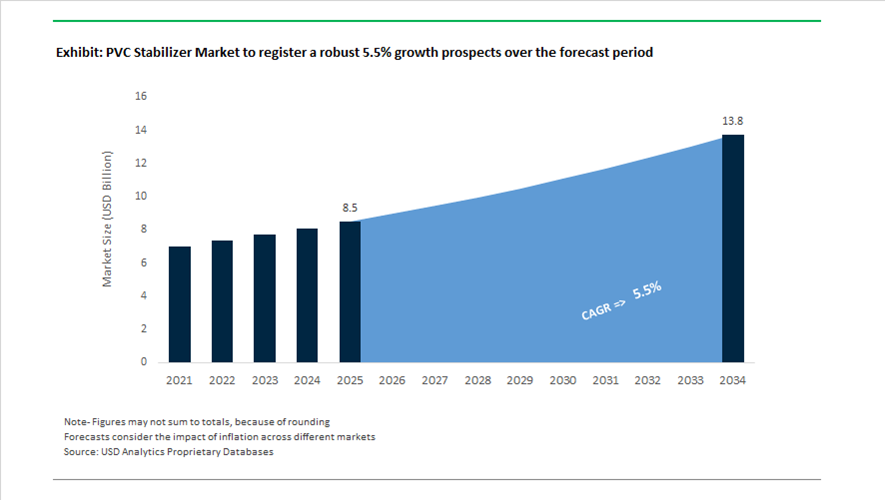

PVC Stabilizer Market Valued at $8.5 Billion in 2025, Projected to Reach $13.8 Billion by 2034 at 5.5% CAGR

The global PVC stabilizer market is valued at $8.5 billion in 2025 and is projected to reach $13.8 billion by 2034, expanding at a CAGR of 5.5%. Demand is rising across calcium-zinc stabilizers, mixed-metal systems, organotin stabilizers, lead-free PVC additives, heat stabilizers for rigid and flexible PVC, and sustainable polymer additive solutions used in pipes, profiles, cables, flooring, medical tubing, and high-clarity packaging. Regulatory restrictions on heavy metals, urban infrastructure expansion in Asia and the Middle East, and decarbonization mandates in additive manufacturing are reshaping global supply chains and R&D priorities.

Regulatory acceleration defined 2024. Effective November 2024, European Union Regulation (EU) 2023/293 mandated reduction of lead content in PVC polymers to below 0.1%, forcing a rapid shift toward calcium-zinc and organic-based stabilization systems across Europe. In March 2024, Valtris Specialty Chemicals appointed Barentz as its primary distributor in the U.S. and Canada to expand the reach of mixed-metal stabilizers and Santicizer® products within construction and automotive markets. In April 2024, ADEKA launched its “ADX 2026” mid-term management plan, emphasizing sustainable polymer additive innovation and greenhouse gas emission reduction across PVC stabilizer production lines. In August 2024, Formosa Plastics announced a significant capacity expansion at its Baton Rouge PVC facility, indirectly increasing regional demand for high-performance heat stabilizers to process higher resin volumes. During early 2024, Goldstab Organics expanded into the MENA region, promoting non-lead and environmentally compliant stabilizers at Plastex Egypt to support regional transition away from heavy-metal additives.

Commercial partnerships and sustainability initiatives intensified in 2025. In January 2025, SONGWON Industrial Group appointed Altek International FZE as distributor for premium PVC stabilizers in the Middle East, addressing surging construction-driven demand linked to urban infrastructure projects. In September 2025, ADEKA received technical recognition for next-generation stabilizer systems enabling enhanced transparency in rigid PVC, strengthening the material’s competitiveness in high-clarity packaging applications. In October 2025 at K 2025, Baerlocher reaffirmed its carbon neutrality target for 2045, announcing investments in solar and biomass energy to reduce Scope 1 and 2 emissions from additive manufacturing. In late 2025, Baerlocher intensified its Tin Replacement program, promoting high-performance calcium-zinc alternatives to organotin stabilizers for drinking water, medical, and food-contact PVC products facing stricter toxicity regulations.

Product innovation and regional market activation extend into 2026. In February 2026, Valtris showcased its sustainable mixed-metal stabilizer portfolio at PLASTINDIA 2026, highlighting compliance with evolving global VOC and toxicity standards while maintaining processing latitude for converters. The PVC stabilizer market is increasingly characterized by lead-free calcium-zinc systems, organotin replacement strategies, mixed-metal stabilizer expansion in North America and the Middle East, carbon-neutral additive production targets, high-transparency rigid PVC stabilization, and regulatory-driven reformulation across EU markets. Infrastructure growth, environmental compliance mandates, and sustainable additive innovation continue to shape competitive positioning across global PVC processing industries.

Key Trends and High-Impact Opportunities in the PVC Stabilizer Market

Mandatory Global Transition to Lead-Free and Cadmium-Free Stabilizer Systems

The PVC stabilizer market has crossed a regulatory point of no return, with the transition to lead-free and cadmium-free systems moving from voluntary compliance to legally enforced market access criteria. Effective November 29, 2024, the European Commission implemented Regulation 2023/923, restricting lead content in PVC articles to below 0.1%. This amendment closes long-standing loopholes for imported finished goods, making compliance mandatory not only for EU-based producers but also for exporters supplying construction products, cables, profiles, and consumer PVC into the European market.

While most European converters phased out lead stabilizers nearly a decade ago, the regulatory tightening has significant implications for global trade flows and recycling economics. Exemptions allowing recovered rigid PVC with up to 1.5% lead content are now strictly time-bound, with a final sunset date of May 28, 2033. This deadline is accelerating immediate investment in advanced re-stabilization technologies, as recyclers can no longer rely on grandfathered formulations to remain compliant. As a result, demand for modern Calcium-Zinc and organic-based stabilizer systems is increasing across both virgin and recycled PVC streams.

Regulatory pressure is also intensifying in North America. In December 2024, the U.S. Environmental Protection Agency designated vinyl chloride as a High-Priority Substance under the Toxic Substances Control Act, followed by a detailed draft scope issued in January 2025. This designation signals heightened scrutiny across the entire PVC value chain, including stabilizer chemistries. In response, Tier-1 wire and cable manufacturers have begun pre-emptive substitution away from legacy lead and selected organotin systems, accelerating the adoption of Calcium-Zinc formulations well ahead of any formal federal bans.

Proliferation of One-Pack Multi-Functional Additive Systems

Operational complexity and rising performance expectations are driving a structural shift toward One-Pack stabilizer systems that integrate primary stabilizers, lubricants, co-stabilizers, and processing aids into a single, pre-engineered formulation. This trend reflects a broader move toward process simplification, batch-to-batch consistency, and risk reduction in high-speed extrusion and calendering environments.

Strategic capacity investments underline the scale of this shift. In October 2025, Songwon Industrial Group announced a major capital commitment to establish a dedicated One Pack Systems production facility in Saudi Arabia. The facility is designed to serve the Middle East’s rapidly expanding infrastructure and construction markets, where large-diameter pipes and fittings demand stabilizer packages that perform reliably under high shear and elevated throughput conditions.

From a technical perspective, modern One-Pack systems are engineered to address chronic production bottlenecks such as plate-out and die fouling. Liquid mixed-metal stabilizer packages released in early 2025 for Middle East and Africa markets integrate hydrotalcites and liquid phosphites to improve thermal buffering and melt lubrication. Field data from high-output extrusion lines indicate that these systems enable 15% to 20% higher line speeds while preserving initial color, surface gloss, and long-term weatherability. For processors, the shift to One-Packs directly translates into lower scrap rates, reduced formulation errors, and improved overall equipment effectiveness.

Enabling the High-Value Use of Recycled PVC Through Re-Stabilization Technologies

The expansion of recycled PVC is constrained not by collection volumes but by thermal degradation and legacy contaminant issues during reprocessing. This creates a high-margin opportunity for advanced re-stabilization packages that restore heat stability, color, and mechanical integrity to post-consumer recyclate.

At NPE2024, Baerlocher demonstrated that its BAEROPOL T-Blend stabilizer technology, when paired with next-generation dual-filtration recycling systems, reduced large-gel coverage in recycled PVC film by nearly 50%. This performance improvement allows recyclers to move rPVC into higher-value applications such as window profiles, technical sheets, and durable construction products rather than downcycling into low-margin products.

Regulatory drivers are amplifying this opportunity. Updated REACH requirements mandate clear labeling for any PVC article containing recovered material with lead content above 0.1%. This has created immediate demand for stabilizer systems capable of passivating residual lead while delivering fresh thermal protection for subsequent processing cycles. Industry specialists, including Reagens Group, have highlighted strong uptake of these solutions across European recycling hubs since late 2024, as converters seek to preserve circularity without sacrificing regulatory compliance.

Specialized Stabilizers for Medical and Food-Contact PVC Applications

Medical devices and food-contact packaging represent the highest-value segments within the PVC stabilizer market, characterized by stringent regulatory oversight, low tolerance for extractables, and premium pricing for validated chemistries. Growth in these applications is increasingly tied to suppliers’ ability to provide comprehensive toxicological documentation and long-term regulatory assurance.

In April 2025, Galata Chemicals expanded its footprint in medical-grade PVC through a strategic European distribution partnership focused on high-purity Calcium-Zinc stabilizers. These formulations are engineered for applications such as blood bags and IV tubing, where compliance with USP Class VI and ISO 10993 biocompatibility standards is mandatory and non-negotiable.

Regulatory intensity is reinforcing this trend. By September 2025, the U.S. FDA had significantly increased inspection frequency for medical device component suppliers, issuing warning letters at a higher rate for insufficient extractables and leachables data. This environment is pushing medical PVC processors to consolidate their supplier base around stabilizer manufacturers capable of delivering validation-ready chemistry supported by robust E&L dossiers. As a result, stabilizers designed for medical and food-contact PVC are commanding substantial price premiums, positioning this segment as a durable profit pool despite broader cost pressures in commodity PVC markets.

PVC Stabilizer Market Share and Segmentation Insights

Metal Based Stabilizers Lead Global PVC Processing Stabilization Technologies

Metal based stabilizers accounted for 52.80% of the PVC Stabilizer Market by type in 2025, reflecting their strong performance in maintaining polymer stability during high temperature PVC processing. Calcium zinc and barium zinc stabilizer systems are widely used to prevent degradation, discoloration, and loss of mechanical strength during extrusion and molding processes. These stabilizers have successfully replaced traditional lead and cadmium based systems in many PVC applications due to improved environmental compliance and regulatory acceptance. In 2025, calcium zinc stabilizers are becoming the dominant formulation in construction materials, offering effective thermal stabilization for PVC pipes, window profiles, and fittings used in infrastructure and building applications.

Rigid PVC Applications Drive Stabilizer Demand in Construction and Infrastructure Materials

Rigid PVC accounted for 58.60% of the PVC Stabilizer Market by application in 2025, reflecting the extensive use of PVC in pipes, window profiles, siding panels, and structural building materials. Stabilizers are essential for protecting PVC during high temperature extrusion processes and for maintaining long term durability in outdoor construction environments. The large scale consumption of rigid PVC in infrastructure, water distribution systems, and building products continues to sustain strong stabilizer demand. In 2025, the transition to lead free PVC formulations has largely been completed globally, with calcium zinc and organic stabilizer systems widely adopted across rigid PVC manufacturing to meet international environmental standards and regulatory requirements.

PVC Stabilizer Market Competitive Landscape

The 2026 PVC stabilizer market is defined by the rapid shift to calcium-zinc (Ca-Zn) and organic stabilizers, recyclate-compatible formulations, and Industry 4.0 one-pack systems. Competitive differentiation is driven by PFAS-free compliance, PCR stabilization, carbon footprint reduction, and high-performance applications in infrastructure, automotive, and medical PVC.

Baerlocher leads tin replacement transition with low-carbon Ca-Zn stabilizers and recycling innovation

Baerlocher GmbH is advancing the global shift away from organotin stabilizers through its expanded Tin Replacement program featuring Ca-Zn systems with up to 50% lower CO2 emissions. Its Baeropol T-Blend additives enhance recyclate compatibility by suppressing thermal degradation and gel formation in PCR PVC. The company is progressing toward 2045 carbon neutrality through biomass and solar integration across global sites, including its India mega-plant. Strong technical service supports converters transitioning from lead-based stabilizers in potable water and medical applications. Global-local operating model enables tailored solutions across regulatory-driven markets. Focus on sustainable additives and circular PVC performance strengthens its leadership in next-generation stabilizer systems.

Adeka strengthens high-performance PVC stabilizers with bio-based additives and transparency innovation

Adeka Corporation is expanding its eco-friendly PVC stabilizer portfolio through advanced clarifiers, bio-based plasticizers, and Ca-Zn systems targeting high-value applications. The TRANSPAREX™ technology enhances optical clarity and is being integrated into ADK STAB stabilizers for rigid PVC films. The ADK CYCLOAID™ series addresses growing demand for recycling additives and bio-based polymeric plasticizers in India and Asia-Pacific. The company targets ¥115 billion in eco-product sales by 2026, focusing on heavy-metal-free stabilizers for automotive interiors. Strong expertise in epoxy-based ADK CIZER stabilizers provides combined heat stability and flexibility for wires and cables. Portfolio diversification supports growth in medical, electronics, and sustainable PVC applications.

Songwon drives margin resilience through pricing strategy and global PVC stabilizer expansion

SONGWON Industrial Group is strengthening its PVC stabilizer market position through strategic pricing and operational optimization. A 12%–20% global price increase in 2026 addresses rising logistics costs and feedstock volatility impacting polymer stabilizers. ESG leadership is reinforced by a Platinum EcoVadis rating, placing the company among the top performers in carbon footprint reduction. Operational improvements include warehouse relocation in the U.S. and procurement optimization in South Korea to enhance supply flexibility. Expansion into the Middle East through Altek International supports growth in infrastructure and desalination projects. Focus on premium stabilizers and regional diversification enhances competitiveness in high-demand PVC applications.

Valtris expands multifunctional PVC stabilizers with bio-based feedstocks and antimicrobial innovation

Valtris Specialty Chemicals is positioning itself in multifunctional PVC stabilizer systems by integrating renewable feedstocks and antimicrobial technologies. The acquisition agreement involving Champlor Renewables strengthens access to bio-based inputs for stabilizers and lubricants. Collaboration with Wells Performance Materials has introduced silver-based antimicrobial additives targeting healthcare-grade PVC applications. New liquid mixed-metal stabilizers offer low volatility and high transparency for flooring and automotive skins. Strategic focus includes Scope 3 emissions tracking and expansion of flame retardant collaborations with Transfar Group. Portfolio integration of sustainability and performance additives supports growth in regulated and high-specification markets.

Sun Ace accelerates one-pack PVC stabilizer adoption with lead-free solutions and EV-grade innovation

Sun Ace is leading the transition to one-pack stabilizer systems in Asia-Pacific, combining stabilizers, lubricants, and processing aids for efficient PVC processing. The company is driving large-scale replacement of lead stabilizers with Ca-Zn and organic-based systems in regional piping projects. R&D efforts focus on UL 94 V-0 compliant stabilizers for EV applications using halogen-free chemistries. Collaboration with PVC resin producers enables dry-blend optimized formulations that increase extrusion line speeds by up to 15%. Strong manufacturing presence across Southeast Asia supports rapid customization and technical service. Focus on dust-free, high-efficiency stabilizers aligns with high-speed extrusion and infrastructure demand.

Reagens advances calcium-organic stabilizers with superior color performance and plate-out-free technology

Reagens SpA is strengthening its position in the European PVC stabilizer market through calcium-organic (COS) technology and advanced tin-replacement solutions. COS stabilizers deliver improved initial color and transparency compared to conventional Ca-Zn systems in rigid PVC applications. Broad portfolio includes mixed-metal stabilizers, tin systems, and specialty lubricants for diverse thermoplastics. Certification under ISO 45001 and ISO 50001 highlights its focus on energy efficiency and safe chemical manufacturing. Development of plate-out-free additives reduces maintenance downtime in high-throughput extrusion processes. Technical specialization and performance-driven formulations support adoption in modern PVC processing environments.

Germany: Post-Lead Transition, Recycling Compatibility, and Net-Zero Additive Design

Germany represents the most mature regulatory and technology-driven PVC stabilizer market in Europe, shaped by early compliance with the EU-wide ban on lead concentrations above 0.1% in PVC products enforced in late 2024. By 2025, German manufacturers such as Baerlocher had transitioned more than 95% of domestic stabilizer output toward high-efficiency Calcium-Zinc systems, establishing Ca-Zn as the structural baseline for rigid and flexible PVC formulations. This shift accelerated further at K-Show 2025, where German suppliers advanced the Tin Replacement Program, positioning Ca-Zn stabilizers as the preferred alternative to organotin in potable water, medical tubing, and food-contact PVC in order to align with evolving REACH and RoHS expectations.

Sustainability and circularity now define competitive differentiation. In late 2025, major German additive producers published 2045 net-zero roadmaps supported by biomass-powered synthesis routes and digital Scope 3 emissions tracking across stabilizer value chains. Product innovation has increasingly focused on recycled-content compatibility. New Baeropol T-Blend formulations launched in August 2025 were engineered to suppress thermal degradation in post-consumer recycled PVC, enabling recyclate to match virgin resin performance during extrusion and calendaring. Parallel investments in renewable feedstocks, including epoxidized soybean methyl esters and waste cooking oil derivatives, reflect ESG-driven procurement mandates. Process efficiency has also advanced, with Q4 2025 adoption of integrated internal-external lubricant One-Pack systems delivering an average 12% reduction in energy consumption on high-speed extrusion lines.

India: Infrastructure-Led Demand and Rapid One-Pack Adoption

India’s PVC stabilizer market is expanding on the back of regulatory enforcement, infrastructure development, and domestic capacity localization. Through 2025, the Ministry of Environment, Forest and Climate Change enforced Lead Stabilizer Regulation Rules that require all potable-water PVC pipes to meet stringent lead extraction thresholds certified by the Bureau of Indian Standards. This has accelerated the structural shift toward Ca-Zn stabilizers and pre-compounded One-Pack systems across pipe and fittings applications. Concurrently, the Ministry of Agriculture’s irrigation expansion programs are driving a projected 24% increase in One-Pack stabilizer adoption for high-pressure PVC piping used in rural water delivery and micro-irrigation networks.

Telecom infrastructure has emerged as a second demand pillar. With the rollout of BharatNet Phase III, Indian cable manufacturers reported stabilizer consumption exceeding 390,000 metric tons during 2024–2025, largely for PVC ducting and fiber-optic sheathing. Policy support under the Specialty Chemicals Production Linked Incentive scheme has reinforced localization, with firms such as Goldstab and Platinum Industries expanding Ca-Zn capacity in Gujarat to reduce import reliance. At the processing level, modernization is delivering tangible productivity gains. Industry disclosures at Indian Petrochem 2025 indicated that processors switching from monomeric additives to integrated One-Pack systems achieved a 21% reduction in processing time, improving throughput consistency and compliance readiness.

China: Scale, Efficiency Mandates, and Controlled Organotin Evolution

China remains the world’s largest consumer and producer of PVC stabilizers, with demand underpinned by infrastructure scale and industrial modernization. In September 2025, the Ministry of Industry and Information Technology implemented an Industrial Equipment Renewal plan requiring stabilizer production facilities to achieve a 20% improvement in energy efficiency or face output curtailments. This mandate is accelerating investment in automated dosing, waste-heat recovery, and process optimization across Ca-Zn and organotin lines.

Despite global substitution trends, China continues to specialize in high-performance organotin stabilizers for applications requiring superior clarity and thermal stability, particularly decorative films and specialty profiles. However, the market is pivoting toward “Greener Tin” variants with reduced toxicity to preserve export access. In 2024 alone, China consumed approximately 620,000 metric tons of PVC stabilizers, with significant volumes directed toward advanced utility grids and support infrastructure linked to next-generation lithography ecosystems. Regulatory oversight has tightened further under the 2025 Chemical Safety Roadmap, which mandates QR-coded batch traceability for hazardous metal stabilizers, enabling rapid recalls and compliance verification in export-oriented regions such as the Pearl River Delta.

United States: TSCA Compliance and Grid-Driven Specialty Demand

The United States PVC stabilizer market is being reshaped by compliance pressure under the Toxic Substances Control Act and demand from power and semiconductor infrastructure. By 2025, American compounders reported a 23% improvement in processing efficiency as legacy lead systems were phased out in favor of non-toxic, liquid One-Pack formulations that simplify dosing and reduce line variability. Grid expansion has been a primary volume driver. In 2024, over 420,000 metric tons of stabilizers were consumed for PVC cable sheathing, with One-Pack systems accounting for 61% of this segment due to their consistency and reduced defect rates in high-speed wire and cable extrusion.

A higher-value specialty segment is emerging alongside CHIPS Act investments. Semiconductor fabs and supporting chemical delivery systems increasingly require ultra-pure PVC additives with zero outgassing and minimal ionic contamination. This has elevated demand for tightly controlled stabilizer chemistries tailored for cleanroom piping and fluid handling, positioning advanced Ca-Zn and hybrid systems as strategic inputs for U.S. electronics manufacturing supply chains.

Comparative Snapshot: PVC Stabilizer Industry by Country

PVC Stabilizer Market County Level Snapshot

|

Country / Region

|

Primary Market Driver

|

Strategic Stabilizer Trend

|

|

Germany

|

Lead-free maturity, recycling mandates

|

Ca-Zn dominance, PCR-optimized One-Pack systems

|

|

India

|

Water, agriculture, telecom infrastructure

|

Rapid One-Pack adoption, Ca-Zn localization

|

|

China

|

Scale and energy efficiency regulation

|

Efficient Ca-Zn growth, controlled organotin evolution

|

|

United States

|

TSCA compliance, grid and semiconductor demand

|

Liquid One-Pack systems, ultra-pure specialty grades

|

PVC Stabilizer Market Report Scope

PVC Stabilizer Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.5 Billion

|

|

Market Size (2034)

|

$13.8 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Type (Metal-Based Stabilizers, Lead-Based Stabilizers, Organic-Based Stabilizers, One-Pack Stabilizer Systems), By Form (Solid, Liquid, Flake & Pellet), By Application (Rigid PVC, Flexible PVC, Films & Sheets, Other PVC Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Baerlocher GmbH, Adeka Corporation, Songwon Industrial Co. Ltd., Valtris Specialty Chemicals, Sun Ace Kakoh Pte. Ltd., Galata Chemicals, Reagens SpA, Pau Tai Industrial Corporation, Vikas Ecotech Limited, Goldstab Organics Pvt. Ltd., Kisuma Chemicals BV, Patcham FZC, Shandong Jinchangshu New Material Co. Ltd., Fine Organics, Akcros Chemicals Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PVC Stabilizer Market Segmentation

By Type

- Metal-Based Stabilizers

- Lead-Based Stabilizers

- Organic-Based Stabilizers

- One-Pack Stabilizer Systems

By Form

- Solid

- Liquid

- Flake & Pellet

By Application

- Rigid PVC

- Flexible PVC

- Films & Sheets

- Other PVC Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in PVC Stabilizer Industry

- Baerlocher GmbH

- Adeka Corporation

- Songwon Industrial Co. Ltd.

- Valtris Specialty Chemicals

- Sun Ace Kakoh Pte. Ltd.

- Galata Chemicals

- Reagens SpA

- Pau Tai Industrial Corporation

- Vikas Ecotech Limited

- Goldstab Organics Pvt. Ltd.

- Kisuma Chemicals BV

- Patcham FZC

- Shandong Jinchangshu New Material Co. Ltd.

- Fine Organics

- Akcros Chemicals Limited

*- List not Exhaustive