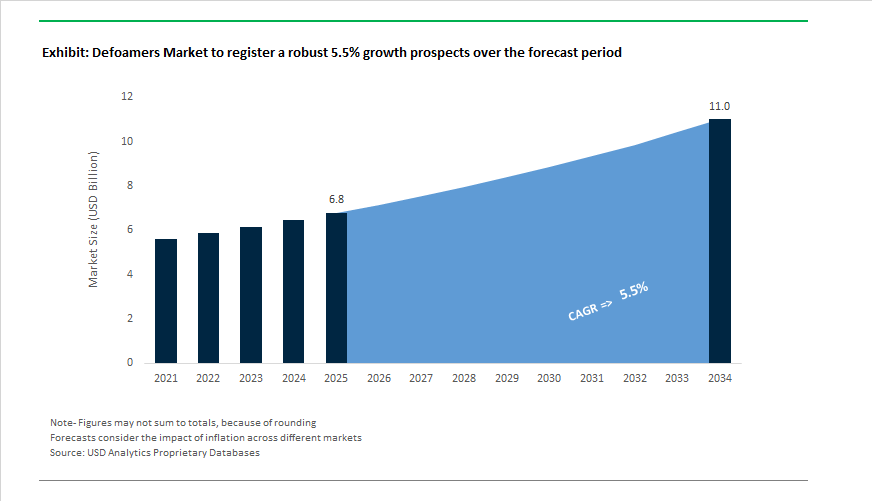

Defoamers Market to Reach $11 Billion by 2034 at 5.5% CAGR Amid Sustainable Silicone Innovation and Water Infrastructure Investment

The Defoamers Market is projected to expand from $6.8 billion in 2025 to $11 billion by 2034, registering a CAGR of 5.5%. Growth is being driven by rising demand for high-efficiency antifoaming agents in waterborne coatings, printing inks, pulp and paper processing, wastewater treatment, and industrial fermentation systems. The structural transition from solvent-based to waterborne formulations in architectural paints and industrial coatings has intensified the need for advanced silicone defoamers capable of controlling microfoam without compromising surface finish, gloss, or film integrity. At the same time, regulatory pressure on VOCs, SVOCs, and mineral oil derivatives is accelerating innovation in bio-based and low-emission defoaming technologies across global specialty chemical portfolios.

Sustainability-focused product launches gained momentum in April 2024, when Evonik introduced TEGO® Foamex 16, a 25% bio-based concentrate, and TEGO® Foamex 11, a siloxane-based emulsion engineered with near-zero VOC and SVOC levels. These launches at the American Coatings Show positioned Evonik strongly within the green additives segment for waterborne paints and inks. In March 2025, Evonik further strengthened its silicone defoamer leadership with TEGO® Foamex 8420, specifically designed for waterborne overprint varnishes and high-speed printing inks, offering strong foam knockdown performance without surface defects. In June 2025, the company introduced TEGO® Foamex 8051 for decorative coatings, emphasizing global regulatory compliance and ultra-low emissions, reinforcing the shift toward environmentally aligned defoaming solutions. Parallel portfolio expansion was visible in 2024, when Munzing Chemie broadened its plant-oil-based DEE FO® range targeting food-contact packaging and paper applications, addressing tightening EU and FDA restrictions on mineral oil-based additives. Capacity expansions also reshaped supply dynamics. BASF completed an expansion of its Foamaster® and Foamstar® defoamer production lines at Dilovasi, Turkey during 2024–2025, strengthening supply to architectural coatings and construction sectors across EMEA. BASF further reinforced its India footprint in February 2026 by adding a new dispersions production line in Mangalore, enhancing local supply of paint additives including defoamers for high-growth South Asian markets.

Strategic acquisitions and macro-level policy initiatives are influencing volume consumption patterns. In February 2025, PennWhite India acquired Sicagen’s defoamer business, expanding its penetration in pulp, paper, and industrial water treatment applications across South Asia. In the U.S., the Environmental Protection Agency confirmed a $6.2 billion allocation for Fiscal Year 2025 water infrastructure upgrades in October 2024, supporting sustained demand for wastewater defoamers used in aeration basins and sludge management systems. Ecolab strengthened its presence in high-purity industrial water systems by completing the acquisition of Ovivo’s Electronics Ultrapure Water business in December 2025, integrating specialized chemical management services that include defoamer applications for semiconductor and high-tech facilities. Corporate restructuring is also shaping competitive positioning. Dow launched its Transform to Outperform initiative in January 2026, targeting a $2 billion EBITDA improvement by streamlining performance materials segments that produce silicone-based defoaming agents. Wacker Chemie initiated a €300 million annual cost reduction program in January 2026, prioritizing high-value WACKER SILICONES specialties, including advanced silicone defoamers tailored for EV battery manufacturing and renewable energy materials processing. These structural shifts, combined with regulatory-driven reformulation and infrastructure spending, are redefining the technological and geographic contours of the global defoamers market.

Trends and Opportunities in the Global Defoamers Market

High-Efficiency Silicone–Polyether Hybrids for Low-Dosage Foam Suppression

Modern industrial formulations are accelerating the adoption of advanced silicone-based defoamers that deliver rapid foam knockdown without inducing surface defects. By late 2025, next-generation polydimethylsiloxane and silicone–polyether hybrid defoamers were demonstrating effective foam suppression at concentrations as low as 0.05 to 0.1%. Technical performance data released in December 2025 showed that these hybrids achieved up to a 95% defoaming rate within 51 seconds in aggressive surfactant systems. This represents a substantial improvement over conventional polyether defoamers, which typically require close to 90 seconds to achieve only around 70% foam reduction.

Surface integrity has become a decisive performance metric, particularly in high-gloss and defect-sensitive applications. In automotive and industrial coatings, which accounted for roughly 27.8% of defoamer demand in 2024, manufacturers are increasingly specifying silicone MQ resin-based defoamers. These materials provide superior thermal and chemical stability under high-shear mixing, enabling uniform film formation without fish-eyes, craters, or haze. As coating systems move toward higher solids and tighter appearance tolerances, silicone–polyether hybrids are emerging as the preferred solution for premium finishes.

Rapid Scale-Up of Bio-Based and Eco-Label Compliant Defoamers

Environmental regulation and customer sustainability requirements are accelerating the replacement of mineral-oil-based defoamers with bio-based and eco-label compliant alternatives. Certification frameworks such as the USDA BioPreferred program and the EU Ecolabel are pushing formulators toward vegetable-oil-derived esters and hybrid systems that balance biodegradability with performance. In 2024 and 2025, companies such as Evonik introduced hybrid defoamer emulsions containing more than 50% bio-based content in the non-aqueous phase. These mineral-oil-free formulations are designed to meet food-contact and packaging ink regulations while delivering consistent foam control in water-based systems.

Regulatory pressure intensified further in June 2024, when new European limitations on specific chemical stabilizers triggered widespread reformulation across water-intensive industries. As a result, vegetable-oil-based defoamers derived from rapeseed and sunflower oils are seeing accelerated uptake in pulp and paper processing, municipal wastewater treatment, and industrial effluent management. Their lower aquatic toxicity and improved biodegradability profiles are aligning foam control strategies with environmental compliance and corporate ESG targets, making bio-based defoamers a structural growth segment rather than a niche alternative.

Specialized Defoamers for Lithium-Ion Battery Slurry Processing

The rapid expansion of lithium-ion battery manufacturing is creating a high-margin opportunity for defoamers engineered specifically for electrode slurry applications. In thick-film electrode coating, entrapped air bubbles can cause pinholes and coating non-uniformity, directly degrading battery capacity, cycle life, and safety. Research published in October 2025 emphasized that defoamers used in battery slurries must be electrochemically inert, ensuring they do not interfere with ionic conductivity or compromise adhesion between active materials and current collectors.

As battery producers adopt high-shear mixing and move toward three-dimensional foam-type current collectors to enhance ion transport, defoamers must also maintain rheological stability under extreme processing conditions. This requirement is driving demand for specialized, non-reactive silicone defoamers capable of preventing sagging or slumping during drying while remaining fully compatible with advanced cathode and anode chemistries. These performance constraints position battery-grade defoamers as a premium sub-segment within the broader market.

Precision Defoaming Solutions for Biomanufacturing and Fermentation

Biomanufacturing and precision fermentation are emerging as one of the fastest-growing opportunity areas for defoamers. By 2025, approximately 40% of global fermentation defoamer demand was attributable to the biopharmaceutical sector, where foam control is critical for maintaining oxygen transfer and preventing bioreactor overflow. In the production of monoclonal antibodies, vaccines, and cell-based therapies, foam-related process disruptions can result in the loss of batches valued in the millions of dollars, elevating defoamers to a risk-mitigation input rather than a cost item.

Food and beverage fermentation is reinforcing this demand. The biological fermentation defoamer market is projected to reach around USD 2.5 billion by 2035, supported by global beer production exceeding 1.9 billion hectoliters and probiotic sales surpassing USD 60 billion. In these applications, clean-label expectations and regulatory scrutiny favor non-toxic, easily removable silicone-based defoamers that do not inhibit microbial growth or contaminate downstream products. As fermentation scales across alternative proteins and bio-based chemicals, precision defoaming is becoming a core enabler of yield, consistency, and regulatory compliance.

Defoamers Market Share and Segmentation Insights

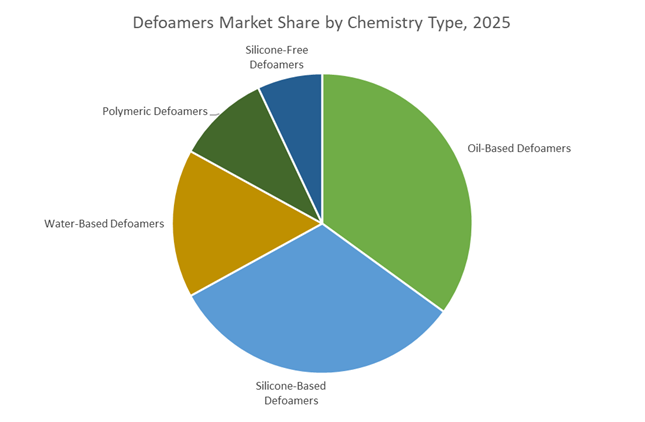

Defoamers Market Share by Chemistry Type : Oil-Based Formulations Lead as Silicone and Water-Based Systems Gain Strategic Ground

Oil-based defoamers account for 35% of global demand in 2025, positioning them as the dominant chemistry due to their cost efficiency and broad usability across pulp and paper, wastewater treatment, and agrochemical manufacturing. Mineral oil and vegetable oil systems blended with hydrophobic silica remain the industry workhorses for large-volume industrial foam control. Silicone-based defoamers represent a high-performance segment, valued for superior foam knockdown at low dosage in textiles, coatings, and high-temperature processing environments, justifying premium pricing. Water-based defoamers are gaining momentum in food processing, beverage production, and waterborne coatings, driven by sustainability mandates and product purity requirements. Polymeric defoamers continue expanding in printing inks, electronic chemicals, and premium paints where formulation compatibility and surface perfection are critical. Silicone-free defoamers serve regulated niches such as automotive paint lines, electronics manufacturing, and select food-contact applications, where silicone contamination risks adhesion failure and surface cratering.

Defoamers Market Share by Application: Water Treatment Dominates as Coatings and Food Processing Accelerate Adoption

Water and wastewater treatment leads the defoamers market with 22% share, fueled by persistent foam generation in aeration tanks and biological treatment systems, where continuous defoamer dosing is essential to meet discharge regulations and operational efficiency targets. Industrial process chemicals form a major secondary segment, spanning chemical manufacturing, fermentation, and mineral processing, where foam control directly impacts reactor safety and production throughput. Pulp and paper remains a core consumer, relying on defoamers across pulping, paper machines, and effluent streams to protect sheet quality and machine speed. Coatings, inks, and adhesives represent a fast-growing application, as waterborne formulations inherently generate foam, increasing demand for high-performance defoaming additives to prevent surface defects. Food and beverage processing requires FDA-approved, food-grade defoamers for sugar refining, fermentation, and produce washing, while oil and gas, cleaning products, and agrochemicals collectively drive steady demand under harsh operating and formulation conditions.

Competitive Landscape of the Defoamers Market

The Defoamers Market is characterized by strong consolidation among multinational chemical leaders, with competition centered on silicone-based antifoams, zero-VOC defoamers, digital dosing systems, and high-performance formulations for coatings, wastewater treatment, pulp & paper, and food processing. Innovation is increasingly driven by sustainability compliance, automated foam control, and precision chemistry for advanced manufacturing environments.

Evonik drives next-generation defoamers for coatings, inks, and semiconductor manufacturing

Evonik Industries AG leads the specialty defoamers segment through its TEGO® portfolio, maintaining dominance in high-performance coatings and printing inks. In March 2025, Evonik launched TEGO® Foamex 8420, a siloxane-based defoamer engineered for waterborne overprint varnishes containing high surfactant loads. Under its “Digital and Sustainable Coatings” strategy, the company expanded TEGO® Foamex 16 and 11 series to deliver ultra-low-VOC architectural coatings with long-lasting foam suppression at minimal dosage. In early 2026, Evonik introduced precision defoaming agents for semiconductor wafer fabrication, strengthening its electronics value-chain integration. Evonik holds a leading position in Paints, Coatings & Inks, the second-largest global defoamers application segment.

BASF scales Foamaster and Foamstar capacity to meet EMEA industrial demand

BASF SE remains a cost and volume leader, leveraging its Verbund production model to ensure feedstock security and stable pricing amid 2025–2026 chemical supply volatility. The company doubled Foamaster® and Foamstar® defoamer capacity at its Dilovasi, Türkiye facility in late 2024/early 2025, targeting accelerating demand across EMEA. BASF maintains its strongest presence in pulp & paper and industrial cleaning, where polymeric defoamers optimize high-speed production lines. Strategically, BASF is transitioning toward Zero-VOC defoamer benchmarks to align with 2026 European Green Deal regulations. Its backward-integrated raw material platform continues to provide competitive resilience in emerging Middle Eastern and African markets.

Dow advances silicone antifoams with smart dosing and AI-driven productivity

Dow Inc. dominates the silicone-based defoamers segment, which represents approximately 36%–40% of global market share, driven by applications in oil & gas and wastewater treatment. Its silicone antifoams are critical for drilling fluid stability and high-volume aeration systems. In January 2026, Dow launched the “Transform to Outperform” initiative, targeting $2 billion in EBITDA uplift through AI-enabled productivity improvements across Performance Materials & Coatings. Dow is also advancing “Smart Dosing” compatibility, optimizing silicone emulsions for integration with inline foam sensors to reduce chemical overuse. This digitalized approach positions Dow as a key enabler of automated, data-driven foam control systems.

Wacker pivots to high-barrier silicone defoamers amid raw material inflation

Wacker Chemie AG is reinforcing its position in premium silicone defoamers through a strategic shift toward low-substitutability applications. In February 2026, Wacker implemented a minimum 25% price increase across core silicone lines to offset a 110% rise in platinum catalyst costs. The company is moving away from commodity defoamers, focusing instead on medical devices, automotive electronics sealing, and extreme pH environments. Its high-purity silicone resins and specialty silanes deliver reliable foam suppression under highly acidic or alkaline conditions. Wacker’s technical leadership in crosslinking silicone formulations makes it the default supplier for mission-critical industrial processes.

Solenis integrates defoamers with real-time monitoring across water and food processing

Solenis has evolved into an all-in-one process improvement platform following its mergers with Diversey and NCH. The company uniquely combines defoamer chemistry with OnGuard™ monitoring systems, enabling pulp mills and municipal plants to automate foam control in real time. Solenis is expanding production to serve the pulp & paper segment, which represents roughly 25% of global defoamer demand. It also leads in food and beverage processing, particularly dairy and brewing, supplying clean-label compliant defoamers aligned with 2026 safety expectations. With a vast global service footprint, Solenis delivers localized technical support across high-growth regions such as Brazil and Southeast Asia.

Shin-Etsu dominates Asia-Pacific with high-stability silicone defoamer emulsions

Shin-Etsu Chemical commands a leading share of the Asia-Pacific defoamers market, a region accounting for approximately 39% of global revenue in 2026. Its KM and KS silicone defoamer series are supplied in oil, emulsion, and powder formats to meet diverse industrial needs. Shin-Etsu holds strong positions in China and Japan, supported by rising wastewater treatment and infrastructure construction activity. The company is expanding its Functional Materials division to capture the 5.9% CAGR APAC growth, emphasizing high-stability emulsions for textile dyeing. Its core strength lies in emulsion engineering that prevents spotting and surface defects in premium paper and textile finishes.

China: Smart Manufacturing as the Core Growth Lever

China’s defoamers market in 2025 is being reshaped by state-led digitalization and environmental compliance, positioning process efficiency as a decisive competitive variable. Under the Phase 2 rollout of the Made in China 2025 framework, chemical producers have embedded AI-driven sensors and machine learning models directly into production lines to detect micro-variations that trigger foam formation. This shift has materially reduced batch failures in coatings, pulp processing, and industrial water treatment, elevating defoamers from auxiliary additives to process-critical inputs.

Capacity expansion is increasingly clustered in advanced chemical parks. The Nanjing Jiangbei New Material Technology Park commissioned new high-performance dispersant and defoamer lines in 2025, leveraging Controlled Free Radical Polymerization technology to enhance molecular stability under high shear conditions. Parallel regulatory pressure on VOC reduction has accelerated reformulation, with nearly 70% of newly commissioned defoamer capacity now aligned to water-borne and high-solids systems. Chinese R&D centers also introduced nano-silica reinforced defoamers in Q4 2025, improving surface finish in automotive and architectural coatings. Looking ahead, the 2026 industrial roadmap links local official performance metrics to adoption of smart additives that respond dynamically to pH and temperature shifts, while raw material strategies in Jiangsu and Zhejiang increasingly prioritize domestic sourcing of siloxanes to de-risk global supply chains.

India: Policy-Backed Localization and Export-Oriented Scale-Up

India’s defoamers industry is transitioning from import substitution to export ambition, supported by coordinated industrial policy. In July 2025, the NITI Aayog Chemical Hub initiative outlined a framework for world-class clusters with shared utilities, logistics, and effluent treatment infrastructure, directly benefiting specialty additive producers. This was reinforced by the introduction of a 2025 Operating Expenditure subsidy scheme that incentivizes incremental domestic output of specialty chemicals, including defoamers used in pulp, textiles, and coatings.

Structural competitiveness is also being enhanced through infrastructure and R&D funding. Under the PM Gatishakti master plan, eight port-adjacent chemical clusters are scheduled for development in 2026, creating cost-efficient export gateways for defoamers targeting global pulp and paper customers. The Department of Chemicals and Petrochemicals increased R&D disbursements by ₹3.75 crore in FY 2024–25, prioritizing green chemistry and high-purity formulations. Feedstock security is improving as well, with the Ministry of Chemicals and Fertilizers confirming a strategic shift in benzene allocation toward downstream derivatives such as cyclohexane and cumene, stabilizing supply for polyether- and silicone-based defoamer production.

United States: Climate Regulation Driving Technology Substitution

In the United States, the defoamers market is being decisively shaped by climate policy and downstream industrial demand. Effective January 1, 2025, the EPA’s AIM Act imposed a Global Warming Potential cap of 150 on multiple aerosol and foam subsectors, triggering rapid reformulation toward low-GWP defoamer technologies. This regulatory pressure intensified further in October 2025, when finalized 2026 HFC allowance allocations accelerated the phase-down of conventional blowing agents and associated stabilizers used in rigid polyurethane foams.

Demand fundamentals remain strong in resource-intensive industries. U.S. pulp exports are projected to reach record levels by 2026, driving robust consumption of non-silicone brown stock defoamers across high-capacity mills in the Southeast. On the supply side, Evonik completed a 50% expansion of precipitated silica capacity at its Charleston, South Carolina site during late 2024 and early 2025, strengthening domestic availability of critical inputs for powder and emulsion defoamers. As a result, the U.S. market is consolidating around compliant, low-emission formulations rather than commodity-grade products.

Germany: Bio-Based Chemistry and Certification-Led Differentiation

Germany’s defoamers landscape is defined by innovation funding, certification, and sustainability-led product differentiation. The Circular Bio-based Europe Joint Undertaking announced a €170.7 million work program for 2026, with explicit support for bio-based additives that improve recyclability in coatings and packaging. This funding environment has accelerated applied research, exemplified by the Fraunhofer Institute’s October 2025 unveiling of Caramide, a fully bio-based polyamide derived from wood-processing by-products and now under evaluation as a stabilizer in industrial defoamer emulsions.

Commercial portfolios are rapidly aligning with certification frameworks. Major producers such as Wacker Chemie and BASF transitioned core defoamer ranges to ISCC PLUS mass-balance feedstocks in late 2025, directly supporting EU 2030 decarbonization targets. At the application level, Evonik introduced TEGO Foamex 8880, engineered to meet the most stringent European eco-label criteria for architectural coatings. In Germany, regulatory credibility and bio-based content increasingly determine supplier selection.

Brazil: Pulp-Led Volume Growth and Localized Manufacturing

Brazil’s defoamers market is tightly coupled with the expansion of its pulp and agribusiness sectors. In April 2024, Kemira entered an exclusive distribution partnership with BIM Kemi, securing a strong foothold in Brazil’s pulp industry through 2025–2026. With national pulp exports forecast to exceed 19.2 million metric tons by 2026, demand is surging for fatty-acid-based defoamers that enhance recovery boiler efficiency and reduce fiber losses.

Secondary demand drivers are emerging from packaging. The reopening of major export markets for Brazilian animal protein in late 2025 has supported a rebound in corrugated box production, lifting defoamer consumption in starch-based adhesive systems. To manage logistics costs and ensure supply reliability, Brazilian producers are increasingly localizing defoamer manufacturing close to pulp mills, reinforcing Brazil’s role as a high-volume, application-driven market.

Comparative Snapshot: Defoamers Market by Country

Defoamers Market County Level Snapshot

Country

Primary Growth Driver

Strategic Focus Area

Market Direction

China

Smart manufacturing and VOC mandates

AI-enabled, water-based defoamers

Technology-led scale-up

India

Policy incentives and export hubs

Localization and green R&D

Import substitution to export

United States

Climate regulation and pulp demand

Low-GWP reformulation

Compliance-driven innovation

Germany

Bio-based funding and certification

ISCC PLUS and eco-label products

Sustainability-led differentiation

Brazil

Pulp and packaging expansion

Fatty-acid-based local production

Volume-driven growth

Defoamers Market Report Scope

Defoamers Market

Parameter

Details

Market Size (2025)

$6.8 Billion

Market Size (2034)

$11 Billion

Market Growth Rate

5.5%

Segments

By Chemistry Type (Silicone-Based Defoamers, Oil-Based Defoamers, Water-Based Defoamers, Polymeric Defoamers, Silicone-Free Defoamers), By Delivery Form (Liquid Defoamers, Emulsion and Dispersion Defoamers, Powder and Solid Defoamers, Concentrated Defoamers), By Application (Industrial Process Chemicals, Coatings, Inks and Adhesives, Water and Wastewater Treatment, Pulp and Paper, Food and Beverage Processing, Oil and Gas, Agrochemicals, Cleaning and Detergents)

Study Period

2019- 2025 and 2026-2034

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

BASF SE, Evonik Industries AG, Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Kemira Oyj, Elementis PLC, Clariant AG, Air Products and Chemicals, Inc., Momentive Performance Materials Inc., San Nopco Limited, BIM Kemi AB, Ashland Inc., Buckman Laboratories International, Inc., Haldia Petrochemicals Limited

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Defoamers Market Segmentation

By Chemistry Type

Silicone-Based Defoamers

Oil-Based Defoamers

Water-Based Defoamers

Polymeric Defoamers

Silicone-Free Defoamers

By Delivery Form

Liquid Defoamers

Emulsion and Dispersion Defoamers

Powder and Solid Defoamers

Concentrated Defoamers

By Application

Industrial Process Chemicals

Coatings, Inks and Adhesives

Water and Wastewater Treatment

Pulp and Paper

Food and Beverage Processing

Oil and Gas

Agrochemicals

Cleaning and Detergents

By Region

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

2. Defoamers Market Landscape & Outlook (2026–2034)

2.1. Introduction to Defoamers Market

2.2. Market Valuation and Growth Projections (2026–2034)

2.3. Transition to Waterborne Systems and Low-VOC Reformulation

2.4. Infrastructure Investment, Water Treatment Expansion, and Industrial Fermentation Demand

2.5. Sustainable Silicone Innovation, Bio-Based Alternatives, and Regulatory Compliance

3. Innovations Reshaping the Defoamers Market

3.1. Trend: High-Efficiency Silicone–Polyether Hybrids for Low-Dosage Foam Suppression

3.2. Trend: Rapid Scale-Up of Bio-Based and Eco-Label Compliant Defoamers

3.3. Opportunity: Specialized Defoamers for Lithium-Ion Battery Slurry Processing

3.4. Opportunity: Precision Defoaming Solutions for Biomanufacturing and Fermentation

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Defoamers Market

5.1. By Chemistry Type

5.1.1. Silicone-Based Defoamers

5.1.2. Oil-Based Defoamers

5.1.3. Water-Based Defoamers

5.1.4. Polymeric Defoamers

5.1.5. Silicone-Free Defoamers

5.2. By Delivery Form

5.2.1. Liquid Defoamers

5.2.2. Emulsion and Dispersion Defoamers

5.2.3. Powder and Solid Defoamers

5.2.4. Concentrated Defoamers

5.3. By Application

5.3.1. Industrial Process Chemicals

5.3.2. Coatings, Inks and Adhesives

5.3.3. Water and Wastewater Treatment

5.3.4. Pulp and Paper

5.3.5. Food and Beverage Processing

5.3.6. Oil and Gas

5.3.7. Agrochemicals

5.3.8. Cleaning and Detergents

5.4. By Region

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. South and Central America

5.4.5. Middle East and Africa

6. Country Analysis and Outlook of Defoamers Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Defoamers Market Size Outlook by Region (2026–2034)

7.1. North America Defoamers Market Size Outlook to 2034

7.1.1. By Chemistry Type

7.1.2. By Delivery Form

7.1.3. By Application

7.1.4. By Region

7.2. Europe Defoamers Market Size Outlook to 2034

7.2.1. By Chemistry Type

7.2.2. By Delivery Form

7.2.3. By Application

7.2.4. By Region

7.3. Asia Pacific Defoamers Market Size Outlook to 2034

7.3.1. By Chemistry Type

7.3.2. By Delivery Form

7.3.3. By Application

7.3.4. By Region

7.4. South America Defoamers Market Size Outlook to 2034

7.4.1. By Chemistry Type

7.4.2. By Delivery Form

7.4.3. By Application

7.4.4. By Region

7.5. Middle East and Africa Defoamers Market Size Outlook to 2034

7.5.1. By Chemistry Type

7.5.2. By Delivery Form

7.5.3. By Application

7.5.4. By Region

8. Company Profiles: Leading Players in the Defoamers Market

8.1. BASF SE

8.2. Evonik Industries AG

8.3. Dow Inc.

8.4. Wacker Chemie AG

8.5. Shin-Etsu Chemical Co., Ltd.

8.6. Kemira Oyj

8.7. Elementis PLC

8.8. Clariant AG

8.9. Air Products and Chemicals, Inc.

8.10. Momentive Performance Materials Inc.

8.11. San Nopco Limited

8.12. BIM Kemi AB

8.13. Ashland Inc.

8.14. Buckman Laboratories International, Inc.

8.15. Haldia Petrochemicals Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Defoamers Market Segmentation

By Chemistry Type

Silicone-Based Defoamers

Oil-Based Defoamers

Water-Based Defoamers

Polymeric Defoamers

Silicone-Free Defoamers

By Delivery Form

Liquid Defoamers

Emulsion and Dispersion Defoamers

Powder and Solid Defoamers

Concentrated Defoamers

By Application

Industrial Process Chemicals

Coatings, Inks and Adhesives

Water and Wastewater Treatment

Pulp and Paper

Food and Beverage Processing

Oil and Gas

Agrochemicals

Cleaning and Detergents

By Region

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

The Defoamers Market is valued at $6.8 billion in 2025 and is forecast to reach $11 billion by 2034, expanding at a CAGR of 5.5%. Growth is underpinned by structural demand in waterborne coatings, wastewater treatment, pulp and paper, and fermentation. Regulatory reformulation toward low-VOC and bio-based systems is accelerating premium product adoption.

Water and wastewater treatment leads with roughly 22% market share, supported by global infrastructure upgrades and stricter discharge norms. Coatings, inks, and adhesives are rapidly expanding due to the shift toward waterborne formulations that inherently generate foam. Pulp and paper remains a high-volume segment, while lithium-ion battery slurry processing is emerging as a high-margin specialty niche.

Restrictions on mineral oil derivatives, VOCs, and SVOCs are pushing manufacturers toward silicone–polyether hybrids and vegetable-oil-based defoamers. Certifications such as USDA BioPreferred and EU Ecolabel are influencing procurement decisions in food, packaging, and municipal applications. Bio-based emulsions exceeding 50% renewable content are moving from niche to mainstream adoption.

Asia Pacific accounts for the largest revenue share, led by China’s smart manufacturing upgrades and India’s policy-backed specialty chemical clusters. The United States is driven by climate regulations and pulp export strength, while Germany emphasizes ISCC PLUS mass-balance compliance. Brazil remains a volume-driven market tied to pulp expansion and localized manufacturing near mills.

Key players include BASF SE, Evonik Industries AG, Dow Inc., Wacker Chemie AG, and Shin-Etsu Chemical Co., Ltd.. These firms compete through silicone-based high-efficiency antifoams, zero-VOC formulations, capacity expansions in EMEA and Asia, and digitalized smart-dosing platforms for industrial process optimization.