Metallic Pigments Market 2025–2034: Recycled Aluminum Innovation, Radar-Transparent Automotive Effects, and Water-Based Zinc Technologies Driving $3.3 Billion Outlook at 5.6% CAGR

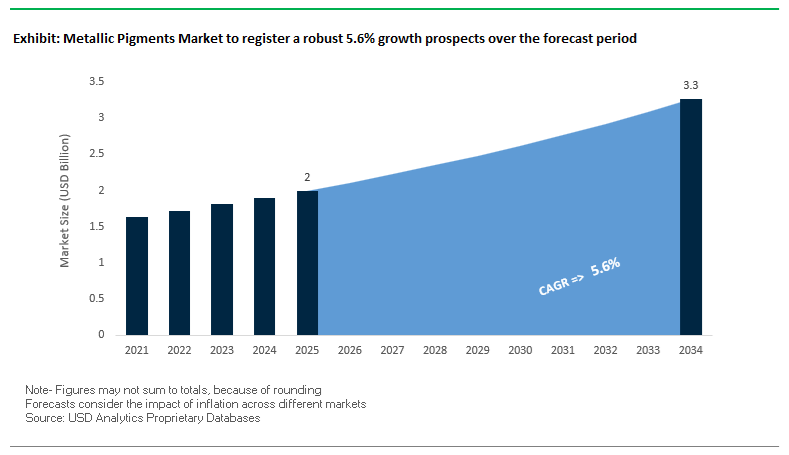

The Metallic Pigments Market is projected to grow from $2 billion in 2025 to $3.3 billion by 2034, registering a CAGR of 5.6%. Market expansion is being driven by increasing demand for aluminum effect pigments, pearlescent mica pigments, zinc flakes, and high-performance special effect pigments across automotive coatings, powder coatings, plastics, cosmetics, and architectural applications. Rising sustainability mandates, recyclability requirements, and the shift toward water-based and low-VOC coating systems are reshaping pigment chemistry and production processes. Automotive OEMs are demanding enhanced flop behavior, hiding power, and sensor compatibility, while packaging and cosmetics brands prioritize vegan-certified, circular, and low-carbon pigment solutions.

In January 2024, ALTANA agreed to acquire the Silberline Group, integrating it into its ECKART division and significantly strengthening global manufacturing and R&D capabilities in aluminum effect pigments. In early 2025, ECKART introduced SILVERSHINE Hydro Platinum and Titanium Grey, radar-transparent pigment pastes designed to maintain sensor functionality in autonomous vehicles. At the European Coatings Show in March 2025, ECKART launched ProFLAKE Zn HYDRO PM 3090, the first zinc flake pigment engineered specifically for water-based corrosion protection systems, enabling industrial coating manufacturers to transition away from solvent-heavy formulations without compromising anti-corrosion performance. In parallel, Sun Chemical expanded its Paliocrom portfolio in March 2025 with Premium Orange L 2900, delivering advanced flop characteristics for high-end automotive basecoats.

Sustainability and recyclability innovation intensified through 2025 and into 2026. In 2025, ECKART expanded its AL-II line produced from secondary aluminum, positioning it as one of the lowest product carbon footprint aluminum pigment solutions in the market. In late 2025, ECKART introduced NIR Silver technology to ensure metallic-look plastics remain detectable by near-infrared sorting systems, addressing recycling inefficiencies in packaging waste streams. Sun Chemical launched Glacier Exterior Ceramic White S1303M at ChinaCoat 2025, a synthetic mica-based pigment providing cool white sparkle effects for exterior coatings. In March 2025, Sun Chemical also introduced vegan, carmine-free metallic pigments for cosmetics, aligning with cruelty-free certification trends. In May 2025, Schlenk demonstrated its Zenexo Ultra-Thin Pigment technology for powder coatings, delivering liquid-metal aesthetics in low-emission systems. In February 2026, DIC Group and Sun Chemical showcased a unified aluminum and mica-based effect pigment portfolio at PAINTINDIA, targeting India’s expanding automotive and infrastructure coating markets.

Metallic Pigments Market Trends and Opportunities

Trend: Circular Economy–Compatible Metallic Pigments for PCR and Monomaterial Packaging

The Metallic Pigments Market is being structurally reshaped by circular economy regulations and brand-level sustainability commitments that prioritize post-consumer recycled content and monomaterial packaging. Traditional metallic pigments, particularly aluminum-based flakes, have historically posed challenges in recycling streams due to contamination risks, discoloration, and mechanical degradation of PCR polymers. As a result, pigment producers are now engineering system-compatible metallic pigments that preserve visual brilliance while remaining fully compatible with mechanical recycling processes.

A defining milestone in this transition was announced at the European Coatings Show 2025, where ECKART expanded its AL-II product line based on secondary aluminum feedstock. These recycled-aluminum pigments are positioned as having the lowest product carbon footprint in the metallic pigment category, directly supporting Scope 3 emissions reduction targets for global packaging and FMCG brands. In parallel, de-inkability has become a non-negotiable performance criterion. In June 2025, INX International showcased washable metallic ink systems engineered to fully separate during caustic wash cycles in PET recycling, enabling true bottle-to-bottle circularity under EU packaging mandates for 2025–2030.

Beyond recyclability, pigment innovation is also enabling the elimination of multi-layer foil laminates. Sun Chemical has deployed high-opacity metallic pigments within oxygen-barrier coatings such as Ecostage™ GB-XA, allowing single-layer polyolefin films to replicate the appearance and barrier properties of aluminum laminates. This shift materially reduces packaging complexity while preserving recyclability, positioning metallic pigments as a functional enabler of circular packaging rather than a barrier.

Trend: Automotive Standardization Around Radar Transparency and Ultra-High Durability

The rapid evolution of autonomous driving systems and shared mobility fleets is redefining performance benchmarks for metallic pigments used in automotive coatings. Beyond aesthetics, pigments must now deliver radar transparency to avoid interference with LiDAR and radar sensors, alongside exceptional long-term weatherability to support extended vehicle service lives and fleet utilization models.

In March 2025, ECKART introduced radar-transparent pigment solutions such as SILVERSHINE Hydro Platinum and Titanium Grey, specifically engineered to maintain signal integrity for advanced driver-assistance systems. These developments address a critical OEM concern, as metallic finishes that distort sensor signals can compromise vehicle safety systems and fail homologation requirements. At the same time, durability expectations have risen sharply. Updated SAE J2527 and GM 9125P specifications for 2025 now require metallic pigments to withstand 5,000 hours of accelerated xenon arc exposure, equivalent to roughly seven years of outdoor service, with a color deviation of less than ΔE 2.0.

To meet these thresholds, pigment suppliers are deploying acrylic-modified metallic pastes such as the STAPA® HD series, optimized for compatibility with modern waterborne basecoats and resistance to chemical stressors including acid rain, industrial fallout, and biological contaminants. These advances support the industry’s move toward 10-plus-year exterior coating warranties, particularly for electric and shared vehicles designed for prolonged operational lifecycles.

Opportunity: EMI-Shielding Metallic Pigments for 5G and Wearable Electronics

The densification of 5G-enabled electronics and the rise of wearables are opening a high-margin opportunity for metallic pigments that provide electromagnetic interference shielding without introducing electrical conductivity risks. As devices operate at millimeter-wave frequencies, susceptibility to EMI has increased sharply, particularly in defense, telecommunications, and medical electronics.

Silver-coated glass and nickel flake pigments are gaining traction as functional fillers within polymer housings, delivering shielding effectiveness while avoiding short-circuit risks associated with bulk metal components. In 2025, demand for specialized EMI-shielding pigments increased by 9.3% in the U.S. defense and telecom sectors, reflecting regulatory requirements for reliability in complex electromagnetic environments. Importantly, these pigments align with the broader lightweighting trend, as conductive polymers and composites are projected to be among the fastest-growing material classes through 2030. Metallic pigments that combine EMI shielding with flexibility and low density are therefore positioned as critical enablers for foldable devices, smart skins, and next-generation wearable platforms.

Opportunity: High-Infrared-Reflective Pigments for Urban Heat Island Mitigation

Urban climate resilience initiatives are creating strong demand for metallic pigments with high near-infrared reflectance in architectural coatings. Under LEED v4.1 standards and municipal cool-roof programs, coatings are increasingly required to reduce solar heat gain without constraining architectural design.

A February 2025 study published via ResearchGate demonstrated that coatings incorporating high-IR-reflective metallic pigments reduced building surface temperatures by up to 34.2°C, corresponding to a 53.6% reduction in peak heat exposure and translating into 10–30% lower air-conditioning energy consumption. Aluminum-based and mica–titanium pigments are now widely integrated into elastomeric and silicone roof coatings to achieve high Solar Reflectance Index ratings, which are becoming mandatory in many high-heat urban zones.

The next phase of growth lies in technological integration. AI-driven color management systems are enabling architects to specify metallic finishes that appear dark or premium, such as bronze or charcoal, while reflecting up to 90% of near-infrared radiation. This capability allows cities to mitigate the Urban Heat Island effect without sacrificing aesthetic differentiation, positioning high-IR-reflective metallic pigments as both an environmental and design-driven growth engine.

Metallic Pigments Market Share and Segmentation Insights

Aluminum Pigments Lead Metallic Pigments Market with Versatile Metallic Effects and Broad Industrial Use

Aluminum pigments accounted for 58.60% of the Metallic Pigments Market share in 2025, making them the dominant metal-based pigment used across coatings, plastics, and printing ink applications. Aluminum pigments are widely valued for their ability to create bright metallic finishes, reflective surfaces, and high visual brilliance in industrial and decorative coatings. These pigments consist of finely milled aluminum flakes that reflect light and produce metallic effects ranging from bright silver finishes to gold-like tones when combined with other color pigments. Aluminum pigments offer strong advantages including cost efficiency, chemical stability, and compatibility with multiple polymer and coating systems, making them suitable for high-volume applications in automotive coatings, consumer product finishes, and packaging decoration. In 2025, the growing demand for premium automotive metallic finishes has driven advancements in aluminum pigment engineering. Manufacturers are developing pigments with tighter particle size distribution, improved flake orientation, and enhanced optical brilliance, enabling modern automotive coatings to achieve complex liquid-metal, sparkle, and high-gloss metallic effects that enhance vehicle aesthetics and brand differentiation.

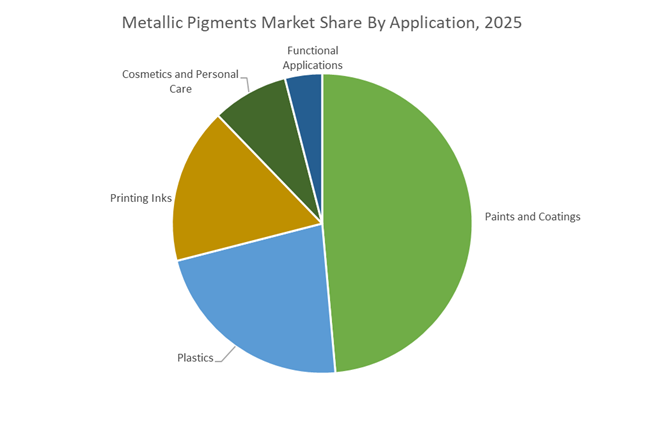

Paints and Coatings Industry Drives the Largest Demand for Metallic Pigments

Paints and coatings accounted for 48.60% of the Metallic Pigments Market share in 2025, establishing the sector as the largest consumer of metallic pigment technologies. Metallic pigments are widely used in automotive OEM coatings, refinish paints, industrial coatings, architectural coatings, and protective coatings, where they provide decorative metallic appearance along with improved light reflectivity and visual depth. The automotive industry remains a particularly significant driver of demand, as vehicle manufacturers increasingly utilize metallic and pearlescent coatings to differentiate models and enhance product appeal. In addition to decorative benefits, metallic pigments also contribute to functional performance characteristics such as UV resistance and barrier protection in coating systems. In 2025, the ongoing transition toward waterborne coating technologies has influenced metallic pigment formulation strategies. Pigment producers are developing passivated aluminum pigments and specialized dispersion technologies that maintain pigment stability in aqueous coating systems, preventing hydrogen gas formation and ensuring consistent flake orientation, which is essential for achieving uniform metallic appearance in modern waterborne automotive and industrial coatings.

Metallic Pigments Market Competitive Landscape

The metallic pigments market in 2026 is driven by radar-transparent coatings, vacuum metallized pigments (VMP), and silica-encapsulated aluminum flakes. Demand is accelerating for PFOA-free dispersions, water-based metallic pastes, and low-PCF pigments tailored for EV coatings, autonomous driving sensors, and sustainable packaging applications.

ECKART leads radar-transparent aluminum pigments and low-carbon recycled metallic solutions

ECKART (ALTANA Group) is dominating the metallic pigments market through advanced aluminum flake technology and radar-transparent coatings tailored for autonomous driving. The acquisition of Silberline significantly strengthens its North American footprint and expands its aluminum pigment portfolio. Its SILVERSHINE Hydro Platinum range enables non-interfering coatings for 77 GHz radar and LiDAR systems, a critical requirement for Level 3/4 EVs. Innovations like ProFLAKE® Zn HYDRO PM 3090 support water-based corrosion protection, replacing solvent-heavy systems. The AL-II recycled aluminum pigment line delivers industry-leading low Product Carbon Footprint (PCF), supported by traceable sustainability metrics. ECKART’s vertical integration and focus on functional optics position it as the benchmark for future-ready metallic pigments.

Sun Chemical advances high-chroma aluminum pigments and functional coatings for EV thermal management

Sun Chemical (DIC Group) is leveraging its R&D scale to develop high-performance metallic pigments for automotive and electronics applications. Its Paliocrom® Brilliant Ruby L 3558 delivers superior chroma, brilliance, and hiding power in both water-borne and solvent-borne coatings. Expansion in perylene pigment production supports hybrid pigment systems like Spectrasense™, enhancing solar heat management in cool-roof and automotive coatings. The integration of Benda-Lutz® aluminum pigments with PPS compounds enables lightweight components with electromagnetic shielding for EV battery systems. Innovations such as Glacier™ Exterior Ceramic White align with demand for “clean, cool sparkle” finishes. Sun Chemical’s focus on functional pigments and thermal management strengthens its position in e-mobility coatings.

BASF Colors & Effects drives phygital metallic aesthetics and digital color simulation technologies

BASF Colors & Effects, under DIC/Sun Chemical management, is redefining metallic pigment applications through “phygital” design integration. Its Automotive Color Report highlights a shift toward multi-dimensional metallic shades using advanced interference pigments. Products like Tesseract Blue deliver dynamic color-shifting effects with enhanced depth, meeting premium EV design requirements. The company’s digital simulation tools allow OEMs to model pigment-light interactions in 3D environments, reducing physical prototyping by up to 40%. Innovations such as Phygital Magnetar combine metallic textures with digital-inspired finishes. BASF’s integration of digital tools with advanced pigment chemistry positions it at the forefront of next-generation automotive coatings.

SCHLENK scales vacuum metallized pigments and high-purity metal powders for advanced applications

SCHLENK Metallic Pigments GmbH is a global leader in VMP technology, delivering high-reflectivity, chrome-like finishes through silica-encapsulated pigments such as Decomet® STV. These pigments ensure stability in water-based and solvent-based systems, supporting premium packaging and automotive coatings. Its Zenexo® VolcanGlow series introduces UV-stable metallic effects for architectural applications. The company is also expanding into additive manufacturing with Rogal® Select powders, offering 99.95% purity for high-conductivity components. Its METAPRINT® LithoCare inks address regulatory requirements for food-safe packaging. SCHLENK’s diversification across coatings, printing, and advanced manufacturing strengthens its competitive positioning.

Toyo Aluminium focuses on high-reflectivity aluminum solutions for electronics and sustainable packaging

Toyo Aluminium K.K. (Toyal) is advancing metallic pigment technologies through sustainable aluminum-based innovations and electronics integration. Its LUXAL®-UV reflector enhances efficiency in solar concentrators and UV-curing systems, supporting renewable energy applications. The company is expanding into semiconductor materials with developments in SiGe/Si wafer-compatible powders and pastes. Its new white aluminum foil products target high-barrier packaging for pharmaceuticals and premium foods. Following its strategic pivot to independent R&D, Toyal is reinforcing its innovation pipeline. With strong expertise in aluminum pastes and powders, the company is well-positioned in high-growth electronics and sustainable packaging markets.

Germany: Sensor-Compatible Effects and Carbon-Neutral Manufacturing

Germany is defining the technological frontier of the metallic pigments market through sensor-compatible aesthetics, low-carbon production, and circular raw material strategies. At the European Coatings Show 2025, ECKART, part of ALTANA, unveiled radar-transparent metallic pigments such as SILVERSHINE Hydro Platinum and Titanium Grey. These materials are engineered to deliver premium metallic finishes on autonomous vehicle bumpers without disrupting ADAS radar performance, positioning Germany at the center of 2026 automotive exterior design requirements. This capability directly addresses OEM demand for functional coatings that combine visual differentiation with sensor integrity.

Sustainability leadership further strengthens Germany’s competitive position. By January 2025, ALTANA achieved CO₂ neutrality across its direct production footprint, including ECKART’s pigment facilities, enabled by full conversion to green electricity and high-efficiency thermal recovery in calcination processes. Raw material strategy is also shifting structurally. ECKART expanded its AL-II product line in 2025 using recycled secondary aluminum, offering one of the lowest carbon footprints available for aluminum pigments in 2026 formulations. In parallel, Schlenk Metallic Pigments deepened collaboration with IGP Pulvertechnik to deliver powder coatings with liquid-paint-level distinctness of image, accelerating substitution of solvent-borne systems in architectural and industrial coatings.

United States: Automotive Color Intensity and Safer Processing Formats

The United States metallic pigments market is advancing through high-impact color innovation, safer pigment handling, and supply chain consolidation. In November 2025, Sun Chemical, a subsidiary of DIC Corporation, introduced Paliocrom Brilliant Ruby L 3558. This intense bluish-red aluminum effect pigment delivers elevated hiding power and chromatic brilliance, aligning with 2026 automotive color trends favoring deep crimson metallic finishes across passenger vehicles and light trucks.

Manufacturing safety and downstream compatibility are also shaping product design. Silberline launched the ET-2025 series in mid-2025, offering coarse aluminum flakes in low-dusting granular form for high-load masterbatches in polyolefins and styrenics. This format reduces airborne metallic particulates in processing environments while maintaining optical performance. Strategic consolidation has reinforced domestic capability, as ALTANA completed the acquisition of Silberline in early 2025, strengthening North American R&D and waterborne industrial coating solutions. Sustainability in packaging is another vector, with Sun Chemical’s Glacier Exterior Ceramic White S1303M enabling recyclable food packaging to achieve satin white effects without traditional metallic pigments, while delivering high chemical resistance.

China: AI-Optimized Milling and Electronics-Driven Demand

China’s metallic pigments market is evolving through digital process optimization, electronics-driven demand, and coordinated resin-pigment innovation. Under the Ministry of Industry and Information Technology’s “AI plus Non-Ferrous” initiative for 2025–2026, pigment producers are deploying AI models to optimize particle size distribution in real time. This approach targets meaningful reductions in energy consumption during high-purity aluminum pigment milling while improving consistency for export-oriented applications.

Capacity expansion supports downstream growth sectors. Throughout 2025, Nouryon and Sun Chemical scaled high-performance material capacities at the Nansha site, with a focus on vacuum-metallized pigments for smart home electronics and connected devices across Asia-Pacific. At ChinaCoat 2025, DIC Corporation showcased BURNOCK WD-569, a high-adhesion resin engineered to work synergistically with metallic pigments for stainless steel and new energy vehicle battery casing coatings. This integration underscores China’s emphasis on system-level solutions rather than standalone pigments.

India: Import Substitution and Domestic Capability Building

India’s metallic pigments market is being reshaped by import controls, mineral security priorities, and targeted R&D funding. In September 2025, the Directorate General of Foreign Trade issued Notification No. 34/2025–26, shifting imports of metallic powders and silver-plated articles from free to restricted status through March 2026. This policy aims to accelerate domestic manufacturing under the Make in India framework, directly benefiting local pigment producers and compounders.

Industrial policy alignment is reinforcing this trajectory. The National Critical Mineral Mission launched in 2025 prioritizes domestic zinc and aluminum pigment production, supporting significant pledged investments for high-performance coated steel used in infrastructure and transport. Innovation capacity is expanding through a ₹20,000 crore private-sector-led research fund announced in May 2025, which includes development of bio-sourced metallic pastes for printing and packaging. These initiatives position India to move beyond import dependence toward value-added metallic pigment formulations tailored for regional end uses.

Thailand: Southeast Asian Automotive and Two-Wheeler Hub

Thailand is strengthening its role as a regional supply and distribution hub for metallic pigments serving Southeast Asia’s automotive and two-wheeler manufacturing clusters. In late 2025, BASF and Sun Chemical expanded blending and distribution operations in Bangpakong. This expansion improves responsiveness to OEM demand for high-durability metallic coatings, particularly for motorcycles and compact vehicles where visual differentiation and weather resistance are critical. Thailand’s positioning reflects proximity-driven agility and integration with ASEAN manufacturing ecosystems.

Country-Level Strategic Positioning in the Metallic Pigments Market

Metallic Pigments Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Core Pigment Technologies

|

Policy or Industry Driver

|

Competitive Positioning

|

|

Germany

|

Sensor-compatible and low-carbon pigments

|

Radar-transparent aluminum, recycled aluminum

|

Automotive ADAS needs, carbon neutrality

|

Technology and sustainability leadership

|

|

United States

|

High-impact color and safer handling

|

Intense aluminum effects, granular flakes

|

Automotive color cycles, workplace safety

|

Premium aesthetics with process safety

|

|

China

|

Digital optimization and electronics

|

AI-milled aluminum, VMP systems

|

MIIT AI initiative, smart electronics

|

Scale with precision and energy efficiency

|

|

India

|

Import substitution and R&D

|

Zinc and aluminum pigments, bio-sourced pastes

|

Make in India, mineral mission

|

Domestic capability expansion

|

|

Thailand

|

Regional supply agility

|

Durable metallic coatings

|

ASEAN automotive growth

|

Proximity-driven distribution hub

|

Metallic Pigments Market Report Scope

Metallic Pigments Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$3.3 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Metal Type (Aluminum Pigments, Copper and Bronze Pigments, Zinc Pigments, Stainless Steel Pigments, Specialty Metal Pigments), By Product Form (Metallic Paste, Metallic Powder, Metallic Ink, Pigment Dispersions), By Technology (Natural Mica-Based, Synthetic Mica-Based, Silica-Encapsulated, Glass Flake-Based), By Application (Paints and Coatings, Printing Inks, Plastics, Cosmetics and Personal Care, Functional Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ALTANA, DIC Corporation, Schlenk Metallic Pigments, Silberline Manufacturing, Toyo Aluminium, Asahi Kasei, BASF, Umicore, Carlfors Bruk, AVL Metal Powders, Metaflake, Radient Color, Sudarshan Chemical Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metallic Pigments Market Segmentation

By Metal Type

- Aluminum Pigments

- Copper and Bronze Pigments

- Zinc Pigments

- Stainless Steel Pigments

- Specialty Metal Pigments

By Product Form

By Technology

- Natural Mica-Based

- Synthetic Mica-Based

- Silica-Encapsulated

- Glass Flake-Based

By Application

- Paints and Coatings

- Printing Inks

- Plastics

- Cosmetics and Personal Care

- Functional Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Metallic Pigments Market

- ALTANA

- DIC Corporation

- Schlenk Metallic Pigments

- Silberline Manufacturing

- Toyo Aluminium

- Asahi Kasei

- BASF

- Umicore

- Carlfors Bruk

- AVL Metal Powders

- Metaflake

- Radient Color

- Sudarshan Chemical Industries

*- List not Exhaustive