Fumed Silica Market Size, CAGR 5.6%, and Strategic Expansion in High-Purity and Low-Carbon Grades (2025–2034)

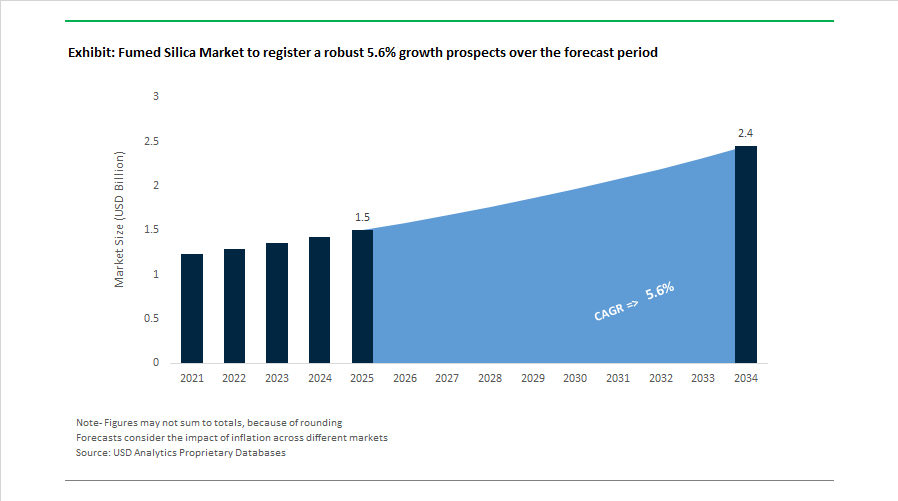

The global Fumed Silica Market is projected to grow from $1.5 billion in 2025 to $2.4 billion by 2034, registering a CAGR of 5.6% during the forecast period. Market expansion is closely tied to rising demand for high-performance rheology modifiers, thermal insulation fillers, anti-caking agents, and reinforcing additives across electronics, automotive, adhesives, sealants, coatings, and specialty chemicals. Growth in electric vehicle battery systems, semiconductor encapsulation materials, advanced coatings, and lightweight construction composites is reinforcing structural demand for high-purity and hydrophobic fumed silica grades.

In September 2025, Cabot Corporation introduced a new high-purity fumed silica engineered for semiconductor encapsulation and battery separator coatings. The development addresses increasing miniaturization in electronics and the need for improved thermal management and electrical insulation in next-generation EV batteries. In July 2025, Wacker Chemie AG launched an advanced hydrophobic fumed silica series designed to enhance rheology control and moisture resistance in high-performance adhesives and aerospace-grade sealants. These launches reflect a broader transition toward application-specific, value-added silica formulations rather than commodity volume expansion.

Sustainability and supply chain efficiency are becoming defining investment themes in the fumed silica industry. In June 2025, Tokuyama Corporation upgraded its vapor-phase hydrolysis production technology to lower carbon emissions per ton of output, directly responding to demand from cosmetics and coatings manufacturers seeking low-carbon raw materials. In April 2025, Mondi plc collaborated with Evonik Industries to introduce fully recyclable paper-based packaging for fumed silica, reducing plastic usage in chemical powder logistics. These moves indicate that ESG alignment is no longer peripheral but embedded in product development and distribution strategies.

Capacity expansion and regional reinforcement remain central to competitive positioning. In June 2024, Evonik Industries inaugurated its AEROSIL® Easy-to-Disperse technology plant in Rheinfelden, enabling production of silica dispersions that eliminate energy-intensive grinding processes in paints and coatings. In November 2024, Qemetica S.A. acquired PPG Industries’ silica products business for approximately $310 million, strengthening its specialty silica footprint in Europe and expanding distribution access in North America. In Q3 2024, HPQ Silicon Inc. advanced commissioning of its pilot Fumed Silica Reactor technology aimed at producing fumed silica directly from quartz, potentially bypassing silicon tetrachloride intermediates and reducing energy intensity.

Margin pressure and cost restructuring are shaping 2025–2026 market dynamics. In October 2025, Wacker Chemie AG launched its PACE program, targeting annual cost reductions exceeding €300 million from 2026 onward following a 42% EBITDA decline driven by high energy costs and weak European demand. In early 2026, Evonik Industries completed a multi-million dollar expansion at its Charleston site, increasing capacity by 50% and modernizing supply chain integration for North American automotive and construction markets. In January 2026, Tokuyama Corporation revised its fiscal performance forecast due to overseas price declines and elevated energy expenses, underscoring industry-wide margin compression in basic chemical segments. In December 2025, Wacker Chemie AG further strengthened its China presence with a new technology center supporting specialty silanes and fumed silica-based rheology modifiers for high-growth adhesives and electronics manufacturing.

The Fumed Silica Market outlook reflects a transition toward high-purity semiconductor applications, EV battery integration, low-carbon production technologies, advanced dispersibility systems, and supply chain optimization. Competitive differentiation is increasingly anchored in process efficiency, energy management, application-specific customization, and regional capacity balancing across Europe, North America, and Asia-Pacific.

Trends and Opportunities in the Global Fumed Silica Market

High-Purity Capacity Expansion Supporting Electromobility and Electronics

The rapid electrification of transport and miniaturization of electronic systems are driving a sharp increase in demand for fumed silica with ultra-low metallic impurities. In lithium-ion batteries, power electronics, and semiconductor-adjacent silicone components, even trace contaminants can trigger electrochemical instability, thermal runaway risks, or dielectric failure. This has elevated high-purity fumed silica from a formulation aid to a mission-critical material input.

In October 2024, Wacker Chemie AG confirmed that its specialty silicone expansion project in Zhangjiagang, China, would come on stream in early 2025. The investment, part of a broader €150 million program, directly targets the three- to four-fold increase in silicone consumption per electric vehicle compared with internal combustion engine platforms. Fumed silica produced at this site is optimized for use in thermal interface materials, battery pack gasketing, and high-voltage insulation systems, where thermal stability and purity are non-negotiable.

Europe is emerging as a parallel hub for electromobility-linked silica demand. In January 2024, Wacker announced a new production site in Karlovy Vary, Czech Republic, dedicated to room-temperature-vulcanizing specialty silicones, with production expected to begin by late 2025 and an eventual capacity exceeding 20,000 metric tons per year. This reinforces the strategic role of fumed silica within Europe’s localized EV and electronics supply chains. In Asia, Evonik Industries AG inaugurated its Alu5 fumed alumina facility in Yokkaichi, Japan, in October 2025. While focused on alumina, the project underscores a broader industry trend toward flame-hydrolysis-based specialty oxides for lithium-ion battery separators and cathode coatings, indirectly strengthening demand for high-performance fumed silica with comparable purity profiles.

EHS-Driven Reformulation and Low-Dusting Sustainable Grades

Environmental, health, and safety regulations are increasingly shaping product design in the fumed silica market, particularly around nanoparticle exposure and carbon intensity. Regulators and downstream manufacturers are placing greater emphasis on worker safety, dust suppression, and lifecycle emissions, accelerating the shift toward surface-treated, granulated, and low-dusting grades.

Effective September 1, 2024, Safe Work Australia implemented stricter controls on crystalline silica exposure, aligning with similar regulatory tightening across Europe and North America. Although fumed silica is amorphous, the heightened scrutiny has pushed suppliers to proactively reformulate products to minimize airborne particulates. Granulated and surface-modified fumed silica grades are now being adopted across construction, coatings, adhesives, sealants, and elastomers to reduce handling risks without compromising rheological performance.

Sustainability is also reshaping production economics. In January 2025, HPQ Silicon Inc. announced successful internal validation of its Fumed Silica Reactor pilot plant developed with PyroGenesis. The technology targets an 86% reduction in energy consumption compared with conventional processes, with a pilot capacity of 50 tons expected by the third quarter of 2025. Such innovations are positioning low-carbon fumed silica as a differentiator for OEMs under pressure to decarbonize their supply chains. Downstream, Cabot Corporation transitioned to more sustainable brown paper packaging for its fumed silica products in April 2024, reflecting a market-wide effort to reduce logistics-related environmental impact alongside core material improvements.

Multifunctional Performance in Next-Generation Battery Architectures

Beyond its established role in gel batteries, fumed silica is gaining strategic importance in next-generation battery chemistries, particularly silicon-anode and solid-state systems. These architectures promise significantly higher energy densities but introduce mechanical and electrochemical challenges that fumed silica is uniquely positioned to address.

Research published in July 2025 demonstrated that incorporating fumed silica as a porous buffer matrix in MoS₂-based anodes nearly doubled discharge capacity to approximately 980 mAh per gram by mitigating volumetric expansion during cycling. This positions fumed silica as a structural stabilizer that enables the commercialization of high-capacity anode materials previously limited by poor cycle life. In solid-state batteries, studies updated in August 2025 showed that fumed silica-filled polymer electrolytes achieved oxidative stability close to 5 volts and sustained 1,000 charge-discharge cycles at industrially relevant rates. These performance gains open a significant growth pathway for fumed silica as an ionic conductivity enhancer and mechanical reinforcement additive in solid-state platforms that are increasingly viewed as the long-term future of energy storage.

Specialized Rheology Control for Industrial Additive Manufacturing

Additive manufacturing is emerging as a high-margin opportunity for fumed silica suppliers, particularly in industrial-scale applications requiring precise flow behavior and rapid structural recovery. Embedded 3D printing and vat photopolymerization processes depend on rheology modifiers that can deliver shear thinning under stress while rapidly rebuilding viscosity to maintain geometric accuracy.

Research released in November 2024 demonstrated that tailoring the surface chemistry of fumed silica, specifically alkyl chain length, enabled supporting baths with recovery times as low as 0.2 seconds. This capability allows the printing of complex, unsupported geometries with high dimensional fidelity, positioning fumed silica as a critical enabler of next-generation manufacturing techniques. In powder bed fusion, fumed silica is increasingly used as a glidant to improve flowability and packing density of polymer and metal powders. As the additive manufacturing market scales toward multi-billion-dollar industrial adoption, demand is rising for methacrylate-functionalized and resin-compatible fumed silica grades that integrate seamlessly with UV-curable systems used in high-speed printers.

Fumed Silica Market Share and Segmentation Insights

Hydrophilic Fumed Silica Leads Industrial Formulations Through Superior Rheology and Reinforcement Performance

Hydrophilic Fumed Silica accounted for 68.40% of the Fumed Silica Market share in 2025, making it the most widely used silica type in industrial formulations. Hydrophilic grades contain surface silanol groups that readily interact with polar systems, enabling them to function effectively as rheology modifiers, thickening agents, and reinforcement fillers across numerous industrial applications. These properties make hydrophilic fumed silica essential in silicone elastomers, adhesives, sealants, coatings, and specialty chemical formulations, where it improves viscosity control, prevents sedimentation, and enhances structural strength. The material’s ability to provide thixotropic behavior and consistent dispersion within polymer matrices ensures reliable performance in both liquid and semi-solid formulations. In 2025, the hydrophilic fumed silica segment is experiencing strong growth driven by the development of ultra-high-purity grades designed for advanced technology industries. Manufacturers are producing hydrophilic silica with extremely low metal ion contamination levels—often below 10 ppm—to meet the stringent purity standards required for semiconductor manufacturing and lithium-ion battery production. These high-purity materials maintain the traditional rheological benefits of fumed silica while supporting critical processes in electronics fabrication and energy storage technologies, reinforcing hydrophilic fumed silica’s leadership in the global market.

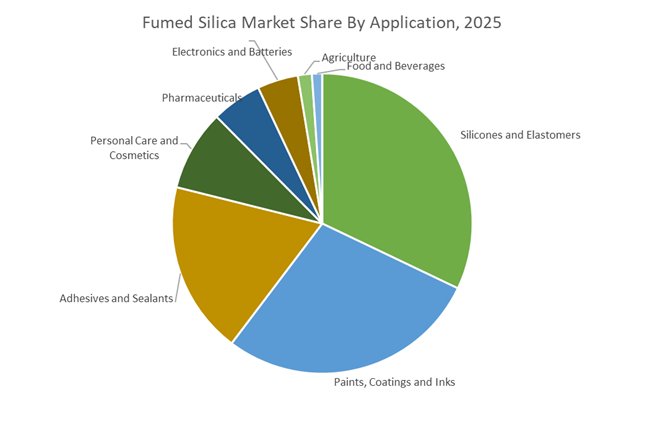

Silicone and Elastomer Manufacturing Drives the Largest Consumption of Fumed Silica

Silicones and Elastomers represented 32.80% of the Fumed Silica Market share in 2025, making them the largest application segment for this specialty material. Fumed silica serves as a reinforcing filler in silicone rubber formulations, including both high-temperature vulcanizing (HTV) and room-temperature vulcanizing (RTV) silicone elastomers. When incorporated into silicone matrices, fumed silica significantly enhances mechanical strength, elasticity, tear resistance, and thermal stability while preserving key silicone properties such as transparency and high-temperature resistance. These performance benefits make reinforced silicone elastomers essential materials in industries ranging from automotive manufacturing and electrical insulation to construction and consumer products. In 2025, demand growth in this segment is strongly influenced by the rapid expansion of the electric vehicle (EV) industry, which relies heavily on silicone-based materials for critical components. EV systems require durable silicone elastomers for high-voltage cable insulation, battery pack seals, thermal interface materials, and environmental gaskets, all of which must withstand extreme temperatures, electrical stress, and chemical exposure. As EV production accelerates globally, silicone manufacturers are increasing consumption of specialized fumed silica grades that maintain electrical insulation properties and thermal stability, further strengthening the importance of this application within the global fumed silica market.

Competitive Landscape in Fumed Silica Market

Evonik Strengthens Asia Expansion While Optimizing Western Assets

Evonik Industries AG maintains global leadership in fumed silica, supported by one of the industry’s most extensive R&D networks. Under its Smart Effects repositioning, Evonik is closing its Waterford, New York fumed silica facility in mid-2025 and its Havre de Grace precipitated silica plant in mid-2026 to streamline asset efficiency. In October 2025, the company announced a significant fumed silica capacity expansion in Asia to address surging demand from lithium-ion battery anodes, battery separator coatings, and semiconductor applications. Collaboration with Mondi plc in April 2025 introduced recyclable, plastic-free packaging for chemical powders, lowering distribution-related carbon intensity. Evonik is also implementing hub concepts and deeper feedstock partnerships to offset elevated European energy costs while strengthening supply security for specialty silica customers.

Cabot Prioritizes High-Purity Grades for Energy Storage and Electronics

Cabot Corporation continues to focus on high-value fumed silica grades for advanced electronics and energy storage systems. In Q1 fiscal 2026, Cabot reported net sales of 849 million dollars, with the Performance Chemicals segment generating 300 million dollars, reflecting resilient demand for specialty silica. The company announced it will cease primary fumed silica production at its Barry, Wales site in late fiscal 2026 while maintaining post-treatment operations for customized surface-modified grades. In September 2025, Cabot launched a new ultra-high-purity fumed silica engineered for semiconductor encapsulation and lithium-ion battery separator coatings. Asia-Pacific remains its largest geographic revenue contributor, generating 349 million dollars in the latest quarter, underscoring the region’s dominance in battery manufacturing and electronics supply chains.

Wacker Integrates HDK® Silica into Semiconductor and Silicone Value Chains

Wacker Chemie AG leverages its HDK® fumed silica brand within a fully integrated silicon, silicone, and semiconductor materials value chain. In October 2025, Wacker launched PACE, a company-wide cost optimization initiative targeting 300 million euros in annual savings by the end of 2026. The company introduced an advanced hydrophobic fumed silica series in July 2025 designed to enhance rheology control, moisture resistance, and thixotropy in high-performance construction adhesives and sealants. Wacker closed 2025 with preliminary sales of 5.49 billion euros and maintained disciplined cash flow management through inventory reductions. Its strategic focus centers on high-margin semiconductor materials and specialty silicones, where fumed silica improves mechanical strength, viscosity control, dielectric properties, and thermal stability in encapsulants and elastomers.

Tokuyama Expands REOLOSIL® Reach Through Distribution and Decarbonization

Tokuyama Corporation is a leading Asian producer of REOLOSIL® fumed silica, known for high-purity manufacturing standards tailored to electronic materials. In Q3 FY2025 results released in January 2026, Tokuyama targeted consolidated net sales of 400 billion yen and operating profit of 45 billion yen. In June 2025, the company expanded global distribution of its REOLOSIL range through a partnership with Environ Speciality Chemicals, strengthening penetration in emerging markets. Production upgrades implemented in mid-2025 significantly reduced carbon emissions intensity, aligning with its 2030 target of a 30% reduction in Scope 1 and Scope 2 emissions. Approximately half of Tokuyama’s net sales now derive from growth businesses, including semiconductor materials and advanced electronics, where fumed silica plays a critical role in CMP slurries, encapsulation resins, and insulating materials.

OCI Leverages Polysilicon Integration for Cost-Competitive Silica Production

OCI Company Ltd. remains one of the top five global fumed silica producers. As a major polysilicon manufacturer, OCI utilizes silicon tetrachloride byproducts to produce cost-efficient pyrogenic silica, reinforcing its integrated circular economy model. The company serves as a critical supplier to South Korea’s lithium-ion battery and semiconductor industries, sectors that are expanding rapidly amid global EV and chip manufacturing growth. OCI is actively broadening its surface-modified fumed silica portfolio, a segment that accounts for over half of global demand due to its application in specialty EV battery components and high-performance coatings. Its feedstock security and regional proximity to advanced manufacturing clusters provide a structural cost and logistics advantage in the Asia-Pacific fumed silica market.

United States: Capacity Modernization and High-Purity Realignment for Advanced Applications

The United States fumed silica market is undergoing a structural upgrade driven by electric vehicle growth, silicone elastomer demand, and higher purity requirements across electronics and personal care. Wacker Chemical Corp. is executing a multi-year, triple-digit million-dollar modernization program at its Charleston, Tennessee facility during 2025–2026. Once fully optimized, the site is positioned as a regional hub for pyrogenic silica with targeted annual output of roughly 14,300 metric tons, directly supporting domestic EV battery components, thermal interface materials, and high-performance silicone elastomers. This investment reflects a strategic move to shorten supply chains for U.S. downstream manufacturers increasingly sensitive to import risk and lead times.

Portfolio rebalancing is also evident. Evonik is completing a 50% capacity expansion at its Charleston, South Carolina plant, with full operation expected in early 2026. The focus is on high-purity silica grades required for green tire tread compounds and semiconductor coatings, signaling a gradual shift from precipitated to fumed silica in performance-critical uses. Cost pressures are shaping pricing dynamics. Cabot Corporation implemented rolling price increases of up to 10% across its CAB-O-SIL product range through late 2024 and 2025 to offset silicon tetrachloride volatility and logistics inflation while sustaining R&D investment in thermal insulation. In parallel, MoCRA enforcement entering its next phase in 2026 has prompted U.S. producers to standardize safety dossiers for cosmetic-grade fumed silica used as rheology and texture modifiers, aligning materials transparency with FDA expectations.

China: Export-Ready Scale and Battery-Driven Innovation

China remains the most dynamic production and consumption center for fumed silica, combining scale, policy support, and downstream integration. Under the Ministry of Industry and Information Technology’s 2025–2026 Petrochemical Industry Work Plan, chemical producers are targeting sustained value growth, with explicit emphasis on high-end electronic chemicals. Fumed silica for semiconductor chip encapsulation and advanced coatings has become a priority category, elevating purity and consistency benchmarks across domestic suppliers.

Industrial capacity continues to expand. Domestic leader HIFULL reached approximately 20,000 tons of annual capacity in 2025 and is actively exporting hydrophobic grades compliant with REACH and K-REACH standards. Environmental performance is becoming a competitive differentiator. Under China’s National Green Initiative, manufacturers such as Henan Xunyu are adopting closed-loop flame hydrolysis processes to cut chlorine emissions and improve energy efficiency, aligning export products with international carbon and lifecycle expectations. On the demand side, China’s dominance in lithium-ion battery manufacturing is reinforcing fumed silica consumption. Innovations in thixotropic gel electrolytes during 2025 demonstrated improved thermal stability and reduced runaway risk in high-capacity power cells, embedding nano-silica as a safety-critical material in next-generation EV batteries.

Germany: Sustainability Financing and Automotive Surface Engineering

Germany’s fumed silica market is shaped by sustainability financing and high-value automotive innovation. In September 2025, Evonik issued green hybrid bonds, allocating proceeds to its Next Generation Solutions roadmap. This includes the planned 2026 rollout of sustainable, bio-based fumed silica grades targeting European life sciences and pharmaceutical excipients, where regulatory scrutiny and traceability requirements are intensifying.

Operational decarbonization is reinforcing brand positioning. Evonik earned a Gold EcoVadis rating in late 2025, with Marl and Hanau sites transitioning to fully renewable electricity for 2026 production cycles. Beyond sustainability, Germany remains a center for automotive coatings innovation. In October 2025, German research laboratories introduced a new fumed silica grade engineered to enhance scratch resistance and surface durability in automotive clear coats, extending the aesthetic lifespan of premium vehicle finishes and reinforcing fumed silica’s role in value-added surface engineering.

Japan: Electronics Precision and Specialty Oxides Leadership

Japan’s fumed silica market is defined by electronics, precision processing, and advanced materials integration. In October 2025, Evonik, through a joint venture with Mitsubishi Materials, inaugurated the Alu5 facility in Yokkaichi. The site serves as a core Asia-Pacific hub for fumed alumina and silica used in ultra-thin battery separator coatings, addressing rising demand for safety and uniformity in high-energy-density cells.

Digitalization is strengthening customer engagement. On June 25, 2025, Tokuyama Corporation launched a dedicated digital platform for its REOLOSIL fumed silica portfolio, providing real-time rheology and dispersion data for semiconductor-grade matting agents. This capability is aligned with the 2026 electronics manufacturing cycle, where process control at the nanoscale is critical. Following record FY2024 sales, Tokuyama increased its FY2025 dividend while reinvesting heavily in Electronic and Advanced Materials R&D, reinforcing its leadership in CMP applications.

Spain and Ukraine: Distribution Partnerships and Supply Chain Resilience

Southern Europe is emerging as a targeted growth market for cost-efficient fumed silica supply through strategic partnerships. In December 2025, Ukrainian producer Orisil expanded its European footprint via a distribution alliance with Keyser & Mackay, focusing on Spain. The partnership prioritizes high-purity amorphous fumed silica for construction chemicals and adhesives, where demand for anti-sagging and rheology control additives remains robust.

Despite geopolitical pressure, Orisil’s 2025 logistics update confirmed stable supply lines into Southern Europe. Mediterranean paint and coatings manufacturers are increasingly adopting Orisil’s anti-settling additives as cost-competitive alternatives to Asian imports, underscoring the importance of regional diversification and supply resilience in the European fumed silica market.

Summary of Country-Level Strategic Drivers in the Fumed Silica Market

Fumed Silica Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Implications for Fumed Silica

|

|

United States

|

Capacity expansion and purity compliance

|

Growth in EV, elastomer, and cosmetic-grade applications

|

|

China

|

Policy-backed scale and battery integration

|

Export-ready hydrophobic grades and EV electrolyte demand

|

|

Germany

|

Green financing and automotive coatings

|

Sustainable grades and high-value surface engineering

|

|

Japan

|

Electronics precision and digitalization

|

Advanced CMP and battery separator materials

|

|

Spain & Ukraine

|

Distribution partnerships and resilience

|

Cost-effective alternatives for construction and coatings

|

Fumed Silica Market Report Scope

Fumed Silica Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.4 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Type (Hydrophilic Fumed Silica, Hydrophobic Fumed Silica), By Surface Area (Low Surface Area, Medium Surface Area, High Surface Area), By Application (Silicones and Elastomers, Paints, Coatings and Inks, Adhesives and Sealants, Personal Care and Cosmetics, Pharmaceuticals, Electronics and Batteries, Agriculture, Food and Beverages), By Grade (Food Grade, Industrial Grade, Pharma and High-Purity Grade)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, Cabot Corporation, Wacker Chemie AG, Tokuyama Corporation, OCI Company Ltd., Applied Material Solutions Inc., Hubei Huifu Nanomaterial Co., Ltd., Orisil, China National Bluestar Group Co., Ltd., Henan Xunyu Chemical Co., Ltd., Kemitura A/S, Tosoh Corporation, Chifeng Shengsen Silicon Technology Co., Ltd., KoreChem Inc., Tata Chemicals Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fumed Silica Market Segmentation

By Type

- Hydrophilic Fumed Silica

- Hydrophobic Fumed Silica

By Surface Area

- Low Surface Area

- Medium Surface Area

- High Surface Area

By Application

- Silicones and Elastomers

- Paints, Coatings and Inks

- Adhesives and Sealants

- Personal Care and Cosmetics

- Pharmaceuticals

- Electronics and Batteries

- Agriculture

- Food and Beverages

By Grade

- Food Grade

- Industrial Grade

- Pharma and High-Purity Grade

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fumed Silica Industry

- Evonik Industries AG

- Cabot Corporation

- Wacker Chemie AG

- Tokuyama Corporation

- OCI Company Ltd.

- Applied Material Solutions Inc.

- Hubei Huifu Nanomaterial Co., Ltd.

- Orisil

- China National Bluestar Group Co., Ltd.

- Henan Xunyu Chemical Co., Ltd.

- Kemitura A/S

- Tosoh Corporation

- Chifeng Shengsen Silicon Technology Co., Ltd.

- KoreChem Inc.

- Tata Chemicals Limited

*- List not Exhaustive