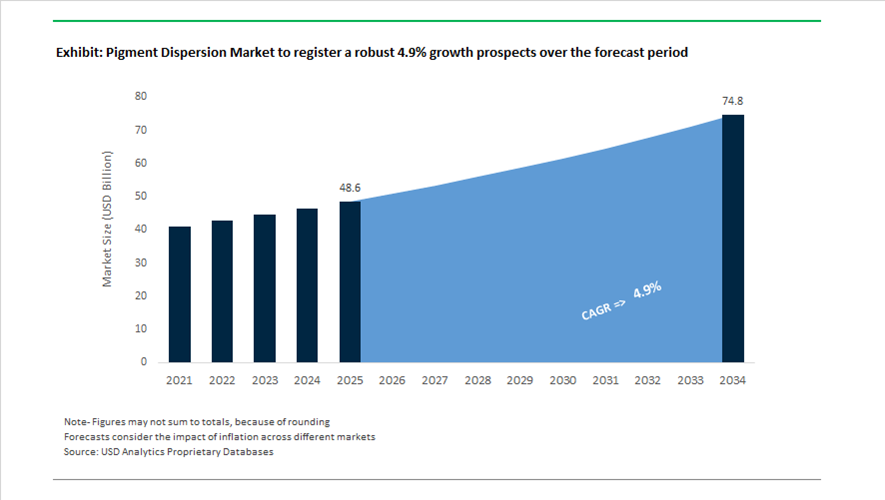

Pigment Dispersion Market Size 2025–2034: $48.6 Billion to $74.8 Billion at 4.9% CAGR Driven by Automotive Coatings, Low-VOC Formulations, and Global Capacity Integration

The global pigment dispersion market is projected to grow from $48.6 billion in 2025 to $74.8 billion by 2034, registering a CAGR of 4.9%. Growth in pigment dispersions for coatings, plastics, inks, construction materials, and high-performance composites is supported by rising demand for automotive refinishes, architectural coatings, packaging inks, and industrial color concentrates. Pigment dispersions, comprising stabilized pigment particles in liquid or polymer carriers, are essential for achieving uniform color strength, optimized rheology, improved gloss, and long-term durability. Increasing emphasis on low-VOC coatings, eco-label-compliant wall paints, and sustainable raw material sourcing is reshaping formulation strategies across global markets.

Industry consolidation accelerated in 2024 and 2025, significantly altering competitive positioning in the pigment dispersion industry. In January 2024, Altana acquired Silberline, strengthening its ECKART division in aluminum effect pigments and enhancing dispersion technology capabilities in North America and Asia. The most transformative development occurred in March 2025 when Sudarshan Chemical Industries finalized acquisition of Germany-based Heubach Group, creating one of the world’s largest pigment and dispersion platforms across 19 manufacturing sites. The integration enhances global R&D reach and production scale while addressing Heubach’s prior financial constraints through operational optimization. In November 2024, Heubach Colorants India reported a 26% quarter-on-quarter revenue increase, reflecting improved EBITDA margins and strong regional dispersion demand in South Asia.

Capacity expansion and technology upgrades are central to growth in advanced pigment dispersions. In November 2025, BASF commissioned a new high-performance dispersant production line in Nanjing using Controlled Free Radical Polymerization technology, strengthening local supply for automotive and industrial coating dispersions in Asia-Pacific. In October 2025, BASF also expanded dispersion capacity in Dilovası, Türkiye, targeting architectural coatings and construction sectors across the Middle East and North Africa. The facility operates on green electricity and emphasizes low-VOC, low-CO2 dispersion technologies aligned with tightening environmental standards. In 2024, Clariant updated its Dispersogen™ and Polyglykol additive portfolios to support eco-label-compliant interior wall paint dispersions, enhancing sedimentation resistance while preserving tinting strength.

Supply chain volatility and pricing strategies shaped 2024–2025 market conditions. In February 2024, Sun Chemical implemented freight surcharges across pigment dispersions due to the Red Sea shipping crisis, which disrupted Suez Canal transit and increased transportation costs. Effective January 1, 2025, the company applied global price adjustments to offset rising raw material and energy expenses, followed by tariff surcharges in May 2025 for color materials affected by trade policy changes in the United States. These measures underscore the sensitivity of pigment dispersion pricing to geopolitical risk and tariff shifts.

Strategic sustainability initiatives are emerging as long-term differentiators in the pigment dispersion market. In mid-2025, ICL Group demonstrated industrial use of Puraloop®, a recycled phosphorus platform supplying circular raw materials for phosphorus-based surfactants and stabilizers used in advanced pigment preparations. In February 2026, DIC Corporation is scheduled to announce Phase 2 of its DIC Vision 2030 strategy, transitioning to a Global Operating Model designed to standardize pigment dispersion quality across subsidiaries, including Sun Chemical, and enhance global production efficiency.

Pigment Dispersion Market Trends and Opportunities: Regulatory Disruption, Electrification Demand, and Circular Carbon Innovation

Global Regulatory Phase-Out of Toxic Pigments Accelerating Shift to High-Performance Organic Dispersions

The Pigment Dispersion market is undergoing a structural transformation driven by stringent global chemical regulations targeting heavy-metal-based pigments, particularly lead and chromium compounds. Regulatory frameworks such as REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) are enforcing the elimination of Chromium (VI) and lead chromate pigments, citing their carcinogenic and environmental risks.

In April 2025, the European Chemicals Agency (ECHA) advanced proposals to restrict Chromium (VI), reinforcing the transition toward high-performance organic (HPO) pigments and hybrid dispersion systems. Simultaneously, global policy discussions are addressing export loopholes, with over 240 tons of toxic pigments previously exported via EU channels, a gap expected to close by 2027 under the Rotterdam Convention’s expanded restrictions.

Industry response is accelerating innovation. By early 2026, BASF Coatings emphasized “sustainability proxy” color strategies, leveraging interference pigments and liquid-metal effects to replace traditional heavy-metal formulations. This aligns with shifting consumer and OEM preferences toward eco-friendly, non-toxic pigment dispersions, particularly in automotive and industrial coatings applications.

Chinese Environmental Regulations and Export Controls Driving Price Volatility and Supply Instability

China’s evolving environmental and trade policies are creating significant disruptions in the global pigment dispersion supply chain. The adoption of the Ecological and Environmental Code in March 2026 consolidates over 30 environmental laws into a unified compliance framework, increasing enforcement intensity on pigment and dye manufacturers.

Additionally, export control measures introduced under MOFCOM Notices No. 61 and 62 impose extraterritorial licensing requirements, including a 0.1% De Minimis rule for Chinese-origin materials in foreign products. This has introduced complex compliance burdens for global dispersion formulators, particularly those reliant on Chinese intermediates.

The impact is evident in financial performance metrics. In early 2026, Heubach Colorants India reported a 32.6% decline in profit before tax, reflecting broader industry downturns and raw material cost volatility. These dynamics are accelerating the adoption of “local-for-local” manufacturing models, as companies seek to stabilize supply chains and mitigate geopolitical risks.

Rising Demand for Conductive Carbon Dispersions in EV Batteries and Energy Storage Systems

The rapid expansion of electric vehicles (EVs) and battery energy storage systems (BESS) is creating a high-growth segment for conductive carbon black dispersions, a critical component in lithium-ion battery electrodes and energy infrastructure.

In late 2025, Orion S.A. confirmed that its PRINTEX® kappa 100 acetylene black had been qualified for major BESS applications, aligning with projections of $1.2 trillion in global BESS investment by 2034. This is significantly boosting demand for high-purity, low-metal-impurity dispersions that meet stringent battery performance requirements.

Technological benchmarks are evolving rapidly. Modern production systems are targeting 50,000 to 80,000 tons per line capacity for conductive carbon blacks, supporting next-generation battery chemistries, including silicon-based anodes. Additionally, EV adoption is indirectly driving demand for abrasion-resistant specialty carbon blacks, as increased vehicle weight and torque accelerate tire wear, expanding application scope across automotive and cable insulation sectors.

This positions conductive dispersions as a strategic growth pillar within the pigment dispersion market, closely tied to global electrification and renewable energy expansion.

Bio-Based and Circular Carbon Dispersions Enabling Sustainable Coatings and Materials Innovation

Sustainability imperatives and Net Zero commitments are accelerating the shift toward bio-based and circular carbon pigment dispersions, reducing dependence on fossil-derived feedstocks. This transition is supported by advancements in recycled carbon technologies and renewable raw materials, aligning with circular economy principles.

In February 2026, Cabot Corporation expanded its EVOLVE Sustainable Solutions platform in Asia-Pacific, introducing circular reinforcing carbons derived from alternative feedstocks. Strategic collaborations with tire manufacturers highlight the growing commercialization of these materials in high-volume applications.

The broader bio-based coatings market is gaining momentum, projected to reach $29.4 billion by 2032, driven by demand for ISCC PLUS-certified bio-based pigments and additives. Innovations such as Mitsui Chemicals’ bio-based epoxy coatings demonstrate the scalability of renewable pigment systems in industrial applications.

Recycling technologies are also advancing. Birla Carbon’s Continua™ Sustainable Carbonaceous Material (SCM), derived entirely from end-of-life tires, offers quantifiable carbon footprint reduction without compromising pigment performance, including color strength and durability. These developments position bio-based dispersions as a high-growth, ESG-aligned segment, supporting sustainable product differentiation across coatings, plastics, and textile industries.

Pigment Dispersion Market Share and Segmentation Insights

Organic Pigment Dispersions Lead High-Performance Color Formulations in Coatings and Printing Systems

Organic pigment dispersions accounted for 52.80% of the Pigment Dispersion Market by pigment type in 2025, reflecting strong demand for high-chroma colorants used in advanced coatings and printing applications. These dispersions deliver superior color intensity, higher tinting strength, and a broader color space compared with inorganic pigments, making them essential for premium paints, coatings, and printing inks. Organic pigments also support heavy-metal-free formulations that align with environmental and regulatory standards across consumer products and industrial coatings. In 2025, advanced polymeric dispersant technologies designed for high-performance organic pigment stabilization are improving dispersion stability, preventing flocculation and crystal growth, and enabling consistent color development in demanding coating and ink formulations.

Paints and Coatings Sector Drives Pigment Dispersion Demand in Global Coating Manufacturing

Paints and coatings represented 42.80% of the Pigment Dispersion Market by application in 2025, reflecting the extensive use of dispersed pigments in architectural coatings, automotive finishes, and industrial protective coatings. Pigment dispersions enable uniform color distribution, improved hiding power, and consistent application performance across waterborne and solvent-based coating systems. The scale of global coatings production continues to support large-volume pigment dispersion consumption. In 2025, the expansion of in-can colorant systems used in retail paint tinting technology is increasing demand for universal pigment dispersions that are compatible with multiple paint bases, allowing precise color matching and flexible inventory management in architectural paint distribution networks.

Pigment Dispersion Market Competitive Landscape

The global pigment dispersion market is shifting toward high-performance aqueous dispersions, CFRP-enabled stability, and bio-based carriers to meet VOC and regulatory requirements. Competition is defined by sustainable innovation, regional production expansion, and advanced dispersion technologies for automotive, electronics, and eco-friendly packaging applications.

Sudarshan-Heubach Integration Builds Global Scale in High-Performance Pigment Dispersions

Sudarshan Chemical Industries, following its March 2025 acquisition of Heubach Group, has created a globally diversified pigment dispersion platform across 19 sites. Integration efforts under CEO Rajesh Rathi focus on combining Heubach’s high-end technical expertise with Sudarshan’s cost-efficient manufacturing scale. The launch of Sudafast Red 313D targets high-performance printing ink applications, while Sudaperm Yellow 2921C addresses premium architectural and industrial coatings. The company is expanding its North American footprint through an exclusive distribution agreement with Lintech International LLC for anti-corrosive and organic dispersions. Sustainability initiatives include renewable energy investments in Maharashtra and Tamil Nadu to support decarbonized production. Portfolio strategy emphasizes organic, inorganic, and anti-corrosive pigment dispersions aligned with global demand for high-performance colorants.

DIC Strengthens High-Chroma Dispersion Portfolio with Integrated Resins and Sustainable Packaging Solutions

DIC Corporation, through Sun Chemical, integrates pigment dispersions with advanced resin systems to deliver high-performance color solutions. The $10 million investment in Newport, Delaware expands quinacridone pigment production for high-chroma red and violet dispersions used in automotive coatings. The launch of SunLam solvent-free ultra-low monomer adhesive supports VOC-free flexible packaging when combined with water-based dispersions. At CHINACOAT 2025, Paliocrom Brilliant Ruby L 3558 demonstrated high brilliance and hiding power for both solvent-borne and water-borne systems in EV battery and interior applications. Strategic focus includes performance material products such as BURNOCK WD-569 resin for battery casings and engineering plastics. Vertical integration across pigments, resins, and dispersions supports advanced energy and packaging applications.

BASF Expands CFRP-Based Dispersion Technology with Localized Production in Asia

BASF SE is advancing pigment dispersion technologies through Controlled Free Radical Polymerization (CFRP) and regional production expansion. The February 2026 commissioning of a new line in Mangalore targets low-VOC and low-odor dispersions for architectural paints and waterproofing systems under Acronal® and Basonal® brands. A November 2025 innovation in Nanjing introduces CFRP-enabled dispersants delivering broader color gamuts and improved stability for automotive and industrial coatings. The company reported €2.4 billion in Industrial Solutions sales in India in 2025, reflecting strong regional demand. Strategic focus includes low Product Carbon Footprint dispersions aligned with EU regulatory frameworks. Dual-sourcing capabilities between Europe and Asia enhance supply chain resilience for global OEM customers.

BYK Advances Digitalized Dispersion Technologies and Sustainable Additives for High-Value Applications

BYK (ALTANA Group) focuses on high-performance wetting and dispersing additives with strong emphasis on digital formulation and sustainability. The August 2025 expansion into Brazil strengthens direct market access and technical service capabilities in South America. Production scaling of Cubic Ink® UV-curing resins and dispersions supports growth in 3D printing applications for aerospace and medical prototyping. Approximately 20% of its workforce is dedicated to R&D, supporting continuous innovation in pigment stabilization and dispersion chemistry. The company secured a €300 million European Investment Bank credit line to fund sustainable technologies, including water-based dispersions and bio-based rheology modifiers. Strategy emphasizes recycling-compatible additives and advanced dispersion performance.

Clariant Expands Sustainable Dispersion Portfolio with Bio-Based Dispersants and Agricultural Applications

Clariant AG is strengthening its pigment dispersion portfolio through sustainable and application-specific innovations. The launch of Dispersogen PSL 100 in March 2026 introduces a 100% active polymeric dispersant for stabilizing high-load agrochemical formulations with improved electrolyte tolerance. Integration of the Tonnegel™ 50 rheology modifier enhances viscosity control in seed coatings and suspension fertilizers across varying conditions. Expansion of Nylostab™ S-EED production in China supports nylon applications requiring high UV stability and color retention. Collaboration with Vertimass LLC highlights Clariant’s capability to integrate dispersion chemistry with biofuel and circular economy technologies. Product strategy focuses on EcoTain®-certified solutions, bio-based dispersants, and high-performance stabilization systems.

India – Acquisition-Led Scale-Up with Compliance-Driven Market Discipline

India’s pigment dispersion industry is undergoing a structural upgrade anchored in global consolidation and domestic policy alignment. The March 2025 acquisition of the Heubach Group by Sudarshan Chemical Industries created a globally integrated pigment and dispersion platform spanning 19 manufacturing sites across Europe, the Americas, and Asia. This move materially expands India’s access to high-performance dispersion technologies for automotive coatings, industrial inks, and plastics, while also strengthening formulation know-how in specialty dispersants. In parallel, Sudarshan’s announced capital expenditure exceeding $100 million in mid-2025 underscores a focus on integrating and modernizing acquired international assets to harmonize quality standards and improve throughput efficiency.

Policy support is reinforcing this consolidation-led momentum. Under the Union Budget 2025–2026, the Production Linked Incentive framework prioritizes specialty dispersants for high-performance coatings as a sunrise segment, improving the economics of domestic capacity expansion. The introduction of Quality Control Orders in February 2025 for more than 150 chemical products has tightened entry barriers, limiting the inflow of sub-standard pigment intermediates and improving pricing discipline for compliant dispersion suppliers. At the application level, Indian formulators such as Pidilite Industries are accelerating R&D into water-based pigment dispersions for textiles and footwear, aligning with sustainability mandates and supporting steady domestic demand growth through 2026.

China – Regulation-Driven Reformulation and Electronics-Led Demand

China’s pigment dispersion market is being reshaped by a convergence of food-contact safety rules, emissions transparency, and electronics-driven purity requirements. The revised GB 4806.10-2025 standard issued in September 2025 significantly expands permitted raw materials while imposing near-zero migration limits for Primary Aromatic Amines. This has forced rapid reformulation of azo-based pigment dispersions toward low-migration polymeric systems, particularly for food packaging and can coatings. Simultaneously, the January 2026 rollout of real-time VOC monitoring has accelerated adoption of water-borne dispersing agents across major hubs such as Nanjing and Shanghai.

At the technology frontier, BASF commissioned a high-performance dispersant line in Nanjing in November 2025 based on Controlled Free Radical Polymerization. This investment directly targets automotive and industrial coatings while integrating local supply chains to reduce Product Carbon Footprint. Under the 2025–2026 chemical growth plan, China is also prioritizing high-purity dispersants for integrated circuits and color filters, positioning pigment dispersion as a strategic input for displays and semiconductor adjacencies rather than a purely coatings-driven segment.

Germany – Technology Intensity and Sustainability-Led Differentiation

Germany remains a global reference point for advanced dispersion chemistry, driven by process innovation and regulatory leadership. In October 2025, German industry players demonstrated commercial deployment of X3D catalyst shaping using additive manufacturing to tailor polymer architectures for dispersion efficiency. This capability improves batch consistency and throughput for high-value dispersion polymers used in automotive and industrial applications. Regulatory drivers are equally influential. The June 2025 update to EU Regulation 2025/1090 has restricted several solvents, accelerating the transition toward compliant polymeric dispersants and reinforcing Germany’s early-mover advantage.

Specialty effect dispersions are a defining growth vector. ECKART has advanced radar-transparent metallic pigment dispersions that enable autonomous driving sensors to function through coated surfaces, opening a premium niche in mobility coatings. Concurrently, major producers including Evonik and BASF have committed to 100% renewable electricity for European dispersion sites by end-2025, embedding sustainability credentials directly into production economics.

Türkiye – Regional Manufacturing Anchor for EMEA

Türkiye has emerged as a critical EMEA hub for pigment dispersions, balancing proximity to end markets with cost-efficient manufacturing. In October 2025, BASF inaugurated a new production line in Dilovası, significantly expanding capacity for architectural and construction dispersions. The facility is purpose-built for low-VOC and low-CO₂ formulations, responding to tightening regulations and growing demand across Türkiye, the Middle East, and Northwest Africa.

Beyond capacity, the Dilovası site strengthens supply chain resilience by regionalizing production for Europe and the Middle East amid persistent trade disruptions. The adoption of the Mass Balance approach and green electricity in 2025 allows BASF to offer reduced-carbon-footprint dispersions, positioning Türkiye as a strategic bridge between sustainability-driven European demand and fast-growing emerging markets.

United States – Bio-Based Innovation and Strategic Reshoring

The US pigment dispersion market is increasingly shaped by bio-based materials, packaging transformation, and supply chain realignment. In November 2025, Trinseo and RWDC Industries announced a joint development program for PHA dispersion technology aimed at compostable and recyclable barrier coatings. These dispersions address oil, grease, and moisture resistance in paper and board while meeting TÜV Austria home-compostable standards, signaling a shift toward functional sustainability in packaging.

Federal policy is reinforcing domestic sourcing. CHIPS Act-related funding in 2025 has extended to ultra-high-purity chemicals, including photoresist-compatible pigment dispersions for semiconductor manufacturing. Concurrently, escalating tariffs on Chinese petrochemical intermediates in spring 2025 have catalyzed a pivot toward local sourcing of carbon black and titanium dioxide dispersions, improving demand visibility for US-based dispersion producers.

Comparative Snapshot – Pigment Dispersion Industry by Country

Pigment Dispersion Market County Level Snapshot

|

Country

|

Strategic Driver

|

2025–2026 Inflection Point

|

Competitive Role

|

|

India

|

Global consolidation and compliance

|

Heubach integration, QCO enforcement

|

Emerging global platform

|

|

China

|

Regulation-led reformulation

|

GB 4806.10-2025, VOC monitoring

|

High-volume adaptive producer

|

|

Germany

|

Process innovation and sustainability

|

X3D shaping, REACH transition

|

Premium technology leader

|

|

Türkiye

|

Regional capacity and resilience

|

Dilovası expansion, low-VOC focus

|

EMEA manufacturing hub

|

|

United States

|

Bio-based and reshoring momentum

|

PHA dispersions, tariff response

|

High-value innovation market

|

Pigment Dispersion Market Report Scope

Pigment Dispersion Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$48.6 Billion

|

|

Market Size (2034)

|

$74.8 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Pigment Type (Organic Pigment Dispersions, Inorganic Pigment Dispersions, Effect Pigment Dispersions), By Dispersion Type (Water-Based Dispersions, Solvent-Based Dispersions, Oil-Based Dispersions, Plasticizer-Based Dispersions), By Application (Paints & Coatings, Printing Inks, Plastics, Textiles, Construction Materials), By End-Use Industry (Packaging & Graphic Arts, Automotive & Transportation, Building & Construction, Consumer Goods & Electronics, Healthcare & Medical Devices)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Sudarshan Chemical Industries Ltd., Clariant AG, DIC Corporation, Altana AG, Heubach Group, Evonik Industries AG, Trinseo PLC, Pidilite Industries Ltd., Arxada, Lubrizol Corporation, Sherwin-Williams Company, Toyo Ink SC Holdings Co. Ltd., Lanxess AG, Akzo Nobel NV

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pigment Dispersion Market Segmentation

By Pigment Type

- Organic Pigment Dispersions

- Inorganic Pigment Dispersions

- Effect Pigment Dispersions

By Dispersion Type

- Water-Based Dispersions

- Solvent-Based Dispersions

- Oil-Based Dispersions

- Plasticizer-Based Dispersions

By Application

- Paints & Coatings

- Printing Inks

- Plastics

- Textiles

- Construction Materials

By End-Use Industry

- Packaging & Graphic Arts

- Automotive & Transportation

- Building & Construction

- Consumer Goods & Electronics

- Healthcare & Medical Devices

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Pigment Dispersion Industry

- BASF SE

- Sudarshan Chemical Industries Ltd.

- Clariant AG

- DIC Corporation

- Altana AG

- Heubach Group

- Evonik Industries AG

- Trinseo PLC

- Pidilite Industries Ltd.

- Arxada

- Lubrizol Corporation

- Sherwin-Williams Company

- Toyo Ink SC Holdings Co. Ltd.

- Lanxess AG

- Akzo Nobel NV

*- List not Exhaustive