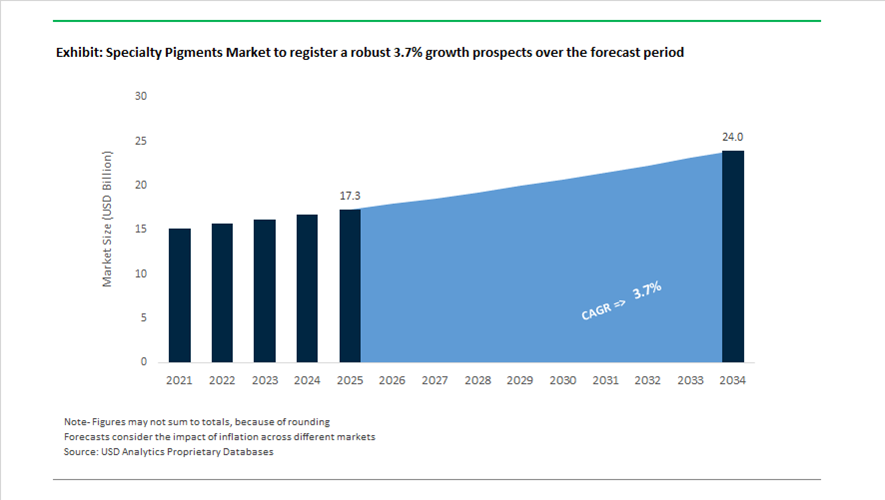

Specialty Pigments Market Valuation 2025–2034: $17.3 Billion to $24 Billion at 3.7% CAGR Shaped by Global Consolidation, Effect Pigments, and Automotive Color Innovation

The global specialty pigments market is valued at $17.3 billion in 2025 and is projected to reach $24 billion by 2034, expanding at a CAGR of 3.7%. Growth is anchored in rising demand for high-performance organic pigments, pearlescent pigments, metallic effect pigments, interference pigments, automotive basecoat pigments, and cosmetic-grade clean-label colorants. Specialty pigments deliver enhanced chroma, opacity, durability, and optical effects across automotive coatings, industrial paints, plastics, inks, cosmetics, and advanced functional surfaces. The competitive landscape is being reshaped by cross-border acquisitions, portfolio rationalization, radar-transparent technologies for autonomous vehicles, and bio-based printing inks aligned with sustainability mandates.

Strategic realignment accelerated in 2024. Effective January 1, 2024, ECKART completed a corporate restructuring, transferring its rheology additives business to BYK and concentrating exclusively on effect pigments and high-purity fillers for beauty and personal care markets. In July 2024, Merck KGaA signed a definitive agreement to divest its global Surface Solutions pigments business to Global New Material International for €665 million. In October 2024, Sudarshan Chemical Industries announced its ₹1,180 crore acquisition of the Heubach Group, strengthening its global presence in organic pigments and performance colorants. At the 2024 American Coatings Show, Sun Chemical introduced Paliocrom Brilliant Ruby EH 5050, an iron-oxide-coated aluminum effect pigment engineered for intense bluish-red brilliance and superior hiding power in automotive basecoats.

The consolidation phase matured in 2025. In March 2025, Sudarshan completed the Heubach acquisition, creating the world’s second-largest pigment manufacturer with 19 international production sites and an expanded high-performance pigment portfolio. The same month, Sudarshan confirmed that its Fairless Hills, Pennsylvania facility would serve as a strategic manufacturing hub to mitigate potential U.S. reciprocal tariff exposure. In March 2025, Sun Chemical launched Chione Electric Scarlet and Chione Electric Sienna, vegan and carmine-free metallic pigments designed for the growing clean beauty cosmetics segment. In early 2025, ECKART introduced the METALSTAR Eco and TOPSTAR Eco printing ink series, formulated with vegetable oils and fatty acid esters to replace mineral oils while maintaining metallic brilliance.

Advanced automotive and autonomous mobility applications defined late 2025 innovation. At the European Coatings Show 2025, ECKART launched SILVERSHINE Hydro Platinum and Titanium Grey, radar-transparent effect pigments that preserve sensor functionality in autonomous vehicles while delivering premium metallic finishes. In September 2025, BASF Coatings unveiled its “Driving the Proxy” 2026 color collection, highlighting Tesseract Blue, an interference pigment that shifts between green and violet hues to create multidimensional surfaces. Meanwhile, Shivtek Spechemi Industries announced a significant capacity expansion in early 2025, targeting fivefold revenue growth by 2030 through increased output of high-performance pigments for industrial coatings. The Merck divestiture finalized in July 2025 further repositioned GNMI as a dominant force in pearlescent pigments under the Susonity brand. These developments in metallic effect pigments, interference color technology, bio-based ink formulations, and global manufacturing consolidation are redefining competitive intensity and innovation pipelines in the specialty pigments market through 2034.

Key Trends and High-Value Opportunities in the Specialty Pigments Market

Energy-Efficiency Mandates Accelerating Adoption of Infrared-Reflective Cool Pigments

The Specialty Pigments Market is experiencing a structurally driven surge in demand as energy-efficiency regulations convert sustainability goals into enforceable building code requirements. The California Energy Commission has finalized the 2025 Building Energy Efficiency Standards under Title 24, Part 6, effective January 1, 2026, mandating the use of materials that enable passive radiative cooling. This regulation has elevated Complex Inorganic Color Pigments as a non-discretionary input for architectural coatings, particularly in roofing and exterior wall applications where near-infrared reflectance is critical.

Across the U.S. Sunbelt, state and municipal authorities are enforcing updated roofing codes that require low-sloped roofs to achieve Solar Reflectance Index values ranging from 64 to 82, depending on climate zone. These thresholds effectively eliminate conventional carbon black pigments from compliant formulations, replacing them with infrared-reflective specialty pigments that maintain dark or neutral aesthetics while reflecting NIR radiation. This regulatory shift has transformed cool pigments from a niche green-building feature into a volume-driven compliance market.

From an economic perspective, the adoption case is reinforced by measurable operational savings. Data published by the Cool Roof Rating Council in 2025 indicates that buildings utilizing cool pigments can reduce annual HVAC energy consumption by up to 25% in residential applications and approximately 15% in commercial retail environments. As energy prices remain volatile, these performance metrics position specialty pigments as a direct contributor to lifecycle cost reduction and return on investment for building owners.

OEM-Led Specification of Interference and Liquid-Metal Effects in Electric Vehicles

In the automotive sector, specialty pigments are increasingly specified as strategic design elements rather than discretionary aesthetic choices. Electric vehicle platforms, characterized by smooth, aerodynamic body panels and reduced mechanical differentiation, rely heavily on surface appearance to convey technological sophistication. As a result, automotive OEMs are formalizing long-term supply agreements for multi-color interference pigments and liquid-metal visual effects that deliver consistent appearance across global production footprints.

BASF Coatings’ 2025–2026 automotive color collection, Driving the Proxy, illustrates this shift through pigments such as Tesseract Blue, which employ advanced interference chemistry to generate multidimensional color shifts between blue, green, and violet. These effects are being optimized to maintain visual depth without compromising sensor compatibility, ensuring that advanced driver-assistance systems and LiDAR performance remain unaffected.

Similarly, PPG’s 2025 Automotive Color Report highlights growing consumer demand for kinetic textures and layered sparkle, exemplified by flagship shades such as Purple Basil. This trend is accelerating the use of mica-based pearlescent pigments and engineered glass-flake systems that deliver premium visual complexity without the weight, corrosion risk, or recyclability concerns associated with traditional metallic pigments. For pigment manufacturers, this represents a sustained demand pull from premium and mid-range EV segments seeking differentiation through surface innovation.

Regulatory Replacement Demand for Heavy-Metal-Free Pigment Systems

One of the most immediate and scalable opportunities in the Specialty Pigments Market stems from regulatory-driven substitution of legacy heavy-metal pigments. European Commission Regulation (EU) 2025/1731, fully effective from September 2025, has tightened restrictions on Carcinogenic, Mutagenic, and Reproductive Toxic substances across consumer-facing applications. This has triggered mandatory reformulation in toys, household goods, and decorative coatings.

Revisions to the EN 71 Toy Standards in October 2025, followed by the EU Toy Safety Regulation 2025/2509 published in December 2025, introduced Digital Product Passports that require full chemical transparency across the value chain. These measures are accelerating the replacement of lead-chromate and cadmium-based pigments with high-performance organic alternatives such as quinacridones and diketopyrrolopyrrole reds, which deliver comparable color strength, heat resistance, and lightfastness.

Parallel enforcement in the United States is reinforcing this shift. California’s Proposition 65 list expanded to approximately 900 chemicals by mid-2025, with new settlement thresholds for lead in art pigments and ceramic decorations set at 90 ppm or lower. This regulatory environment is creating a multi-billion-dollar replacement market for pigment producers capable of delivering non-toxic, high-chroma alternatives that meet both performance and compliance criteria.

Security and Smart Pigments for Anti-Counterfeiting in Pharma and Luxury Goods

Rising counterfeit activity, estimated by the OECD to represent roughly 2.3% of global imports, is driving demand for advanced security pigments across pharmaceutical and luxury packaging. Brand owners are increasingly integrating overt and covert optical features directly into inks, coatings, and polymer substrates to create multi-layered authentication systems that are difficult to replicate.

In the pharmaceutical sector, implementation of the U.S. Drug Supply Chain Security Act is accelerating the adoption of layered security architectures that combine thermochromic, photoluminescent, and forensic pigments within blister packs and labels. By 2025, security ink technology has evolved to incorporate carbon dots and molecular taggants that generate a unique optical fingerprint, enabling rapid field verification and forensic-level traceability.

Beyond authentication, smart pigments are being deployed as functional quality indicators. Industry reviews published in late 2025 highlight the growing use of colorimetric pigments that visually signal temperature excursions in vaccines and biologics. These pigments merge anti-counterfeiting with condition monitoring, allowing stakeholders to verify both product authenticity and cold-chain integrity at the point of use. For specialty pigment suppliers, this convergence of security, compliance, and functional performance represents one of the highest-margin growth avenues in the current market landscape.

Specialty Pigments Market Share and Segmentation Insights

High-Performance Organic Pigments Lead the Specialty Pigments Market for Durability and Color Performance

High-performance organic pigments accounted for 34.80% of the specialty pigments market in 2025, reflecting their strong adoption in applications requiring superior color stability and durability. Pigment classes such as quinacridones, phthalocyanines, diketopyrrolopyrroles (DPP), and perylene pigments deliver excellent heat resistance, chemical stability, and long-term color retention. These properties make them widely used in automotive coatings, industrial coatings, and engineering plastics, where pigments must maintain appearance under harsh environmental conditions. A significant 2025 market trend is the increasing demand for advanced automotive color technologies, where new pigment chemistries enable vibrant shades, deep chromatic colors, and complex visual effects used by automakers to differentiate vehicle models.

Automotive Coatings Segment Drives Specialty Pigment Consumption for Premium Vehicle Finishes

Automotive coatings represent the largest application segment in the specialty pigments market, accounting for 34.80% of total demand in 2025 due to the stringent performance requirements of automotive paint systems. Vehicle coatings require pigments that provide long-term weather resistance, color consistency, UV stability, and scratch resistance while maintaining premium aesthetic quality. Automotive manufacturers increasingly use advanced pigment systems to create distinctive finishes that support brand identity. A key 2025 industry trend is the growing emphasis on electric vehicle color differentiation, where automakers develop unique color palettes, metallic effects, and color-shifting finishes to enhance product appeal while maintaining the durability standards required for exterior automotive coatings.

Specialty Pigments Market Competitive Landscape

The specialty pigments market in 2026 is defined by sustainable pigment innovation, radar-compatible coatings, and high-performance effect pigments. Industry leaders are advancing UHP cosmetic pigments, bio-based dispersions, and digital-ready color systems while leveraging consolidation, vertical integration, and regulatory-compliant formulations to capture high-growth automotive, electronics, and personal care applications.

DIC Corporation Expands Perylene Capacity and Integrates Sustainable Color Platforms for High-Performance Applications

DIC Corporation is strengthening its leadership in specialty pigments through the integration of BASF’s Colors & Effects business and expansion of high-performance pigment capacity. Sun Chemical’s Ludwigshafen expansion targets rising demand for perylene pigments in automotive coatings and industrial finishes. The 2026 organizational restructuring aligns functional products and color materials under a unified sustainable solutions platform. DIC maintains dominance in LCD color filters through its G58 pigment series, supporting 8K OLED and display technologies. The company is advancing low-VOC and bio-renewable pigment systems to comply with EU Green Deal standards. Its portfolio focuses on high-transparency, durable, and environmentally compliant pigment technologies.

BASF Accelerates Digital Color Leadership with LiDAR-Compatible Pigments and Circular Economy Integration

BASF is advancing specialty pigments through digital color innovation and sustainable chemistry integration. Its “DRIVING THE PROXY” automotive color collection introduces interference pigments like Tesseract Blue for multi-dimensional visual effects. PHYGITAL MAGNETAR technology enables liquid-metal finishes compatible with LiDAR and radar sensors for autonomous vehicles. BASF is increasing the use of recycled and renewable feedstocks in pigment production to meet circular economy targets. Its portfolio includes high-performance organic pigments such as Paliotol® and Irgazin®, alongside Paliocrom® effect pigments. The company is also expanding NIR-reflective pigments that enhance thermal management in architectural and automotive coatings.

Sudarshan Chemical Emerges as Global Pigment Titan Through Heubach Integration and Specialty Portfolio Expansion

Sudarshan Chemical Industries has become a global leader following the acquisition of Heubach Group, integrating 19 manufacturing sites worldwide. The company established a second headquarters in Frankfurt to manage expanded European and American operations. Its 2026 strategy focuses on shifting commodity production to India while transforming European sites into specialty pigment innovation hubs. The combined entity exceeds €1 billion in revenue, targeting over $50 million in operational synergies. Sudarshan offers a broad portfolio spanning high-performance pigments, anti-corrosive solutions, and UHP cosmetic pigments. Its specialization in high-performance pigments positions it strongly in automotive, coatings, and personal care sectors.

Venator Advances Titanium Dioxide Plus Strategy with Regulatory-Compliant and High-Performance Pigment Innovations

Venator Materials is focusing on advanced TiO₂ pigments that exceed regulatory and performance benchmarks. The launch of TIOXIDE® TR81 introduces TMP- and TME-free formulations aligned with global safety standards. Its HOMBITAN® and UV-TITAN® pigment lines target high-growth personal care applications, particularly SPF formulations. Venator’s V-PCF digital tool provides real-time carbon footprint data, supporting ESG-driven procurement decisions. The company operates across more than 109 countries, ensuring global supply reliability. Its specialty pigments enhance durability, dispersion, and energy efficiency in coatings and construction materials.

Altana’s ECKART Division Leads Radar-Transparent Pigment Innovation for Autonomous Mobility and Sustainable Coatings

Altana’s ECKART division is pioneering metallic and interference pigments tailored for autonomous vehicle technologies. Its radar-transparent pigment systems enable sensor-compatible automotive coatings critical for Level 4 autonomy. The company secured €300 million in EIB funding to accelerate sustainable pigment R&D. Innovations such as STANDART® Zinc Matt Black and ProFLAKE® Zn HYDRO provide corrosion resistance in water-based systems. ECKART’s AL-II pigment range delivers low product carbon footprint through recycled aluminum feedstocks. The division is advancing eco-friendly coatings aligned with electrification and sustainability megatrends.

Tronox Optimizes Vertical Integration and Cost Leadership Through Strategic TiO₂ Portfolio Rationalization

Tronox is enhancing its specialty pigment competitiveness through vertical integration and cost optimization strategies. The closure of its Fuzhou plant eliminates low-margin capacity and delivers $15 million in annual savings. The company reported $730 million in Q4 2025 revenue, with TiO₂ volumes increasing by 13% driven by demand in India and tariff-protected markets. Its mine-to-pigment integration ensures stable access to titanium and zircon feedstocks amid global volatility. Tronox leads in chloride-process TiO₂, preferred for high-end coatings and specialty plastics. Its focus on high-yield assets strengthens margin resilience and supply chain control.

China Specialty Pigments Market Shifting from Volume Scale to High-Value Effect Systems

China’s specialty pigments industry is undergoing a decisive transition from commodity-scale output toward value-dense, technology-driven pigment systems. A pivotal inflection point occurred in August 2025 when Global New Material International completed its €665 million acquisition of the Surface Solutions business from Merck KGaA. This transaction brought the Iriodin® pearlescent technology platform under Chinese ownership, signaling a strategic shift toward premium automotive, cosmetics, and electronics pigments rather than bulk inorganic volumes. Capacity expansion has followed technology acquisition. GNMI’s Tonglu synthetic mica facility, designed for 100,000 tons annually, reached full-scale operations in Q4 2025, strengthening China’s control over a critical substrate used in high-end effect pigments.

Upstream and regulatory dynamics are accelerating the quality upgrade. In November 2025, BASF commissioned a new CFRP-based dispersant line in Nanjing to stabilize nano-pigments for next-generation automotive finishes, reinforcing China’s role in advanced coating supply chains. At the same time, MIIT guidance is driving domestic producers toward ultra-high-purity pigments for OLED and micro-LED color filters. Environmental enforcement under the 2025 Blue Sky Chemical Mandate has eliminated small-scale lead-chromate facilities, forcing consolidation into compliant organic pigment systems. Trade pressure also plays a role. EU anti-dumping duties on Chinese TiO₂ have pushed producers to diversify into complex inorganic and hybrid pigments that sit outside bulk commodity classifications, improving margins and export resilience.

Germany Specialty Pigments Market Reorganizing Around Sustainability and Portfolio Focus

Germany remains a global benchmark for high-performance and sustainable pigment innovation, even as cost structures tighten. In October 2025, BASF and Carlyle agreed to carve out BASF’s coatings and specialty pigment units into a standalone entity valued at €7.7 billion. This restructuring is designed to insulate specialty color technologies from cyclical petrochemical exposure and allow sharper capital allocation toward premium applications in mobility, electronics, and industrial coatings.

Product innovation continues to anchor competitiveness. Schlenk Metallic Pigments commercialized Zenexo® GoldenShine in late 2024, a recycled-metal leafing pigment targeting consumer electronics aesthetics for the 2025–2026 cycle. Regulatory compliance remains a structural cost driver. Updates to REACH Annex XVII in 2025 increased synthesis costs for organic pigments by an estimated 12 to 18%, primarily due to stricter impurity thresholds. Concurrently, the EU PFHxA restriction adopted in 2024 has accelerated the transition toward aqueous pigment systems, positioning German suppliers as preferred partners for food packaging and textile applications entering the 2026 regulatory window.

India Specialty Pigments Market Emerging as a Consolidation and Export Platform

India’s specialty pigments industry has rapidly evolved from a regional supplier into a consolidation-driven global platform. In October 2024, Sudarshan Chemical Industries Limited announced the acquisition of the global pigment operations of Heubach Group for approximately €127 million. By January 2025, this integration positioned Sudarshan among the leading global producers of high-performance colorants and pigment preparations, with a portfolio spanning automotive coatings, plastics, and inks.

Export performance underscores the strategic shift. During the first half of fiscal 2025, Sudarshan reported 18% year-on-year revenue growth in its pigment division, with specialty grades accounting for nearly 70% of segment earnings. Regulatory tightening has further catalyzed innovation. India’s 2025 enforcement of stricter controls on 112 azo- and benzidine-based dyes has driven accelerated R&D into safer, high-durability organic pigments tailored for textile exports. Supporting this transition, the Department of Chemicals and Petrochemicals expanded its S&T Clusters initiative to 25 clusters in late 2025, providing shared infrastructure for advanced pigment synthesis and scale-up.

Japan Specialty Pigments Market Anchored in Electronics and Mobility Color Science

Japan continues to dominate the ultra-high-value end of the specialty pigments spectrum, particularly in electronics and mobility applications. In late 2025, DIC Corporation reported that shipments of high-value-added pigments for electronics and mobility solutions significantly supported its operating income, with FY2025 forecasts reaching ¥48 billion. Demand is being driven by pigments for LCD color filters, advanced displays, and electronic components requiring exceptional purity and thermal stability.

Automotive aesthetics remain a parallel growth vector. In October 2025, BASF Coatings Japan unveiled the Phygital Magnetar metallic shade for the Asia-Pacific 2026 automotive cycle, leveraging advanced liquid-metal effect pigments. Structurally, DIC is executing Phase 2 of its Vision 2030 strategy, reallocating capital toward next-generation businesses including bio-based pigments and functional pigments for battery thermal management, reinforcing Japan’s positioning at the intersection of color science and advanced materials.

United States Specialty Pigments Market Driven by EVs, Safety Regulation, and Durable Color Demand

The United States specialty pigments market is increasingly shaped by electric mobility, consumer safety regulation, and infrastructure-driven durability requirements. In 2025, Axalta Coating Systems launched a new range of low-energy-cure specialty pigments engineered for EV composite substrates. These pigments reduce curing temperatures and associated emissions, aligning refinish operations with decarbonization targets across the automotive value chain.

Regulatory signals are influencing formulation strategies nationwide. California’s Department of Toxic Substances Control proposed adding microplastic-containing colorants to its Candidate Chemicals List in July 2025, prompting a shift toward liquid-dispersed specialty pigments in cosmetics and personal care. Capacity investments are following demand for durability. In late 2025, Sun Chemical, part of DIC Group, announced expansions in perylene pigment production to support architectural and automotive coatings requiring long-term colorfastness under high UV exposure.

Comparative Snapshot: Specialty Pigments Industry by Country

Specialty Pigments Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Industry Drivers

|

Competitive Position

|

|

China

|

Effect pigments and electronics

|

M&A, synthetic mica, environmental enforcement

|

Scale upgrading to premium

|

|

Germany

|

Sustainable and compliant pigments

|

REACH, recycled metals, portfolio carve-outs

|

Regulatory and technology leader

|

|

India

|

Global consolidation and exports

|

Heubach acquisition, cluster infrastructure

|

Fast-rising global supplier

|

|

Japan

|

Electronics and mobility pigments

|

Display demand, advanced color science

|

Ultra-high-value niche leader

|

|

United States

|

EVs and durable coatings

|

Low-energy cure, safety regulation

|

Innovation-driven domestic market

|

Specialty Pigments Market Report Scope

Specialty Pigments Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.3 Billion

|

|

Market Size (2034)

|

$24 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Product Type (Special Effect Pigments, High-Performance Organic Pigments, Complex Inorganic Color Pigments, Functional Pigments, Specialty Carbon Blacks, Nano-Pigments), By Application (Automotive Coatings, Electronics and Displays, Cosmetics and Personal Care, Packaging and Printing Inks, Plastics and Textiles, Construction and Industrial Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DIC Corporation, Sudarshan Chemical Industries Limited, Global New Material International, BASF SE, Altana AG, Clariant AG, Toyo Ink SC Holdings Co., Ltd., Ferro Corporation, Schlenk Metallic Pigments GmbH, Heubach Group, Dainichiseika Color and Chemicals Mfg. Co., Ltd., The Chemours Company, Tronox Holdings plc, Cabot Corporation, Silberline Manufacturing Co., Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Pigments Market Segmentation

By Product Type

By Application

- Automotive Coatings

- Electronics and Displays

- Cosmetics and Personal Care

- Packaging and Printing Inks

- Plastics and Textiles

- Construction and Industrial Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Pigments Industry

- DIC Corporation

- Sudarshan Chemical Industries Limited

- Global New Material International

- BASF SE

- Altana AG

- Clariant AG

- Toyo Ink SC Holdings Co., Ltd.

- Ferro Corporation

- Schlenk Metallic Pigments GmbH

- Heubach Group

- Dainichiseika Color and Chemicals Mfg. Co., Ltd.

- The Chemours Company

- Tronox Holdings plc

- Cabot Corporation

- Silberline Manufacturing Co., Inc.

*- List not Exhaustive