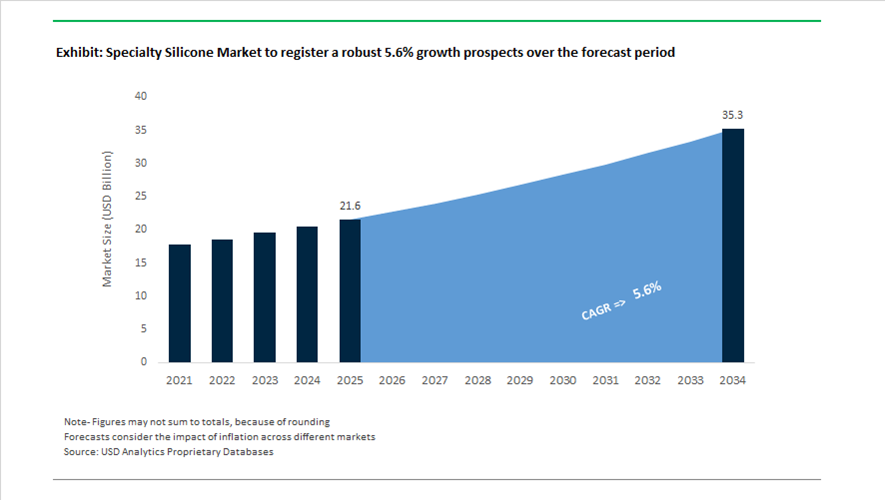

Specialty Silicone Market Valuation 2025–2034: $21.6 Billion to $35.3 Billion at 5.6% CAGR Driven by Electronics-Grade Expansion, Sustainable Elastomers, and Portfolio Restructuring

The global specialty silicone market is valued at $21.6 billion in 2025 and is projected to reach $35.3 billion by 2034, registering a CAGR of 5.6%. Growth is being shaped by rising demand for high-purity silicone elastomers, functional silicone emulsions, medical-grade silicone gels, thermal management silicones, and electronics-grade silicone materials used in EV power modules, semiconductors, advanced medical devices, aerospace components, and additive manufacturing. Manufacturers are actively shifting portfolios from commodity sealants toward high-margin specialty silicones engineered for precision electronics, low-carbon personal care, and 3D printed silicone components. Supply chain restructuring, bio-based feedstocks, and catalyst cost volatility are simultaneously influencing capital allocation and pricing strategies across Asia-Pacific, North America, and Europe.

Strategic consolidation accelerated in May 2024 when KCC Corporation finalized its acquisition of Momentive Performance Materials, integrating advanced specialty silicone technologies into KCC’s global industrial footprint to strengthen its position in automotive and aerospace silicone applications. In early 2024, Siltech Corporation operationalized a new 200,000-square-foot facility in Fort Erie, Ontario, doubling organo-functional silicone capacity and incorporating semi-continuous processing technologies for high-value specialty grades. In May 2024, Shin-Etsu Chemical announced the construction of a new 2.1-billion-yen silicone plant in Pinghu City, Zhejiang Province, scheduled for completion in February 2026 to produce eco-friendly silicone emulsions and functional silicone materials. In October 2024, Momentive Technologies acquired Sibelco’s spherical alumina and spherical silica business, reinforcing filler and ceramics capabilities critical for silicone-based thermal interface materials used in electronics cooling systems.

Capacity expansion in Asia intensified through 2024 and 2025. Dow advanced a $500 million investment at its Zhangjiagang site, targeting a 40% increase in electronics-grade silicone production to serve semiconductor and EV markets. In May 2025, Wacker commissioned new specialty silicone production plants at Zhangjiagang to address demand for medical-grade elastomers and electronics silicones across Asia. In the same month, Dow introduced Decarbia™ reduced-carbon silicone elastomers, supported by Life Cycle Analyses and verified carbon-neutral positioning, aimed at conscious beauty and personal care formulations. In July 2025, Stratasys and Shin-Etsu launched P3™ Silicone 25A for the Origin® DLP 3D printing platform, expanding additive manufacturing applications for high-performance silicone parts in healthcare and industrial sectors. In November 2025, Wacker presented a biomethanol-based silicone gel for wound care at COMPAMED, reinforcing the shift toward sustainable, medical-grade silicone adhesives.

Portfolio realignment and pricing recalibration are defining 2026 dynamics. In late 2025, Elkem announced a definitive agreement to sell the majority of its Silicones division to Bluestar, with closing expected in the first half of 2026, repositioning Elkem as a pure-play materials company. In February 2026, Wacker implemented price increases of 25% or more across silicone product lines, citing a doubling in platinum catalyst costs essential for addition-curing specialty silicones. These acquisitions, electronics-focused expansions, bio-based silicone innovations, additive manufacturing launches, and pricing adjustments are reshaping competitive positioning in the specialty silicone market through 2034.

Structural Trends and Strategic Opportunities in the Specialty Silicone Market

Semiconductor-Grade Silicones as a Core Enabler of Advanced Chip Packaging

The Specialty Silicone Market is entering a structurally elevated demand phase as the semiconductor industry pivots toward chiplet architectures, Fan-Out Wafer-Level Packaging (FOWLP), and high-density heterogeneous integration. These packaging formats impose extreme requirements on materials purity, ionic cleanliness, and thermal stability, making semiconductor-grade silicone elastomers and gels non-substitutable. In advanced logic and AI accelerators, even trace ionic contamination can degrade yields, while stacked dies and dense interconnects generate localized thermal stress that must be managed over long operating lifetimes.

Capital investment trends underline the permanence of this shift. In July 2025, Wacker Chemie AG commissioned its Etching Line Next facility in Burghausen, representing an investment exceeding €300 million. The project is explicitly designed to scale hyper-pure polysilicon and silicone-based precursors for AI and advanced logic chips, reinforcing Wacker’s strategic positioning as a backbone supplier to global semiconductor value chains. Industry estimates indicate that every second computer chip worldwide relies on Wacker materials, highlighting the systemic importance of semiconductor-grade silicones.

Packaging-driven revenue growth is accelerating this demand. By late 2025, advanced packaging adoption surged alongside AI processors such as NVIDIA’s Blackwell platform, which utilizes CoWoS-L technology. Assembly and test leaders, including ASE Technology, are scaling silicone-based underfills, temporary bonding materials, and encapsulants in line with projected packaging and testing revenues of approximately $1.6 billion for 2025. This positions specialty silicones as a critical consumable tied directly to semiconductor capital expenditure cycles.

Medical-Grade Silicones as Non-Negotiable Materials for Long-Life Implants

In parallel, regulatory tightening in the healthcare sector is reinforcing the strategic role of specialty silicones in active implantable medical devices. Updates under the EU Medical Device Regulation and FDA ISO 10993 frameworks have intensified scrutiny of material biocompatibility, extractables, and long-term stability. As of January 2025, the FDA’s Center for Devices and Radiological Health increased its focus on material toxicity in neonatal, cardiovascular, and neurostimulation implants, effectively narrowing the list of acceptable elastomers.

Medical-grade silicones meeting USP Class VI standards are increasingly specified for pacemakers, neurostimulators, and next-generation “smart” implants due to their ability to deliver hermetic sealing, low compression set, and exceptional resistance to hydrolysis and oxidative degradation. Liquid Silicone Rubber formulations are now widely used for precision-molded O-rings, gaskets, and encapsulation layers that must protect embedded electronics from bodily fluids for 10 to 15 years without dimensional drift. This non-substitutable performance profile is anchoring long-term demand for specialty silicones in regulated medical applications.

High-Performance Silicone TIMs for Ultra-Dense AI Data Centers

The rapid scaling of generative AI is pushing server rack power densities beyond 40 kW, a threshold where traditional air cooling becomes inefficient and operationally risky. This shift is creating a premium opportunity for specialty silicone Thermal Interface Materials, including gels, greases, and gap fillers with thermal conductivities exceeding 7 W/m·K. These materials are critical for managing the intense heat flux generated by high-end GPUs and accelerators while maintaining mechanical compliance across repeated thermal cycles.

Product innovation is closely aligned with this demand. At Data Centre World 2025, Dow highlighted its DOWSIL TC-5960 and TC-3080 curable thermal gels, engineered for high-performance AI workloads. These silicone TIMs are designed to resist pump-out and dry-out phenomena, ensuring consistent thermal contact between chips and heat sinks over thousands of on-off cycles. From an operational perspective, advanced silicone TIMs are becoming a lever for sustainability, as cooling systems can account for up to 40% of total power consumption in high-density data centers. Improved thermal efficiency directly supports reductions in energy use, water consumption, and associated greenhouse gas emissions.

Closing the Circularity Gap through Recyclable Silicone Elastomers

Sustainability pressures from consumer electronics, medical devices, and textiles are catalyzing innovation in recyclable silicone materials. Historically, cross-linked silicone rubbers have posed significant end-of-life challenges, but chemical depolymerization and thermoplastic silicone technologies are now reshaping the industry’s circularity profile.

A key breakthrough occurred in November 2025 when Shin-Etsu Chemical announced a recyclable thermoplastic silicone capable of injection molding and end-of-life recycling. The material retains Shore A hardness above 80 and elongation exceeding 800%, making it suitable for demanding applications such as medical coatings and wearable device components.

Mechanical recycling pathways are also gaining traction. In September 2025, Elkem validated a process enabling up to 50% reincorporation of cross-linked High Consistency Rubber waste into new formulations without compromising mechanical performance. Complementing this, Elkem’s SILCOLEASE RE product line, launched in April 2025, utilizes 100% recycled silicone-based fluids for release coatings in the label industry, delivering a reported 70% reduction in carbon footprint. Together, these developments signal that circularity is evolving from a pilot concept into a commercially viable growth engine within the Specialty Silicone Market.

Specialty Silicone Market Share and Segmentation Insights

Specialty Silicone Elastomers Lead the Market Through High-Performance Sealing and Protection Applications

Specialty elastomers accounted for 32.80% of the specialty silicone market in 2025, reflecting their extensive use in applications requiring thermal stability, mechanical flexibility, and long-term durability. These materials include high-temperature vulcanizing silicone, liquid silicone rubber, and room-temperature vulcanizing silicone systems, which are widely used in automotive components, electronic device protection, and medical devices. Their ability to maintain elasticity across a wide temperature range makes them suitable for demanding environments. A major 2025 market driver is the expansion of electric vehicle manufacturing, where silicone elastomers are used in battery pack sealing systems, cooling system components, and electrical connector seals that require resistance to heat, fluids, and vibration.

Automotive and Transportation Sector Drives Specialty Silicone Demand

Automotive and transportation represent the largest application segment in the specialty silicone market, accounting for 32.80% of global consumption in 2025 due to the wide range of silicone materials used in vehicle manufacturing. Silicone components are used in seals, gaskets, hoses, wire insulation, adhesives, and thermal management systems, supporting reliable performance under extreme operating conditions. The durability and temperature stability of silicone materials make them essential for modern automotive engineering. A key 2025 industry trend is the increasing demand for advanced thermal management solutions in electric vehicles, where thermally conductive silicone materials such as gap fillers, encapsulants, and thermal interface compounds help dissipate heat from battery modules and power electronics while maintaining electrical insulation and vibration protection.

Specialty Silicone Market Competitive Landscape

The specialty silicone market in 2026 is defined by carbon transparency, low-carbon silicone platforms, and high-performance materials for EVs, healthcare, and electronics. Leading players are advancing PCF-certified silicones, thermal interface materials, and sustainable silane chemistries while expanding regional manufacturing to support semiconductor and mobility demand.

Wacker Chemie Expands Specialty Silicone Capacity and Advances Low-Carbon Manufacturing for EV and Healthcare Applications

Wacker Chemie is leading specialty silicone innovation through its Strategy 2030 and strong R&D-driven growth. The company reported €5.49 billion in 2025 sales, with silicones contributing €2,733 million. It expanded production capacity in China and established a Specialty Silanes Technology Center to support electronics demand. Wacker introduced biomethanol-based silicone gels for wound care and advanced silicone gap fillers for EV battery safety and thermal management. Production of hybrid polymers at Nünchritz and the transition to biogenic carbon in silicon metal manufacturing are reducing Scope 1 emissions. Its local-to-local supply strategy strengthens its position in high-growth specialty silicone markets.

Shin-Etsu Drives Carbon-Neutral Silicone Innovation and Expands High-Purity Materials for Electronics and EV Systems

Shin-Etsu is accelerating specialty silicone growth through sustainability-focused innovation and large-scale investments. The company committed over ¥100 billion to develop environmentally friendly silicone products and carbon-neutral manufacturing. Its Green Silicones™ portfolio introduces certified carbon-neutral materials alongside recyclable thermoplastic silicones and water-based resins. The CLG gap filler series enhances thermal stability and reliability in high-density electronics and EV battery systems. Expansion of its Akron facility increases capacity for liquid injection molding systems and specialty silanes in North America. Shin-Etsu continues to dominate high-purity silicone and thermal interface material markets.

Dow Launches Decarbia™ Platform and Expands Silicone-Organic Hybrid Technologies for Sustainable Applications

Dow is advancing decarbonized silicone materials through its Decarbia™ platform, offering low-carbon elastomer blends with verified environmental product declarations. The company is scaling silicone-organic hybrid resins for applications in NIR-reflective coatings and high-performance adhesives. Its DOWSIL™ optical silicones enable up to 95% light transmission for LED and display technologies. Dow is also focusing on thermally conductive silicones for semiconductor assembly and electronics protection. By 2026, the company aims to provide full product carbon footprint certification across its specialty silicone portfolio. Its integrated supply chain enhances carbon efficiency from raw materials to finished products.

Momentive Strengthens Tire and Thermal Management Solutions with Advanced Silane Chemistry and High-Performance Silicones

Momentive is focusing on specialty silicones for green tires and advanced thermal management applications following its acquisition by KCC Corporation. The joint venture with Hungpai expands silane production capacity in Asia to support sustainable mobility trends. Its NXT™ P97 and NRX™ silanes improve rolling resistance and energy efficiency in tire applications. The SilCool™ TIG 210 BX thermal grease delivers high conductivity and low bleed performance for automotive ECUs. Momentive is scaling fluorinated liquid silicone rubbers for extreme chemical resistance in aerospace and industrial applications. Its portfolio emphasizes high-performance silicones for EVs, automotive, and energy sectors.

Elkem Restructures Silicone Portfolio and Shifts Focus Toward High-Value Medical and Energy Applications

Elkem is undergoing a strategic transformation through the divestment of its silicones division to Bluestar, expected to close in 2026. The company reported NOK 248 million EBITDA for its silicones segment in Q4 2025, with specialty products outperforming despite pricing pressures. Its R&D efforts in France focused on biocompatible silicones and aerospace-grade coatings. Elkem is reducing production capacity in Norway to manage supply while reallocating capital toward high-growth carbon solutions. The company is strengthening its position in medical-grade elastomers and energy-sector insulation materials. This restructuring reflects a shift toward higher-margin specialty applications.

Shin-Etsu Silicones of America Expands Advanced Dispersants and Conformal Coatings for Electronics and Clean Beauty Markets

Shin-Etsu Silicones of America is expanding its specialty silicone footprint through innovation in dispersants and electronic coatings. The Akron facility expansion supports growing demand for silanes and liquid injection molding systems. Its latest cosmetic silicone dispersants address color stability and UV resistance challenges in high-load formulations. The MR-COAT series provides high-elongation conformal coatings for PCBs, improving durability in automotive and electronic devices. The company continues to strengthen its presence in clean beauty and advanced electronics markets. Its focus on anhydrous systems and high-performance dispersants supports next-generation formulation requirements.

United States Specialty Silicone Market Driven by Closed-Loop Integration and Semiconductor Demand

The United States specialty silicone industry is increasingly shaped by upstream integration, carbon reduction mandates, and electronics-led demand growth. By late 2025, Wacker Chemie fully integrated its Charleston, Tennessee complex into a closed-loop production hub that converts hyper-pure polysilicon byproducts into pyrogenic silica. This internal feedstock loop materially strengthens supply security for high-end silicone elastomers used in electronics, mobility, and advanced industrial applications. Parallel to this structural optimization, the CHIPS and Science Act has begun channeling funding toward upstream material suppliers, accelerating domestic development of electronic-grade silicone fluids designed for immersion cooling in AI data centers and high-density computing environments.

Sustainability and regulatory compliance are simultaneously redefining product portfolios. Momentive Performance Materials reported a 40% reduction in Scope 1 and 2 emissions since 2021, supported by 47% renewable electricity usage across U.S. silicone plants. In late 2025, the company introduced 100% bio-attributed silicone surfactants using mass-balance certified feedstocks, targeting polyurethane foams and industrial formulations. In parallel, Dow launched its Decarbia reduced-carbon platform, delivering carbon-neutral silicone elastomer blends validated through third-party life cycle analyses. State-level PFAS restrictions effective 2025 have further accelerated the shift toward non-fluorinated silicone release coatings for labels and packaging.

China Specialty Silicone Market Anchored in Capacity Expansion and Circular Materials

China’s specialty silicone market is scaling through capacity expansion while aligning with national green manufacturing standards. Shin-Etsu Chemical is scheduled to complete a new functional silicone emulsion plant in Pinghu, Zhejiang Province by February 2026, reinforcing regional supply of eco-friendly silicone products. In March 2025, Wacker Chemie completed a major expansion at Zhangjiagang, significantly increasing downstream capacity for specialty silicone fluids and emulsions serving textiles and personal care.

Innovation is increasingly oriented toward AI and circularity. At CIIE 2025, Elkem introduced BLUESIL ESA 7790, an ultra-high thermal conductivity encapsulant engineered for AI chips operating under sustained thermal loads. Later in 2025, Elkem launched its Sircle product line in China, integrating recycled and bio-based inputs to help customers address Scope 3 emission requirements. These developments align with MIIT’s 2025 roadmap mandating that 80% of new electronics components use low-VOC or solvent-free specialty silicone sealants.

Japan Specialty Silicone Market Defined by Ultra-High Purity and High-Temperature Performance

Japan remains a global benchmark for ultra-high-purity and high-value specialty silicones, driven by semiconductor and advanced mobility requirements. In its late 2025 fiscal briefing, Shin-Etsu Chemical reported a record 21.15% net margin, underpinned by prioritization of ultra-high-purity silicone wafers and specialty photoresists for 2 nm chip fabrication. To reinforce pharmaceutical supply chains, the company announced a ¥10 billion investment in April 2025 to double storage capacity and expand specialty L-HPC production at its Naoetsu plant.

Japanese producers are also extending silicone performance envelopes. At CITE Japan 2025, Shin-Etsu showcased high-soft-focus effect silicones targeting premium automotive interiors. In parallel, Tier-1 suppliers operationalized new phenyl-silicone resin lines in late 2025 capable of continuous operation above 300°C, addressing aerospace and extreme-environment applications where conventional silicone systems fail.

Germany Specialty Silicone Market Focused on Portfolio Agility and Recyclability

Germany’s specialty silicone market is closely tied to portfolio restructuring and sustainability-led innovation. In Q4 2025, BASF finalized the separation of its specialty pigments and resins units, including key silicone additives, to create a more agile entity dedicated to high-margin performance materials. This structural shift enables more targeted capital allocation toward electronics, adhesives, and specialty coatings.

Innovation is increasingly centered on circularity. In April 2025, Evonik unveiled its Debonding on Demand concept, using silicone-modified polyurethanes that allow adhesive removal at defined temperatures, simplifying recycling of electronic assemblies. Evonik also achieved ISCC PLUS certification for its Essen site in late 2024 to 2025 and converted all global PU additive production assets to 100% green electricity by May 2025, enabling large-scale supply of certified bio-attributed silicone additives.

France Specialty Silicone Market Strengthened by Medical and Elastomer Innovation

France plays a critical upstream and R&D role in the European specialty silicone landscape. In late 2024, Elkem completed a €36 million upgrade of its Roussillon upstream plant, raising effective silicone intermediate capacity to 100,000 metric tons per year to support EMEA demand for specialty elastomers. This capacity expansion enhances supply resilience for high-specification applications.

Product innovation remains a differentiator. In March 2025, Elkem Silicones’ France-based R&D team received the Ringier Technology Innovation Award for BLUESIL LSR 3935, a liquid silicone rubber optimized for precision medical device injection molding. This reinforces France’s position in regulated, high-value silicone medical applications.

India Specialty Silicone Market Accelerated by Semiconductor Policy and Local Production

India’s specialty silicone demand is rapidly scaling under policy-driven electronics manufacturing. The approval of four semiconductor units in August 2025 under the India Semiconductor Mission has triggered a sharp rise in demand for electronic-grade silicone potting compounds, encapsulants, and thermal interface materials. These materials are increasingly critical for chip packaging, power electronics, and assembly-level reliability.

Domestic capacity is responding to policy incentives. Local producers such as Elkay Chemicals expanded specialty silicone fluid capacity in late 2025, supported by the Production Linked Incentive scheme for specialty chemicals. This combination of import substitution and demand-side pull is positioning India as an emerging regional market for high-purity and application-specific silicone systems.

Comparative Snapshot: Specialty Silicone Industry by Country

Specialty Silicone Market County Level Snapshot

|

Country

|

Strategic Focus

|

Core Specialty Silicone Applications

|

Structural Direction

|

|

United States

|

Closed-loop integration and decarbonization

|

Pyrogenic silica elastomers, electronic-grade fluids

|

Semiconductor-led localization and PFAS-free reformulation

|

|

China

|

Capacity expansion and circular products

|

Thermal encapsulants, silicone emulsions

|

Low-VOC compliance and AI-ready materials

|

|

Japan

|

Ultra-high purity and high-temperature systems

|

Photoresists, phenyl-silicone resins

|

Margin-led focus on semiconductors and aerospace

|

|

Germany

|

Portfolio agility and recyclability

|

Silicone additives, debondable adhesives

|

Carve-outs and green electricity adoption

|

|

France

|

Medical-grade elastomers

|

LSR for medical devices

|

Upstream capacity and regulated innovation

|

|

India

|

Semiconductor-driven demand

|

Potting compounds and specialty fluids

|

PLI-backed domestic production expansion

|

Specialty Silicone Market Report Scope

Specialty Silicone Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.6 Billion

|

|

Market Size (2034)

|

$35.3 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Specialty Elastomers, Specialty Fluids and Emulsions, Specialty Resins, Silicone Gels and Thermal Interface Materials, Silicone Adhesives and Sealants, Specialty Surfactants and Antifoams), By Application (Electronics and Semiconductors, Automotive and Transportation, Healthcare and Medical, Personal Care and Cosmetics, Building and Construction, Industrial and Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, Momentive Performance Materials Inc., Elkem ASA, Evonik Industries AG, KCC Corporation, Mitsubishi Chemical Group, SABIC, Huber Engineered Materials, Gelest, Inc., Elkay Chemicals Pvt. Ltd., Zhejiang Wynca Chemical Group, Hoshine Silicon Industry Co., Ltd., BRB International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Silicone Market Segmentation

By Product Type

Liquid Silicone Rubber

High Consistency Rubber

Room Temperature Vulcanizing Silicone

- Specialty Fluids and Emulsions

- Specialty Resins

- Silicone Gels and Thermal Interface Materials

- Silicone Adhesives and Sealants

- Specialty Surfactants and Antifoams

By Application

- Electronics and Semiconductors

- Automotive and Transportation

- Healthcare and Medical

- Personal Care and Cosmetics

- Building and Construction

- Industrial and Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Silicone Industry

- Dow Inc.

- Shin-Etsu Chemical Co., Ltd.

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Elkem ASA

- Evonik Industries AG

- KCC Corporation

- Mitsubishi Chemical Group

- SABIC

- Huber Engineered Materials

- Gelest, Inc.

- Elkay Chemicals Pvt. Ltd.

- Zhejiang Wynca Chemical Group

- Hoshine Silicon Industry Co., Ltd.

- BRB International

*- List not Exhaustive