control orders implemented in February 2025, mandating strict purity and certification for over 150 functional additive categories and curbing low-grade imports.

Summary of Country-Level Strategic Drivers in the Functional Additives Market

Functional Additives Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Implications for Functional Additives

|

|

Germany

|

Mass balance chemistry and digital LCA

|

Low-carbon, OEM-grade, traceable additives

|

|

China

|

Semiconductor specialization and scale

|

Growth in CMP, photoresist, and bio-based additives

|

|

United States

|

Performance standards and circular plastics

|

Advanced detergents and recycled-content stabilizers

|

|

Japan

|

Regulatory tightening and battery focus

|

Fluorine-free additives and energy storage materials

|

|

India

|

PLI incentives and global consolidation

|

Rapid capacity expansion and import substitution

|

Functional Additives Market Report Scope

Functional Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5 Billion

|

|

Market Size (2034)

|

$8.2 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Functional Type (Stabilizers, Processing Aids, Property Modifiers, Surface and Aesthetic Additives, Functional Fillers), By Material Compatibility (Polymers and Plastics, Coatings, Inks and Adhesives, Food and Beverage Packaging, Construction Materials), By End-Use Industry (Packaging, Automotive and Transportation, Construction and Infrastructure, Electrical and Electronics, Consumer Goods and Personal Care, Agriculture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, The Lubrizol Corporation, Dow Inc., Clariant AG, Arkema S.A., Songwon Industrial Co., Ltd., ADEKA Corporation, Sudarshan Chemical Industries Limited, Afton Chemical Corporation, Infineum International Ltd., Innospec Inc., LANXESS AG, Solvay S.A., China National Bluestar Group Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Functional Additives Market Segmentation

By Functional Type

- Stabilizers

- Antioxidants

- UV Stabilizers

- Heat Stabilizers

- Light Stabilizers

- Processing Aids

- Lubricants

- Slip Agents

- Antiblocking Agents

- Mold Release Agents

- Property Modifiers

- Impact Modifiers

- Plasticizers

- Flame Retardants

- Antistatic Agents

- Surface and Aesthetic Additives

- Colorants and Pigments

- Optical Brighteners

- Antimicrobials

- Nucleating Agents

- Functional Fillers

- Glass Fibers

- Carbon Black

- Calcium Carbonate

- Kaolin

By Material Compatibility

- Polymers and Plastics

- Coatings, Inks and Adhesives

- Food and Beverage Packaging

- Construction Materials

By End-Use Industry

- Packaging

- Automotive and Transportation

- Construction and Infrastructure

- Electrical and Electronics

- Consumer Goods and Personal Care

- Agriculture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Functional Additives Industry

- BASF SE

- Evonik Industries AG

- The Lubrizol Corporation

- Dow Inc.

- Clariant AG

- Arkema S.A.

- Songwon Industrial Co., Ltd.

- ADEKA Corporation

- Sudarshan Chemical Industries Limited

- Afton Chemical Corporation

- Infineum International Ltd.

- Innospec Inc.

- LANXESS AG

- Solvay S.A.

- China National Bluestar Group Co., Ltd.

*- List not Exhaustive