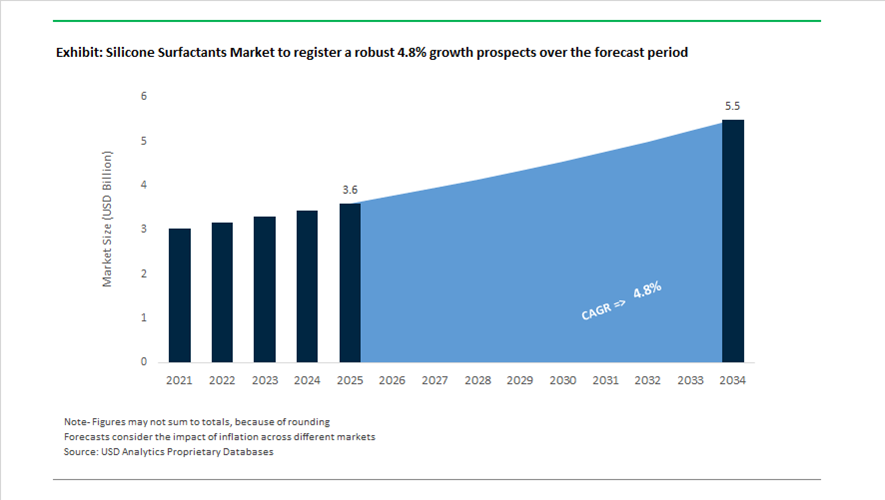

Silicone Surfactants Market Valuation 2025–2034: $3.6 Billion to $5.5 Billion at 4.8% CAGR Driven by PU Foams, Low-VOC Formulations, and Recyclable Silicone Technologies

The global silicone surfactants market is valued at $3.6 billion in 2025 and is projected to reach $5.5 billion by 2034, registering a CAGR of 4.8%. Growth is supported by rising demand for silicone polyether surfactants, emulsifiers, wetting agents, and foam stabilizers across polyurethane (PU) foams, construction insulation, refrigeration cold chain systems, personal care emulsions, industrial coatings, and medical devices. Silicone surfactants provide superior surface tension reduction, foam cell stabilization, hydrophobic-hydrophilic balance control, and compatibility with high-performance resin systems. Increasing regulatory pressure on volatile organic compounds, carbon intensity in chemical feedstocks, and recyclability of polymer systems is reshaping formulation strategies across the specialty surfactant landscape.

In early 2024, Shin-Etsu Chemical launched the KRW-6000 Series, a water-based, fast-curing silicone resin system incorporating surfactant-integrated chemistry that eliminates the need for external emulsifiers. This formulation reduces chemical complexity and VOC emissions in industrial coatings. In April 2024, KCC Corporation completed the full acquisition of Momentive Performance Materials, followed by the January 2025 integration of global silicone operations. The consolidation unified R&D programs for silicone polyethers and specialty emulsifiers used in advanced personal care formulations and industrial coatings. These developments reinforced vertical integration in silicone surfactant precursor and application technologies.

Product innovation and sustainability positioning intensified during 2025. In mid-2025, Dow expanded its VORASURF™ portfolio with next-generation silicone surfactants tailored for rigid PU foams used in commercial refrigeration and cold chain insulation. The formulations are optimized for low-VOC emissions and improved thermal insulation efficiency. In May 2025, Dow introduced its Decarbia™ low-carbon platform, including silicone surfactant-based elastomer blends manufactured from decarbonized silicon metal feedstocks and validated through third-party Environmental Product Declarations. In November 2025, Shin-Etsu announced a recyclable thermoplastic silicone material capable of being melted and reshaped, enabling new recyclable surfactant-treated coatings for medical and consumer electronics applications. At COMPAMED 2025, Wacker Chemie showcased a bio-methanol-derived silicone gel for wound care, leveraging sustainable surfactant chemistry to reduce fossil-carbon dependency while maintaining high adhesion performance.

Structural realignment and localization strategies defined early 2026. In February 2026, Elkem ASA finalized the divestiture of its Silicones division to Bluestar, consolidating surfactant and specialty silicone fluid technologies under Bluestar’s downstream chemicals portfolio. In early 2026, Evonik confirmed measurable impact from its “Tailor Made” efficiency program, streamlining surfactant operations within its Performance Materials division to respond more rapidly to volatility in European construction and home care markets. In December 2025, Wacker strengthened its China Specialty Silanes Center to provide localized support for surfactant precursors serving New Energy Vehicle and 5G infrastructure applications. Shin-Etsu’s ¥2.1 billion Zhejiang plant, scheduled for completion in February 2026, is designed to produce high-functional silicone emulsions and environmentally optimized surfactants for the Asia-Pacific region. These investments, restructuring initiatives, and sustainable chemistry advances are shaping competitive positioning in the silicone surfactants market through 2034.

Regulatory-Led Transformation and High-Value Opportunities in the Global Silicone Surfactants Market

Strategic Reformulation in Consumer Care Driven by EU Volatile Methylsiloxane Restrictions

The silicone surfactants market is undergoing a forced and irreversible reformulation cycle as European regulation reshapes acceptable chemistries in detergents, fabric care, and personal care products. The implementation of Commission Regulation (EU) 2024/1328 has expanded restrictions on cyclic siloxanes D4, D5, and D6 to concentrations below 0.1% by weight across both rinse-off and leave-on products. This regulatory threshold effectively eliminates legacy volatile silicone surfactants from mainstream consumer formulations and accelerates adoption of linear, non-volatile silicone surfactant systems.

Compliance requirements are further tightening through digital traceability. In December 2025, the Council of the European Union approved a revised Detergents and Surfactants Regulation introducing the Digital Product Passport. By 2028, every detergent placed on the EU market must carry a QR-linked digital record detailing surfactant composition, origin, and compliance status. This framework is structurally favoring eco-labeled polyether-modified silicone surfactants with transparent supply chains. Environmental impact assessments published by the European Chemicals Agency project that the expanded VMS ban will cut silicone emissions into air and water systems by up to 90% by 2027. In response, suppliers such as Evonik have launched high-purity linear silicone surfactant portfolios that preserve fabric softness and lubricity while remaining below persistent, bioaccumulative, and toxic thresholds.

Agrochemical Super-Spreader Adoption in Precision and Sustainable Agriculture

A second structural growth trend is unfolding in agrochemicals, where silicone surfactants are being reclassified from optional adjuvants to essential performance enablers. Organosilicone surfactants, particularly trisiloxane-based chemistries, are increasingly specified to address runoff, drift, and poor leaf wetting associated with conventional surfactants. Their ability to reduce water surface tension to near 21 millinewtons per meter allows spray droplets to achieve zero-degree contact angles, ensuring uniform coverage even on waxy or vertical leaf surfaces.

Field trials conducted in March 2025 confirm that this super-spreading effect enables a 15 to 20% reduction in active ingredient application rates per hectare, directly supporting the European Union’s Green Deal objective to halve pesticide usage by 2030. Beyond synthetic crop protection, silicone surfactants are gaining traction in biological formulations. Products such as BREAK-THRU SD 260 from Evonik are being deployed to stabilize microbial biopesticides, improving cell survival and field efficacy. As sustainable agriculture scales globally, silicone surfactants are emerging as a critical interface between environmental compliance and agronomic performance.

Ultra-Low-Foaming Silicone Surfactants for Automated CIP Systems

The rapid automation of industrial hygiene processes is creating a differentiated opportunity for silicone surfactants engineered for extreme Clean-in-Place environments. Food, beverage, and pharmaceutical manufacturers are increasingly relying on automated CIP systems operating under high pressure, high alkalinity, and continuous flow conditions. In these systems, uncontrolled foaming can cause pump cavitation, sensor malfunction, and incomplete cleaning cycles. Silicone surfactants are uniquely positioned as ultra-low-foaming wetting agents and defoamers that remain stable under aggressive chemical and thermal stress.

Automation trends are reinforcing this demand. The International Federation of Robotics reported a 10% increase in global industrial robot installations in 2024, bringing the installed base to 4.28 million units. As automated CIP adoption rises, demand is increasing for silicone surfactants that deliver residue-free breakdown and alkali stability. These materials support compliance in high-value markets such as the United States pharmaceutical import sector, which exceeded $170 billion in 2023. Modern CIP-specific silicone surfactants also enable cleaning at temperatures below 50 degrees Celsius, reducing energy consumption by up to 15% while lowering water usage through fewer rinse cycles.

Silicone Surfactants as Cell Stabilizers in EV Battery Cushioning Foams

The expansion of the electric vehicle battery ecosystem is opening a high-growth opportunity for silicone surfactants as critical foam cell stabilizers. In lithium-ion battery packs, flame-retardant and low-density polyurethane foams are used for cell cushioning, vibration damping, and thermal isolation. Silicone surfactants play an essential role in controlling foam morphology, ensuring uniform closed-cell structures that meet UL 94 V-0 fire safety standards.

In 2024, polyurethane components for EV battery packs alone represented a market exceeding $1.1 billion, with the passenger EV foam segment growing by 17.2% in 2025. New energy vehicle safety standards increasingly specify silicone-modified foams for cell-to-cell compression pads that accommodate battery swelling during charge and discharge while limiting thermal runaway propagation. Material suppliers such as Saint-Gobain and Sheen Technology have qualified silicone-based foams for operating ranges from minus 55 to plus 200 degrees Celsius. In this application, silicone surfactants are a hidden but decisive enabler, delivering the consistent foam architecture required for long-term sealing performance and battery durability across extreme climates.

Silicone Surfactants Market Share and Segmentation Insights

Silicone Polyethers Lead the Silicone Surfactants Market Driven by Versatility in Foam Stabilization and Emulsification

Silicone polyethers accounted for 52.80% of the silicone surfactants market in 2025, making them the dominant product category across multiple industrial and consumer formulations. These surfactants combine silicone backbone properties with polyether chains, enabling excellent surface activity, emulsification, wetting, and stabilization performance. Their tunable hydrophilic–lipophilic balance (HLB) allows formulators to tailor performance for diverse applications such as polyurethane foam stabilizers, personal care emulsifiers, and agricultural adjuvants. A notable 2025 innovation trend is the development of CO₂-philic silicone polyether surfactants designed for supercritical CO₂ processing technologies used in polymer manufacturing and extraction systems. These specialized surfactants enable stable emulsions and foams in CO₂-based processes, expanding the technological scope of silicone surfactant chemistry.

Polyurethane Foams Drive Global Demand for Silicone Surfactants Across Furniture and Insulation Manufacturing

Polyurethane foams represent the largest end-use segment in the silicone surfactants market, accounting for 38.60% of total demand in 2025 due to the critical role silicone surfactants play in foam production. During polyurethane foam formation, silicone surfactants regulate cell nucleation, foam stability, and cell size distribution, ensuring uniform foam structure and mechanical performance. These materials are widely used in flexible foams for furniture, bedding, and automotive seating, as well as rigid foams for thermal insulation in buildings and appliances. A key 2025 market driver is the growing demand for comfort-focused furniture and lightweight automotive materials, combined with increased use of energy-efficient insulation systems, where silicone surfactants enable finer cell structures and improved air flow in both conventional and bio-based polyurethane foam formulations.

Silicone Surfactants Market Competitive Landscape

The 2026 silicone surfactants market is shaped by rising PU foam demand in EV insulation and cold-chain logistics, alongside regulatory-driven shifts to low-cyclic, bio-based siloxanes. Key players are investing in carbon-neutral silicone surfactants, localized production, and high-purity formulations for semiconductor and AI-driven applications.

Dow advances low-carbon silicone surfactants with AI-driven manufacturing and pricing optimization

Dow Inc. is strengthening its silicone surfactants portfolio through its Transform to Outperform initiative, targeting $2 billion in EBITDA growth. The Decarbia™ platform introduces low-carbon silicone surfactants supported by Environmental Product Declarations, aligning with global decarbonization goals. Dow’s Cooling Science Studio in Shanghai accelerates development of dielectric surfactants for AI data center thermal management. With approximately $40 billion in annual sales, the company leverages scale and integration to optimize production via AI and automation. Strategic price increases of 10% to 20% offset rising silicon metal costs and maintain margin resilience. This positions Dow as a leader in sustainable, high-performance silicone surfactants.

Evonik scales PU foam silicone surfactants with streamlined distribution and specialty additive focus

Evonik Industries is focusing on high-margin silicone surfactants for polyurethane foam applications, particularly in insulation for refrigeration and EV battery systems. The company reported €14.1 billion in 2025 sales and projects €1.7 billion to €2.0 billion EBITDA in 2026. Its streamlined North American distribution strategy enhances supply reliability and technical service capabilities. Rising demand for silicone surfactants in rigid PU foams is driving growth within its Custom Solutions segment. The independence of SYNEQT enables sharper capital allocation toward organofunctional siloxanes and specialty additives. This strengthens Evonik’s position in high-performance surfactant systems for industrial and consumer applications.

Shin-Etsu expands ultra-high-purity silicone surfactants with Green Silicones™ and $1.2 billion investment

Shin-Etsu Chemical is investing over $1.2 billion to expand production of advanced silicone surfactants across Japan, Thailand, and the U.S. Its Green Silicones™ roadmap introduces carbon-neutral certified surfactants tailored for semiconductor and electronics markets. The company also developed recyclable thermoplastic silicone materials offering high durability and flexibility, supporting next-generation applications. With projected revenue of ¥2.4 trillion and strong operating income, Shin-Etsu maintains financial strength for continued innovation. Its vertically integrated model ensures consistent quality from raw materials to finished surfactants. This positions the company as a key supplier of ultra-high-purity, sustainable silicone surfactants.

Wacker drives bio-based silicone surfactant innovation with BELNEXT® and localized R&D expansion

Wacker Chemie AG is advancing its silicone surfactants portfolio through Project PACE, targeting over €300 million in annual savings by 2026. The BELNEXT® series introduces bio-based cationic emulsifiers derived from fermentation processes, addressing demand for sustainable personal care formulations. Its China Technology Center enables localized development of surfactants for 5G and EV battery applications. Wacker’s focus on biomethanol-based silicones supports compliance with EU green chemistry mandates. Achieving a Gold EcoVadis rating enhances its positioning in ESG-driven procurement markets. This strategy reinforces Wacker’s leadership in bio-based and high-purity silicone surfactants.

Elkem advances circular silicone surfactants with bio-based PURESIL™ ORG and recycling innovation

Elkem Silicones is focusing on circular silicone surfactant solutions while restructuring its portfolio through divestment to Bluestar. Its PURESIL™ ORG series features bio-based surfactants using sunflower-derived carriers, targeting biodegradable personal care applications. The company achieved over 50% recycling rates in HCR and silicone fluid systems, supporting a closed-loop silicone economy. With operating income of NOK 31 billion and a CDP “A” sustainability rating, Elkem maintains strong ESG credentials. Its innovations align with regulatory pressure on cyclic siloxanes and demand for low-impact materials. This positions Elkem as a pioneer in sustainable and circular silicone surfactant technologies.

Germany Silicone Surfactants Market Anchored by Circular Chemistry and REACH-Ready Reformulation

Germany’s silicone surfactants market is being reshaped by a convergence of decarbonized manufacturing, structural portfolio realignment, and regulatory-driven reformulation. In May 2025, Evonik Industries AG completed the conversion of its global Comfort and Insulation production platform to green electricity. This transition directly affects silicone surfactants used in polyurethane foams, reinforcing Germany’s position as a low-carbon sourcing hub for construction and insulation additives while supporting Evonik’s Scope 1 and 2 emissions reduction targets through 2030.

Strategically, Evonik’s Smart Effects initiative, effective January 2025, merged its Silica and Silanes business lines to create integrated surfactant-filler systems. This realignment is improving formulation efficiency in eco-friendly paints and high-performance tire compounds by enabling optimized wetting, dispersion, and filler compatibility within a single additive architecture. Regulatory pressure has further accelerated innovation. German manufacturers have finalized reformulation of consumer-facing silicone surfactants to comply with the June 2026 EU REACH limits on D4, D5, and D6 siloxanes below 0.1%. At CPHI Frankfurt, industry leaders showcased polyglyceryl-modified silicone surfactants derived from renewable corn feedstocks, offering high emulsification efficiency without compromising biodegradability profiles. Complementing product innovation, the German Chemical Industry Association reported €1.2 billion in collective 2025 investments into circular-ready production lines designed to recover silicone surfactants from industrial waste streams, reinforcing Germany’s leadership in circular chemical infrastructure.

United States Silicone Surfactants Market Driven by Decarbonization Platforms and Federal Policy Alignment

The United States silicone surfactants market is increasingly defined by policy-aligned demand and domestically integrated supply chains. In mid-2025, Dow introduced the Decarbia™ reduced-carbon platform, unveiling the industry’s first carbon-neutral silicone surfactants and elastomer blends produced through decarbonized silicon metal feedstocks. These launches position silicone surfactants as preferred PFAS-free wetting and leveling agents across coatings, elastomers, and construction materials, particularly as federal procurement standards tighten.

Energy efficiency mandates under the Infrastructure Investment and Jobs Act have further stimulated demand. Dow expanded its VORASURF™ silicone surfactants portfolio in 2025 to support rigid polyurethane spray foams used in high-performance building insulation, where cell structure control and thermal efficiency are critical. In parallel, the CHIPS Act has driven the establishment of on-site ultra-high-purity surfactant delivery hubs in Arizona and Ohio, supporting precision wetting requirements in advanced semiconductor lithography. Regulatory momentum is also influencing formulation choices. The EPA’s 2025 PFAS updates have accelerated substitution toward silicone-polyether surfactants in industrial coatings, while expanded tariffs on imported silicone intermediates in early 2025 have reinforced the strategic value of domestic precursor integration across the U.S. silicone surfactants value chain.

China Silicone Surfactants Market Accelerated by Regulatory Tightening and Localized Innovation

China’s silicone surfactants market is undergoing rapid transformation as food safety regulation, environmental taxation, and domestic innovation converge. In September 2025, the National Health Commission issued GB 4806.16-2025, a mandatory standard governing food-contact silicone materials. Effective from September 2026, the regulation introduces strict limits on volatile substances in silicone surfactants used in food-grade packaging, compelling reformulation and accelerating adoption of low-volatility chemistries.

At the same time, China is emerging as a localized innovation hub. In November 2025, Evonik Industries AG partnered with HosenCare to launch the Jinjiang Houxin innovation fund, targeting commercialization of sustainable silicone surfactants for beauty and home care applications. During PCHi 2025 in Guangzhou, market leaders introduced dermosoft® EcoLact C MB, the first anti-dandruff silicone surfactant blend developed and produced locally to address region-specific scalp-care requirements. Environmental enforcement is further reshaping demand. Revisions to China’s Environmental Protection Tax Law in late 2025 introduced a pilot tax on high-VOC additives, triggering a reported 40% year-on-year increase in adoption of water-borne silicone surfactant emulsions across coatings and home care formulations.

Japan Silicone Surfactants Market Defined by High-Purity Standards and E-Mobility Integration

Japan’s silicone surfactants market is characterized by extreme purity requirements and application-specific specialization, particularly in e-mobility and precision personal care. In January 2025, Wacker Asahikasei Silicone inaugurated a new facility in Tsukuba focused on specialty silicone surfactants and thermal interface materials used as heat-dissipating gap fillers in 800V electric vehicle traction batteries. This investment highlights Japan’s leadership in high-reliability materials for next-generation power electronics.

Japanese manufacturers continue to set global benchmarks for ionic cleanliness. Shin-Etsu Chemical has achieved breakdown voltages exceeding 650V on specialized substrates by deploying ultra-low-ionic silicone surfactants that minimize electrical leakage in power modules. In personal care, Japanese technical centers are advancing sugar-modified silicone surfactants that enable self-emulsifying oils, combining silicone sensory performance with biodegradability aligned to domestic eco-labeling standards. Policy support under the 2025 Critical Mineral and Material Security Act has designated silicone precursors as strategic assets, unlocking R&D grants for tin-free curing surfactants and reinforcing Japan’s long-term materials security strategy.

Comparative Snapshot: Country-Level Silicone Surfactants Dynamics

Silicone Surfactants Market County Level Snapshot

|

Country

|

Primary Demand Drivers

|

Strategic Focus Areas

|

Regulatory and Policy Influence

|

|

Germany

|

PU foams, coatings, tires

|

Circular-ready production, bio-based surfactants

|

EU REACH siloxane limits

|

|

United States

|

Building insulation, semiconductors, coatings

|

Carbon-neutral platforms, domestic integration

|

IIJA, CHIPS Act, PFAS updates

|

|

China

|

Food packaging, beauty, home care

|

Localized R&D, water-borne emulsions

|

GB 4806.16-2025, VOC taxation

|

|

Japan

|

EV batteries, power modules, personal care

|

Ultra-low-ionic purity, sugar-modified surfactants

|

Critical materials security act

|

Silicone Surfactants Market Report Scope

Silicone Surfactants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.6 Billion

|

|

Market Size (2034)

|

$5.5 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Silicone Polyethers, Silicone Alkyl Quats, Silicone Betaines, Silicone Sulfates & Carboxylates, Modified Silicone Surfactants), By Application (Emulsifiers, Foaming & Stabilizing Agents, Defoamers & Antifoaming Agents, Wetting & Spreading Agents, Dispersants & Solubilizers, Lubricating & Softening Agents), By End-Use Industry (Personal Care & Cosmetics, Polyurethane Foams, Paints, Inks & Coatings, Agriculture, Textile & Leather, Industrial & Home Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Evonik Industries AG, Wacker Chemie AG, Momentive Performance Materials Inc., Shin-Etsu Chemical Co. Ltd., Elkem ASA, Siltech Corporation, Gelest Inc., Innospec Inc., Zhejiang Xanan Chemical Industrial Group, Kaneka Corporation, CHT Group, Hoshine Silicon Industry Co. Ltd., Nusil Technology, Hubei BlueSky New Material Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicone Surfactants Market Segmentation

By Product Type

- Silicone Polyethers

- Silicone Alkyl Quats

- Silicone Betaines

- Silicone Sulfates & Carboxylates

- Modified Silicone Surfactants

By Application

- Emulsifiers

- Foaming & Stabilizing Agents

- Defoamers & Antifoaming Agents

- Wetting & Spreading Agents

- Dispersants & Solubilizers

- Lubricating & Softening Agents

By End-Use Industry

- Personal Care & Cosmetics

- Polyurethane Foams

- Paints, Inks & Coatings

- Agriculture

- Textile & Leather

- Industrial & Home Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Surfactants Industry

- Dow Inc.

- Evonik Industries AG

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co. Ltd.

- Elkem ASA

- Siltech Corporation

- Gelest Inc.

- Innospec Inc.

- Zhejiang Xinan Chemical Industrial Group

- Kaneka Corporation

- CHT Group

- Hoshine Silicon Industry Co. Ltd.

- Nusil Technology

- Hubei BlueSky New Material Inc.

*- List not Exhaustive