Colorants Market Outlook 2025–2034: $115.6 Billion to $195.3 Billion at 6% CAGR Driven by Sustainable Pigments, NIR Detectability, and Natural Color Expansion

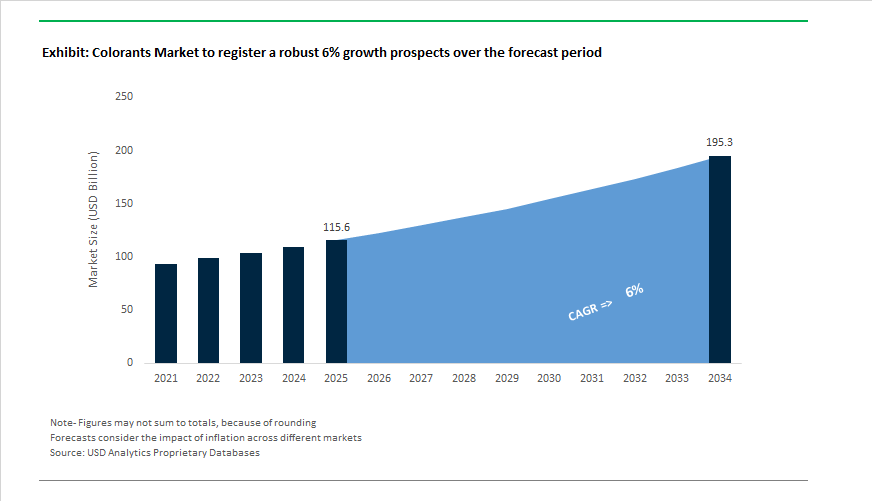

The global Colorants Market is projected to grow from $115.6 billion in 2025 to $195.3 billion by 2034, registering a CAGR of 6%. Growth is being driven by rising demand for high-performance pigments, dyes, aluminum effect pigments, and natural color concentrates across plastics, coatings, packaging, automotive, food, and healthcare applications. Increasing regulatory scrutiny on PFAS, heavy metals, synthetic dyes, and carbon-intensive manufacturing is accelerating innovation in bio-based, NIR-detectable, recyclable-compatible, and low-emission color technologies. At the same time, consolidation among global pigment leaders is reshaping supply chain control and global distribution networks.

Industry consolidation intensified in March 2025, when Sudarshan Chemical Industries Limited finalized the acquisition of Germany’s Heubach Group in a transaction valued at approximately ₹1,180 crore upfront. The deal created the world’s second-largest pigment producer, expanding operations across 19 international sites and significantly increasing combined revenue scale. In December 2025, ALTANA AG secured €300 million in financing from the European Investment Bank to fund sustainable R&D projects from 2025 to 2028, focusing on next-generation colorants that reduce greenhouse gas emissions and eliminate hazardous substances such as PFAS. In December 2024, Runaya and ECKART entered a strategic alliance to establish a sustainable aluminum pigment facility in India, targeting aerospace and solar markets with lower-carbon manufacturing processes. These structural investments reinforce long-term capacity and technology advancement across metallic and specialty pigment segments.

Performance-driven innovation and regulatory compliance accelerated in 2024–2026. In October 2024, BASF Coatings introduced its ROUTING 2024–2025 Automotive Color Trends collection, incorporating carbon-negative components, renewable raw materials, and biodegradable pigments optimized for infrared sensor compatibility in autonomous vehicles. In October 2025, Sun Chemical launched FASTOGEN Super Red BBF at K 2025, engineered for HDPE injection molding with high saturation, low haze, and strong heat resistance to meet strict EU food-contact standards. During the same month, Sun Chemical introduced Spectrasense Black 0089 FK, a near-infrared transparent black pigment that enables dark plastics to be detected and sorted in recycling systems, supporting 2026 circular economy objectives. DIC Corporation and Sun Chemical showcased Paliocrom Brilliant Ruby L 3558 in November 2025, delivering high hiding power and brilliance for automotive and industrial coatings.

Natural color expansion and supply chain transparency became prominent growth drivers. In November 2025, California Natural Color scaled its Crystal-Color technology to produce stable, high-strength natural color concentrates derived from fruits and vegetables, enabling food brands to replace synthetic dyes such as Red No. 3 and Red No. 40. In September 2025, GNT Group expanded its Exberry plant-based color portfolio in Asia-Pacific, introducing heat-stable reds and yellows sourced from non-GMO carrots and safflower for plant-based meat and beverage applications. Clariant accelerated commercialization of its antimony-free AddWorks® titanium catalyst solutions in late 2024–2025, addressing supply disruptions following China’s export restrictions on antimony. In March 2025, Clariant integrated AI-powered Clarita into its reporting framework to manage compliance with European Sustainability Reporting Standards, enhancing traceability across pigment supply chains. In January 2026, Avient introduced GlideTech™ non-PFAS color and functional concentrates for medical devices, aligning healthcare applications with stringent chemical safety mandates. These developments indicate sustained mid-single-digit growth through 2034, supported by circular pigment technologies, heavy-metal elimination, plant-based color innovation, and digital compliance integration across global end-use industries.

Colorants Market Trends and Drivers

Rapid Regulatory Phase-Out of Legacy Pigments Triggering Reformulation and Portfolio Realignment

The Colorants Market is entering a decisive regulatory era, where compliance—not aesthetics—is the catalyst for product reformulation, procurement shifts, and pricing power. Governments worldwide are increasingly restricting the use of heavy metals, perylene structures, and toxic intermediates across consumer and industrial colorant applications.

In January 2025, the U.S. EPA proposed a TSCA Risk Management Rule targeting C.I. Pigment Violet 29 (PV29)—a pigment widely used in automotive coatings and plastics—mandating strict occupational exposure controls across manufacturing and downstream processing. This is driving manufacturers to reroute R&D budgets toward next-generation pigment synthesis that is compliant by design.

Similarly, under EU REACH CMR Category 1B restrictions effective September 1, 2025, substances including Diuron and phosphonium salts are restricted for public-facing products unless below threshold concentrations—forcing formulators to transition toward low-toxicity, long-term stable pigment frameworks.

High-Purity Functional Colorants Tailored for E-Mobility, 5G Electronics, and Thermal Optimization

A second transformation underway is the rise of functionally engineered colorants—pigments defined not by hue, but by electrical, thermal, and safety performance.

In the e-mobility ecosystem, Evonik and peers are delivering high-purity dielectric-safe colorants for EV battery connectors, power busbars, and high-voltage wiring. New engineered systems, such as VESTAMID® PA12, retain dielectric breakdown strength stability even after 1,000 hours of thermal aging—supporting safety-critical visibility standards such as Safety Orange for high-voltage components.

Parallel demand is emerging for Cool Pigment NIR-reflective colorants in automotive coatings and architectural façades. As of 2025, functional colorants that reflect NIR radiation have demonstrated up to 20% reduction in cabin heat load, directly lowering air-conditioning energy consumption and extending EV driving range—making color a measurable contributor to energy efficiency KPIs.

Bio-Based and Nature-Derived Colorants for Sustainable & Low-Energy Textiles

Bio-based pigment development is rapidly transitioning from pilot scale to industrial deployment, supported by chem-tech venture funding and textile-sector sustainability mandates.

In June 2025, French startup EverDye closed a €15-million Series A round to scale microorganism-derived pigments that enable room-temperature textile coloration, reducing dyeing energy demand by ~3× and eliminating heavy-metal contamination—a breakthrough aligned with the US$54.21-billion global bio-textile segment.

Government policy is acting as an accelerant. Under India’s GREAT scheme (December 2025), 24 textile innovation startups received grants targeting algae-derived leather coatings, bio-camouflage dyes, and cold-weather functional textiles—positioning India as a demand hub for scalable low-carbon and non-toxic dyeing technologies.

Photochromic and Thermochromic Smart Colorants for Packaging Intelligence and Real-Time Safety Monitoring

A high-margin growth pool is emerging in responsive colorants—pigments that dynamically change state in response to temperature or light, enabling real-time product authentication, safety signaling, and compliance monitoring.

Thermochromic leuco-dye systems are increasingly used in pharmaceutical and food cold-chain logistics to visually signal temperature breaches for biologics, vaccines, and perishable goods—bridging the gap between quality assurance and consumer trust.

Industrial assets are also adopting reversible thermochromic and photochromic pigments in battery-test strips, firefighting apparel, helmet surfaces, and automotive dashboards—changing color to indicate overheating and reverting once conditions normalize.

This signals a shift where colorants become embedded safety systems, not merely surface finishes—creating a premium category insulated from price-competition.

Colorants Market Share and Segmentation Insights

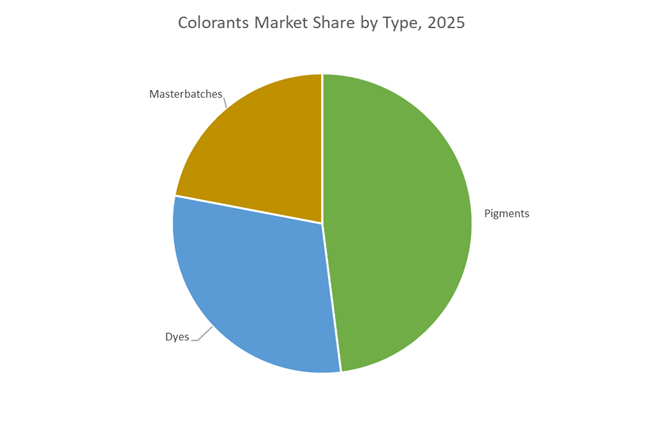

Type Distribution: Pigments Lead Durability Needs While Masterbatches Accelerate Plastics Adoption

Pigments hold 48% of colorants market share in 2025, driven by their insolubility, high opacity, lightfastness, and weather resistance across paints, coatings, plastics, and printing inks. Both inorganic and organic pigments remain the preferred choice where long-term color stability and coverage are critical. Dyes represent a significant segment, valued for solubility and ability to impart vibrant, transparent shades in textiles, paper, leather, and food applications where coloration must penetrate the substrate. Masterbatches form a rapidly expanding category, offering concentrated pigment or additive dispersions in carrier resins that enable clean handling, precise dosing, and process efficiency in plastics manufacturing. Growth is strongest in packaging and consumer goods, where automation and consistency are essential. Across all types, demand is shifting toward high-performance colorants with enhanced heat stability, chemical resistance, and regulatory compliance, supporting advanced applications in automotive, healthcare plastics, and sustainable packaging.

End-Use Industry Breakdown: Paints Lead Volume as Plastics and Packaging Gain Strategic Importance

Paints and coatings account for 28% of global colorant consumption, primarily pigments, supporting architectural aesthetics, industrial branding, and protective coatings where color also signals safety or formulation type. Textiles remain a major dye consumer, driven by reactive and disperse dyes for natural and synthetic fibers, with sustainability initiatives reshaping dyeing technologies. Plastics and rubber rely heavily on pigments and masterbatches for automotive components, electronics, and medical devices requiring thermal and UV stability. Packaging represents a high-growth segment, using masterbatches for branding, UV blocking, and shelf appeal amid expanding e-commerce and sustainable packaging trends. Printing inks consume both pigments and dyes for publishing, labels, and flexible packaging, with digital printing driving new formulations. Personal care and cosmetics demand high-purity, skin-safe colorants, while food and beverages, though smaller, are rapidly transitioning from synthetic dyes to natural color sources to meet clean-label expectations.

Competitive Landscape of the Colorants Market

The Colorants Market is led by vertically integrated chemical majors and specialty pigment innovators advancing ZeroPCF production, PFAS-free chemistries, sustainable dyes, and conductive colorant systems. Competitive differentiation centers on automotive interference pigments, eco-certified textile dyes, food-grade natural blues, and specialty carbons for EV batteries and electronics. Market leaders are accelerating capacity expansion in Asia, embedding AI in color matching, and pivoting toward bio-based and circular platforms. Strategic priorities increasingly focus on decarbonization, regulatory-compliant formulations, and high-fastness performance for cosmetics, construction plastics, textiles, and advanced mobility applications.

BASF advances ZeroPCF pigments with Automotive Color Trends and Verbund integration

BASF remains a dominant force in high-performance colorants, leveraging its Verbund production model to serve automotive, cosmetics, construction, and plastics markets. In its 2025–2026 “DRIVING THE PROXY” Automotive Color Trends collection, BASF introduced Tesseract Blue, a multidimensional shade using advanced interference pigments for enhanced visual depth. Strategically, BASF is transitioning its colorants portfolio toward ZeroPCF using renewable energy and biomass-balanced feedstocks. Key offerings include Aloversil™ cosmetic pigments and Bayferrox® and Colortherm® inorganic colorants. The company announced production capacity expansion in Mangalore, India in early 2026, targeting surging South Asian demand for sustainable coating and plastic coloration systems.

Archroma leads Cleaner Chemistry with EarthColors and low-impact denim solutions

Archroma is the global benchmark for sustainable textile dyes, pioneering Cleaner Chemistry by removing formaldehyde, aniline, and PFAS from its core portfolios. Its EarthColors® platform delivers high-performance dyes derived from non-edible agricultural waste such as nut shells and leaves. At major 2026 trade shows, Archroma debuted DIRSOL® RD chemistry, enabling laser-friendly denim with high-contrast black and indigo effects while reducing environmental impact by 57%. The company also advances AVITERA® SE dyes, cutting water and energy consumption during textile processing and supporting zero-discharge manufacturing goals across global fashion supply chains.

DIC scales organic pigments through Tree-to-Ink integration and AI automation

Following acquisition of BASF’s Colors and Effects business, DIC emerged as a vertically integrated powerhouse in organic pigments and printing inks. Its Tree-to-Ink model spans chemical precursors through finished pigments for electronic displays and specialty inks. In February 2026, DIC launched Phase 2 of Vision 2030, prioritizing Green, Digital, and Quality-of-Life businesses. Key innovations include LINABLUE® Wonder, a natural spirulina-derived blue food colorant produced via smart farming. DIC is also investing aggressively in AI and robotics partnerships to automate color matching and enhance production precision, reinforcing leadership in sustainable, digitally enabled pigment manufacturing.

Clariant delivers PFAS-free specialty colorants for regulated industries

Clariant has repositioned as a pure-play specialty chemicals leader, focusing on additives and color solutions for healthcare, automotive, and 5G infrastructure. In early 2026, the company finalized a completely PFAS-free additive portfolio, supporting brands navigating strict EU and North American environmental regulations. Clariant is expanding its Care Chemicals business via a global joint venture to serve emerging markets with bio-based surfactant systems. Guided by its “Greater Chemistry between People and Planet” strategy, Clariant targets 4 to 6% organic sales growth through 2026 by emphasizing premium formulations, regulatory compliance, and decarbonized colorant technologies.

Cabot strengthens conductive black leadership for EV and electronics markets

Cabot is the world’s leading producer of carbon black and specialty carbon colorants, supplying jet-black and conductive solutions for automotive, energy, and electronics applications. In February 2026, Cabot completed acquisition of Mexico Carbon Manufacturing, securing its Americas supply chain for specialty black concentrates. Its portfolio includes carbon nanotubes and graphenes used as conductive colorants in EV battery systems and electromagnetic shielding. Cabot is also investing heavily in low-VOC inkjet colorants and next-generation specialty carbons aligned with 2026 safety standards. Deep vertical integration enables unmatched batch consistency across high-performance black coatings.

Huntsman shifts toward circular, high-fastness performance colorant systems

Huntsman is a key supplier of chemical intermediates and performance additives that enhance durability and fastness across modern colorant systems. With approximately USD 6 billion in 2025 revenue and more than 55 global facilities, Huntsman serves demanding automotive and aerospace sectors requiring resistance to extreme UV exposure and temperature cycling. In 2026, the company advanced a circularity roadmap, developing additives that enable easier plastic recycling without sacrificing color intensity. Its Differentiation over Commodities strategy prioritizes patent-protected, high-value performance chemistry over standard dyes, strengthening Huntsman’s position in advanced, application-specific coloration solutions.

India: Global Consolidation and Export-Driven Colorant Leadership

India’s colorants industry has entered a structurally transformative phase, marked by global consolidation, export acceleration, and rapid adoption of sustainable color technologies. A defining milestone was achieved in March 2025 when Sudarshan Chemical completed the acquisition of Heubach Group, creating one of the world’s largest pigment platforms with 19 manufacturing sites. This transaction has repositioned India as a central hub for organic pigment innovation, particularly in high-performance applications spanning coatings, plastics, and inks. The integration of European formulation expertise with India’s scale-efficient manufacturing base is reshaping global supply chains for specialty colorants.

Parallel investments are strengthening India’s natural and food-grade colorant capabilities. In February 2025, Oterra A/S commissioned a dedicated blending and application center in Kerala to serve Middle Eastern and Asia-Pacific markets with natural yellow, orange, and red colorants. Export policy support remains a key enabler. The NITI Aayog reported that dye and intermediate exports reached $824.77 million during April to July 2025, supported by the RoDTEP scheme extended through 2026. India also retains global leadership in reactive dye exports, with more than 122,105 annual shipments serving cotton and silk apparel manufacturers worldwide. Sustainability-driven innovation is gaining traction, as Octarine Bio partnered with regional textile leaders in 2025 to scale microbial-fermented bio-dyes under the PurePalette platform, delivering substantial carbon reductions versus conventional synthetic dyes. Regulatory tightening is reinforcing quality leadership, with the Ministry of Chemicals and Fertilizers enforcing mandatory BIS certification for over 150 chemical products in late 2025 to curb substandard industrial colorants.

United States: High-Value Pigments and Sustainable Additives Under Trade Pressure

The United States colorants industry is evolving toward high-value specialty pigments, sustainability-focused additives, and domestic capacity expansion driven by trade dynamics. In December 2025, Vibrantz Technologies announced Infinity Blue as its 2026 Color of the Year, a formulation engineered for cross-industry use in architectural coatings and thermoset plastics. Such aesthetic leadership underscores the U.S. role in trend-setting color development rather than commodity dye production.

Sustainability and recycling compatibility are becoming core differentiators. At Compounding World Expo 2025, Holland Colours Americas Inc. introduced sustainable additives designed to preserve color vibrancy while improving mechanical performance in recycled PET streams. The clean-label movement is also reshaping cosmetic colorants. Sensient Technologies expanded its botanical pigment portfolio in 2025, prioritizing plant-extract-based alternatives to synthetic azo dyes for cosmetics. Trade policy has had a measurable impact. Reciprocal tariffs implemented in early 2025 increased costs for paint and ink producers, accelerating investment in domestic specialty pigment manufacturing. Innovation at the performance frontier continues, with Huntsman Corporation launching next-generation high-heat-resistant pigments for electric vehicle battery enclosures, reflecting growing demand from advanced mobility applications.

Germany: Smart Pigments, Circular Colorants, and Energy-Efficient Dyeing

Germany remains a global technology anchor for advanced pigment science, with innovation increasingly aligned to mobility, circularity, and low-impact processing. In late 2025, BASF SE commissioned an AI-driven production line focused on smart pigments optimized for autonomous vehicle sensor systems, including Lidar-reflective color solutions. This capability positions Germany at the forefront of functional colorants for next-generation automotive platforms.

Consumer-facing applications are also evolving under regulatory pressure. Early 2026 data indicates a strong shift toward ammonia-free botanical hair colorants, driven by stringent EU cosmetic regulations favoring chemically milder formulations. Circularity is a parallel priority. Lanxess AG introduced solvent-free colorants in 2025 that are compatible with both biodegradation and mechanical recycling, supporting EU circular economy targets for 2026. Resource efficiency in textiles is another focal point. Archroma scaled its AVITERA SE dyeing technology in 2025, enabling significant reductions in water and energy use for cellulosic fiber coloration. Collectively, these developments reinforce Germany’s leadership in high-technology, regulation-aligned colorant systems.

China: Volume Leadership with Accelerating Green and Digital Transitions

China continues to dominate global colorant supply by volume, while simultaneously reengineering its industry toward greener and more digitally compatible products. Trade data from late 2025 confirms that China exported over 18,378 shipments of textile dyes in a single quarter, maintaining its position as the primary supplier of disperse and acid dyes for global textile manufacturing. However, policy priorities are shifting. Under the national Petrochemical Industry Roadmap, the Chinese government allocated more than $100 million in 2025 to convert legacy dye-intermediate facilities into green chemistry hubs, targeting reductions in industrial wastewater pollution.

Demand patterns are also changing downstream. In 2025, China’s packaging sector recorded a strong rise in the adoption of inkjet-compatible colorants, driven by the expansion of high-speed digital printing for customized packaging. This transition is increasing demand for colorants with precise particle size control, fast curing, and substrate versatility. As a result, China’s colorants industry is balancing its traditional scale advantage with growing emphasis on sustainability and digital performance.

Vietnam: Import-Driven Growth Supporting Global Apparel Supply Chains

Vietnam has emerged as a critical demand center in the global colorants industry, driven by rapid expansion in apparel and footwear manufacturing. In the 2025 fiscal year, the country recorded over 37,218 shipments of imported textile colorants, reflecting its role as one of the world’s largest importers. This surge is directly linked to Vietnam’s growing importance as an export-oriented manufacturing base for global fashion brands, where consistent color quality and fast turnaround times are essential. While domestic colorant production remains limited, Vietnam’s scale of imports is shaping regional trade flows and reinforcing Asia’s position as the epicenter of textile coloration demand.

Comparative Snapshot: Country-Level Strategic Positioning in the Colorants Industry

Colorants Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Primary End-Use Sectors

|

Direction of Colorant Evolution

|

|

India

|

Global consolidation and exports

|

Textiles, coatings, food colors

|

Organic pigments, bio-dyes, export-grade compliance

|

|

United States

|

Specialty and sustainable pigments

|

Coatings, plastics, cosmetics

|

Botanical, recycled-content-compatible colorants

|

|

Germany

|

Smart and circular pigments

|

Automotive, textiles, cosmetics

|

AI-optimized, solvent-free, low-impact systems

|

|

China

|

High-volume supply with green shift

|

Textiles, packaging

|

Green chemistry and digital-print-ready dyes

|

|

Vietnam

|

Import-led manufacturing growth

|

Apparel and footwear

|

High-throughput textile dye consumption

|

Colorants Market Report Scope

Colorants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$115.6 Billion

|

|

Market Size (2034)

|

$195.3 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Type (Pigments, Dyes, Masterbatches), By Physical Form (Powdered Colorants, Liquid Dispersions, Granular and Pelletized Formats, Paste and Slurry), By Source of Origin (Synthetic, Natural and Bio-based, Recycled and Circular), By End-Use Industry (Textiles, Packaging, Paints and Coatings, Plastics and Rubber, Food and Beverages, Personal Care and Cosmetics, Printing Inks)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Sudarshan Chemical Industries Limited, DIC Corporation, Clariant AG, Archroma AG, Huntsman Corporation, LANXESS AG, Avient Corporation, Sensient Technologies Corporation, Cabot Corporation, DyStar Group, Tronox Holdings plc, Kronos Worldwide Inc., Kiri Industries Limited, Meghmani Organics Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Colorants Market Segmentation

By Type

- Pigments

- Dyes

- Masterbatches

By Physical Form

- Powdered Colorants

- Liquid Dispersions

- Granular and Pelletized Formats

- Paste and Slurry

By Source of Origin

- Synthetic

- Natural and Bio-based

- Recycled and Circular

By End-Use Industry

- Textiles

- Packaging

- Paints and Coatings

- Plastics and Rubber

- Food and Beverages

- Personal Care and Cosmetics

- Printing Inks

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Colorants Industry

- BASF SE

- Sudarshan Chemical Industries Limited

- DIC Corporation

- Clariant AG

- Archroma AG

- Huntsman Corporation

- LANXESS AG

- Avient Corporation

- Sensient Technologies Corporation

- Cabot Corporation

- DyStar Group

- Tronox Holdings plc

- Kronos Worldwide Inc.

- Kiri Industries Limited

- Meghmani Organics Limited

*- List not Exhaustive