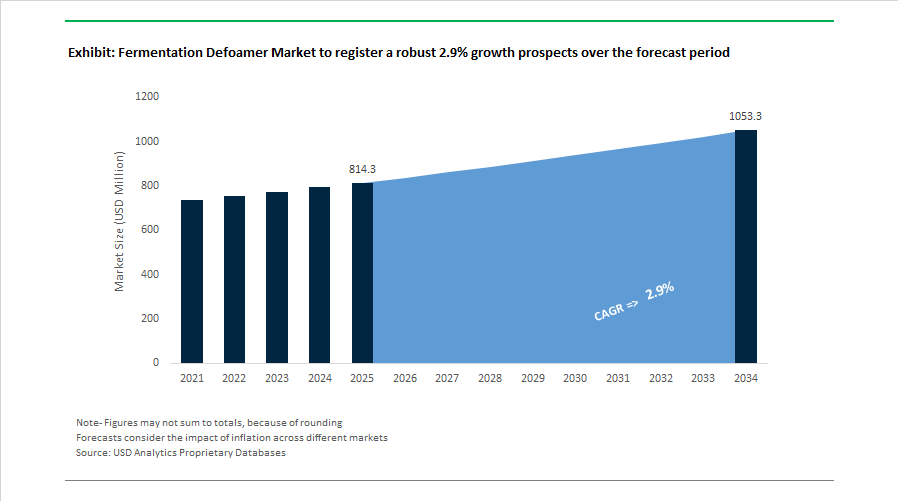

Fermentation Defoamer Market Size 2025–2034: $814.3 Million to $1,053.2 Million at 2.9% CAGR Anchored in Industrial Bioprocess Optimization

The Fermentation Defoamer Market is projected to increase from $814.3 Million in 2025 to $1,053.2 Million by 2034, registering a CAGR of 2.9%. Market expansion reflects structural growth in large-scale industrial fermentation across biofuels, pharmaceuticals, food processing, dairy cultures, wastewater bio-treatment, and specialty enzymes. Foam formation remains a critical bottleneck in aerobic and anaerobic bioreactors, where uncontrolled foaming reduces oxygen transfer efficiency, contaminates exhaust systems, and lowers fermentation yield. As global fermentation capacity scales toward continuous production models, demand for high-performance silicone-based defoamers, polyethersiloxane concentrates, and bio-based antifoam emulsions is increasing in parallel.

In June 2025, Evonik introduced TEGO® Foamex 8051, a 100% active polyethersiloxane defoamer characterized by a nearly zero VOC and SVOC profile, serving as a technology benchmark for low-toxicity foam control in beverage and dairy fermentation systems. In March 2025, Evonik expanded its compliant additive portfolio with TEGO® Foamex 8420, engineered for food-contact applications and increasingly referenced in fermentation-based food processing where clean-label and regulatory transparency are mandatory. In 2025, Shin-Etsu Chemical detailed expansion of its Green Silicone initiative, developing biodegradable silicone defoaming agents tailored for fermentation environments requiring high thermal stability without environmental trade-offs.

During 2024, structural consolidation and regulatory alignment reshaped the competitive landscape. In May 2024, Momentive Performance Materials was fully acquired by KCC Corporation, integrating advanced silicone defoamer technology with expanded Asian manufacturing capabilities targeting pharmaceutical fermentation. In March 2024, Solvay introduced wastewater-specific defoamers to address foam generated in large-scale biorefinery effluent streams, reinforcing the link between fermentation scale-up and downstream foam management. In late 2024, Huntsman restructured its defoamer R&D portfolio in response to evolving U.S. surfactant regulations, transitioning toward higher-purity chemical modifiers designed to maintain foam knockdown efficiency under stricter environmental compliance frameworks. In May 2024, Kemira launched bio-based defoamers for recyclable and biodegradable packaging production, reflecting increased scrutiny on additive compatibility across food fermentation and circular packaging ecosystems. Wacker Chemie AG reported 11% growth in its Biosolutions segment in 2024, allocating capital toward expanded production of pharmaceutical-grade silicone antifoam emulsions used in sterile bioreactors.

In January 2024, the formation of Novonesis through the merger of Novozymes and Chr. Hansen reshaped industrial fermentation supply chains, embedding foam control protocols into integrated biosolutions packages for enzyme and biofuel producers. In October 2023, Dow introduced a high-performance defoamer engineered for extreme pH and temperature variability in continuous industrial fermentation systems, targeting large biofuel and pulp-scale operations where process stability determines yield economics.

Trends and Opportunities in the Fermentation Defoamer Market

Shift Toward Non-Silicone and Bio-Renewable Formulations for Precision Fermentation

As precision fermentation scales for animal-free dairy proteins, enzymes, and specialty fragrances, the tolerance for silicone residues has sharply declined. Downstream purification losses, protein denaturation risks, and regulatory non-compliance have forced producers to transition away from conventional silicone-based defoamers toward food-safe, bio-renewable alternatives.

In early 2025, Evonik expanded its portfolio with TEGO® Foamex 8820 and 8850, silicone-free defoamer concentrates engineered to deliver performance comparable to siloxanes while exceeding 50% bio-renewable content. These products directly target fermentation systems producing recombinant proteins and enzymes, where even trace silicone carryover can disrupt membrane filtration and chromatography yields.

Clean-label expectations are reinforcing this shift. Industry data from December 2025 shows bio-based defoamers have recorded a 25% increase in adoption over the last five years, particularly in North America and Europe. Fermented sweeteners, alternative dairy proteins, and enzyme manufacturers increasingly specify vegetable oil-based and fatty acid ester defoamers to meet GRAS, EFSA, and global food-contact standards.

Biopharmaceutical fermentation is a dominant demand driver. By 2025, approximately 40% of fermentation defoamer consumption is linked to biopharma applications, including antibiotics and therapeutic proteins. In these processes, defoamer selection directly affects oxygen transfer rates, cell viability, and batch release outcomes. The economic risk of batch rejection has made low-toxicity, low-residue defoamers a non-negotiable requirement rather than a cost optimization lever.

Adoption of Automated, In-Line Foam Sensing and Precision Dosing Systems

The digitalization of bioprocessing is redefining how defoamers are applied. Manual, reactive dosing is being replaced by closed-loop, sensor-driven systems that respond in real time to foam formation, agitation changes, and aeration intensity.

At the POWTECH TECHNOPHARM 2025 exhibition in September, automation providers demonstrated integrated Manufacturing Execution Systems linking optical and conductivity-based foam sensors directly to precision dosing pumps. These systems dynamically modulate defoamer addition, preventing foam-over events that cause contamination while avoiding over-dosing that suppresses oxygen mass transfer and reduces volumetric productivity.

Peer-reviewed research published in Animal Feed Science and Technology in 2025 indicates that automated foam control can reduce defoamer consumption by 10% to 20% compared with manual dosing. This efficiency gain is particularly significant in large stirred-tank bioreactors exceeding 100 cubic meters, where aeration rates fluctuate continuously and defoamer misuse can materially impact yield economics.

The rise of Single-Use Systems in 2025 has further accelerated automation. Disposable bioreactors demand high reproducibility and minimal operator intervention. As a result, bioprocess developers are standardizing smart foam control modules as part of validated, zero-defect manufacturing strategies, especially in regulated cell culture and microbial fermentation environments.

Specialty Defoamers for High-Viscosity Biopolymers and Lignocellulosic Broths

The commercialization of high-value biopolymers and lignocellulosic platform chemicals is creating demand for defoamers that can function under extreme rheological conditions. Fermentations producing hyaluronic acid, bacterial cellulose, and advanced polysaccharides generate highly viscous, non-Newtonian broths where gas bubbles become trapped and conventional defoamers rapidly lose effectiveness.

In June 2025, Evonik introduced TEGO® Foamex 8051, a shear-stable defoamer engineered to maintain activity under prolonged high-shear and high-aeration conditions. Such products are critical in fermentations running beyond 72 hours, where mechanical degradation of defoamers historically led to escalating foam risk late in the cycle.

At an industrial scale, lignocellulosic fermentation is moving toward consolidated bioprocessing, where high solids loading and heterogeneous substrates intensify foam formation. Specialty defoamers capable of penetrating dense biomass matrices without inhibiting microbial metabolism represent a significant growth avenue, particularly as bio-based chemical production from agricultural residues transitions from pilot to commercial scale.

Enabling Non-Cytotoxic Foam Control for Cultivated Meat Scale-Up

Cultivated meat has entered a commercialization phase, shifting defoamer requirements from microbial robustness to extreme cytocompatibility. Animal cell cultures are far more sensitive to membrane disruption, making traditional defoamers unsuitable for large-scale cultivated protein bioreactors.

In February 2025, a collaboration between Stämm and SuperMeat highlighted the move toward continuous cultivated chicken production. Scaling to vessels above 10,000 liters requires foam control agents that do not compromise cell viability or interfere with scaffold-free growth systems.

Regulatory progress has intensified focus on ancillary materials. Following Wacker Chemie launching food-grade growth factors in November 2025, defoamers used in serum-free and animal-component-free media are now under direct regulatory scrutiny. Suppliers must demonstrate either complete removal during processing or toxicological safety in the final edible product.

Foam control economics are pivotal. Industry analyses in late 2025 consistently rank foam management among the top three technical barriers to reducing cultivated meat production costs. Advanced, non-cytotoxic defoamers directly improve volumetric productivity by preventing cell loss into foam phases, supporting the cost-down trajectories required for commercial launches across Europe and selected Asian markets.

Fermentation Defoamer Market Share and Segmentation Insights

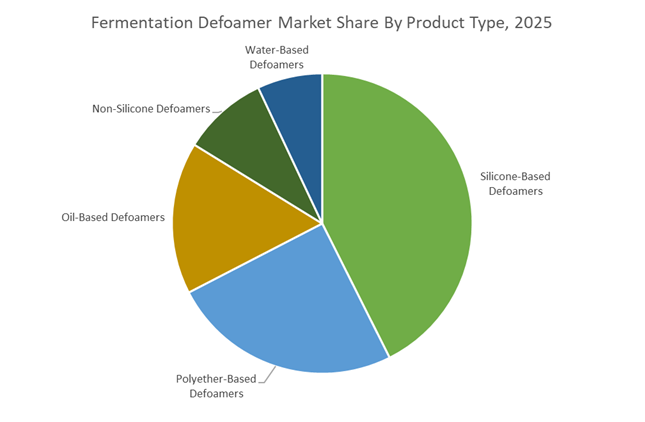

Silicone-Based Defoamers Lead Fermentation Foam Control Technologies with Superior Process Stability

Silicone-Based Defoamers accounted for 42.60% of the Fermentation Defoamer Market share in 2025, making them the most widely adopted solution for foam management in industrial fermentation systems. Their leadership stems from their high surface activity, rapid foam knockdown capability, and exceptional efficiency at extremely low dosage levels, which allows fermentation facilities to maintain stable process conditions without compromising microbial productivity. Silicone-based defoamers are particularly effective in bioreactors and fermentation tanks operating across wide pH ranges, high temperatures, and high agitation environments, where foam formation can disrupt oxygen transfer rates, microbial metabolism, and fermentation yield efficiency. In 2025, the market has seen significant innovation in food-grade and pharmaceutical-grade silicone defoamer formulations, responding to the rapid expansion of fermentation-based production in sectors such as food ingredients, probiotics, enzymes, and biopharmaceuticals. Manufacturers are developing high-purity silicone emulsions with minimal extractables, controlled particle size distribution, and improved regulatory compliance, enabling their use in FDA-compliant fermentation processes. These advanced formulations maintain strong antifoaming performance while meeting the strict purity and safety requirements demanded by the food processing, biotechnology, and pharmaceutical fermentation industries, reinforcing silicone-based defoamers as the dominant product category in the fermentation defoamer market.

Food and Beverage Fermentation Processes Drive the Largest Demand for Defoaming Technologies

Food and Beverage Processing represented 36.80% of the Fermentation Defoamer Market share in 2025, reflecting the extensive scale of fermentation-based production across the global food industry. Fermentation processes are essential for producing beer, wine, yogurt, cheese, baked goods, fermented sauces, and food ingredients such as citric acid, lactic acid, amino acids, and enzymes, all of which generate substantial foam during microbial activity and high-agitation processing stages. Excess foam can significantly reduce fermentation vessel capacity, disrupt oxygen transfer, cause contamination risks, and decrease production efficiency, making effective foam control technologies critical for industrial fermentation operations. A notable shift in 2025 is the increasing demand for clean-label compatible defoamers within food fermentation systems. Food manufacturers are seeking food-grade defoaming agents derived from edible oils, natural emulsifiers, and low-residue formulations that align with consumer expectations for minimally processed ingredients. This has driven the development of non-silicone and hybrid food-grade defoamer technologies designed to maintain strong foam suppression performance while supporting clean-label product positioning in fermented foods and beverages. As fermentation continues to expand within functional foods, plant-based products, and fermentation-derived ingredients, demand for advanced foam control solutions in the food and beverage sector remains the primary driver of the global fermentation defoamer market.

Competitive Landscape in Fermentation Defoamer market

Wacker Chemie AG Leads High-Performance Silicone Fermentation Defoamers

Wacker Chemie AG maintains a strong leadership position in the fermentation defoamer market through its SILFOAM® portfolio designed for pharmaceutical and food-grade fermentation processes. These silicone-based defoamers are available in high-active compounds and water-based emulsions, delivering effective foam suppression at extremely low dosage levels, often in the ppm range. Their formulations exhibit strong resistance to sterilization cycles such as autoclaving, a critical requirement in biotech and vaccine manufacturing. During 2025 and 2026, Wacker expanded its Asia technical center to provide localized foam-profile testing services for biopharma producers in China and India. The company also introduced silicone-free hybrid defoamers tailored for sensor-friendly bioreactors, preventing probe fouling in modern fermentation systems. With strong expertise in high-purity silicone emulsions, Wacker remains a preferred supplier for pharmaceutical fermentation and high-value biologics production.

Dow Chemical Company Expands AI-Optimized Silicone Foam Control Solutions

Dow Chemical Company leverages its global silicone manufacturing scale to supply fermentation defoamers under the DOWSIL™ and XIAMETER™ brands. Its product range spans polydimethylsiloxane fluids and polyether-modified silicone surfactants engineered for high-volume industrial fermentation. Under the Transform to Outperform initiative launched in early 2026, Dow is integrating artificial intelligence to optimize defoamer formulations and enhance production efficiency, targeting significant EBITDA improvements through digitalized operations. The company maintains strong exposure to biofuel fermentation and agricultural feed applications, where cost efficiency and bulk stability are essential. Vertical integration in silicone feedstock production provides resilience against raw material volatility observed during 2024 and 2025. Dow’s scale, digital formulation capabilities, and global distribution network reinforce its competitive strength in industrial fermentation foam control.

Evonik Industries Advances Bio-Based and Precision Fermentation Defoamers

Evonik Industries positions itself as a specialty additives leader emphasizing green transformation in fermentation processing. Its TEGO® Antifoam range includes biodegradable and bio-based defoamers derived from vegetable oil and advanced polyether chemistries. In 2025, Evonik commissioned a new specialty silicone production line to support the rapidly expanding precision fermentation and synthetic biology segments. The company aims for more than 50% of sales to originate from sustainability-advantaged products by 2026, reflecting strong alignment with global environmental standards. Evonik’s surface science expertise allows its fermentation defoamers to enhance gas-liquid mass transfer efficiency, which can improve oxygen transfer rates and overall batch yield. This dual functionality of foam suppression and process optimization strengthens its standing in high-performance industrial biotechnology applications.

Shin-Etsu Chemical Focuses on High-Purity and Regulatory-Compliant Defoamers

Shin-Etsu Chemical Co., Ltd. is a dominant player in the Asia-Pacific fermentation defoamer market, recognized for high-purity silicone additives and strict regulatory compliance. Its KM and KS series silicone defoamers are widely used in dairy fermentation, brewing, and wine production where sensory integrity is critical. The company also offers solid-type defoamers under the AWA CATCHER® brand for continuous drainage and wastewater management associated with fermentation plants. Recent development of fluorosilicone-based agents addresses extreme pH and temperature environments where conventional silicones may degrade. Shin-Etsu’s food-grade defoamers meet Japan’s Food Sanitation Law and international FDA standards, reinforcing trust among beverage and dairy producers. Its technical precision and compliance-driven approach sustain strong regional leadership.

Momentive Performance Materials Targets Specialty and PFAS-Free Fermentation Solutions

Momentive Performance Materials focuses on specialty-first silicone defoamers for pharmaceutical fermentation and high-density cell culture systems. Its SAG™ and Niax™ brands include antifoam compounds suitable for non-aqueous fermentation systems and complex biologics manufacturing. In 2025, the company strengthened local supply chains in Europe and North America to reduce lead times for pharmaceutical clients. Momentive transitioned to PFAS-free processing aids such as Silquest™ PA-1, anticipating tightening global regulations on persistent fluorinated chemicals. A strong partnership model enables co-development of customized defoamer-surfactant packages for contract development and manufacturing organizations. This collaborative, high-value approach reinforces Momentive’s position in specialty fermentation defoamers and advanced bioprocessing environments.

BASF SE Integrates Polyether Defoamers Within Its Low-Emission Production Network

BASF SE remains a key supplier in the European fermentation defoamer market, leveraging its integrated Verbund production model for cost efficiency and raw material optimization. The company emphasizes polyether-polyol defoamers that generate minimal residue on stainless steel surfaces, reducing clean-in-place time and operational downtime in fermentation facilities. Despite broader economic pressures, BASF’s Nutrition and Care segment is projected to strengthen earnings in 2026 through increased demand for bio-derived ingredients. The startup of the Zhanjiang Verbund site in China during late 2025 establishes a low-emission production benchmark for Asian markets. In 2026, BASF introduced water-based defoamer emulsions offering 10 to 15% lower total cost of ownership compared to conventional silicone oils. This blend of sustainability focus, process efficiency, and integrated production reinforces BASF’s competitive relevance in fermentation foam control solutions.

China: Intelligent Blending Scale Meets Feed and Pet Nutrition Regulation

China’s fermentation defoamer landscape in 2025–2026 is being reshaped by the convergence of world-scale blending capacity, stricter hygienic regulation, and AI-driven process control. A pivotal inflection point was reached in early 2025 when Adisseo, a subsidiary of Sinochem, achieved full operational ramp-up of its 37KT specialty blending facility in Nanjing. The site is optimized for precision-engineered defoamer premixes used in large amino acid and enzyme fermenters, leveraging advanced liquid-solid mixing to ensure uniform antifoam performance under high shear and elevated temperatures. This scale positions China to internalize defoamer supply for its expanding fermentation chemicals and feed additives ecosystem.

Regulatory pressure is accelerating formulation upgrades. In August 2025, the Ministry of Agriculture and Rural Affairs enforced mandatory hygienic standards for pet feed, compelling producers to transition toward food-grade silicone defoamers with tighter microbial and contaminant controls. Parallel sustainability mandates are also reshaping operations. The Shanghai Chemical Industry Park confirmed that major defoamer units operated by BASF and Evonik are now powered by 100% renewable electricity. At the process level, manufacturers in the Zhejiang cluster have begun deploying AI platforms from Arsenale Bioyards to automate defoamer dosing. By predicting foam criticality in real time, these systems are reducing chemical overuse by an estimated 15%, improving both cost efficiency and fermentation yields.

India: BioE3-Led Scale-Up and Biofuel Fermentation Demand

India’s fermentation defoamer market is entering a scale-up phase driven by policy-backed biomanufacturing and expanding biofuel infrastructure. The BioE3 Policy moved into active implementation in early 2025, with the Department of Biotechnology launching biofoundries and biomanufacturing hubs that provide fiscal support for bio-based surfactants and defoamers. These hubs are accelerating the adoption of vegetable oil-based and non-silicone defoamers tailored for sustainable fermentation in dairy, brewing, and enzyme production.

Industrial investment is reinforcing this trajectory. In July 2025, Fine Organic Industries announced the acquisition of specialized acreage for a new manufacturing base designed to produce non-silicone defoamers for domestic dairy and alcoholic beverage fermentations. Demand is further amplified by India’s aggressive bioethanol push. Under the National Bioenergy Programme, more than ₹908 crore was allocated in 2024–2025 to second-generation ethanol projects. These high-temperature, high-solids fermentations require defoamers that preserve gas-liquid mass transfer without fouling equipment, elevating the role of thermally stable, low-residue antifoam formulations.

United States: Regulatory Preference and Biopharma Automation

In the United States, fermentation defoamers are increasingly shaped by regulatory preference for safer chemistries and the rapid automation of biopharmaceutical fermentation. In August 2025, Kao Corporation inaugurated its tertiary amine facility in Pasadena, Texas, securing domestic supply of intermediates essential for polyether-modified silicone defoamers. These materials are critical in U.S. biopharma and agrochemical fermentations where consistency and low extractables are mandatory.

Policy alignment is reinforcing this shift. Following the 2026 EPA regulatory cycle, industrial fermenters are transitioning toward defoamers certified under the Safer Choice program, accelerating innovation in biodegradable and VOC-free formulations. Capital investment in precision fermentation is also driving sophisticated defoaming protocols. In April 2025, DSM-Firmenich opened a new precision fermentation facility in the Kansas Animal Health Corridor. The site integrates automated defoaming systems to maximize yields of fermented proteins and enzymes, underscoring how defoamers are becoming digitally managed inputs rather than commodity process aids.

Germany: High-Purity Requirements Under REACH and Biological Crop Protection

Germany’s fermentation defoamer market is increasingly defined by ultra-high purity requirements and regulatory foresight. BASF is scheduled to commission its Inscalis biofactory at Ludwigshafen in the second half of 2025, producing fermentation-derived building blocks for biological crop protection. These sensitive fungal fermentations require low-residue, high-purity defoamers to avoid strain inhibition, elevating technical specifications well beyond conventional industrial standards.

Regulatory preparedness is equally decisive. Ahead of the 2026 REACH recast, German manufacturers including Wacker Chemie AG completed re-registration of key siloxanes, safeguarding the continued use of high-performance silicone antifoams in food-contact and fermentation applications. This proactive compliance reduces supply disruption risk and reinforces Germany’s position as a benchmark market for compliant, performance-driven defoamer technologies.

Malaysia: Sustainable Feedstocks and Regional Supply Leadership

Malaysia is consolidating its role as a sustainable feedstock hub for oil-based fermentation defoamers. In 2025, KLK OLEO expanded its fractionated methyl ester capacity to 500,000 tons annually. These esters are increasingly used as base materials for low-carbon-footprint defoamers distributed across Asia Pacific, particularly in food, bio-detergent, and industrial fermentation.

Sustainability credentials are becoming a commercial differentiator. By mid-2025, Malaysian producers achieved full traceability for palm-based defoamer feedstocks through RSPO certification. This has strengthened acceptance in European clean beauty and bio-detergent value chains, where fermentation processors increasingly require processing aids aligned with deforestation-free and low-emission sourcing standards.

Strategic Snapshot: Fermentation Defoamer Market by Country (2025–2026)

Fermentation Defoamer Market County Level Snapshot

Country

Primary Driver

Defoamer Focus

Strategic Outcome

China

AI integration and feed hygiene standards

Food-grade silicone, smart dosing

Yield optimization and regulatory compliance

India

BioE3 policy and bioethanol scale-up

Bio-based, high-temperature stable

Domestic capacity and sustainable fermentation

United States

Safer Choice regulation and biopharma

Biodegradable, automated defoamers

Precision-controlled fermentation efficiency

Germany

REACH readiness and bio-crop protection

Ultra-pure silicone antifoams

High-spec, regulation-led leadership

Malaysia

RSPO-certified feedstocks

Oil-based, low-carbon defoamers

Regional supply hub with sustainability edge

Fermentation Defoamer Market Report Scope

Fermentation Defoamer Market

Parameter

Details

Market Size (2025)

$814.3 Million

Market Size (2034)

$1053.2 Million

Market Growth Rate

2.9%

Segments

By Product Type (Silicone-Based Defoamers, Oil-Based Defoamers, Polyether-Based Defoamers, Water-Based Defoamers, Non-Silicone Defoamers), By Delivery Form (Liquid Emulsions, Powder and Granular, Concentrated Oils), By Functionality (Antifoaming Agents, Defoamers, De-Aerators), By Application (Food and Beverage Processing, Pharmaceuticals and Biotechnology, Industrial Chemicals, Biofuels, Agriculture, Wastewater Treatment)

Study Period

2019- 2025 and 2026-2034

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

Dow Inc., BASF SE, Evonik Industries AG, Wacker Chemie AG, Elkem Silicones, Shin-Etsu Chemical Co., Ltd., Clariant AG, Hydrite Chemical Co., Kao Corporation, Momentive Performance Materials, KLK Oleo, Ashland Inc., Sixin Chemical, Blackburn Chemicals Ltd, Kemira Oyj

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Fermentation Defoamer Market Segmentation

By Product Type

Silicone-Based Defoamers

Oil-Based Defoamers

Polyether-Based Defoamers

Water-Based Defoamers

Non-Silicone Defoamers

By Delivery Form

Liquid Emulsions

Powder and Granular

Concentrated Oils

By Functionality

Antifoaming Agents

Defoamers

De-Aerators

By Application

Food and Beverage Processing

Pharmaceuticals and Biotechnology

Industrial Chemicals

Biofuels

Agriculture

Wastewater Treatment

By Region

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fermentation Defoamer Industry

2. Fermentation Defoamer Market Landscape & Outlook (2026–2034)

2.1. Introduction to Fermentation Defoamer Market

2.2. Market Valuation and Growth Projections (2026–2034)

2.3. Role of Foam Control in Industrial Bioprocessing and Fermentation Efficiency

2.4. Technological Evolution in Silicone and Bio-Based Defoaming Systems

2.5. Regulatory and Environmental Compliance in Fermentation Additives

3. Innovations Reshaping the Fermentation Defoamer Market

3.1. Trend: Shift Toward Non-Silicone and Bio-Renewable Defoamer Formulations

3.2. Trend: Adoption of Automated In-Line Foam Sensing and Precision Dosing Systems

3.3. Opportunity: Specialty Defoamers for High-Viscosity Biopolymers and Lignocellulosic Fermentation

3.4. Opportunity: Non-Cytotoxic Foam Control Technologies for Cultivated Meat Production

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Process Optimization Technologies

4.3. Sustainability and Low-Emission Chemical Strategies

4.4. Market Expansion and Regional Manufacturing Investments

5. Market Share and Segmentation Insights: Fermentation Defoamer Market

5.1. By Product Type

5.1.1. Silicone-Based Defoamers

5.1.2. Oil-Based Defoamers

5.1.3. Polyether-Based Defoamers

5.1.4. Water-Based Defoamers

5.1.5. Non-Silicone Defoamers

5.2. By Delivery Form

5.2.1. Liquid Emulsions

5.2.2. Powder and Granular

5.2.3. Concentrated Oils

5.3. By Functionality

5.3.1. Antifoaming Agents

5.3.2. Defoamers

5.3.3. De-Aerators

5.4. By Application

5.4.1. Food and Beverage Processing

5.4.2. Pharmaceuticals and Biotechnology

5.4.3. Industrial Chemicals

5.4.4. Biofuels

5.4.5. Agriculture

5.4.6. Wastewater Treatment

5.5. By Region

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. South and Central America

5.5.5. Middle East and Africa

6. Country Analysis and Outlook of Fermentation Defoamer Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Fermentation Defoamer Market Size Outlook by Region (2026–2034)

7.1. North America Fermentation Defoamer Market Size Outlook to 2034

7.1.1. By Product Type

7.1.2. By Delivery Form

7.1.3. By Functionality

7.1.4. By Application

7.1.5. By Region

7.2. Europe Fermentation Defoamer Market Size Outlook to 2034

7.2.1. By Product Type

7.2.2. By Delivery Form

7.2.3. By Functionality

7.2.4. By Application

7.2.5. By Region

7.3. Asia Pacific Fermentation Defoamer Market Size Outlook to 2034

7.3.1. By Product Type

7.3.2. By Delivery Form

7.3.3. By Functionality

7.3.4. By Application

7.3.5. By Region

7.4. South America Fermentation Defoamer Market Size Outlook to 2034

7.4.1. By Product Type

7.4.2. By Delivery Form

7.4.3. By Functionality

7.4.4. By Application

7.4.5. By Region

7.5. Middle East and Africa Fermentation Defoamer Market Size Outlook to 2034

7.5.1. By Product Type

7.5.2. By Delivery Form

7.5.3. By Functionality

7.5.4. By Application

7.5.5. By Region

8. Company Profiles: Leading Players in the Fermentation Defoamer Market

8.1. Dow Inc.

8.2. BASF SE

8.3. Evonik Industries AG

8.4. Wacker Chemie AG

8.5. Elkem Silicones

8.6. Shin-Etsu Chemical Co., Ltd.

8.7. Clariant AG

8.8. Hydrite Chemical Co.

8.9. Kao Corporation

8.10. Momentive Performance Materials

8.11. KLK Oleo

8.12. Ashland Inc.

8.13. Sixin Chemical

8.14. Blackburn Chemicals Ltd

8.15. Kemira Oyj

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Fermentation Defoamer Market Segmentation

By Product Type

Silicone-Based Defoamers

Oil-Based Defoamers

Polyether-Based Defoamers

Water-Based Defoamers

Non-Silicone Defoamers

By Delivery Form

Liquid Emulsions

Powder and Granular

Concentrated Oils

By Functionality

Antifoaming Agents

Defoamers

De-Aerators

By Application

Food and Beverage Processing

Pharmaceuticals and Biotechnology

Industrial Chemicals

Biofuels

Agriculture

Wastewater Treatment

By Region

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

The global Fermentation Defoamer market is projected to grow from $814.3 million in 2025 to $1,053.2 million by 2034, expanding at a CAGR of 2.9%. Growth is closely tied to the rapid expansion of industrial fermentation in biofuels, pharmaceuticals, food ingredients, and enzyme production. As fermentation capacity scales and continuous bioprocessing increases, effective foam control technologies are becoming critical for maintaining oxygen transfer efficiency, process stability, and product yield.

The primary driver is the global expansion of large-scale fermentation infrastructure, particularly in biotechnology, enzyme production, and bio-based chemicals. Foam formation in fermenters can reduce oxygen transfer rates, contaminate exhaust systems, and disrupt microbial growth. Advanced defoamers such as silicone emulsions, polyether-modified antifoams, and bio-based oil defoamers are increasingly used to maintain stable fermentation performance and optimize productivity.

Silicone-based defoamers dominate the market, accounting for more than 42% of global demand in 2025 due to their strong surface activity, rapid foam knockdown, and effectiveness at very low dosage levels. These defoamers perform reliably under high temperature, extreme pH, and high aeration conditions, making them ideal for large industrial bioreactors used in pharmaceuticals, enzymes, and fermentation-derived chemicals.

The food and beverage fermentation sector represents the largest application segment, driven by production of beer, dairy cultures, enzymes, amino acids, and organic acids. The biopharmaceutical industry is another major consumer, where foam control directly affects cell culture viability and batch success rates. Growing fermentation in biofuels, wastewater treatment, and specialty chemicals is further expanding market demand.

Key players include Dow Inc., BASF SE, Evonik Industries, Wacker Chemie AG, Shin-Etsu Chemical, Momentive Performance Materials, Clariant AG, Kemira Oyj, and Kao Corporation. These companies focus on high-purity silicone defoamers, bio-based antifoams, and sensor-compatible formulations designed for automated fermentation systems and regulated bioprocessing environments.