UV Stabilizers Market Overview 2025–2034: $2.6 Billion to $4.3 Billion at 5.7% CAGR Driven by NOR-HALS Innovation, Engineering Plastics Durability, and Agro-Film Weatherability

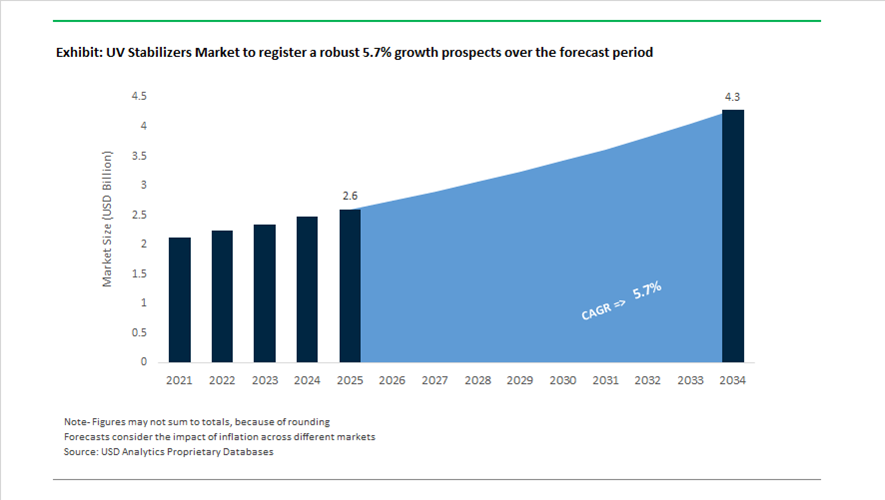

The global UV Stabilizers market is valued at $2.6 billion in 2025 and is projected to reach $4.3 billion by 2034, expanding at a CAGR of 5.7%. Market growth is anchored in rising demand for HALS stabilizers, NOR-HALS additives, hydroxyphenyl triazine (HPT) UV absorbers, polymer light stabilizers, engineering plastics protection, agricultural film stabilizers, and long-life polyolefin durability solutions. Increasing outdoor infrastructure, floating solar installations, automotive lightweighting, and advanced nylon applications are elevating performance requirements for acid resistance, sulfur and chlorine tolerance, and long-term photothermal stability. Simultaneously, manufacturers are optimizing production footprints and expanding specialty additive portfolios to address regulatory and cost pressures across Europe and Asia.

Innovation momentum accelerated from 2024 through 2026. In March 2024, Ashland and DIC Corporation entered a collaboration to co-develop UV stabilizer systems tailored for automotive coatings and advanced packaging substrates. In May 2024, Clariant completed the acquisition of Huntsman’s pigments and additives business, significantly expanding its UV absorber and stabilizer portfolio for industrial coatings and technical textiles. In July 2024, BASF introduced Tinuvin® NOR® 211 AR, a high-performance heat and light stabilizer engineered for agricultural plastics exposed to sulfur- and chlorine-based agrochemicals, marking a strategic shift from inorganic stabilizers toward advanced organic systems. In July 2025, BYK launched BYK-MAX LS 4128 to enhance the UV durability of polyamide materials in high-traffic industrial environments, addressing a longstanding stabilization challenge in engineering plastics. The same month, Everlight Chemical introduced Eversorb® 990, formulated specifically for agricultural films subjected to harsh pesticide and fertilizer exposure. At the European Coatings Show 2025, SONGWON expanded its liquid HPT UV absorber line with the SONGSORB® CS 400 series, targeting waterborne coatings requiring maximum transparency and UV shielding.

Capacity expansion and portfolio repositioning are reinforcing supply resilience and specialty focus. In August 2025, Clariant completed a second production line for Nylostab® S-EED at its Cangzhou, China facility, addressing rising demand in Asian engineering plastics and textile applications. In October 2025 at K 2025, BASF unveiled Tinuvin® NOR® 600, a next-generation NOR-HALS stabilizer delivering superior acid resistance and extreme weatherability for PVC roofing membranes and artificial turf systems. In February 2026 at Plastindia, BASF demonstrated stabilizer performance in floating solar pontoons designed for service lifetimes exceeding 30 years under continuous UV exposure. Strategic manufacturing adjustments also reshaped the value chain. In August 2024, BASF announced consolidation of cyclododecanone precursor production at Ludwigshafen, shifting focus to more cost-efficient global sites. In January 2026, Syensqo divested its Oil & Gas business to concentrate on specialty polymer additives and electronic-grade UV stabilizers within its Performance & Care segment.

Trends and Opportunities in the UV Stabilizers Market

Material Innovation in High-Stakes Industrial and Automotive Systems

The UV stabilizers market is shifting decisively toward high-molecular-weight Hindered Amine Light Stabilizers and advanced triazine absorbers as polymer failure risks escalate in automotive, energy, and electronics applications. This transition is being driven less by cost optimization and more by liability management, warranty exposure, and safety assurance, particularly in electric vehicle platforms where polymer degradation can compromise battery enclosures, cable insulation, and exterior finishes.

In April 2025, Society of Automotive Engineers updated its weathering and durability guidance for interior and exterior polymer components, placing greater emphasis on long-term gloss retention, tensile stability, and resistance to thermal cycling. In response, SONGWON expanded its SONGSORB® CS 400 series of liquid hydroxyphenyl-triazine UV absorbers. These formulations are engineered to withstand the elevated bake temperatures and cyclic heat loads associated with modern EV battery housings and under-hood components, where conventional low-molecular-weight stabilizers exhibit volatility or loss of efficacy.

Parallel innovation is occurring in electronics and 5G infrastructure materials. As telecom equipment migrates outdoors and operates at higher frequencies, resin systems based on polycarbonate and polyphenylene ether are being reformulated with halogen-free, low-migration UV stabilizers. These materials maintain dielectric integrity while preventing surface embrittlement and color shift under continuous solar exposure, a requirement that has become non-negotiable for base stations deployed across high-irradiance regions.

Global Phase-Out of Legacy Absorbers and Region-Specific Reformulation

Regulatory action is accelerating the exit of legacy benzotriazole UV absorbers from the global market, triggering a rapid reformulation cycle across coatings, plastics, and industrial composites. Effective August 4, 2025, the European Commission’s Delegated Regulation (EU) 2025/843 formally listed UV-328 as a Persistent Organic Pollutant, imposing an unintentional trace contaminant limit of 100 mg/kg. This threshold effectively disqualifies UV-328 from most high-performance applications, even where limited derogations remain for automotive uses until 2030.

Tier-1 suppliers are responding by mandating next-generation hydroxyphenyl-triazine absorbers within their approved material lists, accelerating the adoption of stabilizer systems that deliver comparable UV screening without regulatory risk. This transition is particularly pronounced in automotive plastics and heavy-duty industrial coatings, where reformulation timelines are being pulled forward to avoid mid-decade compliance shocks.

At the same time, geographic shifts in polymer manufacturing are reshaping stabilizer design. As production capacity migrates toward the Solar Belt, including India, Southeast Asia, and Mexico, formulators are engineering so-called tropical-grade stabilization packages. Technical trials conducted during 2024 and 2025 demonstrate that combining HALS at approximately 0.45 weight% with nano-scale zinc oxide screeners can triple the service life of polypropylene films under high irradiance compared to conventional absorber-only systems. These formulations address the combined challenges of UV intensity, heat, and humidity that characterize emerging manufacturing hubs.

Securing Multi-Decade Reliability for Renewable and Public Infrastructure

Long-duration exposure requirements in renewable energy and public infrastructure are creating one of the highest-value opportunity segments for UV stabilizers. Solar, wind, and transit projects increasingly specify polymer components with 20 to 25 year performance guarantees, elevating UV resistance from a secondary attribute to a core material specification.

In India, large-scale renewable energy programs during 2024 and 2025, including PM-Surya Ghar and PLI Tranche-II, are driving rapid deployment of solar capacity that relies heavily on UV-stabilized backsheets and encapsulants. To meet these requirements, manufacturers are adopting advanced NOR-HALS technologies such as BASF’s Tinuvin® NOR® series, which provides enhanced resistance to both UV radiation and aggressive environmental contaminants such as sulfur and chlorine commonly present in agricultural and industrial zones.

Beyond energy, public infrastructure programs in the United States and European Union are increasingly tied to climate resilience criteria within public-private partnership frameworks. UV-stabilized composites are gaining traction in wind turbine blades, bridge cable jackets, and public transit components, where UV-induced cracking or discoloration can result in maintenance costs exceeding one million dollars per project. These applications favor high-performance stabilizer systems that extend inspection intervals and reduce lifecycle costs, creating sustained demand for premium UV stabilizer formulations.

Upgrading Post-Consumer Recycled Plastics into High-Value Materials

Regulatory mandates such as the EU Packaging and Packaging Waste Regulation are transforming UV stabilizers into essential enablers of the circular plastics economy. As recycled polymers are exposed to cumulative thermal and oxidative stress, advanced stabilizer systems are required to restore performance characteristics that approach those of virgin resins.

At the K 2025 trade fair, Kisuma Chemicals introduced a new portfolio of magnesium-based synergistic additives designed specifically for post-consumer recycled plastics. These systems minimize yellowing, stabilize melt flow index, and enable compounders to incorporate 30 to 50% recycled content into outdoor furniture, automotive trims, and construction products that were previously inaccessible to recyclates.

Government assessments published by environmental agencies in 2025 underscore the strategic importance of such technologies. Advanced UV stabilizers act as life-extenders, preventing the progressive degradation that limits plastics to one or two recycling loops. This capability is critical for automotive OEMs targeting 25% recycled plastic content in new vehicles by 2030, positioning UV stabilizers as a cornerstone technology in achieving both regulatory compliance and material performance parity within circular manufacturing models.

UV Stabilizers Market Share and Segmentation Insights

Product Type Market Share: Hindered Amine Light Stabilizers Lead with Long-Term UV Protection Efficiency

Hindered amine light stabilizers (HALS) account for 48.60% of the UV stabilizers market in 2025, driven by their superior ability to inhibit photo-oxidation through radical scavenging mechanisms. Their regenerative functionality enables long-term stabilization at low concentrations, making them essential for high-performance applications in automotive plastics, construction materials, and agricultural films. UV absorbers, antioxidants, and quenchers support complementary stabilization roles across formulations. A key trend is the shift toward high-molecular-weight and oligomeric HALS, which reduce migration and extraction risks while enhancing durability, particularly in food contact materials and long-life outdoor polymer applications.

Application Market Share: Plastics and Polymers Segment Leads with Outdoor Performance Requirements

Plastics and polymers hold a 48.60% share in the UV stabilizers market in 2025, reflecting the critical role of stabilizers in protecting materials from UV-induced degradation such as discoloration, embrittlement, and mechanical property loss. Coatings, packaging, adhesives and sealants, agriculture, and personal care applications contribute additional demand across sectors. A key growth driver is the increasing use of plastics in outdoor environments, including automotive exteriors, building products, and agricultural films, where long-term durability is essential. This has driven demand for advanced UV stabilization systems that maintain processing efficiency while delivering extended service life under harsh environmental conditions.

UV Stabilizers Market Competitive Landscape

The UV Stabilizers market in 2026 is defined by material longevity as a decarbonization lever, with NOR-HALS technologies, 30-year durability targets for renewable infrastructure, and advanced scorch protection systems reshaping competition across agricultural films, cables, coatings, and high-performance polymers.

BASF SE Leads NOR-HALS Innovation and 30-Year UV Durability for Floating Solar Infrastructure

BASF SE is dominating the UV Stabilizers market through advanced Tinuvin® and Irgastab® technologies aligned with long-life infrastructure and sustainable plastics. Its Tinuvin® grades enable floating solar pontoons to exceed 30-year service life, addressing harsh UV and humidity exposure in FPV systems. The Tinuvin® NOR® 600 series delivers superior acid resistance, making it ideal for agricultural films, roofing membranes, and artificial turf exposed to pesticides. BASF’s Irgastab® Cable KV 10 ensures scorch protection in XLPE cable insulation, supporting high-voltage transmission networks. Collaboration with Hagihara Industries has demonstrated extended durability in synthetic turf applications up to 10 years. Integration with the VALERAS® sustainability framework enhances transparency in product carbon footprint and lifecycle performance.

SONGWON Strengthens Global UV Stabilizer Supply with Recycling-Focused Formulations

SONGWON Industrial Co., Ltd. is reinforcing its position in the UV Stabilizers market through scale-driven production and recycling-centric stabilizer solutions. The company implemented a 12–20% global price increase in April 2026 to offset rising logistics and raw material costs while maintaining margin stability. Its SONGSORB® CS B stabilizers are engineered to prevent yellowing in post-consumer recycled polyolefins, enabling high-quality mechanical recycling. Expansion into the Middle East and Africa through Chempart Polymers enhances access to major PVC and polyolefin hubs. SONGWON’s integrated Ulsan facility supports large-scale production of HALS, UV absorbers, and antioxidants. Its One-Pack Systems streamline formulation complexity for polymer manufacturers, strengthening operational efficiency and supply reliability.

Clariant AG Expands UV Stabilizer Applications Across Medical Polymers and Asia Markets

Clariant AG is advancing its UV Stabilizers market position through targeted expansion in Asia and high-value medical applications. Its Cangzhou facility in China produces Nylostab® S-EED, a multifunctional stabilizer designed for nylon fibers in automotive and artificial turf applications. The company is promoting Nylostab® for medical polyolefins, where it reduces yellowing caused by gamma sterilization in syringes and non-woven materials. Its introduction of Aristoflex™ SUN demonstrates cross-sector innovation, enhancing UV protection efficiency in personal care formulations. Dispersogen™ PSL 100 supports stability in complex agrochemical formulations, complementing UV stabilizer performance in crop protection systems. This diversified application strategy strengthens Clariant’s position in specialty and regulated markets.

Adeka Corporation Integrates Green UV Stabilizers into Electronics and Transparent Packaging

Adeka Corporation is strengthening its competitive position in the UV Stabilizers market through high-purity additive systems and sustainable supply chain integration. The company has developed a global supply chain for incorporating green UV stabilizers into recycled plastics used in consumer electronics. Its TRANSPAREX™ clarifier technology enhances optical clarity while working synergistically with UV stabilizers for premium cosmetic and medical packaging. Investment in organometallic production for EUV lithography highlights its expertise in light management at the molecular level. Adeka is expanding its presence in South Asia through participation in Plastindia and compounding sector initiatives. This focus on transparency, sustainability, and electronics integration supports its growth in high-value applications.

Syensqo Drives Advanced HALS Stabilizers for Aerospace and EV Composite Protection

Syensqo is positioning itself as a leader in advanced UV stabilizers through its focus on high-performance materials for energy transition sectors. Its CYASORB CYNERGY SOLUTIONS® protect carbon-fiber composites from UV-induced degradation, supporting aerospace and electric vehicle applications. The company reported €1.21 billion EBITDA in 2025, enabling continued investment in specialty stabilizer innovation. ISCC PLUS certification at its Moerdijk facility allows the production of bio-circular stabilizers aligned with Scope 3 emission reduction goals. The launch of Geropon® D2566 enhances pigment dispersion in UV-protective formulations for agrochemical applications. Strategic divestment of its oil and gas business sharpens its focus on sustainable specialty materials and high-growth UV stabilizer markets.

Germany UV Stabilizers Market Anchored in NOR-HALS Innovation and Circular Plastics Leadership

Germany continues to function as the technical and regulatory benchmark for the European UV stabilizers market, driven by high-performance product launches and capacity investments aligned with circular economy objectives. In October 2025, BASF formally introduced Tinuvin NOR 600 at the K2025 trade fair in Düsseldorf. This next-generation NOR-HALS stabilizer class is engineered for exceptional acid resistance, specifically addressing the durability challenges faced by roofing membranes and artificial turf exposed to aggressive atmospheric conditions. The product launch reflects a broader shift toward stabilizers designed for extended service life in demanding outdoor polymer applications, including construction films, geomembranes, and sports infrastructure.

Manufacturing scale-up is reinforcing Germany’s leadership position. BASF completed a multi-million-euro expansion at its Ludwigshafen site in mid-2025, increasing dedicated capacity for hindered amine light stabilizers to meet accelerating European demand for long-life and low-maintenance plastics. This expansion is closely linked to the integration of circular economy principles. German polymer producers are increasingly aligning with BASF’s VALERAS sustainability platform, which enables mass-balance certification and the use of bio-attributed carbon in UV stabilizers. This approach allows downstream customers to measurably reduce product carbon footprint while maintaining identical performance characteristics, positioning Germany as a reference market for sustainable stabilizer qualification.

China UV Stabilizers Market Reshaped by Recycled Plastics Mandates and NEV Collaboration

China’s UV stabilizers market is undergoing rapid structural transformation driven by regulatory mandates and targeted industry partnerships. In preparation for February 1, 2026, the State Administration for Market Regulation issued nine new national standards governing recycled plastics. These standards impose defined performance and durability requirements on stabilizers used in closed-loop recycling systems, compelling manufacturers to develop UV stabilizers that withstand multiple thermal and mechanical reprocessing cycles without degradation. As a result, demand is shifting decisively toward high-molecular-weight and low-migration stabilizer chemistries.

Industrial capacity expansion is concentrated within specialty chemical clusters. In 2025, Suqian Unitechem and Rianlon significantly expanded production across Jiangsu and Hebei, focusing on triazine-based UV absorbers optimized for outdoor electronics and 5.5G telecommunication hardware. Strategic collaboration is further shaping the market. In August 2025, Rianlon entered a joint development partnership with BASF to co-engineer sustainable UV stabilizer packages for China’s rapidly growing new energy vehicle interior components. These formulations prioritize low fogging, long-term color stability, and recyclability, aligning UV stabilizers with China’s broader NEV policy and environmental performance targets.

South Korea UV Stabilizers Market Defined by Net-Zero Manufacturing and Supply Chain Control

South Korea’s UV stabilizers market is increasingly differentiated by carbon efficiency and upstream integration. SONGWON Industrial announced that its Ulsan production complex will transition to externally supplied zero-emission steam by early 2026. This move is projected to reduce emissions by approximately 25,900 tCO2-equivalent annually, positioning the facility among the most carbon-efficient stabilizer manufacturing hubs globally. Lower product carbon footprint is becoming a decisive purchasing criterion for multinational customers, strengthening South Korea’s export competitiveness.

Innovation is closely linked to recycled plastics performance. At K2025, Songwon unveiled XP2121, an experimental stabilizer designed to significantly improve the weatherability of low-quality recycled polypropylene used in electronics housings and technical components. This development supports closed-loop plastic systems without sacrificing UV resistance. Parallel investments have focused on upstream security. Throughout 2025, Songwon finalized major capital projects in di-alkylphenol production, securing reliable access to critical intermediates for UV stabilizer synthesis and insulating operations from volatility in global phenol derivative markets.

United States UV Stabilizers Market Influenced by Regulatory Reform and Aerospace R&D

The United States UV stabilizers market is shaped by regulatory evolution in personal care and targeted federal funding for advanced materials. Under the Modernization of Cosmetics Regulation Act, the U.S. Food and Drug Administration is expected to finalize updated sunscreen regulations by the end of 2025. This reform accelerates the review of new UV filters, with bemotrizinol progressing toward a potential GRASE determination by March 2026. The outcome is expected to significantly alter formulation strategies in the U.S. sun care and dermatological products segment, aligning domestic standards more closely with European practices.

Supply chain localization is also strengthening. Valtris Specialty Chemicals and Songwon expanded North American logistics and technical service capabilities in early 2025, emphasizing faster sample delivery and localized formulation support for automotive clear-coat and industrial coatings customers. In parallel, the U.S. Department of Energy allocated new research funding in 2025 for the development of bio-derived UV stabilizers suitable for high-performance aerospace composites. This funding supports long-term substitution of petrochemical stabilizers in lightweight structural materials used in defense and aviation platforms.

Taiwan UV Stabilizers Market Focused on Agricultural Films and Advanced Composites

Taiwan’s UV stabilizers market is characterized by application-specific innovation targeting agriculture and high-performance composites. In July 2025, Everlight Chemical launched Eversorb 990, a stabilizer engineered to maximize light transmission and extend service life in agricultural mulch films. The product addresses the dual requirement of enhanced photosynthetic efficiency and prolonged outdoor durability, supporting higher crop yields and reduced film replacement frequency.

Composite materials represent a second growth axis. Building on the 2024 introduction of the Eversorb CP Series, Everlight expanded its portfolio in late 2025 to include composite-grade UV stabilizers for carbon-fiber-reinforced polymers used in high-end sporting goods and electric vehicle chassis. These formulations are designed to protect structural integrity and surface aesthetics under prolonged UV exposure, reinforcing Taiwan’s role as a niche innovation hub within the global UV stabilizers market.

Summary of Country-Level UV Stabilizers Market Dynamics

UV Stabilizers Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Key Application Drivers

|

Market Positioning

|

|

Germany

|

NOR-HALS innovation and circular certification

|

Roofing membranes, artificial turf, long-life plastics

|

European technical and regulatory benchmark

|

|

China

|

Recycled plastics mandates and NEV collaboration

|

5.5G hardware, automotive interiors, recycled polymers

|

Policy-driven scale and partnership-led innovation

|

|

South Korea

|

Net-zero manufacturing and upstream control

|

Electronics housings, recycled PP

|

Carbon-efficient global supply hub

|

|

United States

|

Sunscreen reform and aerospace R&D

|

Sun care, automotive coatings, composites

|

Regulation-led demand and advanced research market

|

|

Taiwan

|

Application-specific stabilizer design

|

Agricultural films, CFRP components

|

Niche innovation and specialty applications hub

|

UV Stabilizers Market Report Scope

UV Stabilizers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Hindered Amine Light Stabilizers, UV Absorbers, Quenchers, Antioxidants), By Form (Liquid, Powder, Beads and Granules), By Application (Plastics and Polymers, Coatings, Adhesives and Sealants, Agriculture, Personal Care and Cosmetics, Packaging)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Songwon Industrial Co. Ltd., Clariant AG, Solvay S.A., Adeka Corporation, Everlight Chemical Industrial Corp., Sabo S.p.A., Valtris Specialty Chemicals, Rianlon Corporation, Suqian Unitechem Group, Evonik Industries AG, Mayzo Inc., Lycus Ltd., Addivant, Sarex Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

UV Stabilizers Market Segmentation

By Product Type

- Hindered Amine Light Stabilizers

- UV Absorbers

- Quenchers

- Antioxidants

By Form

- Liquid

- Powder

- Beads and Granules

By Application

- Plastics and Polymers

- Coatings

- Adhesives and Sealants

- Agriculture

- Personal Care and Cosmetics

- Packaging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the UV Stabilizers Market

- BASF SE

- Songwon Industrial Co. Ltd.

- Clariant AG

- Solvay S.A.

- Adeka Corporation

- Everlight Chemical Industrial Corp.

- Sabo S.p.A.

- Valtris Specialty Chemicals

- Rianlon Corporation

- Suqian Unitechem Group

- Evonik Industries AG

- Mayzo Inc.

- Lycus Ltd.

- Addivant

- Sarex Chemicals

*- List not Exhaustive