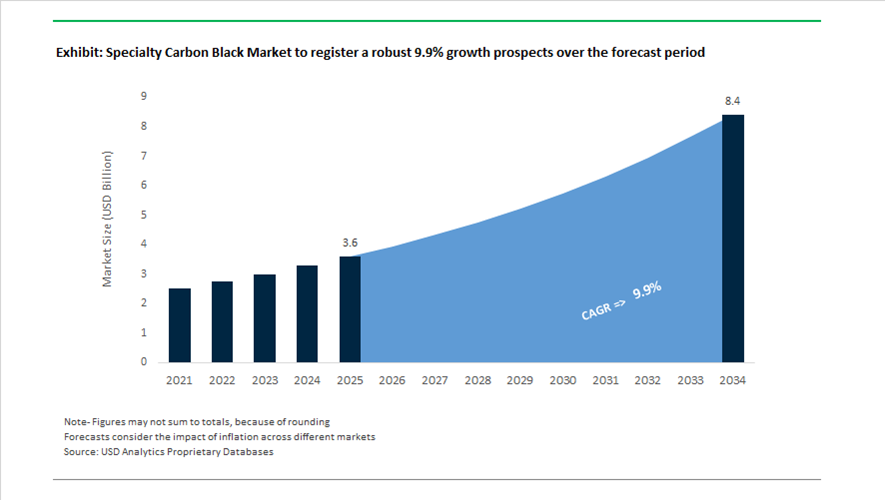

Specialty Carbon Black Market Valuation 2025–2034: $3.6 Billion to $8.4 Billion at 9.9% CAGR Powered by EV Batteries, Circular Feedstocks, and High-Performance Coatings

The global specialty carbon black market is valued at $3.6 billion in 2025 and is projected to reach $8.4 billion by 2034, expanding at a strong CAGR of 9.9%. Growth is driven by rising demand for conductive carbon blacks, acetylene black, ultra-high-performance pigment blacks, and bio-circular carbon grades across lithium-ion batteries, energy storage systems, high-voltage cables, automotive coatings, inks, and advanced polymer compounds. Specialty carbon black differs from commodity reinforcing grades due to its controlled particle size distribution, structure, conductivity profile, and dispersion characteristics, making it essential in EV battery electrodes, electromagnetic shielding materials, and premium coatings. The accelerating electrification of transport, grid modernization projects, and sustainability mandates are structurally elevating high-conductivity and low-carbon-footprint carbon blacks.

In April 2024, Himadri Specialty Chemical Ltd announced a $2.64 billion investment plan to expand specialty carbon black capacity by 70,000 tons, focusing on materials for energy storage and electric vehicle batteries. In October 2024, Sudarshan Chemical Industries signed an agreement to acquire the Heubach Group, integrating advanced pigment technologies that complement high-performance carbon black applications in coatings. During 2024–2025, Birla Carbon operationalized its Asia Post-Treatment facility in India, achieving full integration by September 2025 and producing advanced Raven grades such as 1035, 1185 Ultra, and 1255 for regional coatings and ink markets.

Battery-driven innovation intensified in 2025 and 2026. In November 2025, Orion S.A. announced that its PRINTEX® kappa 100 acetylene black was qualified by a leading battery energy storage system manufacturer for high-voltage cable and renewable energy infrastructure applications. In January 2026, Cabot Corporation signed a multi-year agreement with PowerCo SE, Volkswagen Group’s battery subsidiary, to supply conductive carbons and dispersions for lithium-ion battery production. In 2025, PCBL Limited established Nanovace Technologies Ltd, a joint venture focused on nano-silicon anode materials, signaling a move up the battery materials value chain. On January 28, 2026, PCBL commenced commercial production at its Line-4 facility, adding 60,000 metric tons of annual capacity targeting specialty rubber and coatings demand.

Sustainability and regional capacity expansion define the competitive landscape in 2026. In February 2026, Cabot completed the acquisition of Mexico Carbon Manufacturing from Bridgestone, strengthening its North American manufacturing footprint. The same month, Cabot validated circular reinforcing carbon production at its facilities in Indonesia and China, establishing circular capabilities across the Americas, Europe, and Asia. Orion launched ECOLAR 50 POWDER in February 2026, a specialty carbon black produced entirely from bio-circular feedstock, enabling coatings manufacturers to reduce Scope 3 emissions while maintaining performance parity with conventional grades. In February 2026, Punia Metox began operations at its Andhra Pradesh facility with 12,000 tonnes per year capacity, planned to double within six months to meet rising specialty demand. These strategic investments, circular feedstock validation, EV supply agreements, and conductive material innovations are positioning specialty carbon black as a critical material platform in energy storage and high-performance coatings markets through 2034.

Specialty Carbon Black Market Trends and Opportunities: Electrification Demand, Circular Feedstocks, and Ultra-Purity Applications

Lithium-Ion Battery Boom Driving Structural Demand for Conductive Carbon Black Additives

The Specialty Carbon Black market is experiencing a structural demand surge driven by the rapid expansion of lithium-ion battery manufacturing, electric vehicles (EVs), and grid-scale energy storage systems (BESS). Conductive carbon black has transitioned from a niche additive to a mission-critical material for electrode conductivity, electron mobility, and thermal stability, directly influencing battery performance and lifecycle efficiency.

The scale of demand expansion is anchored in global electrification trends. With battery manufacturing capacity reaching 3 terawatt-hours by 2024 and electric vehicle sales surpassing 17 million units globally, the requirement for high-performance conductive additives has intensified. These materials are engineered for ultra-low electrical resistance, enabling improved charge-discharge efficiency and extended cycle life, particularly in heavy-duty EV and high-capacity storage systems.

Industrial validation of this trend is evident in late 2025 developments, where Orion S.A.’s PRINTEX® kappa 100 acetylene black was qualified for major Battery Energy Storage System (BESS) applications. This aligns with the increasing deployment of high-voltage subsea and underground transmission infrastructure, where reliable energy storage is critical. As a result, conductive carbon black is emerging as a strategic material in next-generation energy ecosystems, underpinning both mobility electrification and grid modernization.

Sustainability Mandates and Regulatory Pressure Accelerating Shift to Low-Carbon Feedstocks

Environmental regulations and corporate decarbonization targets are fundamentally reshaping the Specialty Carbon Black market, driving a transition toward sustainable, traceable, and low-carbon feedstocks. Traditional petroleum-derived production routes are facing increasing scrutiny, prompting manufacturers to adopt circular economy models and ESG-compliant production frameworks.

Supply chain strategies are evolving in parallel. To mitigate cost pressures, including the 0.5 percentage point inflation impact from tariffs on critical intermediates, leading players are implementing “local-for-local” manufacturing models. For instance, Orion S.A.’s new facility in La Porte, Texas, is set to become the only U.S.-based production site for ultra-pure acetylene carbon black, strengthening regional supply resilience.

Regulatory developments are also intensifying compliance requirements. The adoption of China’s Ecological and Environmental Code in March 2026, consolidating over 30 environmental statutes, is forcing manufacturers in key regions such as Shaanxi and Shandong to upgrade environmental performance or risk production constraints. Simultaneously, ESG certification is becoming a competitive necessity. Companies like Cabot Corporation have achieved ISCC PLUS certification across global operations, leveraging tire pyrolysis oil (TPO) to produce circular carbon materials aligned with 2030 Net Zero targets. This shift is positioning sustainability as a core value driver in specialty carbon black production and procurement strategies.

Circular Carbon Black from Tire-Derived Oil (TDO) Unlocking Low-Carbon Growth Pathways

The adoption of Tire-Derived Oil (TDO) and end-of-life tire (ELT) recycling technologies represents a major growth opportunity, enabling the Specialty Carbon Black market to decouple from fossil fuel volatility while advancing circular economy objectives. TDO-based production is emerging as a scalable solution for low-carbon, high-performance specialty carbon black grades, particularly in automotive and industrial applications.

In February 2026, Cabot Corporation validated circular carbon production at its facilities in Indonesia and China under the EVOLVE Sustainable Solutions platform, demonstrating the feasibility of drop-in replacements for conventional carbon black without compromising performance metrics such as dispersion quality, conductivity, and durability. This is critical for maintaining compatibility with existing manufacturing processes while improving sustainability profiles.

The strategic importance of TDO is further reinforced by tire manufacturers’ commitment to achieving 40% sustainable material usage by 2030. By integrating circular feedstocks, specialty carbon black producers can deliver 5% to 10% reductions in product carbon footprint, directly supporting OEM sustainability goals. Technologies such as Birla Carbon’s Continua™ Sustainable Carbonaceous Material (SCM) highlight the maturity of this segment, proving that recycled inputs can meet stringent requirements for jetness, structural integrity, and long-term performance. This positions circular carbon black as a high-growth, ESG-aligned segment within specialty materials markets.

Ultra-High Purity Carbon Black for Semiconductor and Additive Manufacturing Applications

A high-margin opportunity is emerging in the development of ultra-high purity carbon black (>99.9%), driven by the increasing complexity of semiconductor manufacturing and advanced additive manufacturing (3D printing). These applications require materials with minimal impurities, controlled particle morphology, and high dispersibility, positioning specialty carbon black as a critical enabler of next-generation electronics.

In semiconductor fabrication, ultra-pure carbon black is gaining traction in polycrystalline silicon carbide (SiC) substrate production, where it supports the development of energy-efficient power devices used in EVs, renewable energy systems, and high-frequency electronics. Strategic initiatives by companies such as Tokai Carbon underscore the growing importance of high-purity carbon materials in precision semiconductor processes.

Beyond semiconductors, high-purity carbon black is expanding into 3D printing and advanced coatings, where uniform particle distribution and chemical stability are essential for achieving precision manufacturing outcomes and high-performance antistatic properties. These materials enable the production of complex geometries and miniaturized electronic components, supporting innovation in sectors such as aerospace, healthcare, and consumer electronics.

Industry consolidation is reinforcing this strategic shift toward high-value applications. In February 2026, Henkel’s $2.5 billion acquisition of Stahl Holdings signaled a broader move away from commoditized rubber-grade products toward specialized, technology-driven material portfolios. This trend highlights the growing importance of ultra-purity, performance-driven carbon black solutions as a cornerstone of advanced manufacturing ecosystems.

Specialty Carbon Black Market Share and Segmentation Insights

Powder Form Specialty Carbon Black Leads the Market for High-Performance Dispersion Applications

Powder form specialty carbon black accounted for 52.80% of the specialty carbon black market in 2025, reflecting its strong performance advantages in high-end material applications. Powder carbon black offers higher surface area, superior dispersion characteristics, and optimal particle structure, making it ideal for demanding applications such as conductive plastics, high-jetness coatings, and specialty printing inks. These properties enable enhanced electrical conductivity, deeper color intensity, and improved reinforcement in polymer systems. A key 2025 innovation trend is the development of low-dust specialty carbon black powders, where manufacturers apply surface treatments and advanced particle engineering techniques to reduce airborne particulates during handling while maintaining the high-performance characteristics required for advanced industrial applications.

Plastics Industry Drives Specialty Carbon Black Demand Through Conductive and UV-Stabilized Materials

Plastics represent the largest application segment in the specialty carbon black market, accounting for 38.60% of global demand in 2025 due to the essential functional properties carbon black provides in polymer systems. Specialty carbon black enhances UV resistance, electrical conductivity, color strength, and mechanical reinforcement in engineering plastics and packaging materials. Conductive carbon black grades are widely used in electrostatic discharge safe packaging, automotive components, and electronic device housings. A major 2025 growth driver is the rapid expansion of conductive plastic materials used in electronics and electric vehicle applications, where specialty carbon black enables electromagnetic interference shielding, static control, and reliable electrical performance in advanced polymer components.

Specialty Carbon Black Market Competitive Landscape

The global specialty carbon black market in 2026 is driven by conductive carbon additives, EV battery materials demand, and decarbonized production technologies. Leading players are focusing on high-purity grades, localized manufacturing, and sustainable carbon solutions to support energy storage, advanced coatings, and electronics applications.

Cabot Strengthens Conductive Carbon Leadership with LITX® Innovation and Strategic North American Expansion

Cabot Corporation is reinforcing its dominance in specialty carbon black through its Performance Chemicals segment, which delivered an 18% EBIT increase in FY2025. The company’s LITX® 95F conductive carbon is engineered to enhance lithium-ion battery energy density and charge efficiency, aligning with EV and energy storage demand. Its acquisition of Mexico Carbon Manufacturing strengthens regional supply chains and supports North American production resilience. A global price increase of up to 20% reflects strong demand for high-purity carbon black used in semiconductors and advanced coatings. Cabot’s leadership in conductive additives and fumed silica reinforces its role in high-performance material applications. Its strategic focus on energy transition and digitalization strengthens competitive positioning.

Orion Advances Battery-Grade Carbon Black and Localization Strategy with PRINTEX® kappa 100 and Gas Black Expertise

Orion S.A. is positioning itself as a pure-play leader in specialty carbon black with strong emphasis on conductive additives and gas black technology. Its PRINTEX® kappa 100 acetylene black has achieved commercial qualification for battery energy storage systems, supporting grid modernization and renewable integration. The company’s localization strategy includes expansion of production capacity in France and development of a new facility in Texas to mitigate geopolitical risks. Orion’s gas black products deliver superior jetness and blue undertones for high-end coatings and printing inks. Its EcoVadis Platinum rating highlights leadership in sustainable manufacturing and circular carbon solutions. The company’s focus on battery-grade carbon and premium pigments enhances its market competitiveness.

Birla Carbon Expands Specialty Carbon Production and Sustainable Continua™ Solutions in Asia-Pacific Markets

Birla Carbon, part of the Aditya Birla Group, is expanding its specialty carbon black footprint through its Asia Post Treatment facility in India, scaling Raven 1000 and 1200 series production for coatings and plastics. The launch of Raven 401P enhances tinting performance and design flexibility in waterborne and solvent-based coatings. Its Continua™ SCM portfolio supports circular economy initiatives by enabling higher recycled content in rubber applications without compromising performance. The company maintains ISCC Plus certification across all global manufacturing sites, reinforcing sustainability credentials. Operational excellence is demonstrated by a record-low safety performance metric. Birla Carbon’s regional expansion and innovation strengthen its position in high-growth specialty carbon segments.

Imerys Graphite & Carbon Strengthens Conductive Materials Portfolio Through Battery Partnerships and Grid Infrastructure Applications

Imerys Graphite & Carbon is advancing its role in specialty carbon materials through strategic collaboration with Shanghai Shanshan, supporting Europe’s battery anode supply chain. Its ENSCO® conductive carbon blacks are critical for high-voltage cable insulation used in renewable energy infrastructure. Project Horizon targets €50–€60 million in cost savings through industrial optimization, enhancing operational efficiency. The company is prioritizing investments in high-value carbon materials while reallocating capital from non-core lithium projects. Its expertise in conductive carbon and graphite integration supports advanced energy storage and grid applications. Imerys’ focus on performance materials strengthens its position in electrification-driven markets.

Mitsubishi Chemical Strengthens Integrated Carbon Value Chain and Green Transformation in Conductive Carbon Black

Mitsubishi Chemical Group leverages its vertically integrated coal-tar-to-carbon value chain to deliver high-performance conductive carbon black for electronics and automotive applications. Its MITSUBISHI™ conductive carbon series is widely used in anti-static components, IC trays, and heating systems. The DIAPOL™-WMB wet masterbatch technology enhances dispersion and improves tire performance, supporting eco-tire innovation. The company’s restructuring emphasizes Green Transformation, including development of biomass-derived carbon black. Integration of needle coke and pitch coke production provides feedstock optimization and cost efficiency. Mitsubishi Chemical’s integrated approach strengthens its competitiveness in advanced carbon materials.

Tokai Carbon Expands ASEAN Capacity and UV-Resistant Carbon Black Portfolio Through Strategic Acquisition and Environmental Upgrades

Tokai Carbon Co., Ltd. is strengthening its specialty carbon black market presence through the acquisition of Bridgestone Carbon Black Thailand, expanding supply capacity in the ASEAN region. The company is focusing on UV-protective carbon black grades for outdoor plastics and telecommunications infrastructure. Its tailored high-structure and low-structure powders support fiber applications requiring consistent dispersion and durability. Capital investments are being directed toward upgrading furnace black production lines to meet stringent environmental regulations. Tokai Carbon’s regional expansion and product innovation support growth in automotive and industrial applications. Its focus on compliance and performance materials enhances its competitive positioning.

United States Specialty Carbon Black Market Anchored by Circular Inputs and Battery Materials

The United States specialty carbon black industry is transitioning toward circular feedstocks, higher purity benchmarks, and regionally resilient supply chains. In October 2025, Cabot Corporation expanded manufacturing at its Ville Platte, Louisiana site to scale circular reinforcing carbons produced from tire pyrolysis oil. These grades, marketed under the EVOLVE Sustainable Solutions platform, directly address OEM and tire manufacturer demand for lower lifecycle emissions without compromising reinforcing performance. Structural rationalization is also reshaping the market. Orion S.A. announced the shutdown of three to five underperforming American lines by the end of 2025, reallocating capital toward specialty grades for coatings, inks, and battery applications where reliability and consistency are critical.

Environmental compliance and purity standards are reinforcing competitive differentiation. Tokai Carbon CB Ltd. completed major environmental investments across its U.S. plants in 2025, enabling stable operations under some of the most stringent emissions thresholds globally. At the same time, domestic producers are accelerating production of 99.9% purity conductive carbon blacks for lithium-ion battery electrodes, supported by federal procurement preferences such as the BioPreferred Program. Trade policy is amplifying localization. The imposition of a 25% tariff on select carbonaceous intermediates in March 2025 has accelerated a make-in-region strategy, reinforcing U.S. capacity utilization. Safety leadership remains a hallmark, with the International Carbon Black Association awarding Gold Safety recognition in June 2025 to multiple U.S. sites, including Orion’s Belpre and Ivanhoe plants.

China Specialty Carbon Black Market Driven by EV Scale and Carbon Market Tightening

China’s specialty carbon black industry is being reshaped by EV-driven demand and a rapidly tightening carbon regulatory framework. As of 2025, China accounts for more than 60% of global EV battery production, creating sustained demand for conductive carbon blacks used to enhance electrode conductivity and cycle stability. This demand is increasingly met by localized specialty grades as producers adapt portfolios away from commodity furnace blacks. International players are deepening localization. Birla Carbon debuted its BC1060 specialty grade at RubberTech 2025 in Shanghai, targeting anti-vibration and sealing applications for Chinese automotive OEMs.

Policy pressure is intensifying. In August 2025, the State Council released guidance shifting carbon regulation from intensity-based control to absolute emissions caps, fundamentally altering the operating economics of high-emission plants. The Ministry of Ecology and Environment expanded the national carbon emissions trading scheme in March 2025, compelling specialty producers to integrate carbon capture, adopt cleaner feedstocks, or relocate capacity. Technology upgrades are supporting this transition. Asia-based post-treatment facilities have enabled the local production of high-value, surface-modified specialty grades for coatings and inks, reducing lead times and reinforcing China’s position as a volume and application-driven market.

Germany and European Union Specialty Carbon Black Market Defined by Circular Innovation and Trade Defense

Germany represents the innovation core of Europe’s specialty carbon black industry, with policy-backed R&D and circularity at the center. Orion S.A. is executing a €6.4 million R&D program funded by German and EU agencies to develop climate-neutral carbon black using alternative non-fossil carbon sources. This work builds on the BlackCycle project, under which Orion became the first producer to manufacture circular carbon black from 100% tire pyrolysis oil. In March 2025, the European Commission recognized this achievement through its Innovation Radar, underscoring Europe’s strategic emphasis on circular materials.

Trade policy and portfolio restructuring are progressing in parallel. The EU initiated anti-dumping investigations into imported carbon black during 2025, aiming to shield domestic specialty producers from low-cost, high-emission imports. At the corporate level, Tokai Carbon completed the divestment of its German subsidiary TOKAI ERFTCARBON GmbH in June 2025, reflecting a broader European trend of exiting legacy graphite and commodity assets to focus capital on higher-margin specialty carbon materials aligned with emissions-constrained markets.

India Specialty Carbon Black Market Scaling Through Capacity and Carbon Science

India’s specialty carbon black market is expanding rapidly through large-scale capacity investments and innovation-led export growth. Himadri Specialty Chemical Ltd. announced a strategic investment of approximately USD 2.64 billion during 2024–2025 to add 70,000 tons of specialty capacity, targeting high-performance plastics, coatings, and fiber-grade applications. This expansion reflects India’s shift from commodity rubber blacks toward engineered specialty grades with higher value density.

Innovation infrastructure is strengthening export competitiveness. Birla Carbon’s Taloja research center has positioned India as a global hub for carbon science, driving development of the Continua sustainable carbonaceous materials portfolio. As a result, Indian exports reached record levels in 2025, particularly in conductive masterbatches and fiber-grade carbon blacks supplying global electronics, textiles, and advanced composites markets.

Thailand Specialty Carbon Black Market Focused on Regional Modernization

Thailand is emerging as a modernized production base for specialty carbon black serving Southeast Asia. Tokai Carbon is scheduled to complete the relocation of its Thai manufacturing operations by the end of 2025. The new site offers expanded land availability, upgraded process controls, and advanced emissions mitigation systems, enabling future specialty capacity additions.

Regional demand for coatings and coloration is also shaping product strategy. Birla Carbon leveraged its Bangkok platform in September 2025 to introduce Raven 401P, a specialty grade designed for tinting and tonal solutions in Southeast Asian architectural and industrial coatings. This positions Thailand as a responsive hub for fast-growing regional coatings markets.

Comparative Snapshot: Country-Level Specialty Carbon Black Dynamics

Specialty Carbon Black Market County Level Snapshot

|

Country / Region

|

Primary Demand Drivers

|

Strategic Focus Areas

|

Structural Impact

|

|

United States

|

Batteries, coatings, sustainability

|

Circular TPO feedstocks, high-purity grades

|

Localized, compliance-driven supply

|

|

China

|

EV batteries, automotive

|

Conductive grades, carbon trading compliance

|

Policy-shaped capacity transition

|

|

Germany / EU

|

Circular materials, regulation

|

Non-fossil carbon, anti-dumping protection

|

Innovation-led premium positioning

|

|

India

|

Exports, plastics, textiles

|

Large-scale specialty expansion, R&D

|

Rapid scale with cost advantage

|

|

Thailand

|

Regional coatings demand

|

Modernized plants, low-emission tech

|

Southeast Asia production hub

|

Specialty Carbon Black Market Report Scope

Specialty Carbon Black Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.6 Billion

|

|

Market Size (2034)

|

$8.4 Billion

|

|

Market Growth Rate

|

9.9%

|

|

Segments

|

By Form (Granules, Powder), By Grade / Function (Conductive Carbon Black, High Jetness Carbon Black, Fiber Grade Carbon Black, UV-Stabilized Carbon Black, Food-Grade Carbon Black), By Process Type (Furnace Black, Gas Black, Lamp Black, Thermal Black, Acetylene Black), By Application (Plastics, Coatings & Paints, Inks & Toners, Batteries & Energy Storage, Mechanical Rubber Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cabot Corporation, Orion S.A., Birla Carbon, Tokai Carbon Co. Ltd., Imerys S.A., Denka Company Limited, Mitsubishi Chemical Group, Himadri Specialty Chemical Ltd, Continental Carbon Company, Omsk Carbon Group, PCBL Limited, Lion Specialty Chemicals Co. Ltd., Geotech International B.V., Black Cat Carbon Black, Longxing Chemical Stock

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Carbon Black Market Segmentation

By Form

By Grade / Function

- Conductive Carbon Black

- High Jetness Carbon Black

- Fiber Grade Carbon Black

- UV-Stabilized Carbon Black

- Food-Grade Carbon Black

By Process Type

- Furnace Black

- Gas Black

- Lamp Black

- Thermal Black

- Acetylene Black

By Application

- Plastics

- Coatings & Paints

- Inks & Toners

- Batteries & Energy Storage

- Mechanical Rubber Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Carbon Black Industry

- Cabot Corporation

- Orion S.A.

- Birla Carbon

- Tokai Carbon Co. Ltd.

- Imerys S.A.

- Denka Company Limited

- Mitsubishi Chemical Group

- Himadri Specialty Chemical Ltd

- Continental Carbon Company

- Omsk Carbon Group

- PCBL Limited

- Lion Specialty Chemicals Co. Ltd.

- Geotech International B.V.

- Black Cat Carbon Black

- Longxing Chemical Stock

*- List not Exhaustive