Silicone Additives Market Valuation 2025–2034: $4.1 Billion to $8.1 Billion at 7.9% CAGR Accelerated by PFAS Replacement and High-Performance Formulations

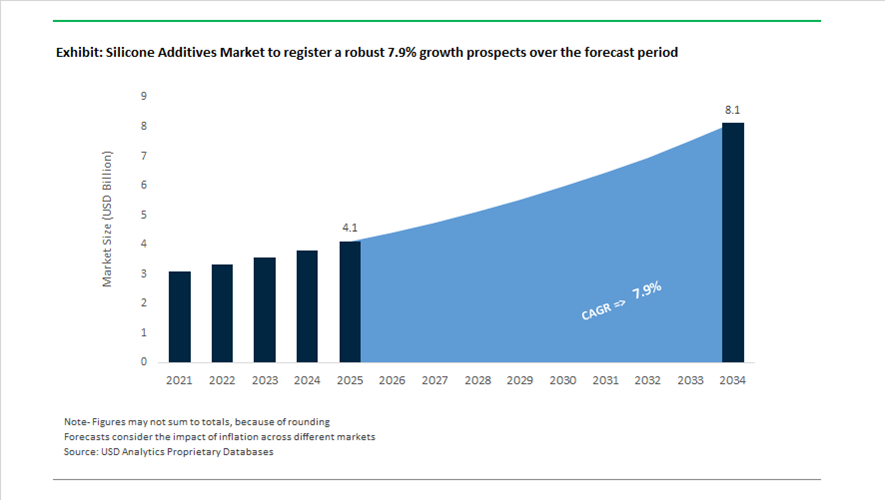

The global silicone additives market is valued at $4.1 billion in 2025 and is projected to reach $8.1 billion by 2034, expanding at a CAGR of 7.9%. Growth is anchored in rising demand for high-performance silicone surfactants, defoamers, leveling agents, slip additives, and polymer processing aids across coatings, construction, personal care, packaging films, polyurethane foams, electronics encapsulation, and renewable energy infrastructure. Silicone additives improve surface wetting, dispersion stability, scratch resistance, lubricity, UV durability, and dielectric performance, making them critical in advanced coatings, EV battery modules, 5G infrastructure, and sustainable packaging. The phase-out of PFAS-based materials in food-contact and industrial applications is creating a structural replacement cycle that directly benefits silicone-based polymer processing aids and surface modifiers.

In May 2024, Momentive Performance Materials completed the acquisition of a significant portion of Elkem ASA’s silicones business, consolidating European manufacturing assets and reinforcing its global position in high-performance silicone additives. During 2024–2025, Shin-Etsu Chemical progressed with its ¥100 billion investment plan to expand highly functional silicone product lines in Gunma and Naoetsu, Japan, with specific emphasis on environmentally optimized and high-purity silicone additives. In March 2025, Dow launched its downstream silicones expansion project in Zhangjiagang, China, establishing an integrated production model spanning monomers to value-added additives for 5G electronics, electric vehicle battery insulation, and renewable energy components.

Portfolio innovation and regulatory-driven product reformulation intensified throughout 2025. In March 2025, Croda International introduced its first bio-based silicone additives targeting cosmetics and premium packaging applications, offering reduced carbon footprint without compromising tactile performance and release efficiency. In April 2025, BASF SE secured regulatory approval to acquire Solvay’s European silicones business, integrating specialized silicone additive capabilities into its construction chemicals and automotive coatings segments. In May 2025, Evonik transitioned its global polyurethane silicone additive production footprint to 100% green electricity, covering key sites in the United States and Japan, reinforcing ESG positioning in the specialty additives sector. In September 2025, Dow launched DOWSIL™ 5-1050, a silicone-based polymer processing aid designed to replace fluoropolymer-based additives ahead of the August 2026 EU ban on PFAS in food-contact materials.

Advanced product engineering continued into 2026. In July 2025, Wacker unveiled POWERSIL® 1900 A/B, a high-consistency silicone rubber additive developed for spiral extrusion of composite insulators used in high-voltage power transmission systems. In early 2025, KCC Silicone introduced SeraSense AG-21, a multifunctional silicone fluid additive designed to enhance spreadability in personal care formulations and improve lubricating efficiency in industrial systems. In February 2026, Elkem announced a final agreement to divest its Silicones division to Bluestar through a share swap arrangement, enabling Elkem to refocus on silicon products and carbon materials. This structural reorganization reshapes competitive alignment across the silicone additives landscape while reinforcing specialization in high-value, performance-driven applications.

High-Impact Trends and Scalable Opportunities in the Global Silicone Additives Market

Automotive Coating Evolution Driven by Electrification and Lightweight Multi-Material Platforms

The rapid expansion of electric vehicles and the parallel shift toward lightweight, multi-material vehicle architectures are redefining requirements for automotive coatings and surface additives. Traditional paint systems optimized for steel substrates are proving inadequate for carbon fiber composites, aluminum, and advanced polymers now used in EV body structures and battery enclosures. As a result, OEMs and Tier 1 suppliers are increasingly specifying silicone-modified clearcoats and functional silicone additives that deliver superior leveling, defect suppression, and long-term surface durability on non-metallic substrates.

At K 2025, leading silicone producers such as WACKER and Dow introduced ceramifying silicone additives engineered for EV busbars and battery housings. These materials are designed to form a ceramic-like insulating layer under extreme thermal stress, a critical safety requirement for 800 volt and 1,200 volt vehicle architectures where electrical isolation failure can trigger cascading system faults. Beyond safety, aesthetic durability has become a defining differentiator for premium EV brands. Industry validation tests now require silicone additives to deliver up to 90% gloss retention after standardized car wash abrasion cycles, reinforcing their role in achieving mar resistance and long-term visual appeal. With silicone-related automotive components projected to reach approximately $7.52 billion in value by the end of 2025, these performance-driven specifications are structurally lifting demand for high-functionality silicone additives.

Regulatory Pivot and Clean Label Reformulation in Consumer Care Products

Regulatory pressure is emerging as a second structural demand shaper in the silicone additives market, particularly within personal care and home care formulations. The European Union’s REACH restrictions on cyclic siloxanes are forcing formulators to redesign product architectures around linear, high-molecular-weight silicones or bio-based hybrid alternatives that preserve sensory performance while meeting compliance thresholds. As of March 2025, the European Chemicals Agency confirmed enforcement timelines for the inclusion of D6 alongside D4 and D5, with a strict 0.1% by weight limit for leave-on products becoming enforceable by June 2027.

This regulatory inflection has already driven a reported 25% increase in R and D spending among global consumer brands such as L’Oréal and Unilever as they race to secure compliant silicone substitutes. The European Commission estimates that these measures could reduce cumulative silicone emissions to air and water systems by up to 90% by 2030. In response, plant-based methanol derived eco-series silicones are gaining traction in 2025 as the preferred solution for ESG-aligned consumer brands, repositioning compliant silicone additives as value-enhancing ingredients rather than regulatory liabilities.

Thermally Stable Silicone Antifoams for Lithium-Ion Battery Manufacturing

The rapid localization of lithium-ion battery production through gigafactory investments is creating a high-value opportunity for silicone antifoams, wetting agents, and dispersants engineered for extreme processing conditions. Modern battery electrode manufacturing relies on high-speed coating of aqueous slurries containing silicon anodes and high-nickel cathodes, where even microscopic air entrapment can cause coating defects that lead to thermal runaway risks.

In December 2025, BYK launched its BYK-ET 3000 series, specifically formulated for high-shear, high-temperature electrode slurry environments. These additives maintain performance stability during aggressive drying cycles and prevent crater formation that can compromise battery safety. As battery manufacturers such as ProLogium accelerate adoption of aqueous binders to reduce VOC emissions, demand is rising for silicone defoamers that remain effective in the presence of conductive carbons. Industry assessments indicate that optimized silicone antifoams can improve production yields by up to 15% by eliminating micro-bubble related defects, positioning them as a yield-enhancing process enabler rather than a cost input.

Functional Silicone Additives Enabling Industrial-Scale Additive Manufacturing

A parallel growth opportunity is emerging as additive manufacturing transitions from prototyping to full-scale production of end-use components. Silicone additives are increasingly specified to impart injection-mold-like surface quality, flexibility, and durability to printed resins and filaments, particularly in medical, automotive, and aerospace applications. At Formnext 2025, ALTANA through its Cubic Ink platform showcased resin systems incorporating silicone additives that enable water-breakable silicone molds. This Print and Inject approach allows complex hearing aids and prosthetics to be produced at industrial scale across North America and Europe.

Material science validation published in December 2025 further highlights the role of silicone-related additives in reinforcing thermoplastic filaments. Studies demonstrate that silicon nitride nanoparticle incorporation in PA12 can increase tensile strength and elastic modulus by more than 20%. This opens a pathway for silane-treated silicone additives to function as compatibilizers in load-bearing 3D printed components, supporting the next generation of aerospace and defense additive manufacturing applications where mechanical reliability and surface integrity are non-negotiable.

Silicone Additives Market Share and Segmentation Insights

Defoamers & Antifoaming Agents Dominate Silicone Additives Market Across Industrial Processing Applications

Defoamers and antifoaming agents accounted for 22.40% of the silicone additives market in 2025, making them the most widely used silicone additive category across industrial manufacturing processes. Silicone-based defoamers deliver highly effective foam suppression at very low concentrations, combined with excellent thermal stability, chemical inertness, and compatibility with diverse formulations. These properties make them essential in industries such as paints and coatings, wastewater treatment, food processing, pulp and paper, and chemical manufacturing. A notable 2025 development is the increasing demand for food-grade silicone defoamers, where manufacturers are producing formulations that meet stringent food contact and pharmaceutical purity regulations, enabling their safe use in sensitive processing environments requiring strict product purity.

Paints & Coatings Industry Drives Silicone Additive Demand for Surface Performance Enhancement

Paints and coatings represent the largest end-use segment in the silicone additives market, accounting for 28.40% of global consumption in 2025 due to the critical role silicone additives play in improving coating surface properties. Silicone-based additives provide leveling, slip, mar resistance, foam control, and water repellency, enabling the production of high-performance architectural, industrial, and automotive coatings. The scale of global coatings manufacturing continues to support strong demand for silicone additives across multiple product types. A major 2025 innovation trend is the development of advanced high-performance coating formulations, including self-cleaning, anti-graffiti, anti-ice, and extreme weather-resistant coatings, where functional silicone additives deliver durable surface modification capabilities that cannot be achieved with conventional organic additives.

Silicone Additives Market Competitive Landscape

The 2026 silicone additives market is shaped by regulatory pressure on cyclic siloxanes, AI-driven formulation, and demand for low-VOC, circular silicone chemistries. Leading players are advancing bio-based feedstocks, thermoplastic silicones, and battery-grade additives to support EVs, coatings, and advanced manufacturing applications.

Evonik advances high-performance dispersants and distribution optimization for coatings and digital printing

Evonik Industries AG is reinforcing its leadership in silicone additives through its Custom Solutions segment, focusing on high-margin coatings and green energy applications. The company reported 2025 adjusted EBITDA of €1.87 billion and maintains a 2026 outlook of €1.7–€2.0 billion despite a 7% sales decline. Its 2026 distribution restructuring across North America enhances technical service via partners like Andicor, Palmer Holland, and Chem-Materials. The launch of TEGO® Dispers 695 targets radiation-curing inks and high-performance polyurethane systems, addressing digital printing demands. Expansion in hydroxyl-terminated polybutadienes (HTPB) supports aerospace adhesives and sealants. This integrated strategy positions Evonik at the forefront of smart coatings and additive innovation.

Dow accelerates carbon-neutral silicone additives with Decarbia platform and VORASURF™ expansion

Dow Inc. is leading the shift toward carbon-neutral silicone additives through its Decarbia platform, integrating low-carbon silicon feedstocks with advanced additive performance. The company introduced low-carbon silicone elastomers backed by Environmental Product Declarations, aligning with Scope 3 emission targets. Its expanded VORASURF™ RF series enhances insulation efficiency in polyurethane foams for refrigeration and cold-chain logistics. The Transform to Outperform initiative targets $2 billion EBITDA uplift, supported by AI-driven process optimization and a $1 billion cost reset in 2026. Dow’s vertically integrated supply chain ensures feedstock security and performance consistency. This positions the company as a leader in sustainable silicone surfactants and industrial additives.

Shin-Etsu pioneers recyclable thermoplastic silicone additives for medical and electronics applications

Shin-Etsu Chemical is redefining silicone additives with its breakthrough thermoplastic silicone, combining recyclability with high mechanical performance (Durometer A 80+ and elongation above 800%). The company is reallocating R&D investments toward filler-free, transparent silicone additives for optical and medical uses. Its Solution-Engineering initiative bridges thermoset durability with thermoplastic processing advantages. Sustainability leadership is reinforced by Platinum ratings and over 75% of operations certified to ISO standards. Applications include soft-touch electronics and advanced medical coatings where purity and flexibility are critical. This innovation positions Shin-Etsu at the forefront of circular silicone materials.

BYK expands EV battery additives and recyclate solutions amid ECHA-driven regulatory transition

BYK-Chemie GmbH is positioning itself as a regulatory leader by developing alternatives to restricted cyclic siloxanes under ECHA guidelines. The company implemented a 5.2% global price increase in 2026 to fund R&D into safer additive chemistries. Expansion into South America via BYK do Brasil strengthens its footprint in automotive and packaging sectors. BYK is gaining traction in EV battery manufacturing by supplying additives for LFP, NCM, and silicon-based electrode slurries. Its SCONA recyclate additives enhance compatibility in recycled polymers, supporting circular economy initiatives. This dual focus on compliance and innovation secures BYK’s role in next-generation materials.

Elkem advances silicone circularity with recycling breakthroughs and medical-grade innovations

Elkem Silicones is undergoing a major transformation following the divestment of its silicones division assets to Bluestar, sharpening its focus on core materials. The company achieved a breakthrough in recycling high-consistency rubber (HCR), enabling over 50% reuse in new formulations without performance loss. Its SILBIONE™ LSR portfolio includes electro-conductive, biocompatible silicones for advanced medical devices and implants. Elkem maintains strong ESG credentials with a CDP “A” rating for environmental performance. The company’s circularity initiatives align with global sustainability mandates and healthcare innovation trends. This positions Elkem as a leader in recyclable silicone technologies.

Wacker strengthens integrated silicone additives portfolio with pricing strategy and pyrogenic silica synergy

Wacker Chemie AG is reinforcing its silicone additives leadership through operational discipline and strategic price adjustments of up to 25% in 2026, driven by rising raw material costs. The Silicones division contributes approximately 50% of total revenue, underscoring its central role in the company’s portfolio. Wacker offers over 2,800 silicone-based products, including fluids, emulsions, and silane-terminated polymers for diverse industrial applications. Its integration with pyrogenic silica production enables optimized additive performance through in-house formulation control. The company’s solutions are critical for energy transmission, coatings, and release liners. This integrated model ensures long-term competitiveness in high-performance silicone additives.

Japan: High-Functionality Leadership Anchored in Electronics and EV Thermal Management

Japan continues to set the technical benchmark in silicone additives by aligning advanced materials innovation with electronics and electrified mobility. In January 2025, Wacker Chemie AG inaugurated a dedicated production line in Tsukuba for silicone-based Thermal Interface Materials, reinforcing Japan’s role as a critical supplier of heat-dissipating gap fillers for traction batteries and power electronics. This capacity expansion coincides with a structural shift toward highly functional silicones, as Shin-Etsu Chemical reported a 6.1% increase in consolidated net sales for FY2024–2025, driven primarily by electronic materials and precision additives.

Upstream capability is being strengthened through ultra-high-purity precursors. In late 2025, Evonik Industries opened its Alu5 fumed alumina plant in Yokkaichi, engineered to produce surface-modified alumina using advanced silicone additives for lithium-ion battery separators. Automotive and semiconductor convergence is accelerating demand for ceramifying silicone rubber additives that form insulating layers during thermal runaway events, while parallel R&D in precision encapsulation additives for HBM3e packaging underpins Japan’s domestic AI-chip ambitions. Environmental compliance further shapes formulation choices, as the 2025 Greenhouse Gas Emission Intensity Index compels manufacturers to adopt low-energy curing silicone additive systems.

South Korea: Memory-Centric Scale-Up and Portfolio Consolidation

South Korea’s silicone additives market is structurally linked to its dominance in memory and advanced packaging. In 2025, Wacker Chemie AG expanded its Jincheon site with a new line for specialized silicone sealants and additives, directly serving semiconductor and automotive OEMs. With High Bandwidth Memory projected to represent a material share of DRAM revenue by late 2025, domestic formulators have accelerated adoption of epoxy molding compound silicone additives tailored for thermal stability and warpage control in stacked-die architectures.

Industry consolidation has reshaped competitive dynamics. KCC Corporation completed the full integration of Momentive Performance Materials, creating a vertically integrated platform spanning functional silicone additives across Asia-Pacific. Beyond semiconductors, South Korean manufacturers are leveraging silane-based additives to enhance TOPCon and HJT solar cell efficiency, while policy support under the K-Semiconductor Belt strategy aims to localize a substantial share of high-purity chemical additives used in wafer fabrication by 2026.

China: Regulatory Reset Driving Water-Borne and Resource-Recovery Systems

China remains the global volume leader in silicone additives, with scale supported by integrated upstream-to-downstream manufacturing. Regulatory developments in 2025 have materially altered formulation strategies. The introduction of the mandatory national standard GB 4806.16-2025 for food-contact silicone rubber imposed stricter VOC indicators, while amendments to the Environmental Protection Tax Law expanded VOC taxation through pilot programs. Together, these measures are accelerating a transition toward water-borne silicone additives and low-emission processing routes.

Policy direction under the Ministry of Ecology and Environment emphasizes resource-recovery silicone systems that minimize heavy metal catalysts, favoring producers with closed-loop process control. Large-scale players such as Hoshine Silicon Industry and Zhejiang Xinan Chemical continue to expand integrated additive circuits. Demand diversification is evident, with rising use of silicone-based super-spreaders in agrochemicals to improve uptake while reducing runoff, and sustained growth in municipal wastewater treatment driving consumption of silicone defoamers aligned with national sewage treatment targets.

United States: Policy-Led Demand from Semiconductors, Infrastructure, and PFAS Substitution

In the United States, silicone additives demand is increasingly policy-driven. CHIPS Act implementation has directed federal subsidies toward on-site ultra-high-purity chemical systems at new semiconductor mega-fabs, benefiting domestic producers of silicone additives for cleanroom-compatible processes. Concurrently, EPA actions on PFAS in 2025 have catalyzed an R&D shift toward PFAS-free silicone-based surfactants and leveling agents in coatings and industrial formulations.

Capital markets and infrastructure spending reinforce this trajectory. Evonik Industries issued a green hybrid bond in September 2025 to fund bio-based methanol inputs for silicone elastomers, reflecting the financialization of sustainability objectives. Federal infrastructure programs have expanded the use of silane-treated fiberglass and silicone water repellents in bridges and highways, while EV supply chain localization has driven scale-up of advanced silicone additives by Dow for green tire and durability-focused mobility applications.

Comparative Snapshot: Silicone Additives by Country

Silicone Additives Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Technical Focus Area

|

|

Japan

|

EV batteries, advanced electronics

|

TIMs, ceramifying additives, HBM encapsulation

|

|

South Korea

|

Memory and packaging

|

EMC silicone additives, solar cell enhancement

|

|

China

|

Regulatory compliance and scale

|

Water-borne systems, defoamers, agro-spreaders

|

|

United States

|

Policy and infrastructure

|

PFAS-free additives, UHP fab systems

|

Silicone Additives Market Report Scope

Silicone Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2034)

|

$8.1 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Product Type (Defoamers & Antifoaming Agents, Wetting & Dispersing Agents, Silicone Surfactants, Rheology Modifiers, Adhesion Promoters, Lubricating & Slip Agents, Leveling Agents, Water Repellents, Thermal Interface Additives), By Form (Silicone Fluids, Silicone Resins, Silicone Gels, Silicone Elastomers), By End-Use Industry (Paints & Coatings, Plastics & Composites, Personal Care & Cosmetics, Healthcare & Medical, Electronics & Semiconductors, Automotive & Transportation, Construction, Agriculture, Food & Beverage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co. Ltd., Momentive Performance Materials Inc., Evonik Industries AG, Elkem ASA, BYK-Chemie GmbH, Siltech Corporation, Gelest Inc., Innospec Inc., Kaneka Corporation, CHT Group, Hoshine Silicon Industry Co. Ltd., Zhejiang Xinan Chemical Industrial Group, Specialty Silicone Products Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicone Additives Market Segmentation

By Product Type

- Defoamers & Antifoaming Agents

- Wetting & Dispersing Agents

- Silicone Surfactants

- Rheology Modifiers

- Adhesion Promoters

- Lubricating & Slip Agents

- Leveling Agents

- Water Repellents

- Thermal Interface Additives

By Form

By End-Use Industry

- Paints & Coatings

- Plastics & Composites

- Personal Care & Cosmetics

- Healthcare & Medical

- Electronics & Semiconductors

- Automotive & Transportation

- Construction

- Agriculture

- Food & Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Additives Industry

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co. Ltd.

- Momentive Performance Materials Inc.

- Evonik Industries AG

- Elkem ASA

- BYK-Chemie GmbH

- Siltech Corporation

- Gelest Inc.

- Innospec Inc.

- Kaneka Corporation

- CHT Group

- Hoshine Silicon Industry Co. Ltd.

- Zhejiang Xinan Chemical Industrial Group

- Specialty Silicone Products Inc.

*- List not Exhaustive